Problem 3-6A (Continued)

Part 4

ADVENTURE TRAVEL

Adjusted Trial Balance

April 30, 2015

No. Account Title Debit Credit

101 Cash …………………………………………………. $27,000

106 Accounts receivable ………………………….. 1,750

124 Office supplies ………………………………….. 600

Problem 3-6A (Continued)

Part 5

ADVENTURE TRAVEL

Income Statement

For Month Ended April 30, 2015

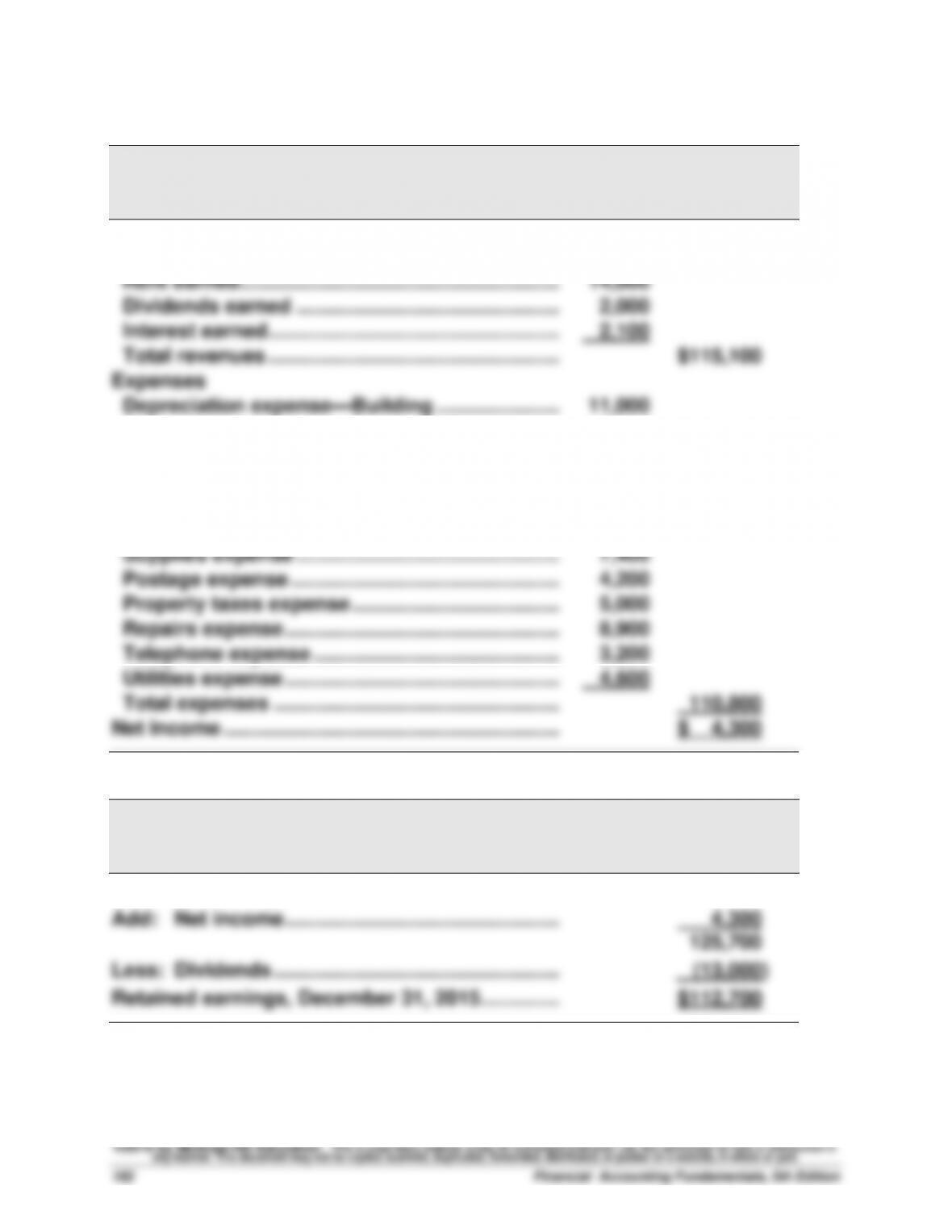

Commissions earned ………………………………………….. $9,750

Expenses

Depreciation expense—Computer equipment ……. $ 500

ADVENTURE TRAVEL

Statement of Retained Earnings

For Month Ended April 30, 2015

Retained earnings, April 1, 2015 ……………….. $ 0

Problem 3-6A (Continued)

