CHAPTER 6

CASH AND INTERNAL CONTROL

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Define internal control and its

purpose and principles.

1, 2, 3, 4, 6

6-1, 6-11

6-1, 6-2

6-1

6-3, 6-5, 6-6

6-7, 6-8

C2. Define cash and cash

equivalents and explain how to

report them.

7, 10,11, 12,

13

6-2

6-3

6-1, 6-9

Analytical objectives:

A1 Compute days’ sales uncollected

ratio and use it to assess

liquidity.

6-8

6-12

6-1, 6-2, 6-9

Procedural objectives:

P1. Apply internal control to cash

receipts and disbursements.

9

6-3, 6-11

6-4, 6-7

6-5, 6-7

P2. Explain and record petty cash

fund transactions.

8

6-4

6-5, 6-6

6-2, 6-3

P3. Prepare a bank reconciliation.

6-5, 6-6, 6-7

6-8, 6-9,

6-10, 6-11

6-4, 6-5

P4A. Describe the voucher system to

control cash disbursements.

(Appendix 6A)

6-9

6-13

P5A. Apply the net method to

control purchase discounts.

(Appendix 6B)

5

6-10

6-14

6-4

*See additional information on next page that pertains to these quick studies, exercises and problems.

Additional Information on Related Assignment Material

The Serial Problem for Success Systems continues in this chapter. Problems 6-4A and 6-5A can be

completed using Excel. Problem 6-2A and 6-5A, and the Serial Problem can be completed with Sage 50

Software. Problem 6-2A can be completed with QuickBooks.

Connect reproduces assignments online, in static or algorithmic mode, which allows instructors to

monitor, promote, and assess student learning. It can be used for practice, homework, or exams.

Synopsis of Chapter Revisions

• Dandelion Chocolate: NEW opener with new entrepreneurial assignment

• New learning notes added to bank reconciliation

• New chart for timing differences for bank reconciliation

• Updated receivables analysis using Hasbro and Mattel

Chapter Outline

Notes

I. Internal Control

A. Purpose of Internal Control

An internal control system consists of policies and procedures

managers use to:

1. Protect assets.

2. Ensure reliable accounting.

3. Promote efficient operations.

4. Urge adherence to company policies.

B. Sarbanes Oxley Act (SOX)

Section 404 of SOX requires the managers and auditors of

companies whose stock is traded on an exchange (called public

companies) to document and certify the system of internal

controls.

C. Principles of Internal Control:

1. Establish responsibilities.

2. Maintain adequate records.

3. Insure assets and bond key employees.

4. Separate recordkeeping from custody of assets.

5. Divide responsibility for related transactions.

6. Apply technological controls.

7. Perform regular and independent reviews.

The Committee of Sponsoring Organizations (COSO) provides a

framework for how these principles improve the quality of

financial reporting.

D. Technology and Internal Control

Technology provides quick access to databases and information.

Examples of how technology impacts internal control:

1. Reduces processing errors.

2 Allows more extensive testing of records.

3. Limits hard copy evidence of processing steps but can

electronically store additional evidence.

4. Requires that crucial separation of responsibilities be carefully

distributed among fewer employees.

5. Increased e-commerce increases risks of credit card theft,

computer viruses and online impersonation.

E. Limitations of Internal Control

1. Human Element

a. Error: negligence, fatigue, misjudgment, r confusion

b. Fraud: opportunity, pressure, rationalization

2. Cost-benefit principle—the costs of internal controls must not

exceed their benefits.

Chapter Outline

Notes

II. Control of Cash—Basic guidelines for control of cash and cash

equivalents include: handling of cash must be separate from

recordkeeping of cash, cash receipts are promptly deposited in bank,

and disbursements of cash are by check.

A. Cash, Cash Equivalents, and Liquidity

1. Liquidity refers to a company’s ability to pay for its near term

obligations.

2. Cash includes currency and coins, deposits in bank and

checking accounts (called demand deposits), many savings

accounts (called time deposits), and items that are acceptable

for deposit in those accounts (customers checks, cashier

checks, certified checks, and money orders).

3. Cash equivalent (examples; short-term U.S. Treasury bills and

money market funds) are short-term, highly liquid investment

assets meeting two criteria:

a. Readily convertible to a known cash amount.

b. Sufficiently close to their maturity date so that market

value is not sensitive to interest rate changes.

