Problem 5-1B (Concluded)

3d. Specific Identification

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Apr. 1

20 @ $3,000.00 = $ 60,000.00

Apr. 6

30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

Apr. 9

8 @ $3,000.00

27 @ $3,500.00

= $118,500.00

12 @ $3,000.00

3 @ $3,500.00 = $ 46,500.00

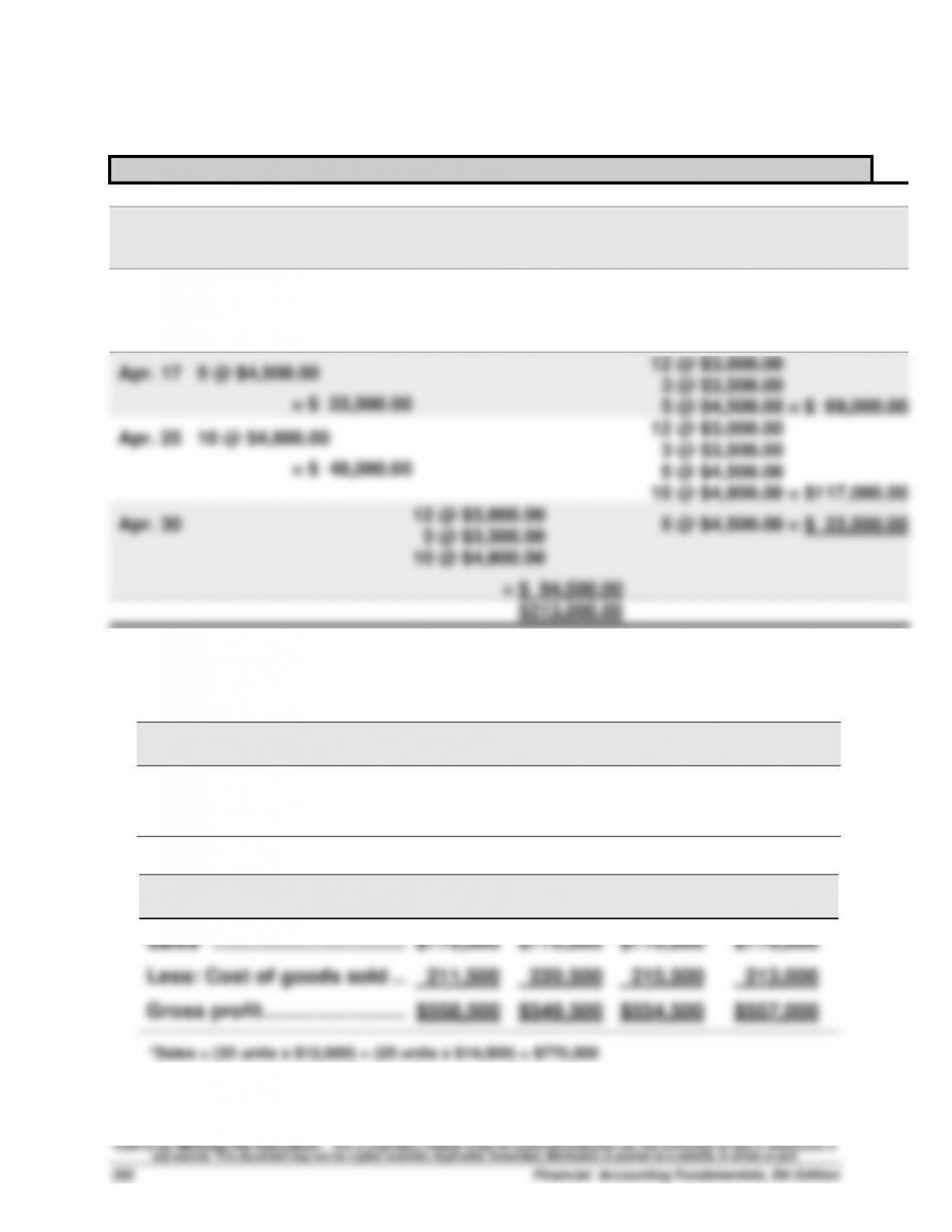

Apr. 17

5 @ $4,500.00

= $ 22,500.00

12 @ $3,000.00

3 @ $3,500.00

5 @ $4,500.00 = $ 69,000.00

Apr. 25

10 @ $4,800.00

= $ 48,000.00

12 @ $3,000.00

3 @ $3,500.00

5 @ $4,500.00

10 @ $4,800.00 = $117,000.00

Apr. 30

12 @ $3,000.00

3 @ $3,500.00

10 @ $4,800.00

= $ 94,500.00

5 @ $4,500.00 = $ 22,500.00

$213,000.00

Specific identification—Alternative Computation

Cost of goods sold—20 [8+12] units from beginning inventory, 30 [27+3] units from

April 6 purchase, and 10 units from April 25 purchase

Ending Cost of

Specific Identification Inventory Goods Sold

(20 x $3,000) + (30 x $3,500) + (10 x $4,800) ………… $213,000

$235,500 [Total Goods Available] – $213,000 [Cost of Goods Sold] .. $22,500

4.