Part 5—continued

ADVENTURE TRAVEL

Balance Sheet

April 30, 2015

Assets

Cash ………………………………………………………………………. $27,000

Accounts receivable ………………………………………………. 1,750

Office supplies ……………………………………………………….. 600

Problem 3-6A (Continued)

Part 6

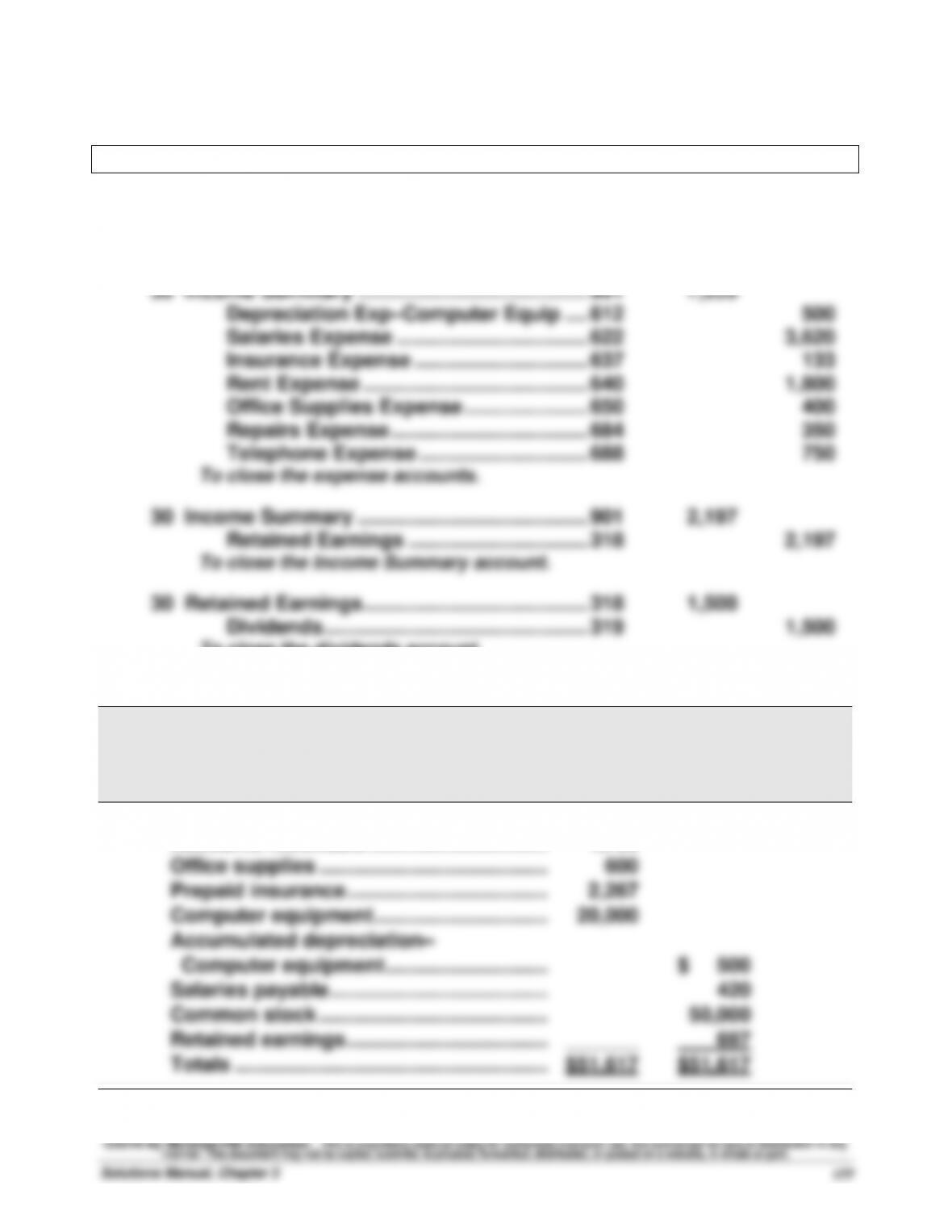

Closing entries

April 30 Commissions Earned …………………………….. 405 9,750

Income Summary ……………………………. 901 9,750

To close the revenue account.

