Exercise 8-19 (10 minutes)

Jan. 1

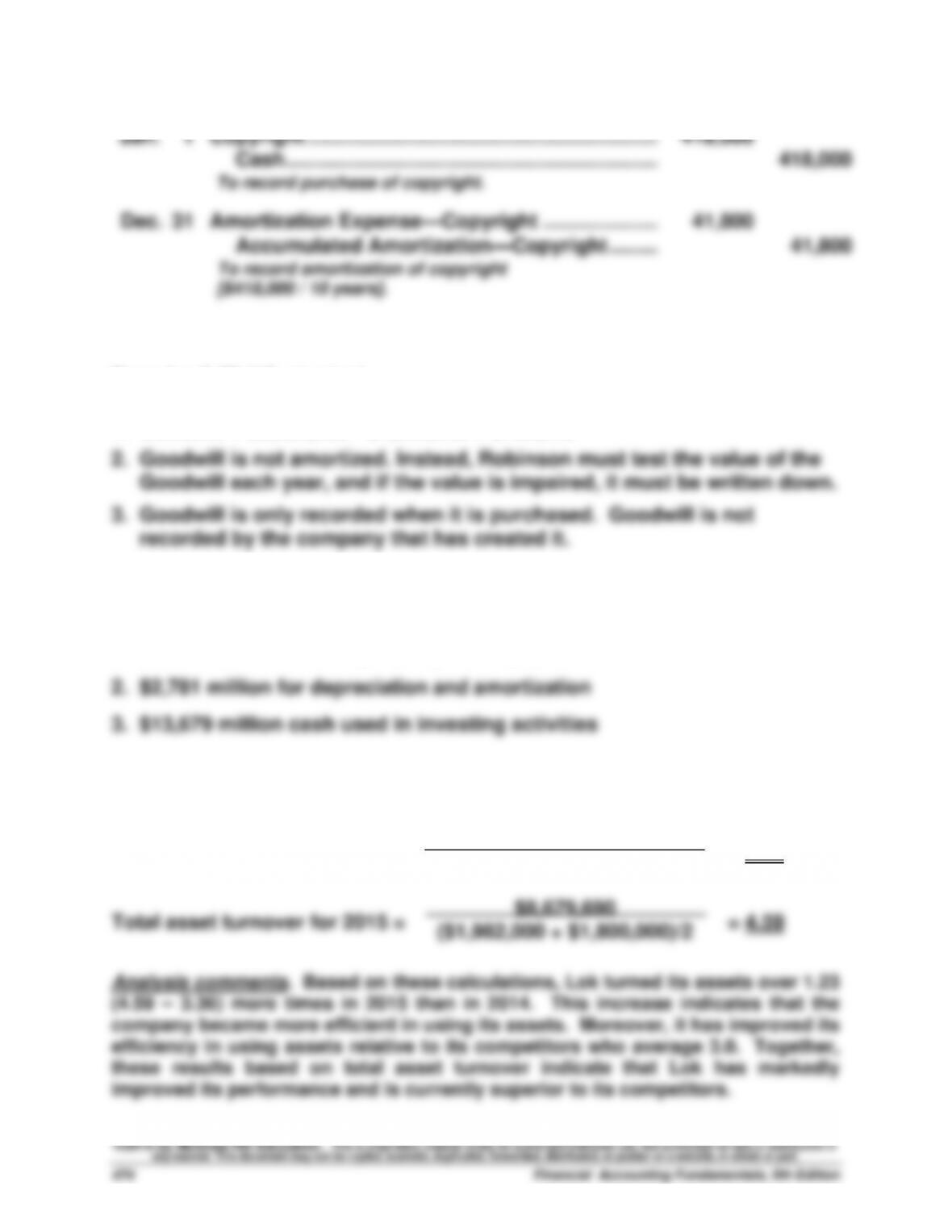

Copyright ……………………………………………………….

418,000

Cash…………………………..……………………………..…….

418,000

To record purchase of copyright.

Dec. 31

Amortization Expense—Copyright ……………………….

41,800

Accumulated Amortization—Copyright …………….

41,800

To record amortization of copyright

[$418,000 / 10 years].