FIFO

LIFO

Weighted

Average

Specific

Identification

Sales* ……………………………..…

$770,000

$770,000

$770,000

$770,000

Less: Cost of goods sold ……

211,500

220,500

215,500

213,000

Gross profit ……………………..…

$558,500

$549,500

$554,500

$557,000

*Sales = (35 units x $12,000) + (25 units x $14,000) = $770,000

Problem 5-2B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

20 units @ $3,000

$ 60,000

April 6 …………………………………………..

30 units @ $3,500

105,000

April 17 ………………………………………….

5 units @ $4,500

22,500

April 25 ………………………………………….

10 units @ $4,800

48,000

Units available ……………………………….

65 units

Cost of goods available for sale ……..

$235,500

2. Units in ending inventory

Units available (from part 1) …………..…………..

65 units

Less: Units sold (35 + 25) …………………………..

60 units

Ending Inventory (units) ………………..…………

5 units

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(5 x $4,800)……………………………………………………….

$24,000.00

(20x$3,000)+(30x$3,500)+(5x$4,500)+(5x$4,800) …

$211,500.00

b. LIFO

(5 x $3,000)………………………………………………………

$15,000.00

(15x$3,000)+(30x$3,500)+(5x$4,500)+(10x$4,800)

$220,500.00

c. Weighted average ($235,500/65=$3,623.08 [rounded])

(5 x $3,623.08)…………………………………………………..

$18,115.40

$235,500 [Goods Available] – $18,115.40 [Ending Inventory] ……

$217,384.60

d. Specific identification

(5 x $4,500)……………………………………………………….

$22,500.00

$235,500 [Goods Available] – $22,500 [Ending Inventory] ………..

$213,000.00

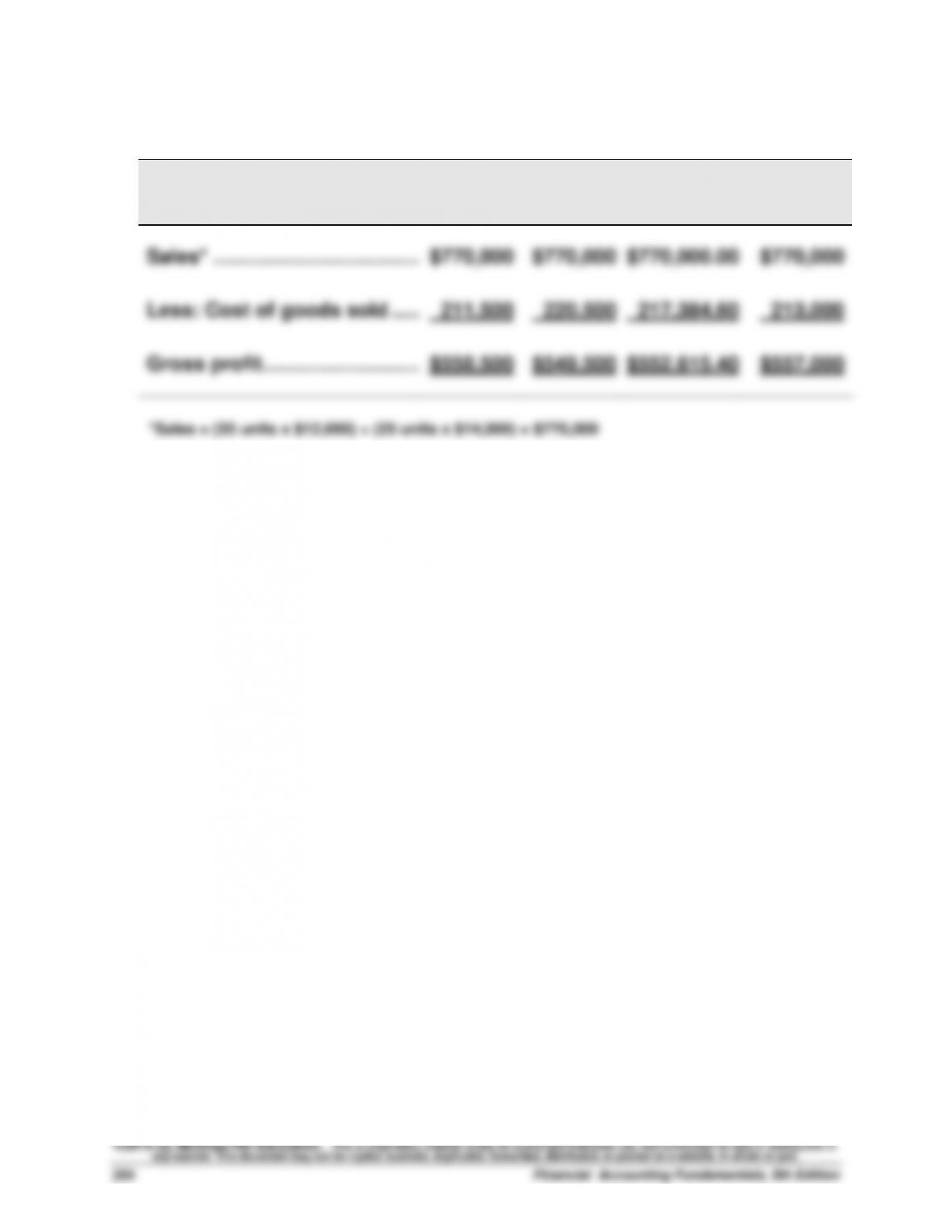

Problem 5-2B (Concluded)

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

Sales* ………………………………..

