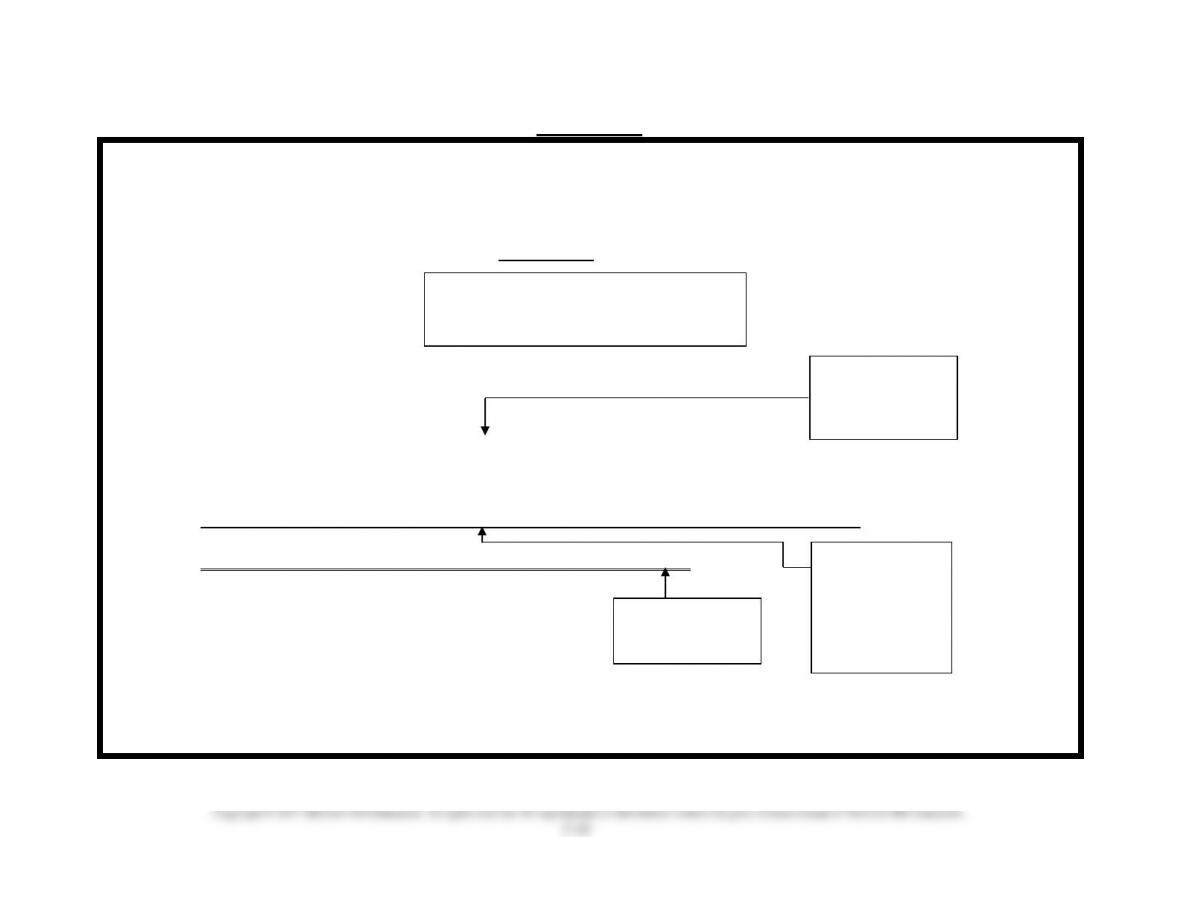

VISUAL #3-1

ACCRUAL BASIS ACCOUNTING

(Follows GAAP)

Requires that the

Income Statement

(for a period)

report

ALL REVENUES EARNED in period (Collected or Not)

Minus ALL EXPENSES INCURRED in period (Paid or Not)

Equals Net Income or Net Loss for the period

ACCOUNTS MUST BE ADJUSTED TO FOLLOW PRINCIPLES

GAAP

Revenue

Recognition

GAAP

Periodicity

GAAP

Expense

Recognition

(or Matching)

