Problem 6-5B (Concluded)

Part 3

(1) Some of the checks in the numbered sequence may have cleared the

(2) Some of the checks in the numbered sequence may remain

(3) The issuer of the checks may have voided one or more of the checks

(4) Occasionally, a check will reach the bank but the bank will incorrectly

SERIAL PROBLEM — SP 6

Serial Problem — SP 6, Business Solutions (50 minutes)

Part 1

BUSINESS SOLUTIONS

Bank Reconciliation

March 31, 2016

Bank statement balance …..

$67,566

Book balance …………………….…….

$68,057

Add

Add

Bank error …………………………

Deposits in Transit ……………

500

0

Bank interest …………………..………

33

______

68,066

68,090

Deduct

Deduct

Outstanding Check ………....

128

Safety deposit rental $ 50

______

Charge for checks … 102

152

Adjusted bank balance …….

$67,938

Adjusted book balance ……..……………………

$67,938

Part 2

Mar. 25

Miscellaneous Expenses …………………………….……….

677

50

Cash ……………………………………………………....

101

50

To record safety deposit box rental.

26

Miscellaneous Expenses …………………………….……….

677

102

Cash ……………………………………………………....

101

102

To record charge for printing checks

31

Cash …………………………………………………………..……….

101

33

Interest Revenue …………………………………..……….

404

33

To record interest earned.

Reporting in Action — BTN 6-1

1.

($ in millions)

Balance

September

28, 2013

Cash and

equivalents

as % of:

Balance

September

29, 2012

Cash and

equivalent

s as % of:

Cash and cash

equivalents ……………

$ 14,259

—

$ 10,746

—

Current assets ………..

73,286

19.5%

57,653

18.6%

Current liabilities …….

43,658

32.7

38,542

27.9

Shareholders’ equity .

123,549

11.5

118,210

9.1

Total assets …………….

207,000

6.9

176,064

6.1

2. Per the statement of cash flows for year ended September 28, 2013

($ millions):

Cash and equivalents, beginning-year …………… $10,746

Cash and equivalents, year-end ……………………… $14,259

Reporting in Action (Concluded)

