Serial Problem, SP 3 (Continued)

Part 8

BUSINESS SOLUTIONS

Post-Closing Trial Balance

December 31, 2015

Debit Credit

Cash ………………………………………………………………………. $ 48,372

Accounts receivable ………………………………………………. 5,668

Computer supplies …………………………………………………. 580

Prepaid insurance ………………………………………………….. 1,665

Prepaid rent …………………………………………………………… 825

Office equipment ……………………………………………………. 8,000

Serial Problem, SP 3 (Continued)

[Instructor Note: Ledger includes all entries from prior three months. The Working

Papers shorten the solution by showing account balances as of November 30.]

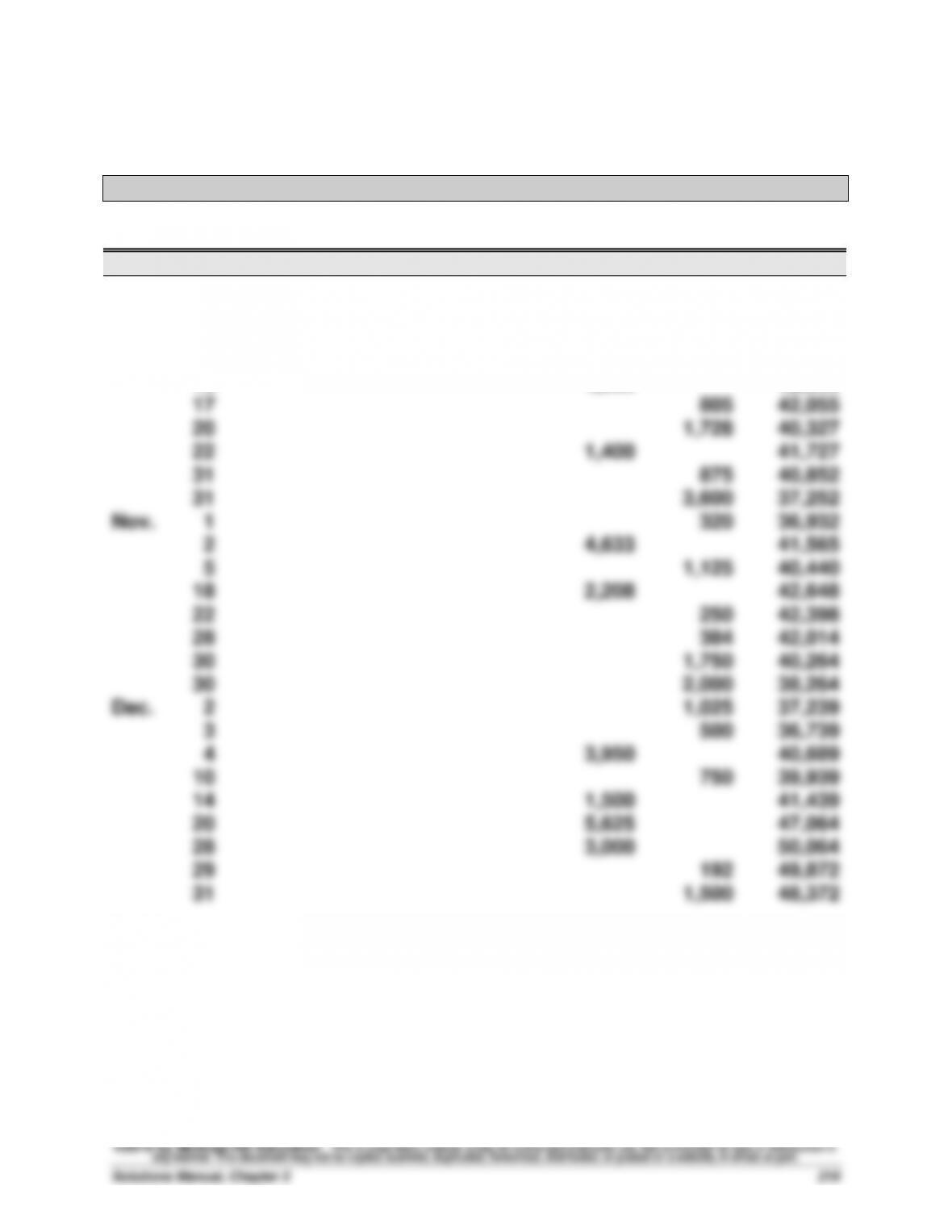

General Ledger

Cash

Acct. No. 101

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

45,000

45,000

2

3,300

41,700

5

2,220

39,480

8

1,420

38,060

15

4,800

42,860

17

805

42,055

20

1,728

40,327

22

1,400

41,727

31

875

40,852

31

3,600

37,252

Nov.