GAAP

Expense

Recognition

or Matching

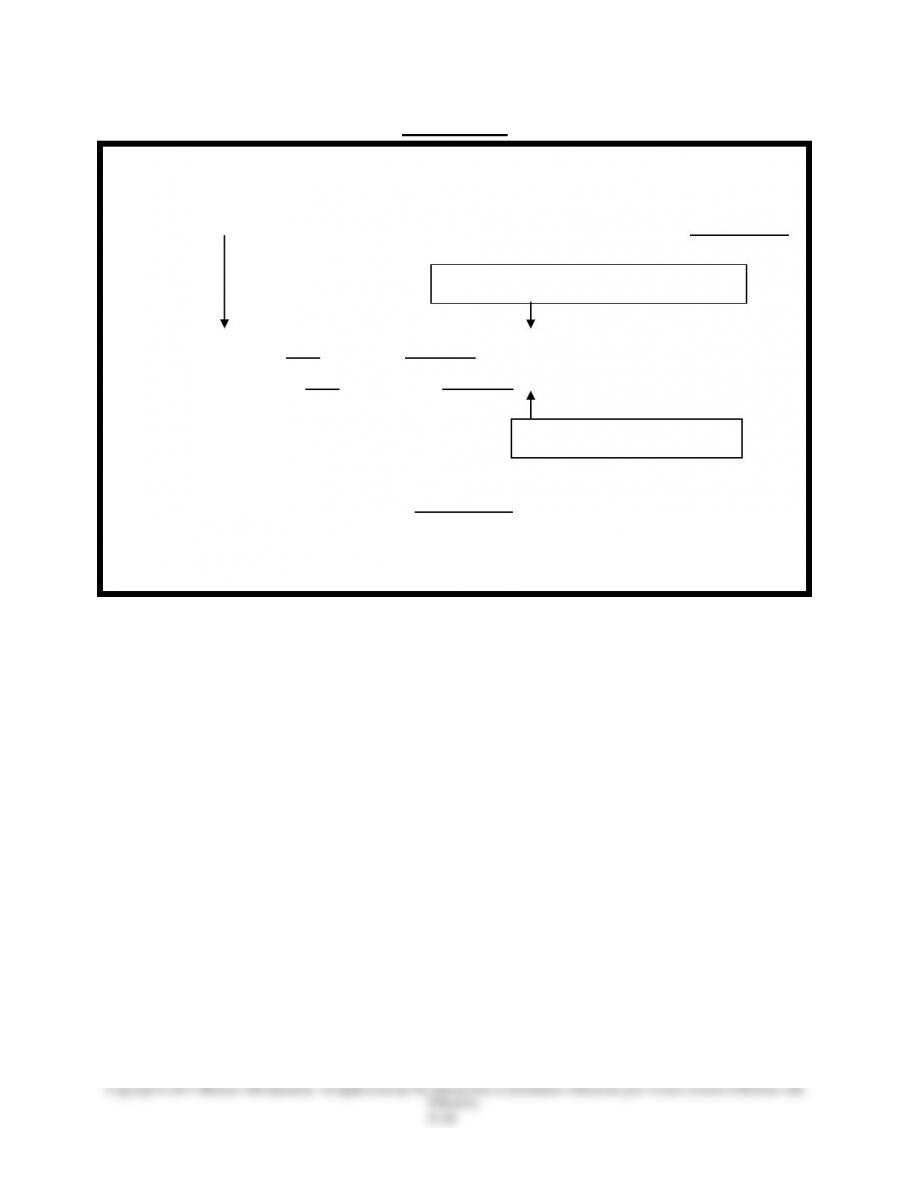

VISUAL #3-2

DEFERRALS

The converse of statements in Visual #3-1 also applies.

Revenue not earned or expense not incurred results in Deferrals*

UNEARNED = LIABILITY *

A REVENUE not earned cannot be shown, even if collected.

An EXPENSE not incurred cannot be shown, even if paid.

PREPAID = ASSET *

*We defer or postpone the reporting of the collected revenues

(as revenues) and prepaid expenses (as expenses) until the

revenue is earned and the expense is incurred.