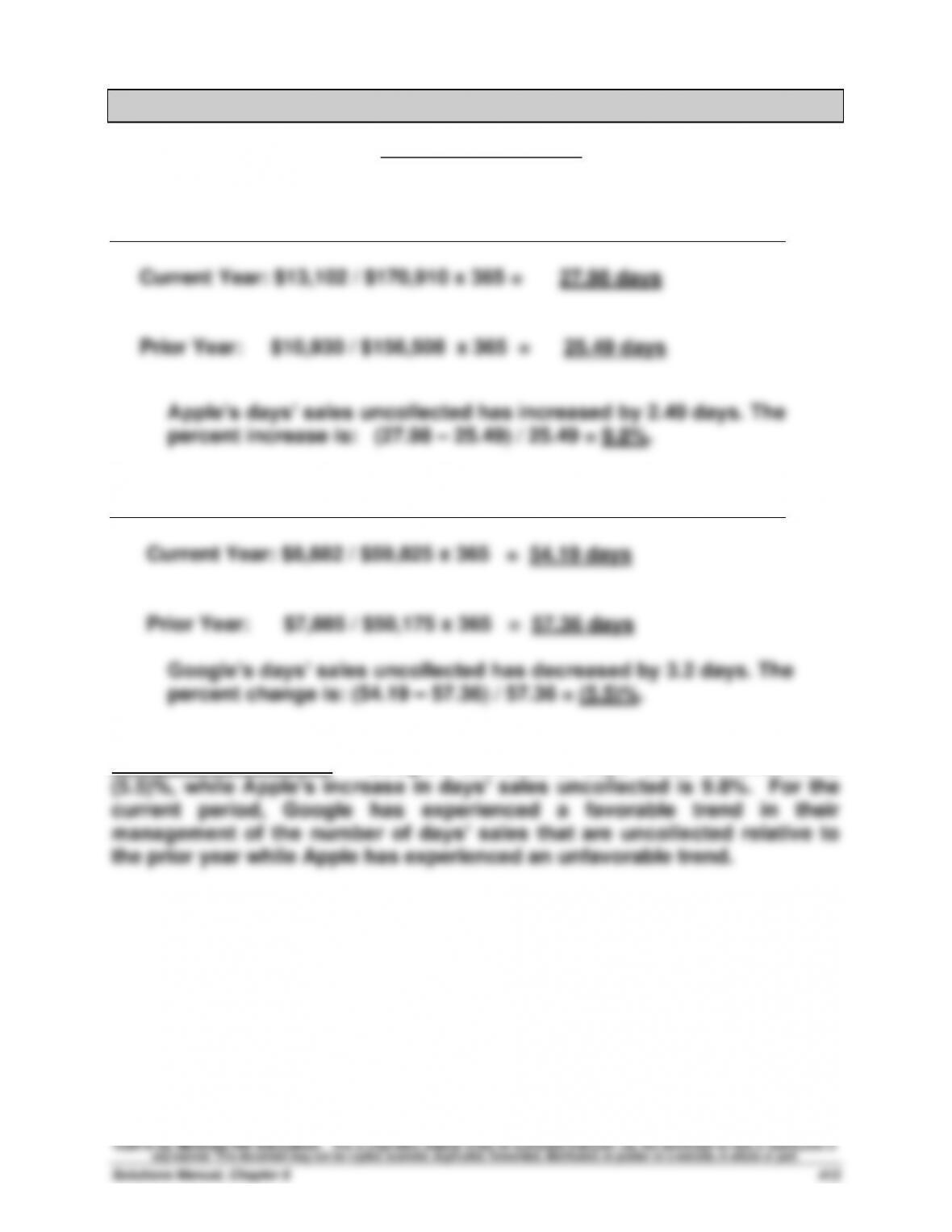

3. Days’ Sales Uncollected ($ thousands)

Days’ sales uncollected = x 365

The number of days of uncollected sales in accounts receivable has

4. Solution depends on the annual report information obtained.

Accounts receivable

Net sales

Comparative Analysis — BTN 6-2

Days’ sales uncollected = x 365

Apple ($ millions)

Google ($ millions)

Comparative Analysis: Google’s decrease in days’ sales uncollected is

Accounts receivable

Net sales

Ethics Challenge — BTN 6-3

1. In a small business office it is very important that the owner of the

2. Unfortunately, due to collusion of the employees, the bank

3. Despite the collusion, the scheme is not foolproof. For example, some

ways in which the scheme might be uncovered or prevented include the

following:

• A bank employee may become suspicious and call Dr. Conrad and

4. Dr. Conrad should review her salary schedules for employees to make

sure that she is at least offering market pay. She may want to consider

Communicating in Practice — BTN 6-4B

Memorandum

To: “Owner”

From: “Consultant”

Date: __________

Subject: Advice on monitoring purchase discounts

[Instructor’s Note: The response should acknowledge the owner’s concern and

recommend the net method of recording purchases. It should explain how this method

results in the recording of “Discounts Lost,” which will flow through to the income

statement, thus providing the information desired. The memo might look something like

the following.]

Taking It to the Net — BTN 6-5

[Instructor Note: These answers were taken from the ACFE’s 2014 Report to the Nations.]