To close the dividends account.

Part 7

ADVENTURE TRAVEL

Post-Closing Trial Balance

April 30, 2015

Debit Credit

Cash …………………………………………………. $27,000

Accounts receivable ………………………….. 1,750

Problem 3-6A (Continued)

Part 7—continued

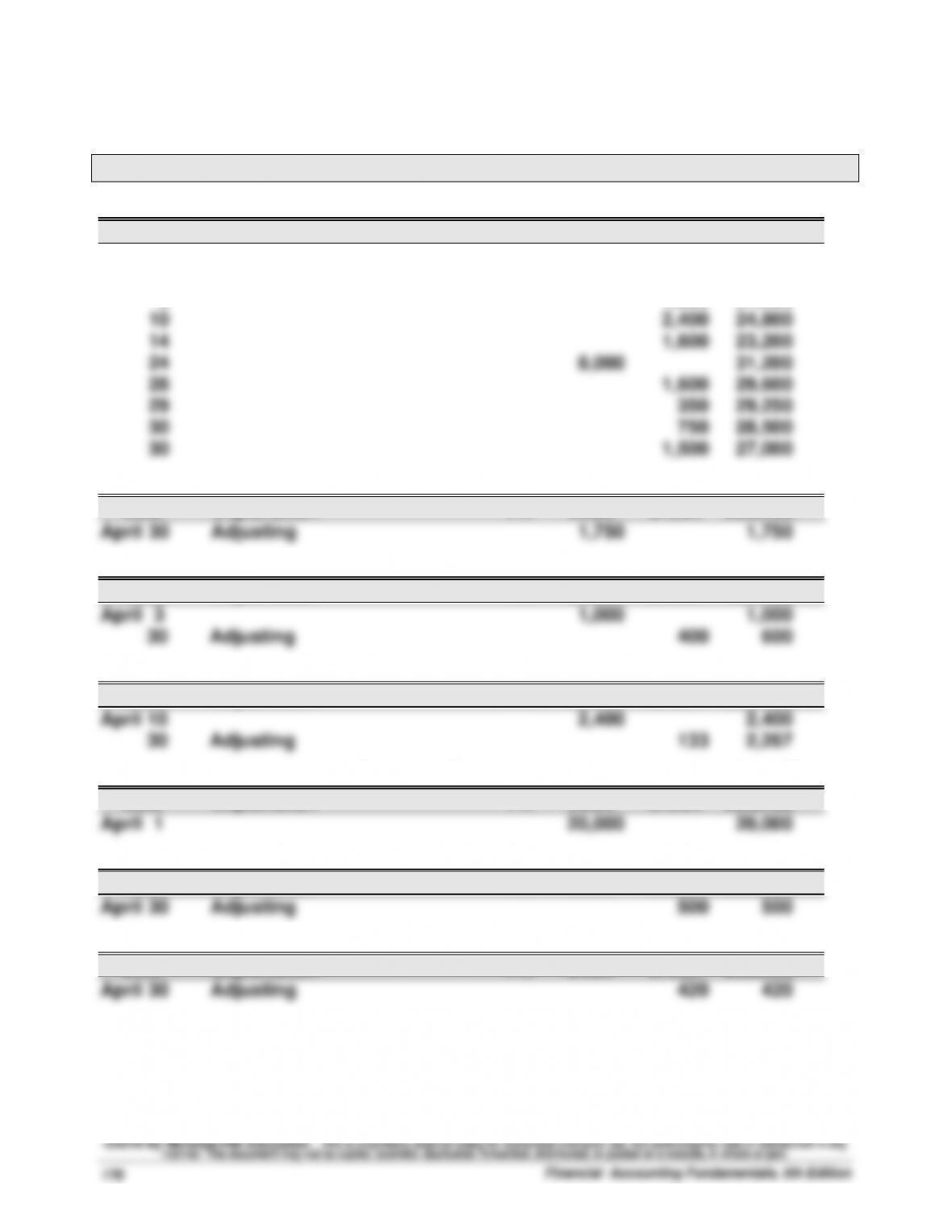

Ledger as of April 30

Cash Acct. No. 101

Date Explanation PR Debit Credit Balance

April 1 30,000 30,000

2 1,800 28,200

3 1,000 27,200

Accounts Receivable Acct. No. 106

Date Explanation PR Debit Credit Balance

Office Supplies Acct. No. 124

Date Explanation PR Debit Credit Balance

Prepaid Insurance Acct. No. 128

Date Explanation PR Debit Credit Balance

Computer Equipment Acct. No. 167

Date Explanation PR Debit Credit Balance

Accumulated Depreciation–Computer Equipment Acct. No. 168

Date Explanation PR Debit Credit Balance

Salaries Payable Acct. No. 209

Date Explanation PR Debit Credit Balance

Problem 3-6A (Continued)