Note: Only investments purchased within three months of

their maturity dates usually satisfy these criteria.

B. Cash Management

1. Goals of Cash Management

a. Plan cash receipts to meet cash payments when due

b. Keep minimum level of cash necessary to operate.

2. Effective cash management principles:

a. Encourage collection of receivables

b. Delay payment of liabilities until last possible day allowed

c. Keep only necessary levels of assets

d. Plan expenditures

e. Invest excess cash

C. Control of Cash Receipts

Procedures for protecting cash received over-the-counter and by

mail:

1. Apply internal control principles.

2. Record cash shortages and overages in an income statement

account called Cash Over and Short.

D. Control of Cash Disbursements

To safeguard against theft:

1. Require all expenditures be made by checks. (Exception—

small payments made from petty cash fund.)

2. Deny access to the accounting records to anyone, other than

the owner, who has authority to sign checks.

Chapter Outline

Notes

3. Use a voucher system of control that establishes procedures

for:

a. verifying, approving and recording obligations for

eventual cash disbursement.

b. issuing checks for payment of verified, approved, and

recorded obligations.

(Documents in a voucher system are listed and explained in

appendix notes)

4. Use a petty cash system of control as follows:

a. Write and cash a check to establish petty cash fund.

Record as a debit to Petty Cash and credit to Cash.

(Use the Petty Cash account only when the fund is

established or size of fund is increased or decreased.)

b. Assigning a petty cashier (custodian) to account for

the amounts expended and to keep receipts.

c. Reimbursement—debit the expenses or other items

paid for with petty cash and credit Cash for the

amount reimbursed to the petty cash fund.

d. Record any petty cash shortages/overages.

III. Banking Activities as Controls

A. Basic Bank Services

Bank accounts permit depositing money for safeguarding and

helps control withdrawals. Electronic Funds Transfer (EFT) is an

electronic communication transfer of cash from one party to

another.

B. Bank Statement

Shows activities of a bank account and is used to prove the

accuracy of the depositor’s cash records in preparing a bank

reconciliation.

1. Bank reconciliation –a report that explains (reconciles) the

difference between the balance of a checking account

according to the depositor’s records and the balance reported

on the bank statement.

2. Factors causing the bank statement balance to differ from the

depositor’s book balance are:

a. Outstanding checks.

b. Deposits in transit.

c. Deductions for uncollectible items and services

d. Additions for collections and interest.

e. Errors by either the bank or depositor

Chapter Outline

Notes

3. Steps in preparing the bank reconciliation:

a. Identify the bank balance of the cash account (balance per

bank).

b. Identify and list any unrecorded deposits (deposits in

transit) and any bank errors understating the bank balance.

Add them to the bank balance.

c. Identify and list any outstanding checks and any bank

errors overstating the bank balance. Deduct them from the

bank balance.

d. Compute the adjusted bank balance, also called corrected

or reconciled balance.

e. Identify the company’s balance of the cash account

(balance per book).

f. Identify and list any unrecorded credit memoranda from

the bank, any interest earned, and errors that understated

the book balance. Add them to the book balance.

g. Identify and list any unrecorded debit memoranda from

the bank, service charges, and errors that overstated the

book balance. Deduct them from the book balance.

h. Compute the adjusted book balance, also called corrected

or reconciled balance.

i. Verify the two adjusted balances from steps d and h are

equal. If yes, they are reconciled. If not, check for

accuracy and missing data to achieve reconciliation.

4. Adjusting entries from a bank reconciliation

a. All reconciling additions to book balance are debits to

cash. Credit depends on reason for addition (Examples:

Credit Interest Income for interest on balance and Notes

Receivable when bank collected note).

b. All reconciling subtractions from book balance are credits

to cash. Debit depends on reason for subtraction.

(Examples: Debit Miscellaneous Expense for bank service

charge and Accounts Receivable/customer for NSF

checks.).

Chapter Outline

Notes

IV Global View—Compares U.S. GAAP to IFRS

A. Internal control purposes, principles and procedures are basically

the same across the globe.

B. The definitions of cash are similar for U.S. GAAP and IFRS.

C. There is a global demand for banking services, bank statements

and bank reconciliations and bank services are a part of effective

internal control.

IV. Decision Analysis—Days’ Sales Uncollected

A. Also called days’ sales in receivables.

B. Used to evaluate the liquidity of a company; estimates how

quickly a company will convert its accounts receivable into cash.