http://www.acfe.com/rttn/docs/2014-report-to-nations.pdf

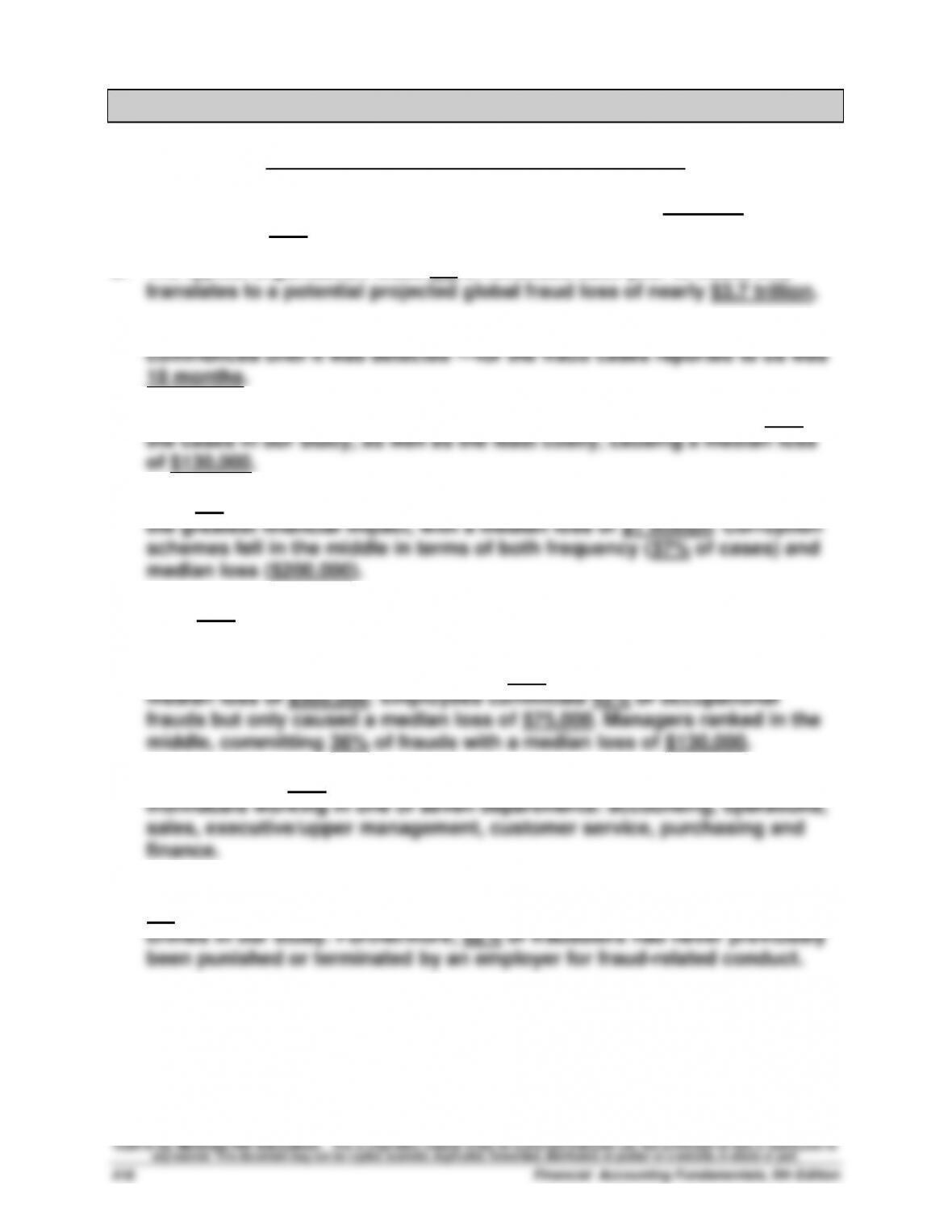

1. The median loss caused by the frauds in our study was $145,000.

Additionally, 22% of the cases involved losses of at least $1 million.

2. The typical organization loses 5% of revenues each year to fraud; this

3. The median duration — the amount of time from when the fraud

4. Asset misappropriations are the most common fraud, occurring in 85% of

5. Only 9% of cases involved financial statement fraud, but those cases had

6. Over 40% of all cases were detected by a tip — more than twice the rate of

any other detection method.

7. Owners/executives only accounted for 19% of all cases, but they caused a

8. Approximately 77% of the frauds in our study were committed by

9. The vast majority of occupational fraudsters are first-time offenders; only

5% had been convicted of a fraud-related offense prior to committing the

Teamwork in Action — BTN 6-6

Common internal controls visible in a typical retail store include:

1. Door locks and roll–down screens for after-hours lock-up.

2. Electronic detection devices stationed at entrances or anti-theft

3. Security cameras.

Entrepreneurial Decision — BTN 6-7

1. Seven principles of internal control along with examples are:

a. Establish responsibilities. The clerks at the counter should be

responsible for handling cash. The other employees should be

responsible for preparing the orders and helping customers. There

e. Divide responsibility for related transactions. The employee

responsible for ordering inventory should be separate from the

employee controlling inventory who should also be separate from

the employee who pays for inventory.

2. As the business grows, controls will become more important. The

Hitting the Road — BTN 6-8

No formal solution exists for this activity. It is usually interesting for the

class to exchange their discoveries via class discussion. This is

particularly the case with respect to popular college service/product

centers. Common controls found in college units include:

1. Door locks and roll–down screens for after-hours lock-up.

Global Decision — BTN 6-9

1.