$770,000

$770,000

$770,000.00

$770,000

Less: Cost of goods sold …...

211,500

220,500

217,384.60

213,000

Gross profit ………………………..

$558,500

$549,500

$552,615.40

$557,000

*Sales = (35 units x $12,000) + (25 units x $14,000) = $770,000

Problem 5-3B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

150 units @ $300

$ 45,000

May 6 …………………………………………...

350 units @ $350

122,500

May 17 …………………………………………..

80 units @ $450

36,000

May 25 …………………………………………..

100 units @ $458

45,800

Units available ……………………………….

680 units

Cost of goods available for sale ……..

$249,300

2. Units in ending inventory

Units available (from part 1) …………..…………..

680 units

Less: Units sold (180 + 300) …………..…………..

480 units

Ending Inventory (units) ………………..…………

200 units

3a. FIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

May 1

150 @ $300 = $ 45,000

May 6

350 @ $350 = $122,500

150 @ $300

350 @ $350 = $167,500

May 9

150 @ $300 = $ 45,000

30 @ $350 = $ 10,500

320 @ $350 = $112,000

May 17

80 @ $450 = $ 36,000

320 @ $350

80 @ $450 = $148,000

May 25

100 @ $458 = $ 45,800

320 @ $350

80 @ $450

100 @ $458 = $193,800

May 30

300 @ $350 = $105,000

20 @ $350

80 @ $450

100 @ $458 = $ 88,800

$160,500

Problem 5-3B (Continued)

3b. LIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

May 1

150 @ $300 = $ 45,000

May 6

350 @ $350 = $122,500

150 @ $300

350 @ $350 = $167,500

May 9

180 @ $350 = $ 63,000

150 @ $300

170 @ $350 = $104,500

May 17

80 @ $450 = $ 36,000

150 @ $300

170 @ $350

80 @ $450 = $140,500

May 25

100 @ $458 = $ 45,800

150 @ $300

170 @ $350

80 @ $450

100 @ $458 = $186,300

May 30

100 @ $458 = $ 45,800

80 @ $450 = $ 36,000

120 @ $350 = $ 42,000

150 @ $300

50 @ $350 = $ 62,500

$186,800

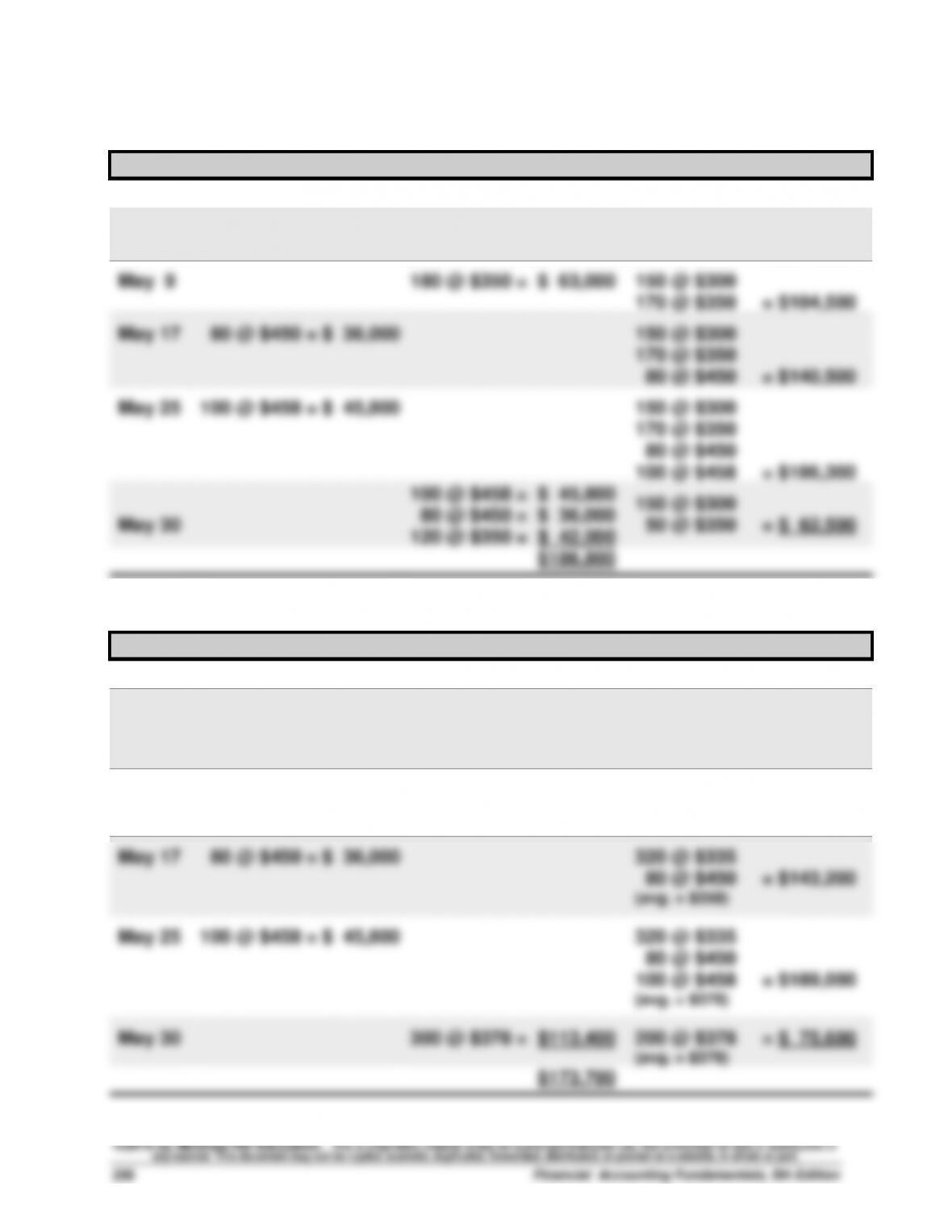

3c. Weighted Average perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

May 1

150 @ $300 = $ 45,000

May 6

350 @ $350 = $122,500

150 @ $300

350 @ $350 = $167,500

(avg. = $335)