1

320

36,932

2

4,633

41,565

5

1,125

40,440

18

2,208

42,648

22

250

42,398

28

384

42,014

30

1,750

40,264

30

2,000

38,264

Dec.

2

1,025

37,239

3

500

36,739

4

3,950

40,689

10

750

39,939

14

1,500

41,439

20

5,625

47,064

28

3,000

50,064

29

192

49,872

31

1,500

48,372

Serial Problem, SP 3 (Continued)

Accounts Receivable

Acct. No. 106

Date

Explanation

PR

Debit

Credit

Balance

Oct.

6

4,800

4,800

12

1,400

6,200

15

4,800

1,400

22

1,400

0

28

5,208

5,208

Nov.

8

5,668

10,876

18

2,208

8,668

24

3,950

12,618

Dec.

4

3,950

8,668

28

3,000

5,668

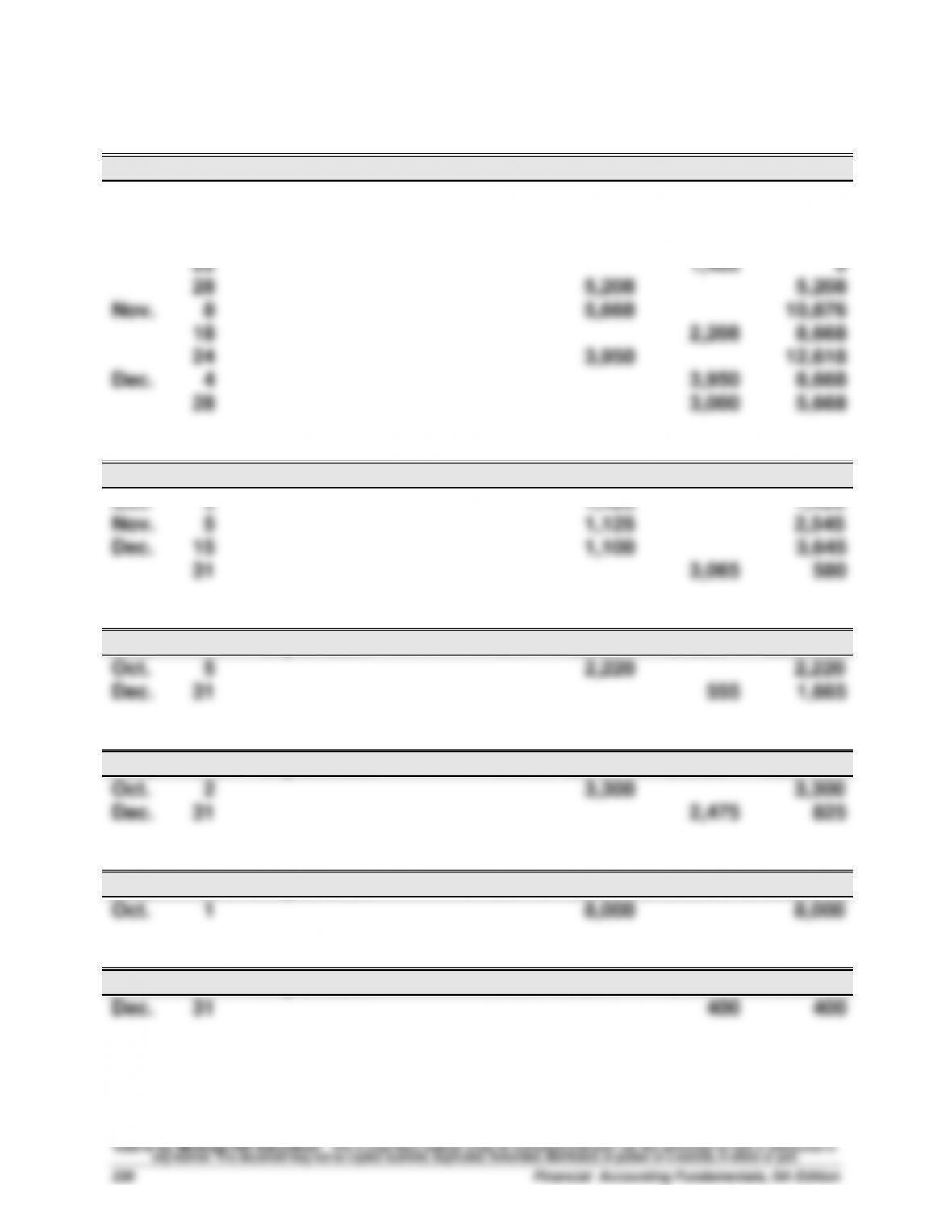

Computer Supplies

Acct. No. 126

Date

Explanation

PR

Debit

Credit

Balance

Oct.

3

1,420

1,420

Nov.

5

1,125

2,545

Dec.

15

1,100

3,645

31

3,065

580

Prepaid Insurance

Acct. No. 128

Date

Explanation

PR

Debit

Credit

Balance

Oct.

5

2,220

2,220

Dec.

31

555

1,665

Prepaid Rent

Acct. No. 131

Date

Explanation

PR

Debit

Credit

Balance

Oct.

2

3,300

3,300

Dec.

31

2,475

825

Office Equipment

Acct. No. 163

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

8,000

8,000

Accumulated Depreciation—Office Equipment

Acct. No. 164

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

400

400

Serial Problem, SP 3 (Continued)

