Exercise 5-7 (20 minutes)

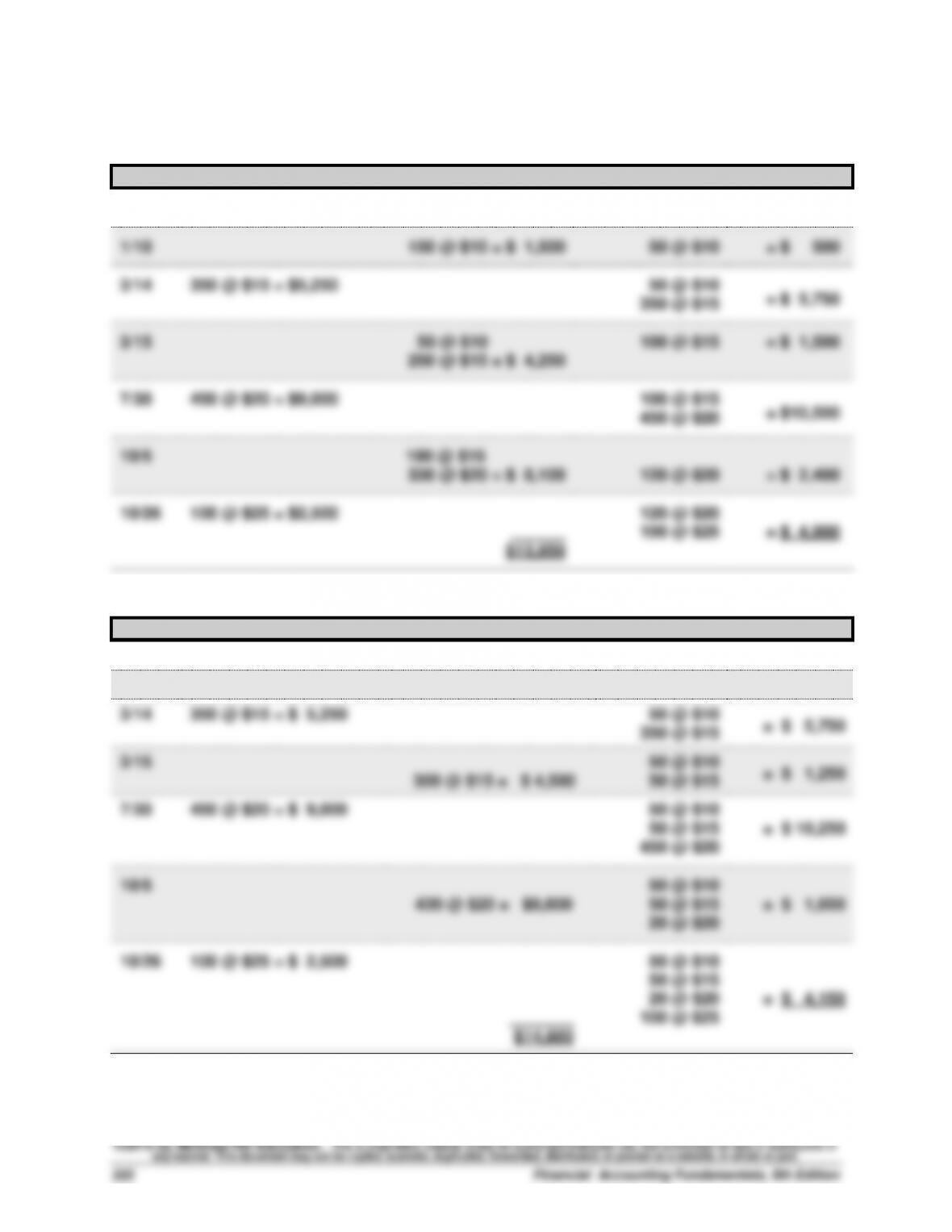

a. FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

200 @ $10

= $ 2,000

1/10

150 @ $10 = $ 1,500

50 @ $10

= $ 500

3/14

350 @ $15 = $5,250

50 @ $10

= $ 5,750

350 @ $15

3/15

50 @ $10

100 @ $15

= $ 1,500

250 @ $15 = $ 4,250

7/30

450 @ $20 = $9,000

100 @ $15

= $10,500

450 @ $20

10/5

100 @ $15

330 @ $20 = $ 8,100

120 @ $20

= $ 2,400

10/26

100 @ $25 = $2,500

120 @ $20

______

100 @ $25

= $ 4,900

$13,850

b. LIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

200 @ $10

= $ 2,000

1/10

150 @ $10 = $ 1,500

50 @ $10

= $ 500

3/14

350 @ $15 = $ 5,250

50 @ $10

= $ 5,750

350 @ $15

3/15

50 @ $10

= $ 1,250

300 @ $15 = $ 4,500

50 @ $15

7/30

450 @ $20 = $ 9,000

50 @ $10

50 @ $15

= $ 10,250

450 @ $20

10/5

50 @ $10

430 @ $20 = $8,600

50 @ $15

= $ 1,650

20 @ $20

10/26

100 @ $25 = $ 2,500

50 @ $10

50 @ $15

20 @ $20

= $ 4,150

_______

100 @ $25

$14,600

Exercise 5-7 (Concluded)