Exercise 8-20 (10 minutes)

1. Goodwill = $2,500,000 – $1,800,000 = $700,000

Exercise 8-21 (15 minutes)

1. $7,358 million cash for property and equipment

Exercise 8-22 (15 minutes)

Total asset turnover for 2014 = = 3.36

$5,856,480

($1,800,000 + $1,686,000)/2

Exercise 8-23A (15 minutes)

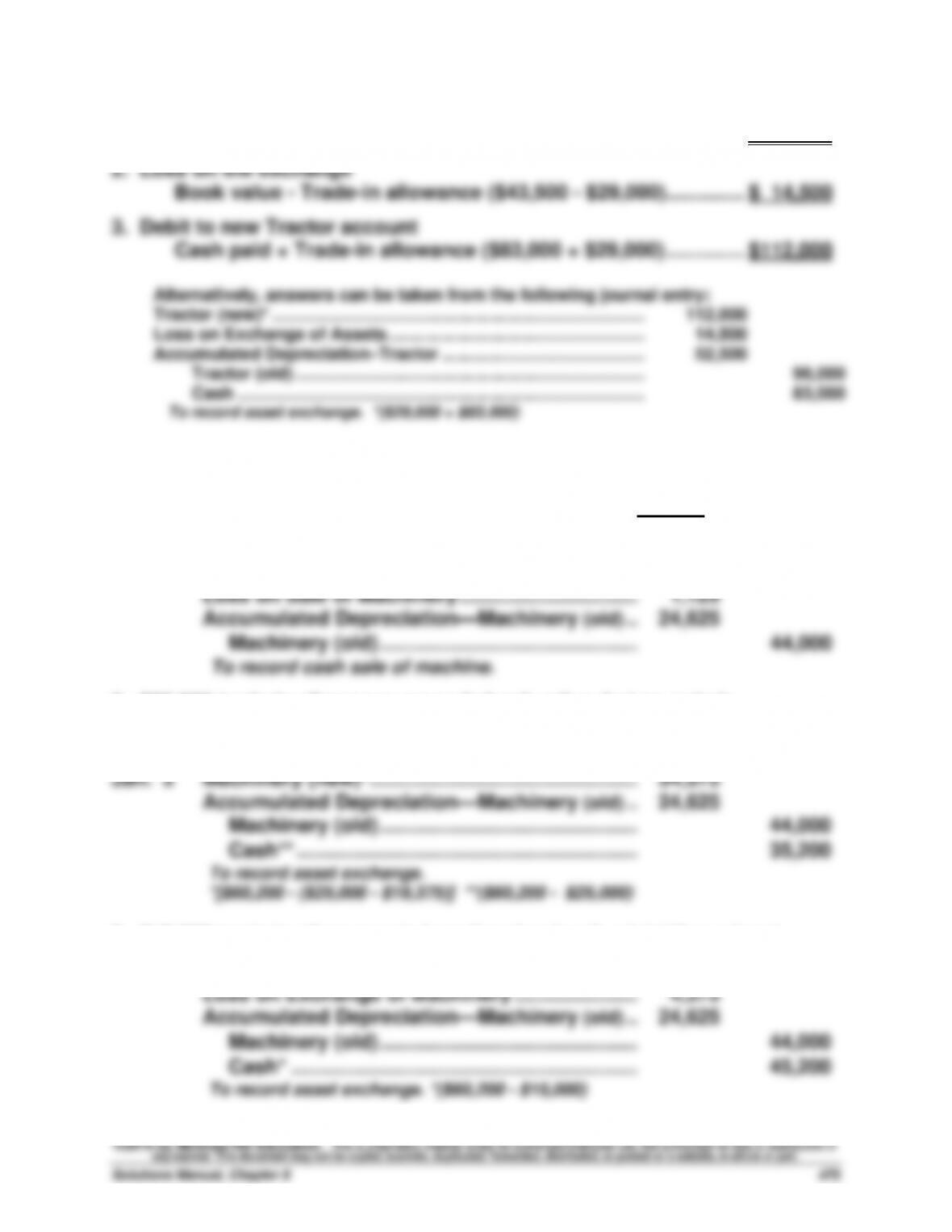

1. Book value of the old tractor ($96,000 – $52,500) …………………….. $ 43,500

Exercise 8-25 (20 minutes)

(Amounts for this exercise are in euros millions)

1.

Depreciation expense …………………………………………….

6,689

Accumulated depreciation—Property, plant

and equipment……………………………………………..

6,689

To record depreciation on property, plant and

equipment.

2.

Property, plant and equipment ……………………………….

11,061

Cash ……………………………………………………………….

11,061

To record betterments (improvements) on property,

plant and equipment.