(KRW millions)

Current

year

balance

Cash as

percent

of:

Prior

year

balance

Cash as

percent

of:

Cash (and equivalents) …………

16,284,780

—

18,791,460

—

Current assets …………..………

110,760,271

14.7%

87,269,017

21.5%

Total assets ……………….………

214,075,018

7.6

181,071,570

10.4

Current liabilities ……….………

51,315,409

31.7

46,933,052

40.0

Total equity………………..………

150,016,010

10.9

121,480,206

15.5

Analysis comment: Cash has decreased as a percent of current assets

Global Decision (Concluded)

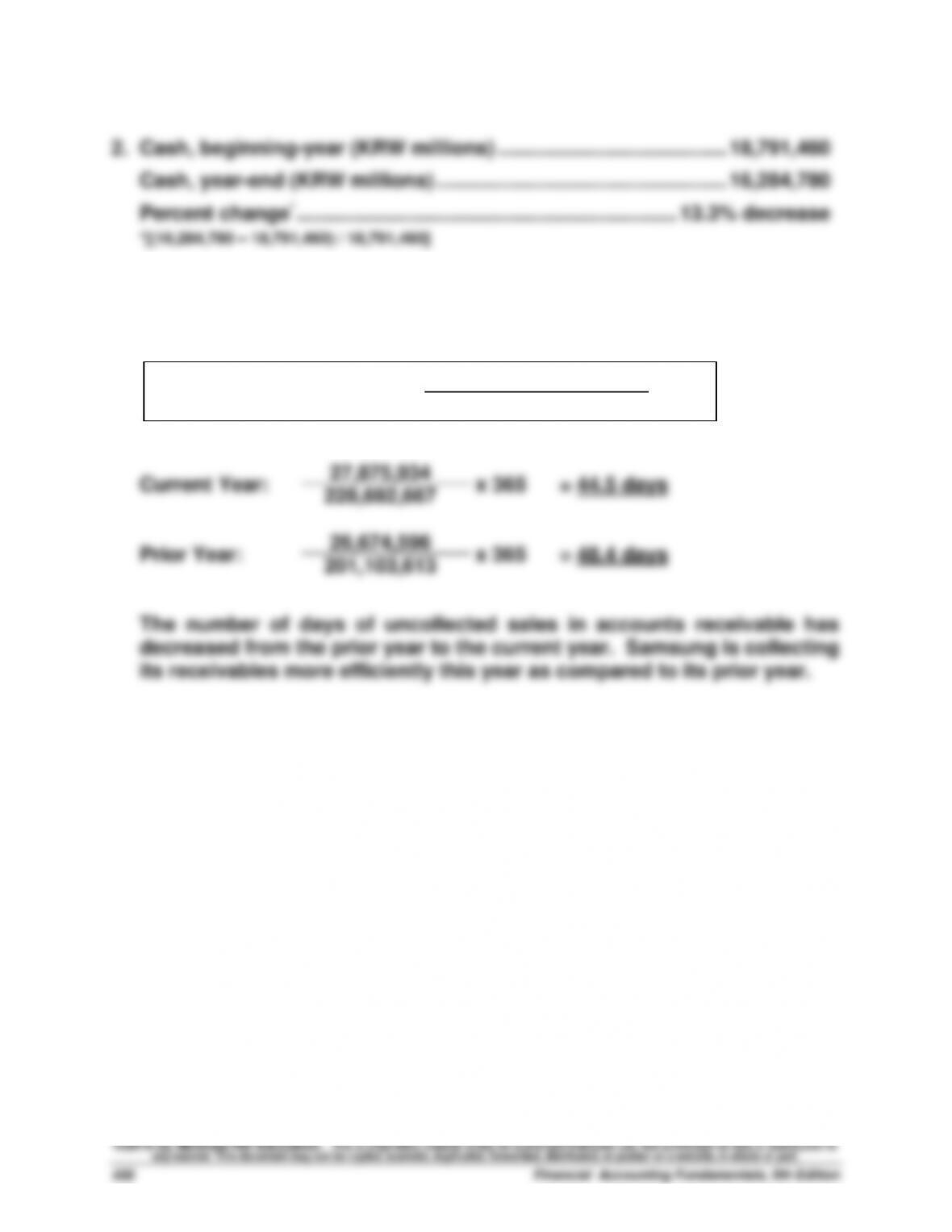

3. Days’ Sales Uncollected Formula (KRW millions)

Days’ sales uncollected = x 365

Accounts receivable

Net sales