Alternate Solution Format

Ending Cost of

Inventory Goods Sold

a. FIFO

(100 x $25) + (120 x $20) ………………………………………………… $4,900

FIFO Gross Margin

Sales revenue (880 units sold x $40 selling price) ……………..……..

$35,200

Less: FIFO cost of goods sold ………………………………………………..

13,850

Gross profit ……………………………………………………………………..……..

$21,350

LIFO Gross Margin

Sales revenue (880 units sold x $40 selling price) ……………..……..

$35,200

Less: LIFO cost of goods sold ………………………………………………..

14,600

Gross profit ……………………………………………………………………..……..

$20,600

Exercise 5-8 (15 minutes)

a. Specific Identification method—Cost of goods sold

Cost of goods available for sale ………………………………………

$18,750

Ending inventory under specific identification

3/14 purchase ( 45 @ $15) …………………………………..……

$ 675

7/30 purchase ( 75 @ $20) …………………………………………

1,500

10/26 purchase (100 @ $25) …………………………………………

2,500

Total ending inventory under specific identification ….……

4,675

Cost of goods sold under specific identification ……….……

$14,075

b. Specific Identification method—Gross margin

Sales revenue (880 units sold x $40 selling price) ……….……

$35,200

Less: Specific identification cost of goods sold ………………

14,075

Gross profit ……………………………………………………………….……

$21,125

Exercise 5-9A (20 minutes)

Cost of goods available for sale = $18,750 (given in Exercise 5-7)

Ending Cost of

Periodic Inventory System Inventory Goods Sold

a. FIFO—Periodic

(100 x $25) + (120 x $20) …………………………………….. $4,900

(200 x $10) + (350 x $15) + (330 x $20) ………………… $13,850

b. LIFO—Periodic

Sales revenue (880 units sold x $40 selling price) …………….

$35,200

Less: FIFO cost of goods sold …………………………………….….

13,850

Gross margin ……………………………………………………………….….

$21,350

LIFO—Periodic Gross Margin

Sales revenue (880 units sold x $40 selling price) …………….

$35,200

Less: LIFO cost of goods sold …………………………………….….

16,450

Gross margin ……………………………………………………………….….

$18,750

Exercise 5-10 (15 minutes)

Per Unit

Total

Total

LCM Applied

to Items

Inventory Items

Units

Cost

Market

Cost

Market

Helmets ………..

24

$50

$54

$1,200

$1,296

$1,200

Bats ……………..

17

78

72

1,326

1,224

1,224

Shoes …………..

38

95

91

3,610

3,458

3,458

Uniforms ……...

42

36

36

1,512

1,512

1,512

$7,648

$7,490

$7,394

Lower of cost or market of inventory by product = $7,394

Exercise 5-11 (20 minutes)

1. a. LIFO ratio computations

LIFO current ratio (2015) = $220/$200 = 1.1

LIFO inventory turnover (2015) = $740/ [($110+$160)/2] = 5.5

2. The use of LIFO versus FIFO for Cruz markedly impacts the ratios computed.

Specifically, LIFO makes Cruz appear worse in comparison to FIFO numbers

on the current ratio (1.1 vs. 1.5) but better on inventory turnover (5.5 vs. 3.8)

Exercise 5-12 (25 minutes)

1. Correct gross profit = $850,000 – $500,000 = $350,000 (for each year)

2. Reported income figures

Year 2014

Year 2015

Year 2016

Sales …………………………….

$850,000

$850,000

$850,000

Cost of goods sold

Beginning inventory …..

$250,000

$230,000

$250,000

Cost of purchases ………

500,000

500,000

500,000

Good available for sale ……

750,000

730,000

750,000

Ending inventory ………..

230,000

250,000

250,000

Cost of goods sold ……..

520,000

480,000

500,000

Gross profit ………………….

$330,000

$370,000

$350,000

Exercise 5-13 (20 minutes)

2014 Inventory turnover 2014 Days’ Sales in Inventory

2015 Inventory turnover 2015 Days’ Sales in Inventory

Analysis comment: It appears that during a period of increasing sales, Palmer

Exercise 5-14A (20 minutes)

Ending

Inventory

Cost of

Goods Sold

a. Specific identification

(50 x $2.90) + (50 x $2.80) + (50 x $2.50) ………….