C. Calculated by dividing current balance of accounts receivable by

net sales and multiplying the result by 365.

V. Documents in a Voucher System—Appendix 6A

Important documents of a voucher system of control include:

A. Purchase Requisition—lists the merchandise needed and requests

that it be purchased.

B. Purchase Order—used by purchasing department to place an order

with a vendor (seller or supplier).

C. Invoice—an itemized statement of goods prepared by the vendor

(copy sent to buyer) listing the customer’s name, items sold, sales

prices, and terms of sale.

D. Receiving report—used by receiving department to verify that

goods conform to purchase order.

E. Invoice Approval—used by accounting department to verify all

necessary documents related to a purchase are assembled and

approve payment of the related invoice.

F. Voucher—can be a folder used to hold all documents related to a

given transaction and authorizes its recording.

Chapter Outline

Notes

VI. Controls of Purchases Discounts—Appendix 6B

A. Recording inventory purchases using net method provides

more control than gross method.

B. Gross method in a perpetual inventory system—records

the purchase (debit inventory, credit accounts payable) at

the gross amount and later reduces the inventory account

by the amount of the discount if invoice is paid within the

discount period. If the invoice is not paid within the

discount period the inventory account is not affected.

C. Net method in a perpetual inventory system—records

purchases (debit inventory, credit accounts payable) at net

amount and later records Discount Lost and increases

accounts payable if the invoice not paid within discount

period.

D. Discount Lost is an expense account and is brought to

management’s attention so they can seek to identify the

reason for discounts lost such as oversight, carelessness or

unfavorable terms.

E. Periodic inventory system differs from perpetual (under

either method) in that increases to inventory are recorded

in Purchases account and decreases to inventory for the

discount are recorded in Purchases Discount.