3.

Cash …………………………..…………………………………………

700

Loss on disposal of property, plant and equipment ..

500

Accumulated Depreciation—Property, plant and

equipment …………………………………………………………..

1,162

Property, plant and equipment …………………………

2,362

To record asset disposals.

4. Volkswagen would decrease its property, plant and equipment account

by €118 at December 31, 2013, for its 2013 total impairments.

PROBLEM SET A

Problem 8-1A (50 minutes)

Part 1

Estimated

Market Value

Percent

of Total

Apportioned

Cost

Building ……………………..

$508,800

53%

$477,000

Land ………………………….

297,600

31

279,000

Land improvements ……

28,800

3

27,000

Vehicles …………………….

124,800

13

117,000

Total ………………………….

$960,000

100%

$900,000

2015

Jan. 1

Building …………………………………………………….…

477,000

Land ……………………………………………………………………..

279,000

Land Improvements …………………………………..…………..

27,000

Vehicles ……………………………………………………….

117,000

Cash …………………………..……………………….….

900,000

To record asset purchases.

Part 2

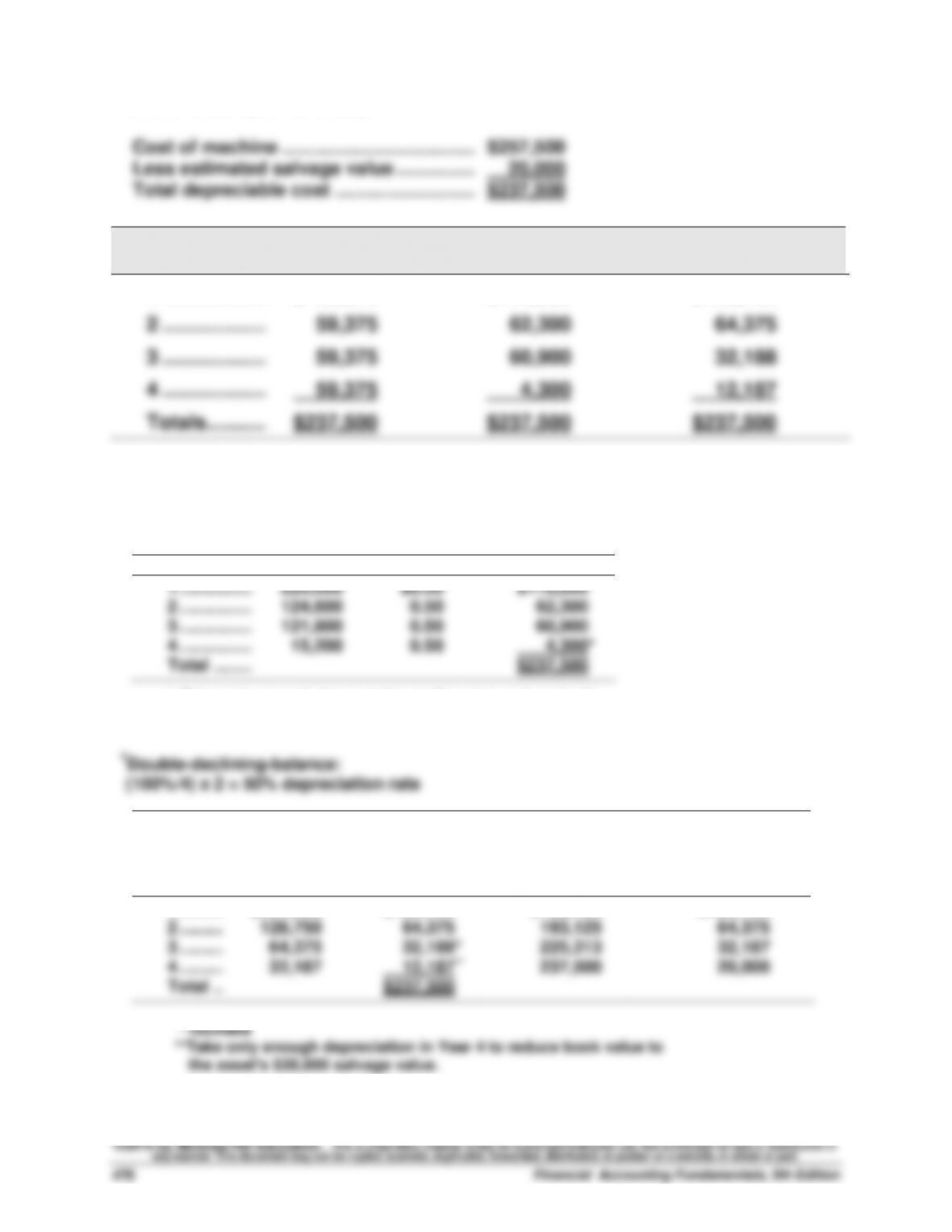

Year 2015 straight-line depreciation on building

Part 3

Year 2015 double-declining-balance depreciation on land improvements

Part 4

Accelerated depreciation does not lower the total amount of taxes paid over

the asset’s life. Instead, it defers or postpones taxes to the later years of an

Problem 8-2A (25 minutes)

Problem 8-3A (45 minutes)

Part 1

Land

Building

2

Building

3

Land

Improve-

ments 1

Land

Improvements

2

Purchase price* ……….………

$1,612,000

$598,000

$390,000

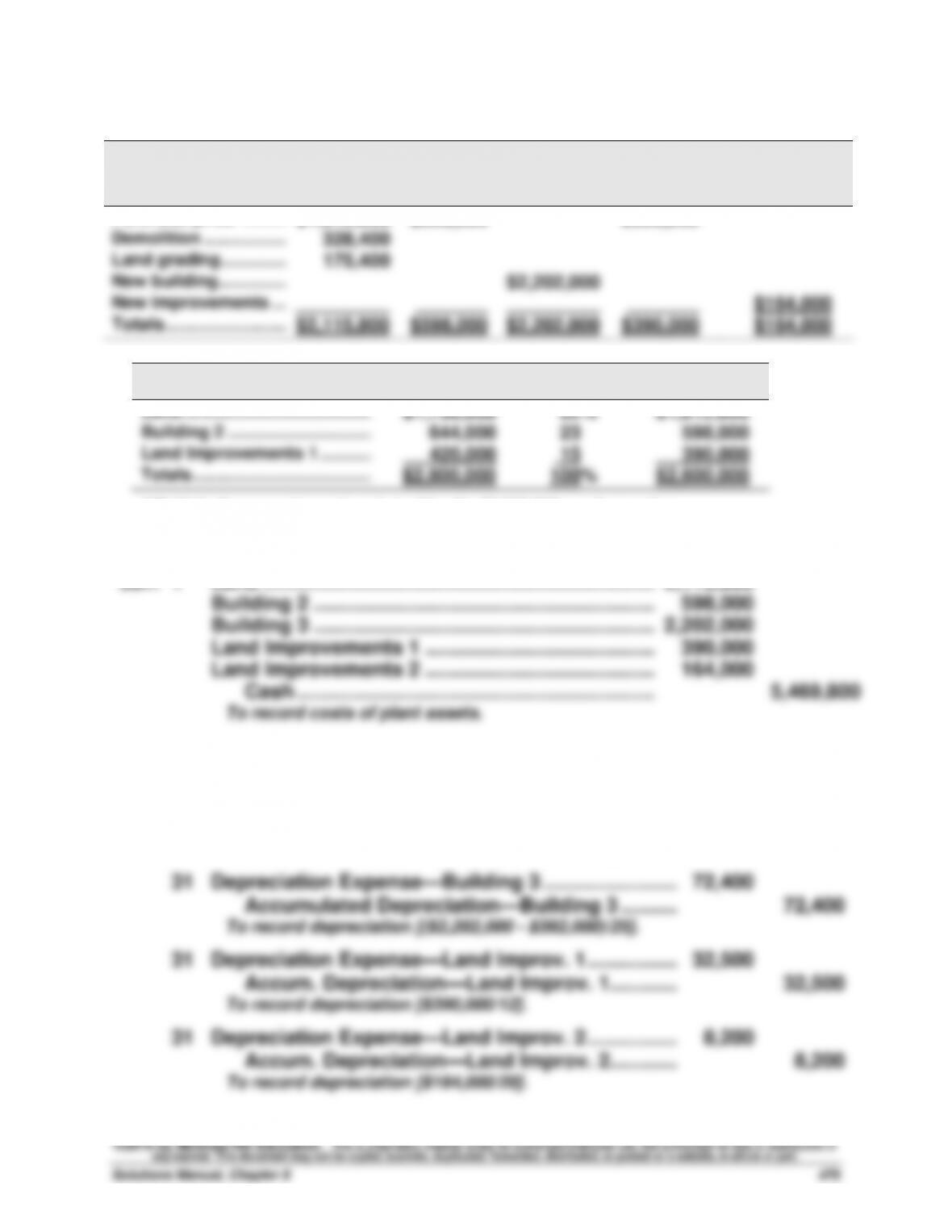

Demolition ………………………

328,400

Land grading …………..………

175,400

New building……………………

$2,202,000

New improvements ….………

_________

_______

_________

_______

$164,000

Totals …………………………..