May 9

180 @ $335 = $ 60,300

320 @ $335 = $107,200

(avg. = $335)

May 17

80 @ $450 = $ 36,000

320 @ $335

80 @ $450 = $143,200

(avg. = $358)

May 25

100 @ $458 = $ 45,800

320 @ $335

80 @ $450

100 @ $458 = $189,000

(avg. = $378)

May 30

300 @ $378 = $113,400

200 @ $378 = $ 75,600

(avg. = $378)

$173,700

©2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 5

357

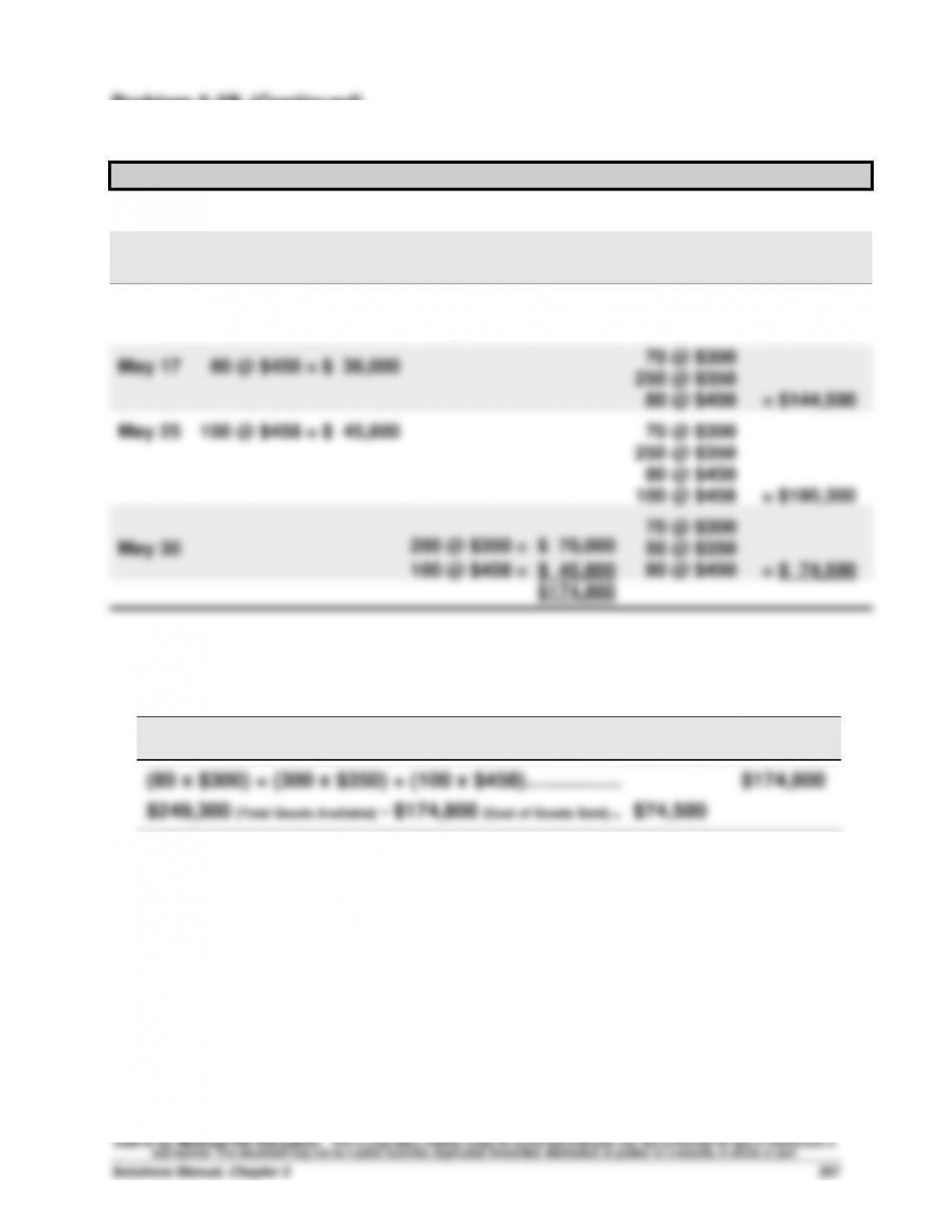

Problem 5-3B (Continued)