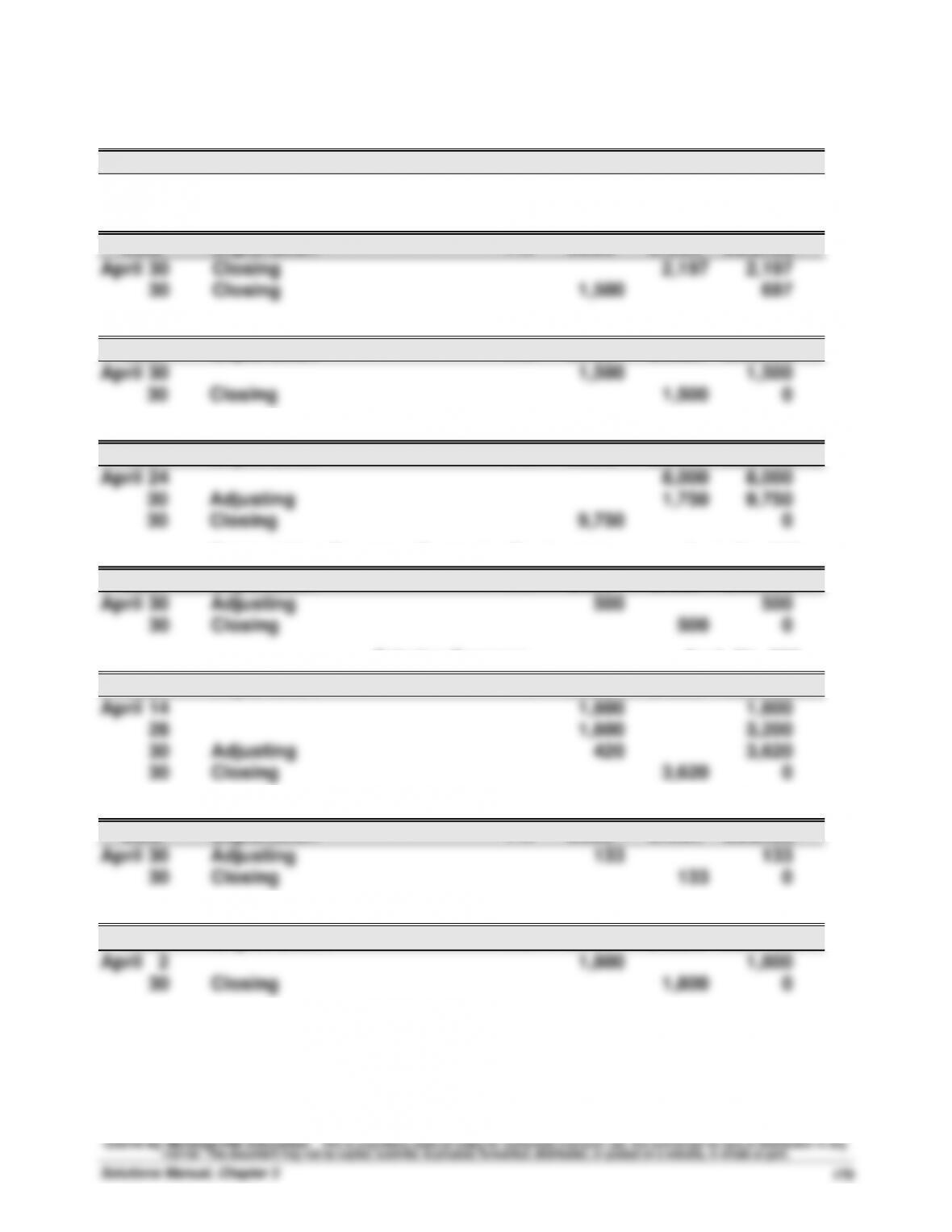

Common Stock Acct. No. 307

Date Explanation PR Debit Credit Balance

April 1 50,000 50,000

Retained Earnings Acct. No. 318

Date Explanation PR Debit Credit Balance

Dividends Acct. No. 319

Date Explanation PR Debit Credit Balance

Commissions Earned Acct. No. 405

Date Explanation PR Debit Credit Balance

Depreciation Expense–Computer Equipment Acct. No. 612

Date Explanation PR Debit Credit Balance

Salaries Expense Acct. No. 622

Date Explanation PR Debit Credit Balance