$2,115,800

$598,000

$2,202,000

$390,000

$164,000

*Allocation of purchase price

Appraised

Value

Percent

of Total

Apportioned

Cost**

Land …………………………………..

$1,736,000

62%

$1,612,000

Building 2 …………………………..

644,000

23

598,000

Land Improvements 1 ………....

420,000

15

390,000

Totals ………………………………...

$2,800,000

100%

$2,600,000

**Multiply the percentages in column 3 by the $2,600,000 purchase price.

Part 2

2015

Jan. 1

Land …………………………………………………………….

2,115,800

Building 2 …………………………………………………….

598,000

Building 3 …………………………………………………….

2,202,000

Land Improvements 1 …………………………………..

390,000

Land Improvements 2 …………………………………..

164,000

Cash ……………………………………………………….

5,469,800

To record costs of plant assets.

Part 3

2015

Dec. 31

Depreciation Expense—Building 2 …………………….…..

26,900

Accumulated Depreciation—Building 2 ………..…..

26,900

To record depreciation [($598,000 – $60,000)/20].

Depreciation Expense—Building 3 …………………….…..

72,400

Accumulated Depreciation—Building 3 ………..…..

72,400

To record depreciation [($2,202,000 – $392,000)/25].

Depreciation Expense—Land Improv. 1 ……………..…..

32,500

Accum. Depreciation—Land Improv. 1 ………….…..

32,500

To record depreciation [$390,000/12].

Depreciation Expense—Land Improv. 2 ……………..…..

Accum. Depreciation—Land Improv. 2 ………….…..