3d. Specific Identification

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

May 1

150 @ $300 = $ 45,000

May 6

350 @ $350 = $122,500

150 @ $300

350 @ $350 = $167,500

May 9

80 @ $300 = $ 24,000

100 @ $350 = $ 35,000

70 @ $300

250 @ $350 = $108,500

May 17

80 @ $450 = $ 36,000

70 @ $300

250 @ $350

80 @ $450 = $144,500

May 25

100 @ $458 = $ 45,800

70 @ $300

250 @ $350

80 @ $450

100 @ $458 = $190,300

May 30

200 @ $350 = $ 70,000

100 @ $458 = $ 45,800

70 @ $300

50 @ $350

80 @ $450 = $ 74,500

$174,800

Specific identification—Alternative Computation

Cost of goods sold—80 units from beginning inventory, 300 [100+200] units from May

6 purchase, and 100 units from May 25 purchase

Ending Cost of

Specific Identification Inventory Goods Sold

©2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Financial Accounting Fundamentals, 5th Edition

358

Problem 5-3B (Continued)

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

Sales* ………………………………..

$636,000

$636,000

$636,000

$636,000

Less: Cost of goods sold …...

160,500

186,800

173,700

174,800

Gross profit ………………………..

$475,500

$449,200

$462,300

$461,200

*Sales = (180 units x $1,200) + (300 units x $1,400) = $636,000

5. The manager of Aloha Company likely will prefer the FIFO method

Problem 5-4B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

150 units @ $300

$ 45,000

May 6 …………………………………………...

350 units @ $350

122,500

May 17 …………………………………………..

80 units @ $450

36,000

May 25 …………………………………………..

100 units @ $458

45,800

Units available ……………………………….

680 units

Cost of goods available for sale ……..

$249,300

2. Units in ending inventory

Units available (from part 1) …………..…………..

680 units

Less: Units sold (180 + 300) …………..…………..

480 units

Ending Inventory (units) ………………..…………

200 units

Problem 5-4B (Concluded)

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(100 x $458.00) + (80 x $450.00) + (20 x $350.00) ..

$88,800.00

(150 x $300.00) + (330 x $350.00) ……………………….

$160,500.00

b. LIFO

(150 x $300.00) + (50 x $350.00) ………………………..

$62,500.00

(100 x $458.00) + (80 x $450.00) + (300 x $350.00)

$186,800.00

c. Weighted average ($249,300/680=$366.62 [rounded])

(200 x $366.62) …………………………………………………

$73,324.00

$249,300 [Goods Available] – $73,324 [Ending Inventory] ………..

$175,976.00

d. Specific identification

(70x$300)+(50x$350)+(80x$450)+(0x$458) …………

$74,500.00

$249,300 [Goods Available] – $74,500 [Ending Inventory] ………..

$174,800.00

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

Sales* ………………………………..

$636,000

$636,000

$636,000

$636,000

Less: Cost of goods sold …...

160,500

186,800

175,976

174,800

Gross profit ………………………..