$410.00

$3,855 [Goods Available] – $410.00 [Ending Inventory] …………

$3,445.00

b. Weighted average ($3,855/1,500 = $2.57)

150 x $2.57 [rounded to cents] ………………………………….

385.50

$3,855 [Goods Available] – $385.50 [Ending Inventory] …………

3,469.50

c. FIFO

(150 x $2.90)…………………………………………………..

435.00

(96 x $2.00) + (220 x $2.25) + (544 x $2.50) +

(480 x $2.80) + (10 x 2.90) ………………………….

3,420.00

d. LIFO

(96 x $2.00) + (54 x $2.25) ……………………………….

313.50

(160 x $2.90) + (480 x $2.80) + (544 x $2.50) +

(166 x $2.25) ……………………………………………..

3,541.50

Income effect: FIFO provides the lowest cost of goods sold, the

highest gross profit, and the highest net income, which is not

unexpected during a period of rising costs.

Exercise 5-15A (20 minutes)

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. Specific Identification

(50 x $2.80) + (10 x $2.00) ……………………………….

$160.00

$2,540.00 [Goods Available] – $160.00 [Ending Inventory] …….

$2,380.00

b. Weighted Average ($2,540.00/1,000 = $2.54)

(60 x $2.54)…………………………………………………….

152.40

$2,540.00 [Goods Available] – $152.40 [Ending Inventory] …….

2,387.60

c. FIFO

(22 x $2.00) + (38 x 2.30) …………………………………

131.40

(138 x $3.00) + (300 x $2.80) + (502 x $2.30) …….

2,408.60

d. LIFO

(60 x $3.00)…………………………………………………….

180.00

(22 x $2.00) + (540 x $2.30) + (300 x $2.80) +

(78 x $3.00) ……………………………………………….

2,360.00

Income effect: LIFO provides the lowest cost of goods sold, the

highest gross profit, and the highest net income, which is not

unexpected during a period of declining costs.

Exercise 5-16B (20 minutes)

At Cost

At Retail

Goods available for sale

Beginning inventory …………………………………………...

$ 63,800

$128,400

Cost of goods purchased …………………………………...

115,060

196,800

Goods available for sale ……………………………………..

$178,860

325,200

Deduct net sales at retail ……………………………………....

260,000

Ending inventory at retail ……………………………………....

$ 65,200

Cost ratio: ($178,860/$325,200) = 0.55 ………………………..

Ending inventory at cost ($65,200 x 55%) ……………....

$ 35,860

Exercise 5-17B (20 minutes)

Goods available for sale

Inventory, January 1 ………………………………………….….

$ 225,000

Net cost of goods purchased* …………………………….….

802,250

Goods available for sale …………………………………….….

1,027,250

Less estimated cost of goods sold

Net sales ……………………………………………………………….

$1,000,000

Estimated cost of goods sold

[$1,000,000 x (1 – 30%)] …………………………………….

(700,000)

Estimated March 31 inventory …………………………..….….

$ 327,250

* $795,000 – $11,550 + $18,800 = $802,250

Exercise 5-18 (15 minutes)

1. Samsung generally applies the (weighted) average cost assumption when

assigning costs to its inventories. An exception is for its materials–in–

transit.

PROBLEM SET A

Problem 5-1A (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

100 units @ $50.00

$ 5,000

March 5 ………………………………………...

400 units @ $55.00

22,000

March 18 ………………………………………..

120 units @ $60.00

7,200

March 25 ………………………………………..

200 units @ $62.00

12,400

Units available ……………………………….

820 units

Cost of goods available for sale

$46,600

2. Units in ending inventory

Units available (from part 1) …………..…………..

820 units

Less: Units sold (420 + 160) …………..…………..