Insurance Expense Acct. No. 637

Date Explanation PR Debit Credit Balance

Rent Expense Acct. No. 640

Date Explanation PR Debit Credit Balance

Problem 3-6A (Concluded)

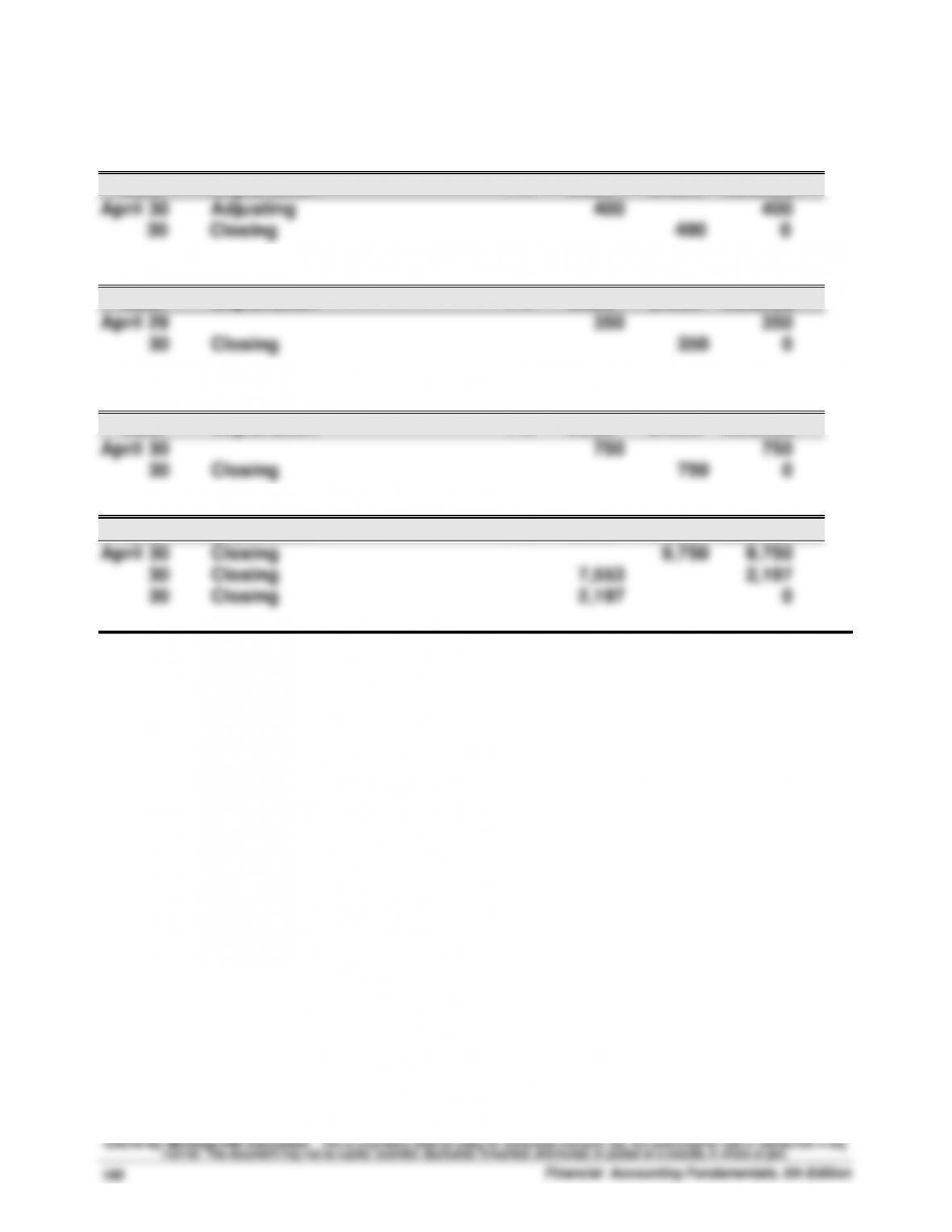

Office Supplies Expense Acct. No. 650

Date Explanation PR Debit Credit Balance

Repairs Expense Acct. No. 684

Date Explanation PR Debit Credit Balance

Telephone Expense Acct. No. 688

Date Explanation PR Debit Credit Balance

Income Summary Acct. No. 901

Date Explanation PR Debit Credit Balance

Problem 3-7A (15 minutes)

1.