$475,500

$449,200

$460,024

$461,200

*Sales = (180 units x $1,200) + (300 units x $1,400) = $636,000

5. The manager likely will prefer the FIFO method because it would yield

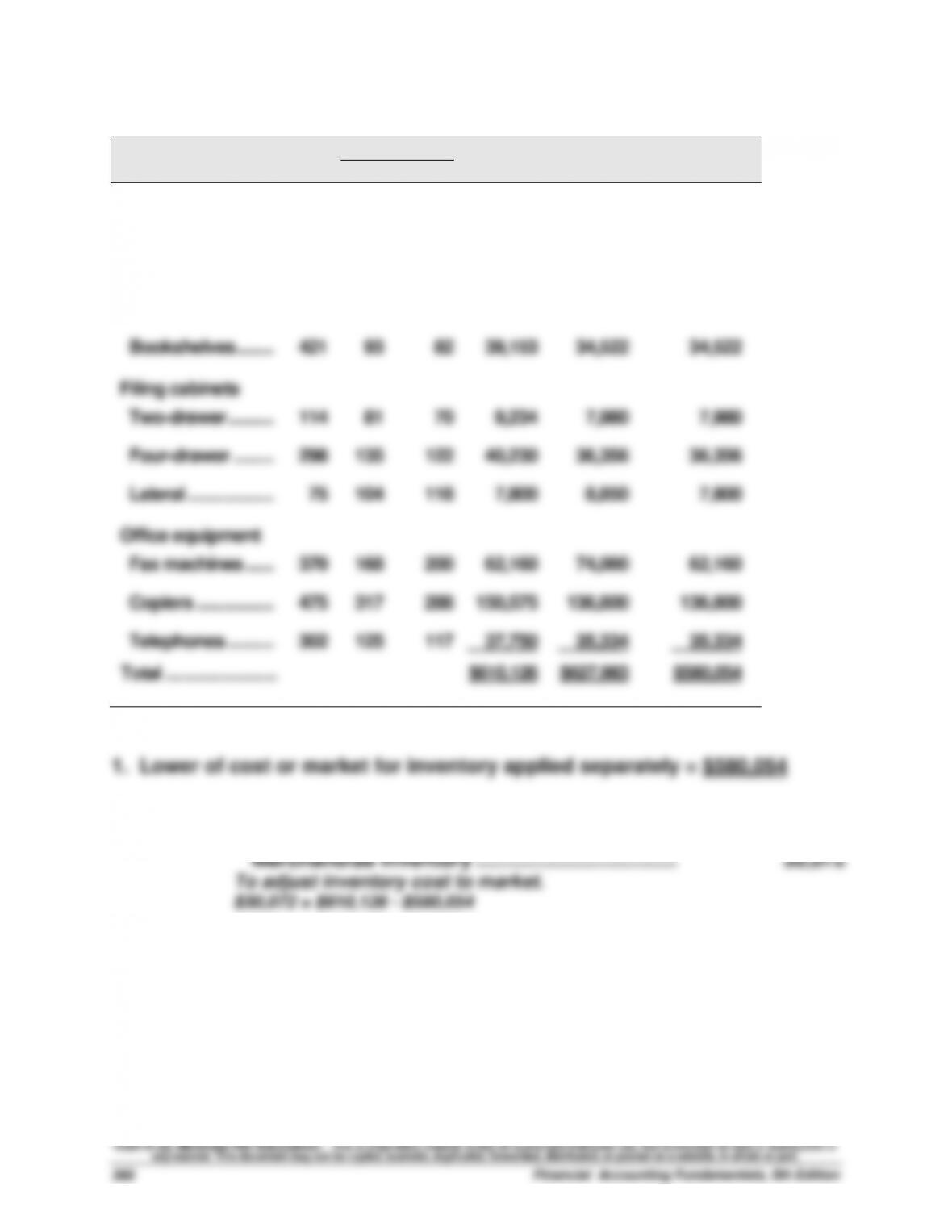

Problem 5-5B (50 minutes)

Per Unit

Total

Total

LCM Applied

Inventory Items

Units

Cost

Market

Cost

Market

to Items

Office furniture

Desks ………………..

536

$261

$305

$139,896

$163,480

$139,896

Credenzas …………

395

227

256

89,665

101,120

89,665

Chairs ………………..

687

49

43

33,663

29,541

29,541

Bookshelves ……..

421

93

82

39,153

34,522

34,522

Filing cabinets

Two–drawer ……….

114

81

70

9,234

7,980

7,980

Four–drawer ………

298

135

122

40,230

36,356

36,356

Lateral ……………….

75

104

118

7,800

8,850

7,800

Office equipment

Fax machines ……

370

168

200

62,160

74,000

62,160

Copiers ……………..

475

317

288

150,575

136,800

136,800

Telephones ……….

302

125

117

37,750

35,334

35,334

Total …………………….

$610,126

$627,983

$580,054

2.

Dec 31

Cost of Goods Sold ………………………………………….….

30,072

Merchandise Inventory ……………………………….….

30,072

To adjust inventory cost to market.

$30,072 = $610,126 – $580,054

Problem 5-6B (35 minutes)

Part 1

(a)

Cost of goods sold

2014

2015

2016

Reported ……………………………..

$ 207,200

$ 213,800

$ 197,030

Adjustments: 12/31/2014 error

+ 18,000

– 18,000

12/31/2015 error

________

– 26,000

+ 26,000

Corrected …………………………....

$ 225,200

$ 169,800

$ 223,030

(b)

Net income

2014

2015

2016

Reported ……………………………..

$ 175,800

$ 212,270

$ 184,910

Adjustments: 12/31/2014 error

– 18,000

+ 18,000

12/31/2015 error

________

+ 26,000

– 26,000

Corrected …………………………....

$ 157,800

$ 256,270

$ 158,910

(c)

Total current assets

2014

2015

2016

Reported ……………………………..

$ 276,000

$ 277,500

$ 272,950

Adjustments: 12/31/2014 error

– 18,000

12/31/2015 error

________

+ 26,000

________

Corrected …………………………....

$ 258,000

$ 303,500

$ 272,950

(d)

Equity

2014

2015

2016

Reported …………………………………….

$ 314,000

$ 315,000

$ 346,000

Adjustments: 12/31/2014 error

– 18,000

12/31/2015 error

________

+ 26,000

________

Corrected ………………………………..….

$ 296,000

$ 341,000

$ 346,000

Part 2

Total net income for the combined three-year period ($572,980) is not affected by

Part 3

The overstatement of inventory by $18,000 results in an understatement of cost of

goods sold by that same amount. The $18,000 understatement of cost of goods

Problem 5-7BA (25 minutes)

Part 1

Number and total cost of units available for sale

6,500 units in beginning inventory @ $35 ………………………..

$ 227,500

11,500 units purchased @ $33 ………………………………………….

379,500

13,400 units purchased @ $32 ………………………………………….

428,800

11,000 units purchased @ $29 ………………………………………….

319,000

7,600 units purchased @ $27 ………………………………………….

205,200

50,000 units available for sale …………………………………………..

$1,560,000

Part 2

a. FIFO periodic

Total cost of 50,000 units available for sale…….

$1,560,000

Less ending inventory on a FIFO basis

7,600 units @ $27………………………………………

$205,200

900 units @ $29………………………………………

26,100

231,300

Cost of goods sold ………………………………………..

$1,328,700

b. LIFO periodic

Total cost of 50,000 units available for sale…….

$1,560,000

Less ending inventory on a LIFO basis

6,500 beg. inv. units @ $35 ………………………….

$227,500

2,000 units @ $33………………………………………..

66,000

293,500

Cost of goods sold ………………………………………..

$1,266,500

c. Weighted average periodic

Total cost of 50,000 units available for sale…….

$1,560,000

Less ending inventory at weighted average cost

($1,560,000/50,000) x 8,500 units………………….