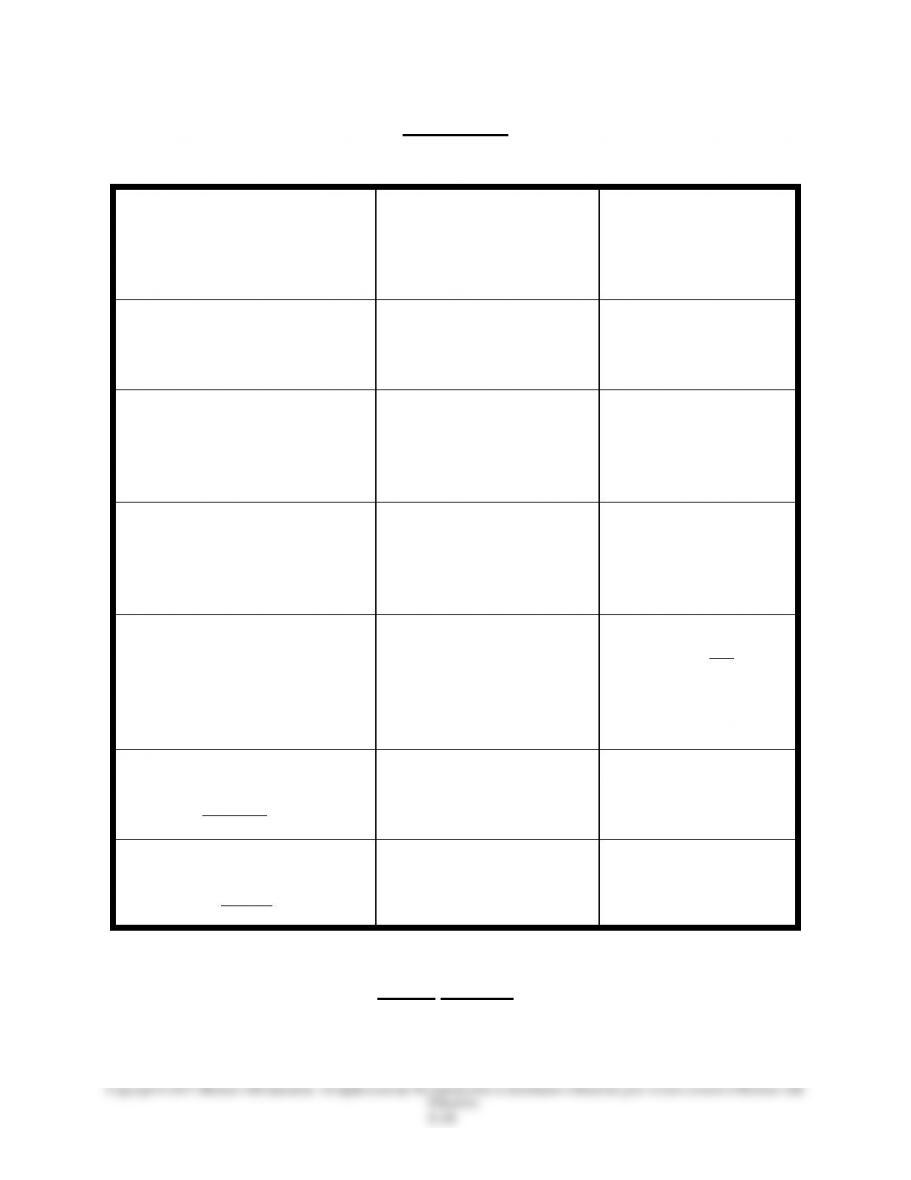

VISUAL #3-3

ADJUSTMENTS

TYPE

GENERALIZED*

ENTRY

AMOUNT

1A. Prepaid (deferred)

expenses—initially recorded as

assets

Dr. _________ Expense

Cr. the Asset* acct.

Amount used, or

consumed, or expired

1B. Prepaid (deferred)

expenses—that are depreciable

(plant assets)

Dr. Depreciation Expense

Cr. Accumulated

Depreciation

Portion of cost

allocated to this period

as depreciation

1C. Prepaid (deferred)

expenses—initially recorded as

expenses (alternate treatment—

appendix)

Dr. the Asset** acct.

Cr. ________ Expense

Amount left, or

not consumed, or

unexpired

2A. Unearned revenues—

(revenue received in advance)

initially record as liability

(unearned account)

Dr. Unearned ________

Cr. the Revenue** acct.