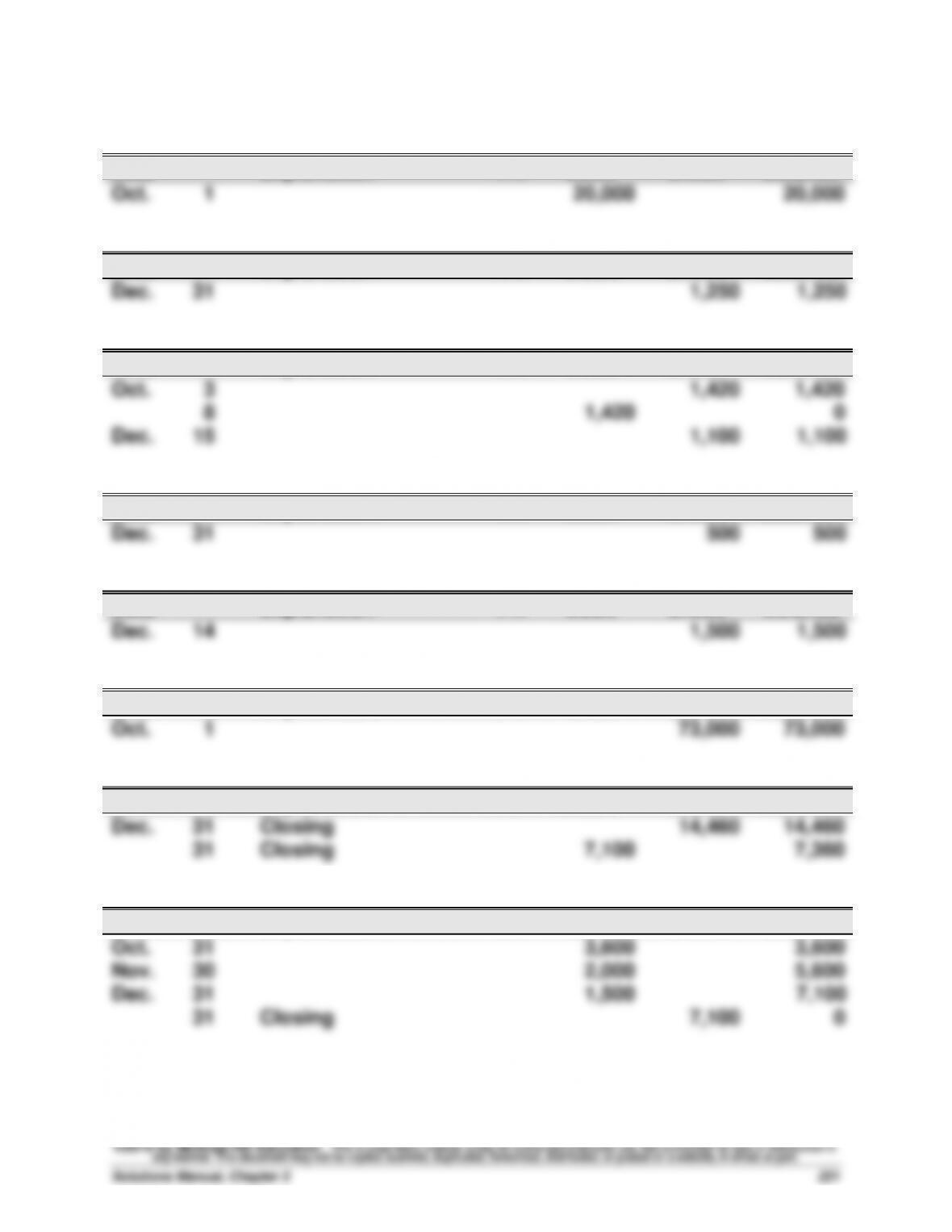

Computer Equipment

Acct. No. 167

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

20,000

20,000

Accumulated Depreciation—Computer Equipment

Acct. No. 168

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

1,250

1,250

Accounts Payable

Acct. No. 201

Date

Explanation

PR

Debit

Credit

Balance

Oct.

3

1,420

1,420

8

1,420

0

Dec.

15

1,100

1,100

Wages Payable

Acct. No. 210

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

500

500

Unearned Computer Services Revenue

Acct. No. 236

Date

Explanation

PR

Debit

Credit

Balance

Dec.

14

1,500

1,500

Common Stock

Acct. No. 307

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

73,000

73,000

Retained Earnings

Acct. No. 318

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

Closing

14,460

14,460

31

Closing

7,100

7,360

Dividends

Acct. No. 319

Date

Explanation

PR

Debit

Credit

Balance

Oct.

31

3,600

3,600

Nov.

30

2,000

5,600

Dec.

31

1,500

7,100

31

Closing

7,100

0

Serial Problem, SP 3 (Continued)