265,200

Cost of goods sold ………………………………………..

$1,294,800

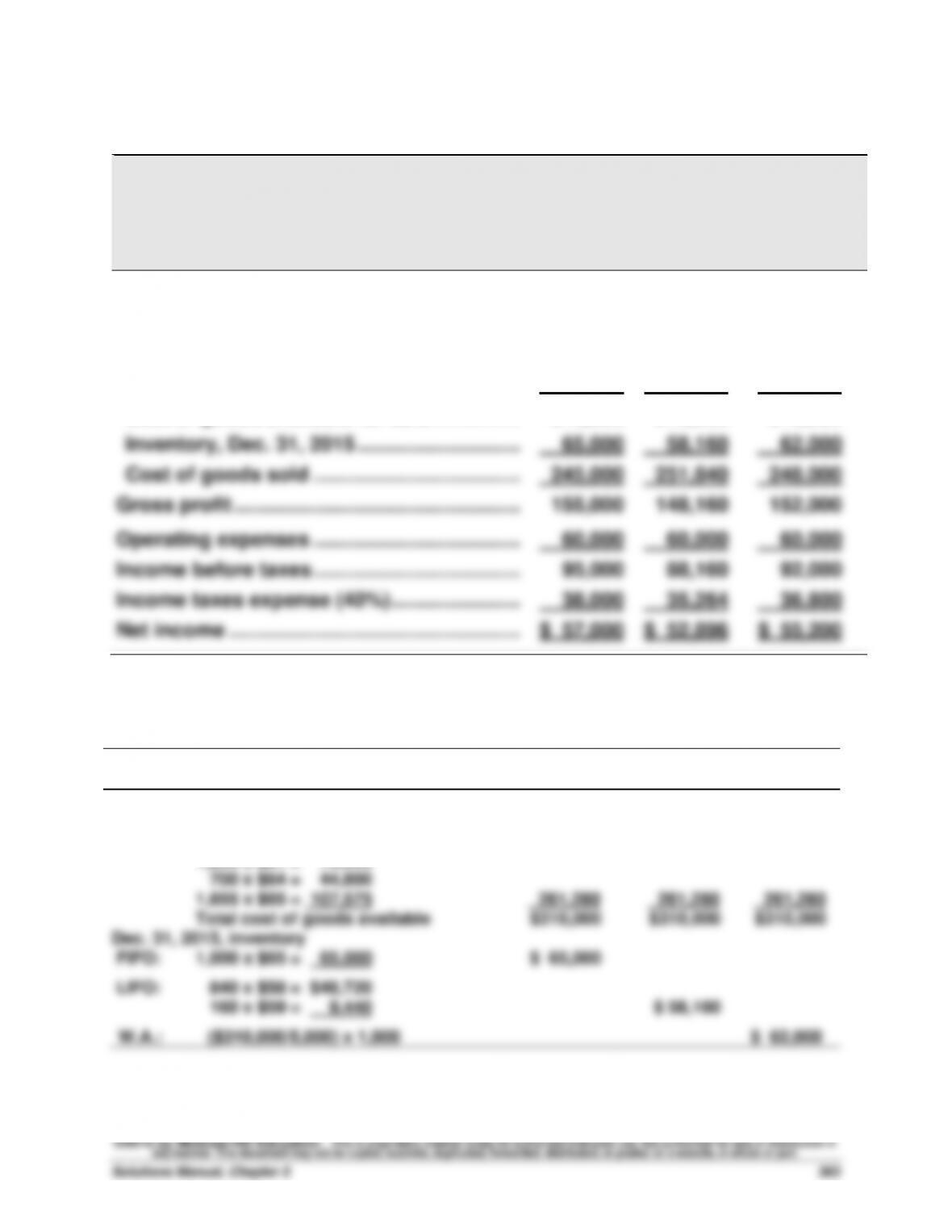

Problem 5-8BA (30 minutes)

Part 1

SHEPARD COMPANY

Income Statements Comparing FIFO, LIFO, and Weighted Average

For Year Ended December 31, 2015

FIFO

LIFO

Weighted

Average

Sales ……………………………………………………..

$400,000

$400,000

$400,000

Cost of goods sold

Inventory, Dec. 31, 2014 ………………………..

48,720

48,720

48,720

Cost of purchases…………………………………

261,280

261,280

261,280

Cost of goods available for sale …………….

310,000

310,000

310,000

Inventory, Dec. 31, 2015 ………………………..

65,000

58,160

62,000

Cost of goods sold ……………………………….

245,000

251,840

248,000

Gross profit ……………………………………………

155,000

148,160

152,000

Operating expenses ……………………………….

60,000

60,000

60,000

Income before taxes ……………………………….

95,000

88,160

92,000

Income taxes expense (40%) …………………..

38,000

35,264

36,800

Net income …………………………..………………..