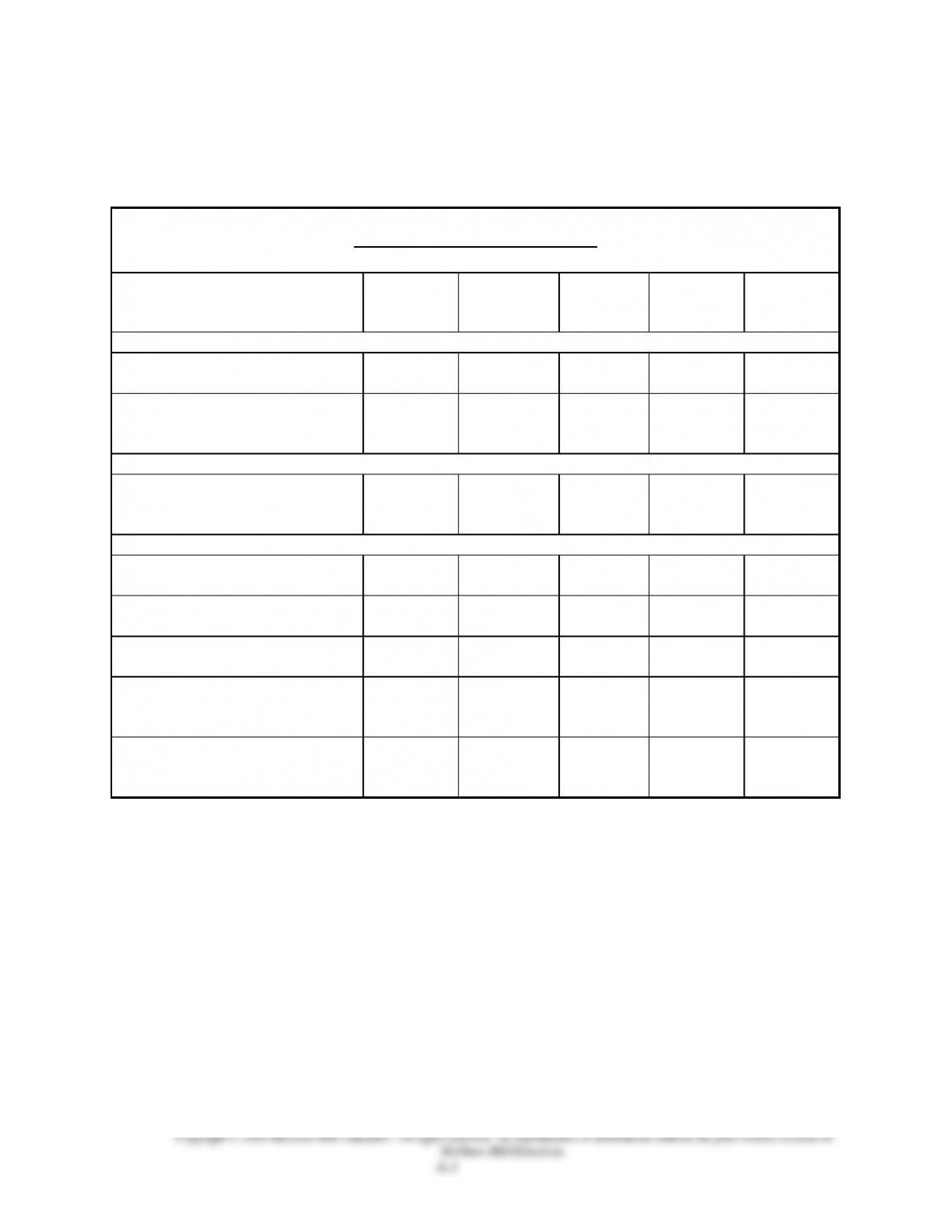

VISUAL #6-1

BANK RECONCILIATION

Reasons for discrepancies between

bank statement balance and checkbook

balance: Handle as follows:

Unrecorded deposits Add to Bank Balance

Outstanding checks Deduct from Bank Balance

Bank service charges Deduct from Book Balance

Debit memos Deduct from Book Balance

Credit memos Add to Book Balance

NSF checks Deduct from Book Balance

Interest Add to Book Balance

Errors Must analyze individually

(bank errors affect bank

balance and book errors

affect book balance)

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

Alternate Demonstration Problem

Chapter 6

The Betsy Dough Company wants to prepare a bank reconciliation for the

month of June. When the bank statement for the month of June arrives

from the bank, the following steps are performed:

1. The deposits to the bank account, as recorded on the bank statement,

are compared to the deposit slips retained by the company. It is noted

that the last deposit, of $400, occurred after banking hours on the day of

the bank statement and therefore has not been recorded by the bank on

this bank statement.

2. Checks returned with the bank statement are compared to the checks

written and listed in checkbook. This comparison shows that there are

checks outstanding amounting to $1,456.

3. The ending balances on the statement and in the company’s books are

determined. The ending bank statement balance is exactly $10,129

whereas the books show $9,000.

4. Other information contained on the bank statement, not previously

known to the company, is determined. This includes the following: (a) a

note of $180 plus $20 interest from a customer for a total of $200 has

been collected by the bank and credited to our account; (b) a check

from Frank Ony for $120 previously deposited by us has been returned

for lack of sufficient funds; (c) the bank has charged us $25 for its

services (this includes a $10 fee for the NSF check). The $10 fee for the

NSF check will be charged to the customer.

5. A bank reconciliation is prepared; it does not balance! The difference is

$18, so a transposition error is looked for (whenever the difference is a

multiple of 9, there is a very good chance that there has been an

inadvertent exchange of two digits (for example, writing 29 when it

should have been 92). An error is found. Check number 141 was written

for $235 for Advertising Expense and cleared the bank for $235, but was

recorded in the company records as $253.

Required:

Prepare a bank reconciliation for the Betsy Dough Company at June 30,

20XX.

Solution: Alternate Demonstration Problem

Chapter 6

BETSY DOUGH COMPANY

Bank Reconciliation

June 30, 20XX

Bank Statement

Bank statement balance ………………………………………

$10,129

Add:

Deposit of June 30 ……………………………………..

400

10,529

Deduct:

Outstanding checks ……………………………………

1,456

$ 9,073

Depositor’s Books

Book balance of cash ………………………………………….

$ 9,000

Add:

Proceeds of customer note collected

by bank ………………………………………………………

200

Error in recording Check No. 141 ………………..

18

Deduct:

NSF check from Frank Ony …………………………

$ 120

Bank service charges …………………………………

25

145

$ 9,073

Adjusting entries Based on the Bank Reconciliation (made by depositor)

Cash………………………………………………………………. 218

Notes Receivable …………………………………………. 180

Interest Revenue ………………………………………….. 20

Advertising Expense ……………………………………… 18

Accounts Receivable – F. Ony ……………………………….. 130

Miscellaneous Expense ………………………………………... 15

Cash 145