580 units

Ending Inventory (units) ………………..…………

240 units

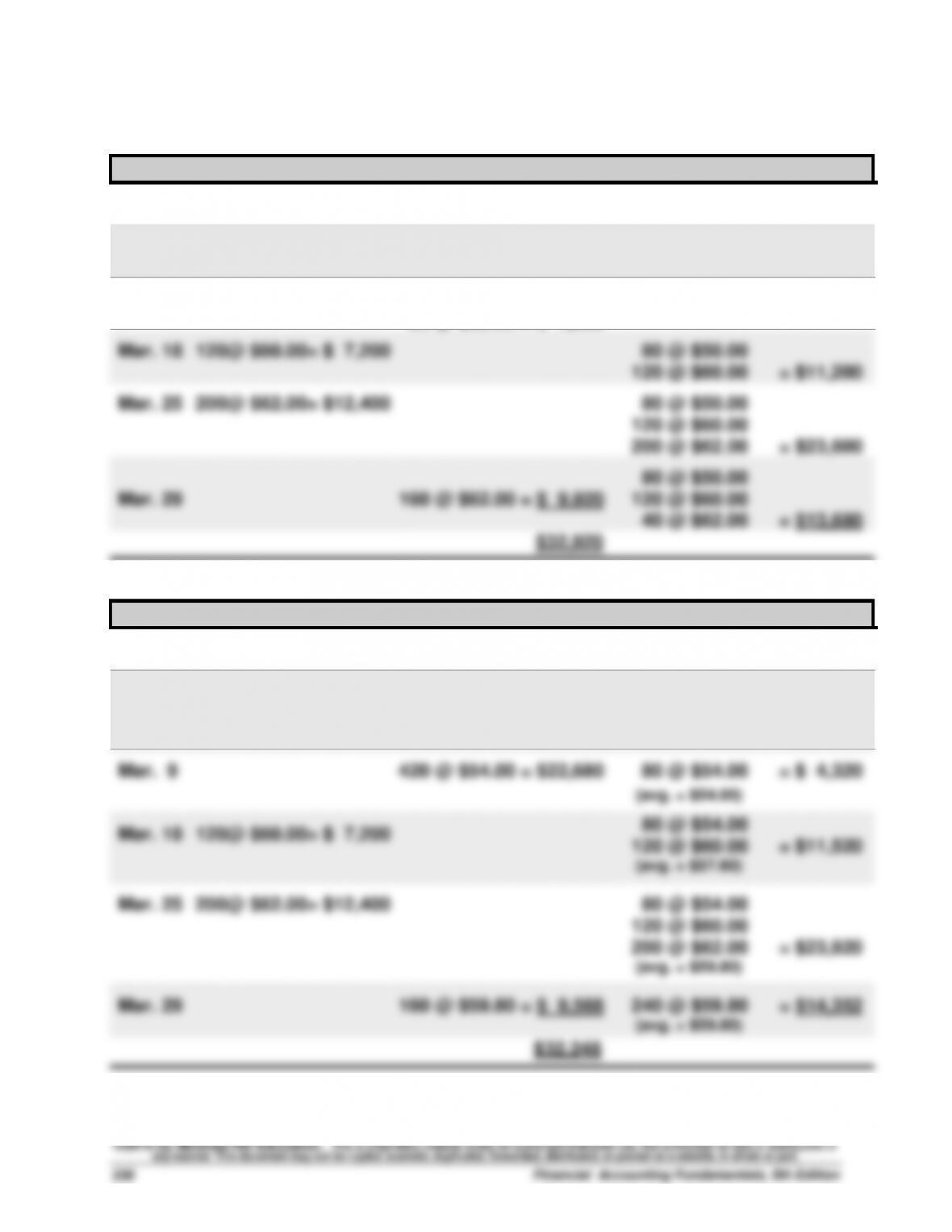

3a. FIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Mar. 1

100 @ $50.00 = $5,000

Mar. 5

400 @ $55.00 = $22,000

100 @ $50.00

400 @ $55.00 = $27,000

Mar. 9

100 @ $50.00 = $ 5,000

320 @ $55.00 = $17,600

80 @ $55.00 = $ 4,400

Mar. 18

120 @ $60.00 = $ 7,200

80 @ $55.00

120 @ $60.00 = $11,600

Mar. 25

200 @ $62.00 = $ 12,400

80 @ $55.00

120 @ $60.00

200 @ $62.00 = $24,000

Mar. 29

80 @ $55.00 = $ 4,400

80 @ $60.00 = $ 4,800

40 @ $60.00

200 @ $62.00 = $14,800

$31,800

Problem 5-1A (Continued)

3b. LIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Mar. 1

100 @ $50.00 = $ 5,000

Mar. 5

400@ $55.00= $22,000

100 @ $50.00

400 @ $55.00 = $27,000

Mar. 9

400 @ $55.00 = $22,000

20 @ $50.00 = $ 1,000

80 @ $50.00 = $ 4,000

Mar. 18

120@ $60.00= $ 7,200

80 @ $50.00

120 @ $60.00 = $11,200

Mar. 25

200@ $62.00= $12,400

80 @ $50.00

120 @ $60.00

200 @ $62.00 = $23,600

Mar. 29

160 @ $62.00 = $ 9,920

80 @ $50.00

120 @ $60.00

40 @ $62.00 = $13,680

$32,920

3c. Weighted Average perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Mar. 1