$ 57,000

$ 52,896

$ 55,200

Supporting calculations

FIFO

LIFO

Weighted

Average

Dec. 31, 2014, inventory (840 x $58) ………………

$ 48,720

$ 48,720

$ 48,720

Purchases

600 x $59 = $ 35,400

1,205 x $61 = 73,505

700 x $64 = 44,800

1,655 x $65 = 107,575

261,280

261,280

261,280

Total cost of goods available

$310,000

$310,000

$310,000

Dec. 31, 2015, inventory

FIFO:

1,000 x $65 = 65,000

$ 65,000

LIFO:

840 x $58 = $48,720

160 x $59 = 9,440

$ 58,160

W.A.:

($310,000/5,000) x 1,000

$ 62,000

Problem 5-8BA (Concluded)

Part 2

If Shepard Company had been experiencing decreasing costs in the

Part 3

Advantages

LIFO: Assuming a trend of increasing costs, the advantage of using LIFO is

Disadvantages

LIFO: Assuming a trend of increasing costs, the disadvantage of using

Problem 5-9BB (25 minutes)

Part 1

MACKLIN COMPANY

Estimated Inventory

December 31

At Cost At Retail

Goods available for sale

Beginning inventory ………………………………………

$ 90,022

$115,610

Cost of goods purchased ……………………………….

502,250

761,830

Goods available for sale …………………………..…….

$592,272

$877,440

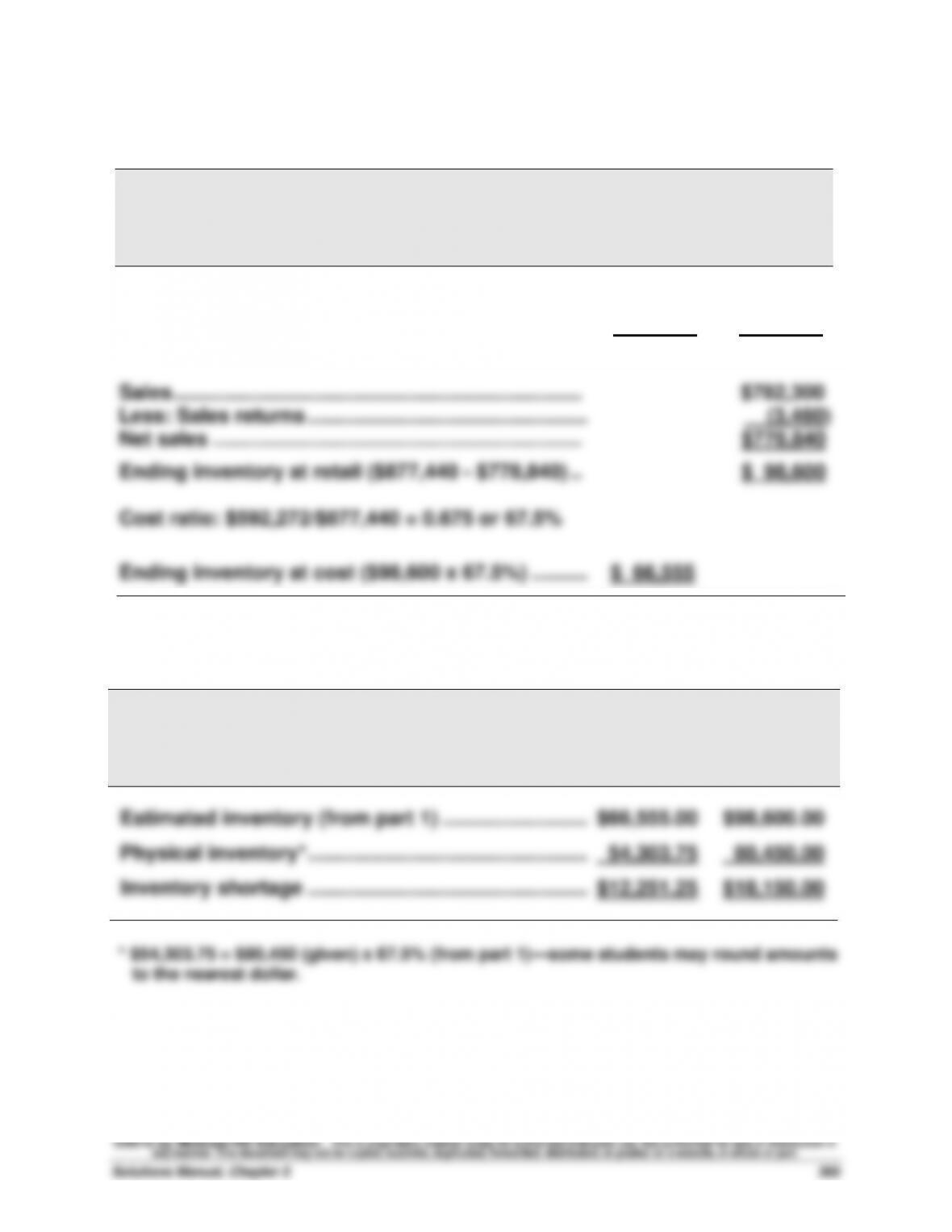

Sales ……………………………………………………………….

$782,300

Less: Sales returns …………………………………………..

(3,460)

Net sales …………………………………………………………

$778,840

Ending inventory at retail ($877,440 – $778,840) ..

$ 98,600

Cost ratio: $592,272/$877,440 = 0.675 or 67.5%

Ending inventory at cost ($98,600 x 67.5%) ……….……..

$ 66,555

Part 2

MACKLIN COMPANY

Inventory Shortage

December 31

At Cost At Retail

Estimated inventory (from part 1) ……………………....

$66,555.00

$98,600.00

Physical inventory* …………………………………………....

54,303.75

80,450.00

Inventory shortage …………………………………………....

$12,251.25

$18,150.00