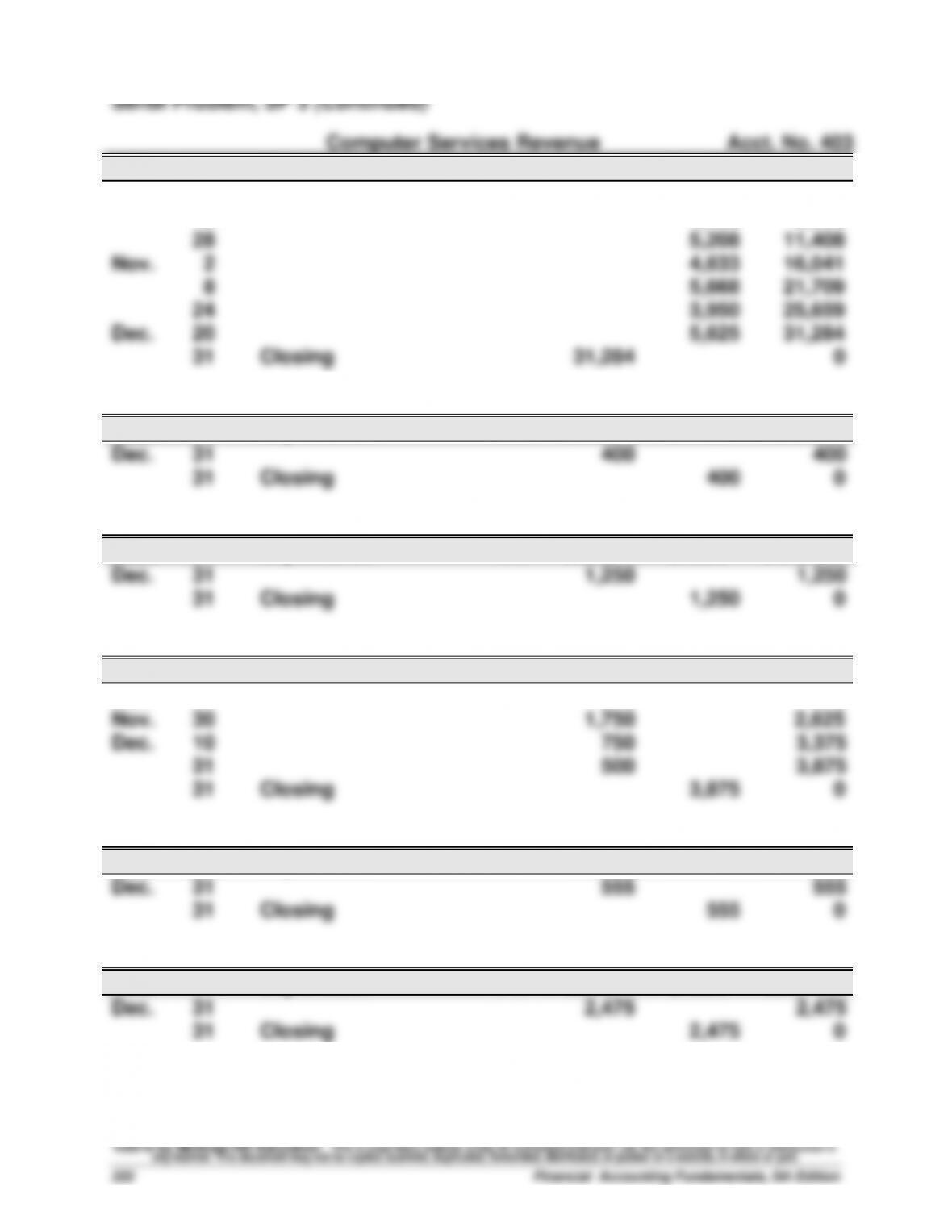

Computer Services Revenue

Acct. No. 403

Date

Explanation

PR

Debit

Credit

Balance

Oct.

6

4,800

4,800

12

1,400

6,200

28

5,208

11,408

Nov.

2

4,633

16,041

8

5,668

21,709

24

3,950

25,659

Dec.

20

5,625

31,284

31

Closing

31,284

0

Depreciation Expense—Office Equipment

Acct. No. 612

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

400

400

31

Closing

400

0

Depreciation Expense—Computer Equipment

Acct. No. 613

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

1,250

1,250

31

Closing

1,250

0

Wages Expense

Acct. No. 623

Date

Explanation

PR

Debit

Credit

Balance

Oct.

31

875

875

Nov.

30

1,750

2,625

Dec.

10

750

3,375

31

500

3,875

31

Closing

3,875

0

Insurance Expense

Acct. No. 637

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

555

555

31

Closing

555

0

Rent Expense

Acct. No. 640

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

2,475

2,475

31

Closing

2,475

0

Serial Problem, SP 3 (Concluded)

Computer Supplies Expense

Acct. No. 652

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

3,065

3,065

31

Closing

3,065

0

Advertising Expense

Acct. No. 655

Date

Explanation

PR

Debit

Credit

Balance

Oct.

20

1,728

1,728

Dec.

2

1,025

2,753

31

Closing

2,753

0

Mileage Expense

Acct. No. 676

Date

Explanation

PR

Debit

Credit

Balance

Nov.

1

320

320

28

384

704

Dec.

29

192

896

31

Closing

896

0

Miscellaneous Expense

Acct. No. 677

Date

Explanation

PR

Debit

Credit

Balance

Nov.

22

250

250

Dec.

31

Closing

250

0

Repairs Expense—Computer

Acct. No. 684

Date

Explanation

PR

Debit

Credit

Balance

Oct.

17

805

805

Dec.