100 @ $50.00 = $ 5,000

Mar. 5

400@ $55.00= $22,000

100 @ $50.00

400 @ $55.00 = $27,000

(avg. = $54.00)

Mar. 9

420 @ $54.00 = $22,680

80 @ $54.00 = $ 4,320

(avg. = $54.00)

Mar. 18

120@ $60.00= $ 7,200

80 @ $54.00

120 @ $60.00 = $11,520

(avg. = $57.60)

Mar. 25

200@ $62.00= $12,400

80 @ $54.00

120 @ $60.00

200 @ $62.00 = $23,920

(avg. = $59.80)

Mar. 29

160 @ $59.80 = $ 9,568

240 @ $59.80 = $14,352

(avg. = $59.80)

$32,248

©2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Problem 5-1A (Concluded)

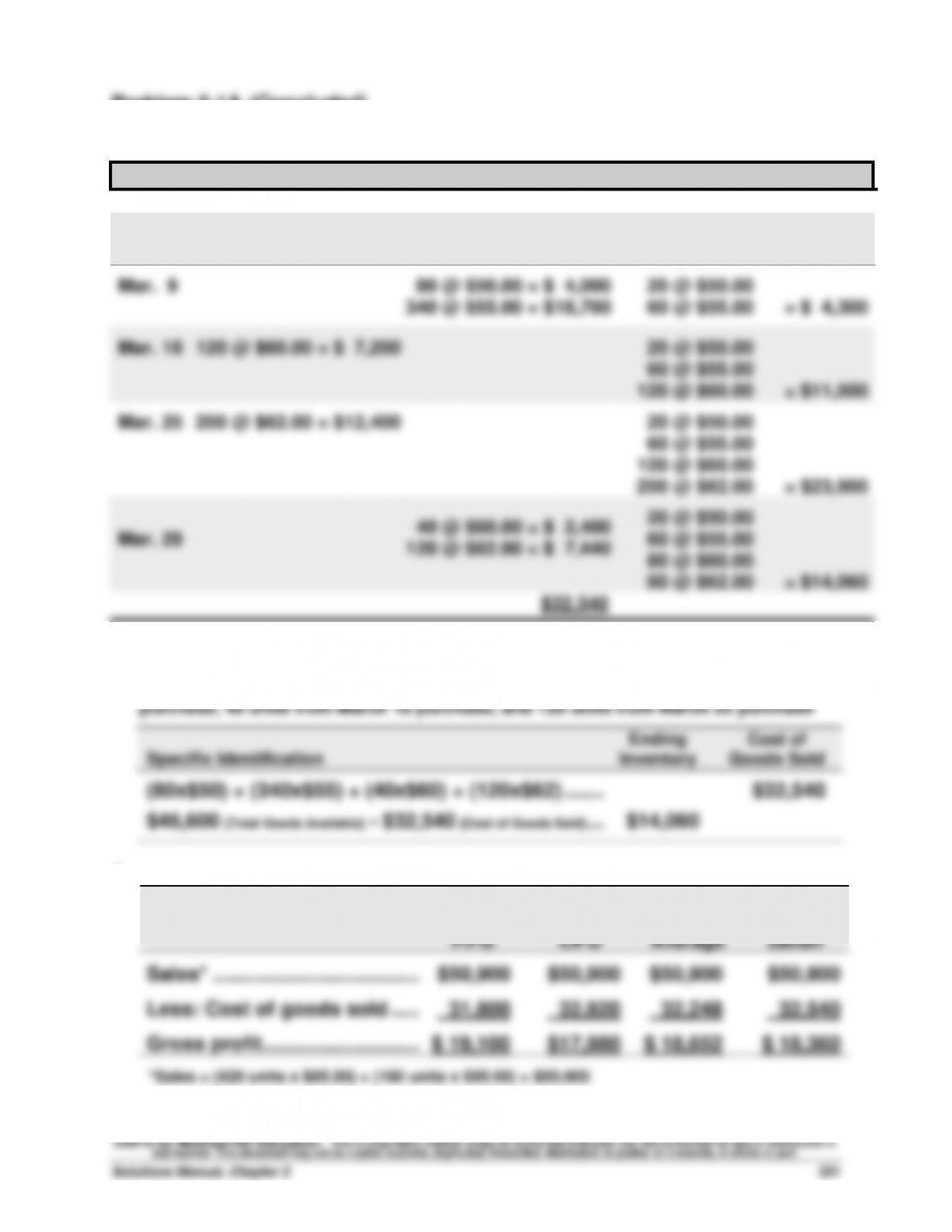

3d. Specific Identification

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Mar. 1

100 @ $50.00 = $ 5,000

Mar. 5