B

6.

C

11.

E

16.

C

2.

Z

7.

F

12.

C

17.

C

3.

A

8.

E

13.

A

18.

Z

4.

A

9.

A

14.

C

19.

A

5.

E

10.

G

15.

A

20.

E

Problem 3-8A (75 minutes)

Part 1

TYBALT CONSTRUCTION

Income Statement

For Year Ended December 31, 2015

Revenues

Professional fees earned …………………………….. $97,000

Depreciation expense—Equipment ……………… 6,000

Wages expense ………………………………………….. 32,000

Interest expense …………………………………………. 5,100

Insurance expense ……………………………………… 10,000

Rent expense ……………………………………………… 13,400

TYBALT CONSTRUCTION

Statement of Retained Earnings

For Year Ended December 31, 2015

Retained earnings, December 31, 2014 ………….. $121,400

Problem 3-8A (Continued)

TYBALT CONSTRUCTION

Balance Sheet

December 31, 2015

Assets

Current assets

Plant assets

Equipment ………………………………………………….. 40,000

Accumulated depreciation—Equipment ………. (20,000) 20,000

Building ……………………………………………………… 150,000

Accumulated depreciation—Building ………….. (50,000) 100,000

Accounts payable ……………………………………….. $ 16,500

Interest payable ………………………………………….. 2,500

Rent payable ………………………………………………. 3,500

Wages payable …………………………………………… 2,500

Property taxes payable ……………………………….. 900

Unearned professional fees ………………………… 7,500

Current portion of long-term note payable…… 7,000

Problem 3-8A (Continued)

Part 2

(1) Professional Fees Earned ……………………… 97,000

Rent Earned ………………………………………….. 14,000

(2) Income Summary ………………………………….. 110,800

Depreciation Expense—Building …….. 11,000

Depreciation Expense—Equipment …. 6,000

Wages Expense………………………………. 32,000

(3) Income Summary ………………………………….. 4,300

(4) Retained Earnings …………………………………. 13,000

Dividends ……………………………………….. 13,000

PROBLEM SET B

Problem 3-1B (15 minutes)

1. H 5. B 9. I

Problem 3-2B (30 minutes)

Part 1

Adjustment (a)

Adjustment (b)

Policy

Cost per Month

Months Active

in Fiscal Year

2015

Fiscal Year

2015

Expense

A

$250

($6,000/24 mo.)

12

$3,000

B

200

($7,200/36 mo.)

7

1,400

C

110

($1,320/12 mo.)

3

330

Total

$4,730

Adjustment (c)

Problem 3-2B (Concluded)

Adjustment (d)

Oct. 31 Depreciation Expense—Building …………………….. 5,400

Accumulated Depreciation—Building ………. 5,400

current salaries. *(4 days x $1,000)

Cash Payment for (e)

Problem 3-3B (90 minutes)