3

500

1,305

31

Closing

1,305

0

Income Summary

Acct. No. 901

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

Closing

31,284

31,284

31

Closing

16,824

14,460

31

Closing

14,460

0

Reporting in Action — BTN 3-1

1. The revenue recognition principle requires that revenue be recorded when

2. Apple provides information on revenue recognition in its Note 1 titled

“Summary of Significant Accounting Policies.” It reports that “The

3. For fiscal year-end September 28, 2013, the profit margin is ($ millions):

4. The revenue items from its income statement must be identified, and those

would be credited to Income Summary as step 1 in the closing entry

5. The total expenses that would be debited to Income Summary as step 2 in

the closing entry process must be computed. Apple’s total expenses for

6. The balance of Income Summary before it is closed as of its fiscal year–

7. Solution depends on the financial statements accessed.

1. Apple

Current year, profit margin = $37,037 / $170,910 = 21.7%

2. Apple and Google have a comparable profit margin in the current year, but

Apple is more successful on the basis of profit margin in the prior year

3. Apple’s current ratios: ($ in millions)

Current year …………………………... $73,286 / $43,658 = 1.68

4. In both years, Google has the higher current ratio (4.58 vs 1.68 for the

current year; 4.22 vs. 1.50 in the prior year), suggesting a better ability to

5. Apple’s current ratio increased from 1.50 to 1.68. Google’s current ratio

also increased from 4.22 to 4.58.

6. Google’s current ratio is above (better than) the industry average for both

years, and Apple’s is below (worse than) the industry average for both

Ethics Challenge — BTN 3-3

1. GAAP requires that annual deprecation be accumulated in a contra-

asset account, called Accumulated Depreciation. While property, plant,

2. One strength of Smith’s method would be the ease of preparing the

balance sheet. The property, plant, and equipment balance in the

3. While both approaches would lead to the same total assets on the

Communicating in Practice — BTN 3-4

TO: _____________________

FROM: _____________________

DATE: ______________________

SUBJECT: CLARIFICATIONS—OBJECTIVE OF THE CLOSING PROCESS

[Following is a sample of what the memorandum’s contents might include.]

When we speak of “closing the books” or the closing process we are not

talking about ending or closing the business nor doing anything that reflects

this thinking in the financial statements. Let me use an analogy to explain the

concept of the closing process and then you will see the distinction more

clearly.

Scoreboards are used to temporarily hold information that will allow us to

or scores that were not relevant to either game. You can see that the

scoreboard must be zeroed-out to prepare it for accumulating data to

determine the outcome of the next game.

The revenue and expense accounts temporarily hold the information to

determine if the owner(s) won or lost in the game of business. Each fiscal

period should be viewed as a separate game. After the data in these accounts

[Note: The memorandum need not discuss the income summary account since the assignment

requires explaining the concept, not the procedure.]

1. The Gap’s main brands (stores) are The Gap, Old Navy, and Banana

Republic. It also has Piperlime and Athleta brands.

2. The Gap’s fiscal year–end is January 28, 2012. It appears that The Gap’s

3. Net sales for the year ended January 28, 2012, are $14,549 million.

Teamwork in Action — BTN 3-6

Note that there is no specific solution to this activity. Still, the presentation

of each expert team should reflect the following summary points:

Before Adjusting

Balance Sheet Income Statement

Type Account Account Adjusting Entry

Prepaid expenses Asset overstated Expense understated Dr. Expense

Cr. Asset*

* For depreciation, one would Credit the Accumulated Depreciation contra account.

Some implementation notes: This activity allows all students to be actively

involved in the learning process. Encourage students to take the opportunity

Entrepreneurial Decision — BTN 3-7

1. a. To record the collection of cash from sale of the gift certificate in

advance of delivery of merchandise to the customer:

2. Carrying less inventory would allow the company to save the costs of

keeping and maintaining that added inventory; such as warehousing

3. If the company carries additional inventory, it can potentially sell more

merchandise and increase its profits. This might further fuel increased

sales as additional customers might be attracted to its products. On

Hitting the Road — BTN 3-8

There is no formal solution to this field activity. The instructor may wish to

tally students’ findings to show results across companies as to use of work

sheets, software preferences, and time it takes to prepare finalized annual

financial statements.

Global Decision — BTN 3-9

1. Samsung (KRW in millions)

Current year, profit margin = ₩30,474,764/ ₩228,692,667= 13.3%

2. Apple is slightly more successful on the basis of profit margin in the

current year relative to Google. However, both Apple and Google are

more successful on the basis of profit margin in the current year