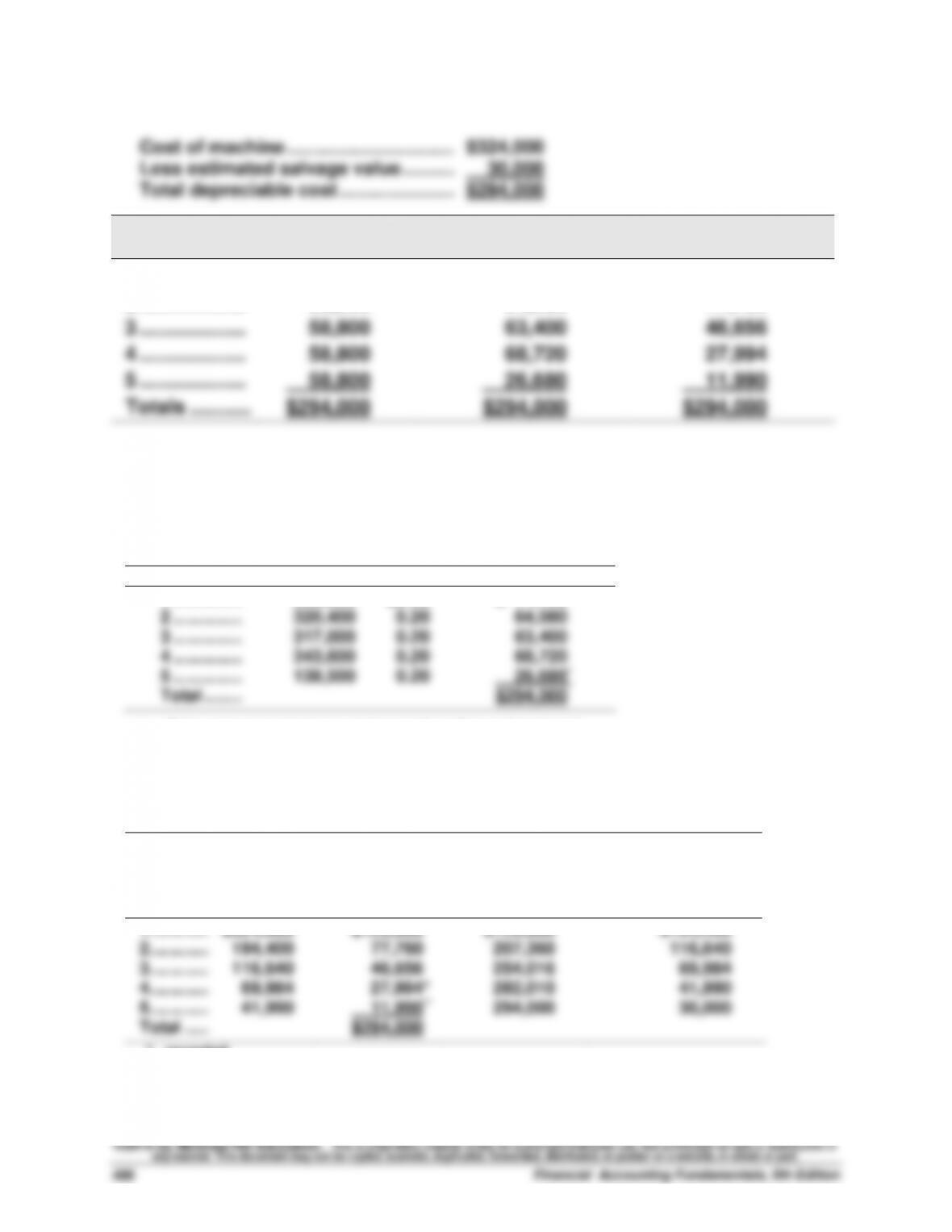

Problem 8-4A (50 minutes)

2014

Jan. 1

Equipment ……………………………………………………....

300,600

Cash …………………………………………………………...

300,600

To record loader costs ($287,600 +$11,500 +$1,500).

Jan. 3

Equipment ……………………………………………………….

4,800

Cash ………………………………………………………….…..

4,800

To record betterment of loader.

To record depreciation.

Jan. 1

Equipment ……………………………………………………….

5,400

Cash ………………………………………………………….…..

5,400

To record extraordinary repair on loader.

Cash ………………………………………………………….…..

To record ordinary repair on loader.

Problem 8-5A (40 minutes)

2014

Jan. 1

Trucks ………………………………………………………………...

22,000

Cash ……………………………………………………………...

22,000

To record cost of truck ($20,515 + $1,485).

To record depreciation [($22,000 – $2,000)/5].

To record depreciation.

To record sale of truck.

Problem 8-6A (20 minutes)

1.

Jan. 2

Machinery ……………………………………………………….

178,000

Cash …………………………..……………………………...

178,000

To record machinery purchase.

Jan. 3

Machinery ……………………………………………………….

2,840

Cash …………………………..……………………………...

2,840

To record machinery costs.

Jan. 3

Machinery ……………………………………………………….

1,160

Cash …………………………..……………………………...

1,160

To record machinery costs.

2. a. First year

Dec. 31

Depreciation Expense—Machinery ………………….……

28,000

Accumulated Depreciation—Machinery ……..……

28,000

To record depreciation [($182,000 – $14,000)/6].

b. Fifth year

Dec. 31

Depreciation Expense—Machinery ………………….……

28,000

Accumulated Depreciation—Machinery ……..……

28,000

To record year’s depreciation.

3. Accumulated depreciation at the date of disposal

Five years’ depreciation (5 x $28,000) …………………....

$140,000

Book value at the date of disposal

Original total cost ………………………………………………...

$182,000

Accumulated depreciation …………………………………....

(140,000)

Book value …………………………………………………………..

$ 42,000

a. Sold for $15,000 cash

Dec. 31

Cash ……………………………………………………………..…….

15,000

Loss on Sale of Machinery …………………………….…….

27,000

Accumulated Depreciation—Machinery ………….…….

140,000

Machinery ……………………………………………………….

182,000

Dec. 31

Cash ……………………………………………………………..…….

50,000

Accumulated Depreciation—Machinery ………….…….

140,000

Machinery ……………………………………………………….

182,000

Gain on Sale of Machinery …………………………..

8,000

Dec. 31

Cash ……………………………………………………………..…….

30,000

Accumulated Depreciation—Machinery ………….…….

140,000

Loss from Fire ……………………………………………….…….

12,000

Problem 8-7A (20 minutes)

a.

July 23

Mineral Deposit …………………………..…………….…………

4,715,000

Cash ……………………………………………………….

4,715,000

To record purchase of mineral deposit.

b.

July 25

Machinery ……………………………………………………….

410,000

Cash ……………………………………………………….