Parts 1 and 2

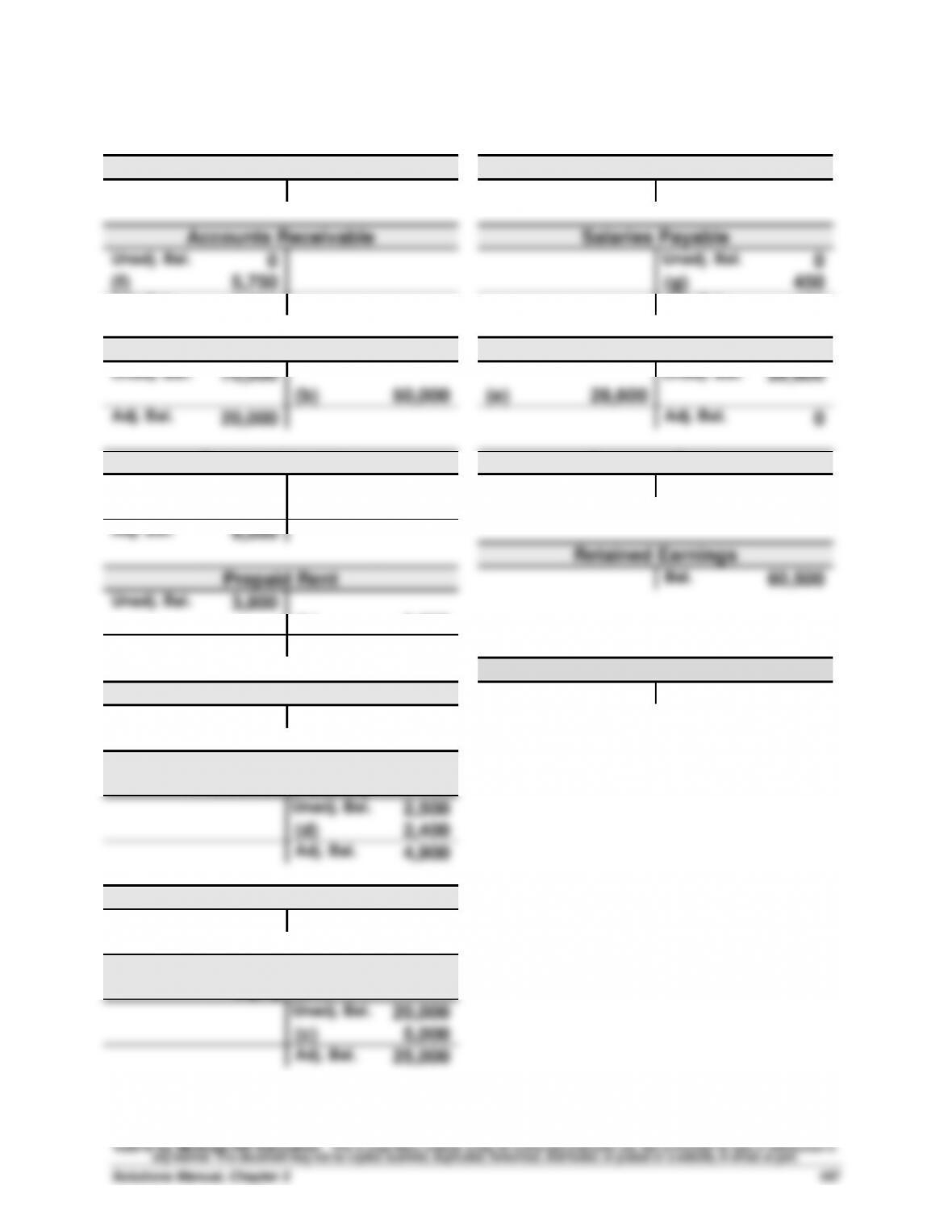

Cash

Accounts Payable

Bal.

60,000

Bal.

11,200

Accounts Receivable

Salaries Payable

Unadj. Bal.

0

Unadj. Bal.

0

(f)

5,750

(g)

450

Adj. Bal.

5,750

Adj. Bal.

450

Teaching Supplies

Unearned Training Fees

Unadj. Bal.

70,000

Unadj. Bal.

28,600

(b)

50,000

(e)

28,600

Adj. Bal.

20,000

Adj. Bal.

0

Prepaid Insurance

Common Stock

Unadj. Bal.

19,000

Bal.

11,000

(a)

9,500

Adj. Bal.

9,500

Retained Earnings

Prepaid Rent

Bal.

60,500

Unadj. Bal.

3,800

(h)

3,800

Adj. Bal.

0

Dividends

Professional Library

Bal.

20,000

Bal.

12,000

Accumulated Depreciation—

Professional Library

Unadj. Bal.

2,500

(d)

2,400

Adj. Bal.

4,900

Equipment

Bal.

40,000

Accumulated Depreciation—

Equipment

Unadj. Bal.

20,000

(c)

5,000

Adj. Bal.