400 @ $55.00 = $22,000

100 @ $50.00

400 @ $55.00 = $27,000

Mar. 9

80 @ $50.00 = $ 4,000

340 @ $55.00 = $18,700

20 @ $50.00

60 @ $55.00 = $ 4,300

Mar. 18

120 @ $60.00 = $ 7,200

20 @ $50.00

60 @ $55.00

120 @ $60.00 = $11,500

Mar. 25

200 @ $62.00 = $12,400

20 @ $50.00

60 @ $55.00

120 @ $60.00

200 @ $62.00 = $23,900

Mar. 29

40 @ $60.00 = $ 2,400

120 @ $62.00 = $ 7,440

20 @ $50.00

60 @ $55.00

80 @ $60.00

80 @ $62.00 = $14,060

$32,540

Specific identification—Alternative Computation

Cost of goods sold—80 units from beginning inventory, 340 units from March 5

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

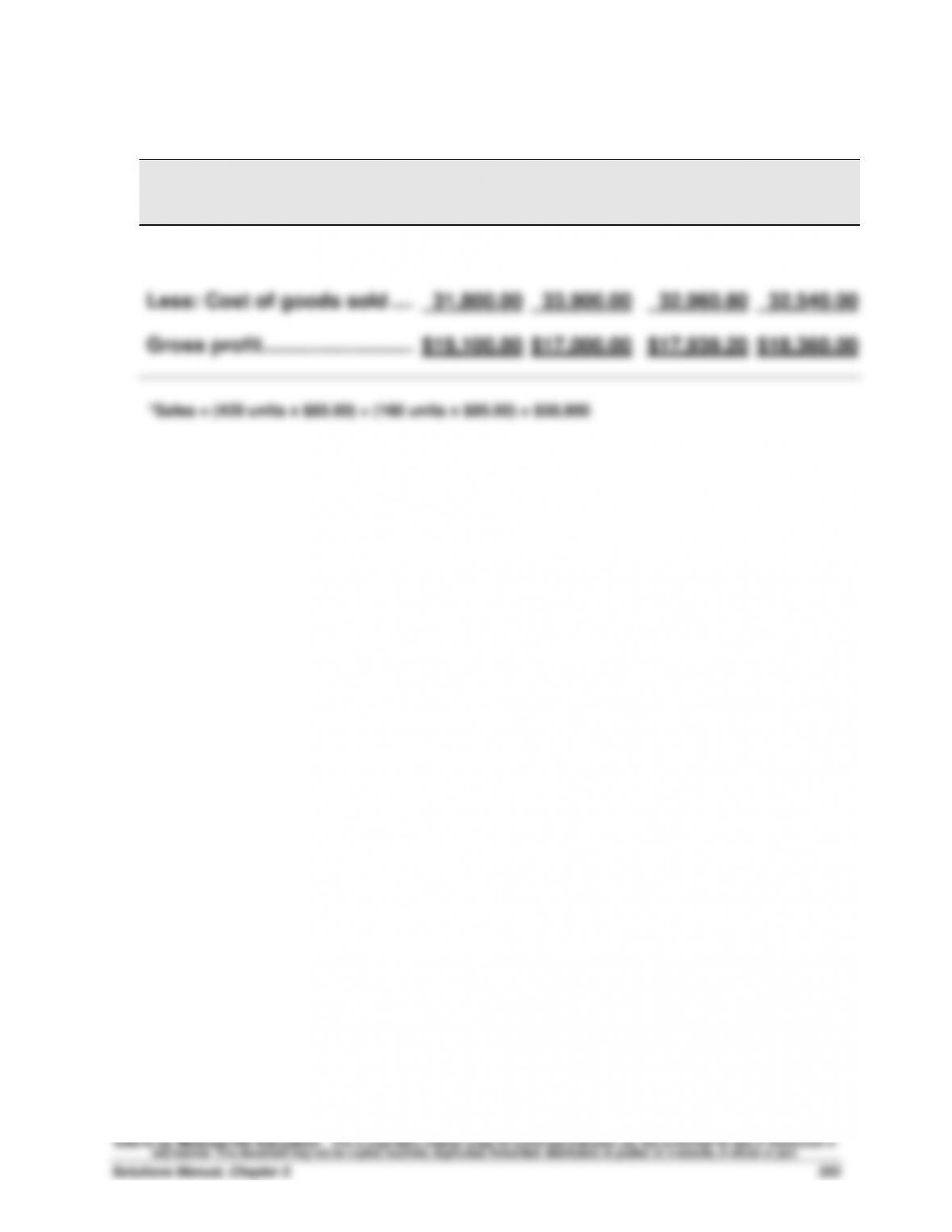

Sales* ………………………………..