410,000

To record costs of machinery.

c.

Dec. 31

Depletion Expense—Mineral Deposit ……………………

441,600

Accum. Depletion—Mineral Deposit ……..…………

441,600

To record depletion [$4,715,000/

5,125,000 tons = $0.92 per ton.

480,000 tons x $0.92 = $441,600].

d.

Dec. 31

Depreciation Expense—Machinery …………….…………

38,400

Accum. Depreciation—Machinery ………..…………

38,400

To record depreciation [$410,000/

5,125,000 tons = $0.08 per ton.

480,000 tons x $0.08 = $38,400].

Analysis Component

Similarities—Amortization, depletion, and depreciation are similar in that

Problem 8-8A (20 minutes)

1.

2015

(a)

June 25

Leasehold ……………………………………………………....

200,000

Cash ………………………………………………………..…….

200,000

To record payment for sublease.

(b)

July 1

Prepaid Rent………………………………………………….……

80,000

Cash ………………………………………………………..…….

80,000

To record prepaid annual lease rental.

(c)

July 5

Leasehold Improvements …………………………………….

130,000

Cash ………………………………………………………..…….

130,000

To record costs of leasehold improvements.

2.

2015

(a)

Dec. 31

Rent Expense ………………………………………………..…….

10,000

Accumulated Amortization—Leasehold …….…….

10,000

To record leasehold amortization ($200,000/10 x 6/12).

(b)

Dec. 31

Amortization Expense—Leasehold Improvements ….…….

6,500

Accumulated Amortization—Leasehold

Improvements …………………………………………….……..

6,500

To record leasehold improvement amortization

($130,000/10 years remaining on lease x 6/12).

(c)

Dec. 31

Rent Expense ………………………………………………..…….

40,000

Prepaid Rent ………………………………………………….

40,000

To record one-half year lease rental ($80,000 x 6/12).

PROBLEM SET B

Problem 8-1B (50 minutes)

Part 1

Estimated

Market Value

Percent

of Total

Apportioned

Cost

Building ……………………..

$ 890,000

50%

$ 900,000

Land …………………………..

427,200

24

432,000

Land improvements ……

249,200

14

252,000

Trucks ………………………..

213,600

12

216,000

Total …………………………..

$1,780,000

100%

$1,800,000

2015

Jan. 1

Buildings ……………………………………………..………..

900,000

Land …………………………………………………….…

432,000

Land Improvements ……………………………..……………….

252,000

Trucks ………………………………………………….……

216,000

Cash ……………………………………………….………

1,800,000

To record asset purchases.

Part 2

Year 2015 straight-line depreciation on building

Part 3

Year 2015 double-declining-balance depreciation on land improvements

Part 4

Accelerated depreciation does not increase the total amount of taxes paid

over the asset’s life. Instead, it defers or postpones taxes to the later years of

Problem 8-2B (25 minutes)

Problem 8-3B (45 minutes)

Part 1

Land

Building

B

Building

C

Land

Improve-

ments B

Land

Improve-

ments C

Purchase price* ……….

$ 868,000

$527,000

$155,000

Demolition ………………

122,000

Land grading …………..

174,500

New building……………

$1,458,000

New improvements ….

_________

_______

_________

_______

$103,500

Totals ……………………..

$1,164,500

$527,000

$1,458,000

$155,000

$103,500

Allocation of

purchase price

Appraised

Value

Percent

of Total

Apportioned

Cost

Land …………………………………..

$ 795,200

56%

$ 868,000

Building B …………………………..

482,800

34

527,000

Land Improvements B ……..…..

142,000

10

155,000

Totals …………………………….…..

$1,420,000

100%

$1,550,000

Part 2

2015

Jan. 1

Land ……………………………………………………………….

1,164,500

Building B……………………………………………………….

527,000

Building C……………………………………………………….

1,458,000

Land Improvements B ……………………………………..

155,000

Land Improvements C ……………………………………..

103,500

Cash ………………………………………………………….

3,408,000

To record cost of plant assets.

Part 3

2015

Dec. 31

Depreciation Expense—Building B …………………….…….

28,500

Accumulated Depreciation—Building B ……………………..

28,500

To record depreciation [($527,000 – $99,500)/15].

Depreciation Expense—Building C ……………………...

60,000

Accumulated Depreciation—Building C …………..

60,000

To record depreciation [($1,458,000 – $258,000)/20].

31,000

31,000

10,350

10,350