25,000

Problem 3-3B (Continued)

Parts 1 and 2

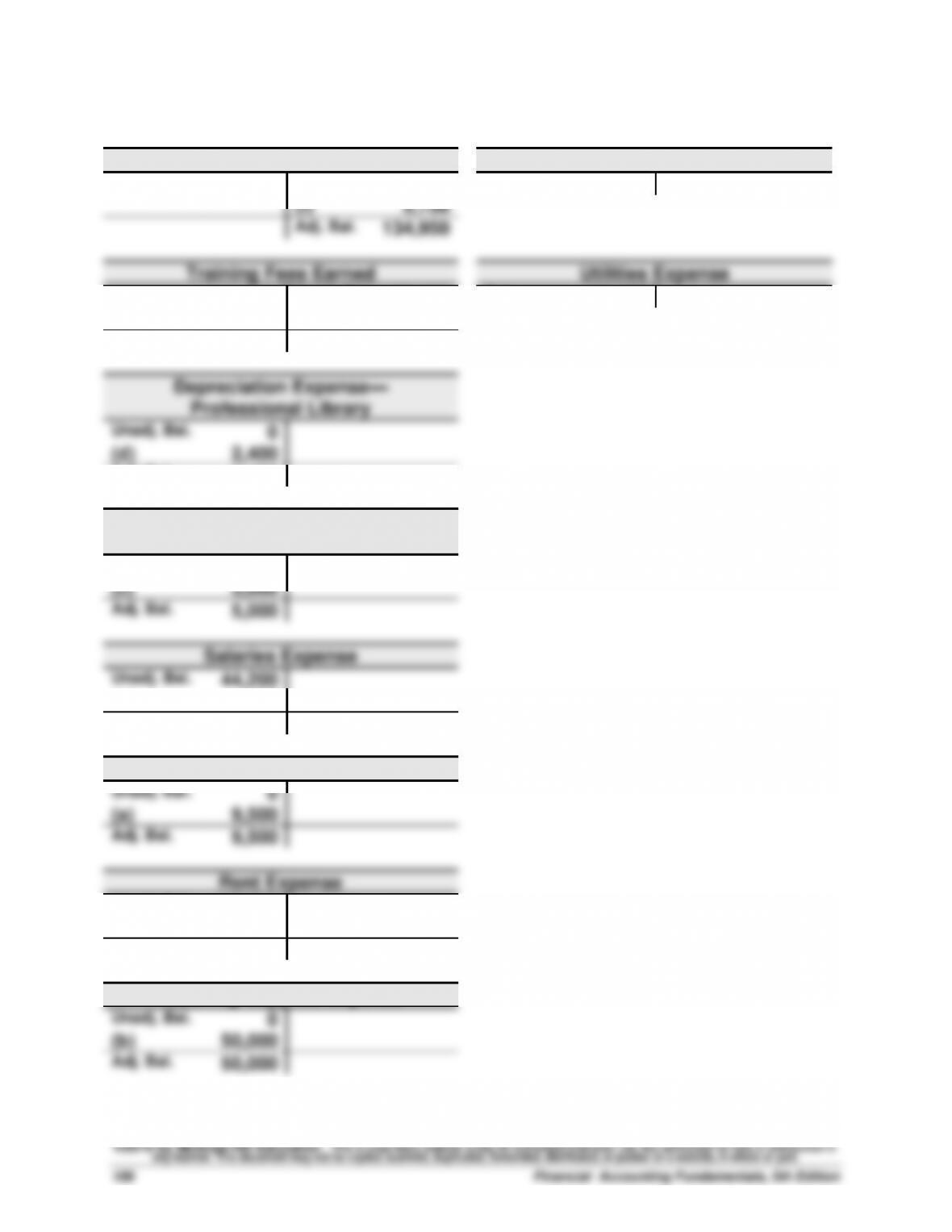

Tuition Fees Earned

Advertising Expense

Unadj. Bal.

129,200

Bal.

19,000

(f)

5,750

Adj. Bal.

134,950

Training Fees Earned

Utilities Expense

Unadj. Bal.

68,000

Bal.

13,400

(e)

28,600

Adj. Bal.

96,600

Depreciation Expense—

Professional Library

Unadj. Bal.

0

(d)

2,400

Adj. Bal.

2,400

Depreciation Expense—

Equipment

Unadj. Bal.

0

(c)

5,000

Adj. Bal.

5,000

Salaries Expense

Unadj. Bal.

44,200

(g)

450

Adj. Bal.

44,650

Insurance Expense

Unadj. Bal.

0

(a)

9,500

Adj. Bal.

9,500

Rent Expense

Unadj. Bal.

29,600

(h)

3,800

Adj. Bal.

33,400

Teaching Supplies Expense

Unadj. Bal.

0

(b)

50,000

Adj. Bal.

50,000