$50,900

$50,900

$50,900

$50,900

Less: Cost of goods sold …...

31,800

32,920

32,248

32,540

Gross profit ………………………..

$ 19,100

$17,980

$ 18,652

$ 18,360

*Sales = (420 units x $85.00) + (160 units x $95.00) = $50,900

Problem 5-2A (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

100 units @ $50.00

$ 5,000

March 5 ………………………………………...

400 units @ $55.00

22,000

March 18 ………………………………………..

120 units @ $60.00

7,200

March 25 ………………………………………..

200 units @ $62.00

12,400

Units available ……………………………….

820 units

Cost of goods available for sale

$46,600

2. Units in ending inventory

Units available (from part 1) …………..…………..

820 units

Less: Units sold (420 + 160) …………..…………..

580 units

Ending Inventory (units) ………………..…………

240 units

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(200 x $62.00) + (40 x $60.00) ………………………….

$14,800.00

(100 x $50.00) + (400 x $55.00) + (80 x $60.00) …

$31,800.00

b. LIFO

(100 x $50.00) + (140 x $55.00) ……………………….

$12,700.00

(200 x $62.00) + (120 x $60.00) + (260 x $55.00)

$33,900.00

c. Weighted average ($46,600/820 = $56.83)

(240 x $56.83) ………………………………………………..

$13,639.20

$46,600 [Goods Available] – $13,639.20 [Ending Inventory] …..

$32,960.80

d. Specific identification

(20x$50)+(60x$55)+(80x$60)+(80x$62) …………….

$14,060.00

$46,600 [Goods Available] – $14,060.00 [Ending Inventory] …..

$32,540.00

Problem 5-2A (Concluded)

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

Sales* ………………………………..

$50,900.00

$50,900.00

$50,900.00

$50,900.00

Less: Cost of goods sold …...

31,800.00

33,900.00

32,960.80

32,540.00

Gross profit ………………………..

$19,100.00

$17,000.00

$17,939.20

$18,360.00

*Sales = (420 units x $85.00) + (160 units x $95.00) = $50,900

Problem 5-3A (40 minutes)

1. Calculate cost of goods available for sale and units available for sale

Beginning inventory ……………………...

600 units @ $45.00

$27,000

Feb. 10 ………………………………………….

400 units @ $42.00

16,800

Mar. 13 ………………………………………….

200 units @ $27.00

5,400

Aug. 21 …………………………..……………..

100 units @ $50.00

5,000

Sept. 5 …………………………..……………..

500 units @ $46.00

23,000

Units available ……………………………….

1,800 units

Cost of goods available for sale

$77,200

2. Units in ending inventory

Units available (from part 1) …………..…………..

1,800

Less: Units sold (800+600) …………….…………..

1,400

Ending Inventory (units) ………………..…………

400

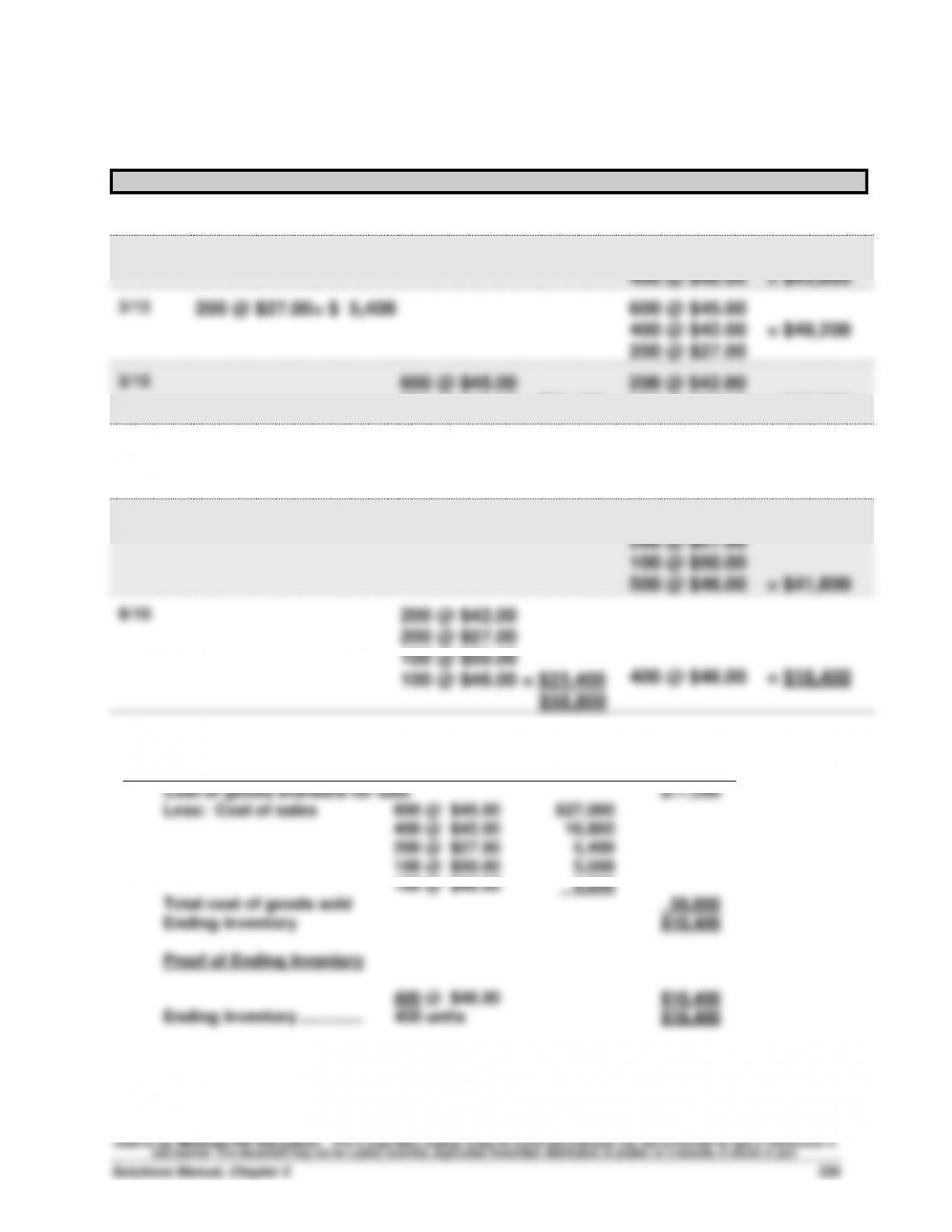

Problem 5-3A (Continued)

3a. FIFO perpetual

Date

Goods Purchasd

Cost of Goods Sold

Inventory Balance

1/1

600 @ $45.00 = $27,000

2/10

400 @ $42.00= $16,800

600 @ $45.00

400 @ $42.00 = $43,800

3/13

200 @ $27.00= $ 5,400

600 @ $45.00

400 @ $42.00 = $49,200

200 @ $27.00

3/15

600 @ $45.00

200 @ $42.00 = $35,400

200 @ $42.00

200 @ $27.00 = $13,800

8/21

100 @ $50.00= $ 5,000

200 @ $42.00

200 @ $27.00 = $18,800

100 @ $50.00

9/5

500 @ $46.00= $23,000

200 @ $42.00

200 @ $27.00

100 @ $50.00

500 @ $46.00 = $41,800

9/10

200 @ $42.00

200 @ $27.00

100 @ $50.00

100 @ $46.00 = $23,400

400 @ $46.00 = $18,400

$58,800

FIFO Alternate Solution Format

Cost of goods available for sale

$77,200

Less: Cost of sales

600 @ $45.00

$27,000

400 @ $42.00

16,800

200 @ $27.00

5,400

100 @ $50.00

5,000

100 @ $46.00

4,600

Total cost of goods sold

58,800

Ending Inventory

$18,400

Proof of Ending Inventory

400 @ $46.00

$18,400

Ending Inventory ……………..

400 units

$18,400

Problem 5-3A (Continued)

3b. LIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

600 @ $45.00 = $27,000

2/10

400 @ $42.00= $16,800

600 @ $45.00

400 @ $42.00 = $43,800

3/13

200 @ $27.00= $ 5,400

600 @ $45.00

400 @ $42.00 = $49,200

200 @ $27.00

3/15

200 @ $27.00

400 @ $42.00

200 @ $45.00 = $31,200

400 @ $45.00 = $18,000

8/21

100 @ $50.00= $ 5,000

400 @ $45.00

100 @ $50.00 = $23,000

9/5

500 @ $46.00= $23,000

400 @ $45.00

100 @ $50.00

500 @ $46.00 = $46,000

9/10

500 @ $46.00

100 @ $50.00 = $28,000

400 @ $45.00 = $18,000

$59,200

LIFO alternate solution format

Cost of goods available for sale

$77,200

Less: Cost of sales

500 @ $46

$23,000

100 @ 50

5,000

200 @ 27

5,400

400 @ 42

16,800

200 @ 45

9,000

Cost of Goods Sold

59,200

Ending Inventory

$18,000

Proof of Ending Inventory

400 @ 45

18,000

Ending Inventory…

400 units

$18,000