Amount earned to date

2B. Unearned revenues—

(revenue received in advance)

initially recorded as a revenue

(alternate treatment—

appendix)

Dr. the Revenue** acct.

Cr. Unearned________

Amount still not

earned

3. Accrued expenses—

(expenses incurred but not yet

recorded)

Dr. _________ Expense

Cr. _________ Payable

Amount accrued

4. Accrued revenues

(revenues earned but not

yet recorded)

Dr. ________ Receivable

Cr. the Revenue** acct.

Amount accrued

*Note: (1) Each adjustment affects a Balance Sheet Account and an Income

Statement Account and (2) CASH NEVER appears in an adjustment.

**Title or account name varies.

Alternate Demonstration Problem #1

Chapter Three

On July 1, 2015, Howard M. Tenant, Inc., rents office space from John Q.

Landlord for two years, starting immediately, at a rate of $100 per month, or

$2,400 in total. The full $2,400 was paid on this date. Record the original

transaction and the appropriate adjusting entries in 2015, 2016, and 2017

from the point of view of Tenant and Landlord.

Solution: Alternate Demonstration Problem #1

Chapter 3

Tenant

Landlord

7/1/15

Prepaid Rent …………….

2,400

Cash ………………………..

2,400

Cash

2,400

Unearned Rent

Rev. ………………..

2,400

12/31/15

Rent Expense …………..

600

Unearned Rent Rev.

600

Prepaid Rent ……..

600

Rent Revenue

600

12/31/16

Rent Expense …………..

1,200

Unearned Rent Rev.

1,200

*Prepaid Rent …….

1,200

Rent Revenue

1,200

12/31/17

*Rent Expense ………….

600

Unearned Rent Rev.

600

Prepaid Rent ……..

600

Rent Revenue

600

An Alternative Solution (Based on the Appendix)

Tenant

Landlord

7/1/15

Rent Expense …………..

2,400

Cash ………………………..

2,400

Cash ………………….

2,400

Rent Rev. ………….

2,400

12/31/15

Prepaid Rent ……………

1,800

Rent Rev.

1,800

Rent Expense …….

1,800

Unearned Rent

Revenue ………….

1,800

*12/31/15

Rent Expense …………..

1,200

Unearned Rent Rev.

1,200

Prepaid Rent ……..

1,200

Rent Revenue

1,200

*12/31/16

Rent Expense …………..

600

Unearned Rent Rev.

600

Prepaid Rent ……..

600

Rent Revenue

600

*Notice the adjustment is the same in 2016 and 2017 under both

approaches. This is because the adjustment in the appendix alternative

solution places all remaining unexpired/unearned amounts in the

asset/liability accounts to be considered for future adjustment.

Alternate Demonstration Problem #2

Chapter Three

The trial balance of Large Company, Inc., at the end of its annual

accounting period is as follows:

LARGE COMPANY, INC.

Trial Balance

December 31, 2015

Cash ………………………………………………………………..

$ 4,000

Accounts Receivable………………………………..

400

Prepaid Insurance ……………………………………………

1,200

Supplies …………………………………………………………

2,100

Equipment ………………………………………………………

20,000

Accumulated Depreciation—Equipment ……………

$ 2,000

Common Stock ……………………………………….

Retained earnings …………………………………………..

19,000

Dividends ………………………………………………………..

2,000

Revenue ………………………………………………………….

33,000

Salaries Expense ……………………………………………..

18,300

Rent Expense ………………………………………………….

6,000

______

Totals ………………………………………………………………

$54,000

$54,000

Additional information:

1. Expired insurance, $400.

2. Unused supplies, per inventory, $800.

3. Estimated depreciation, $1,000.

4. Earned but unpaid salaries, $700.

5. Services completed for a client by year-end but the client has not been

billed for those services, $500

Required:

Prepare adjusting entries.

Solution: Alternate Demonstration Problem #2

Chapter 3

1.

Insurance Expense …………………………………….

400

Prepaid Insurance ………………………………..

400

Supplies Expense ………………………………………

1,300

Supplies ………………………………………………

1,300

$2,100 – 800 inventory = 1,300 supplies used

Depreciation Expense Equip. ……………………..

1,000

Accumulated Depreciation Equip. …………

1,000

Salaries Expense ……………………………………….

700

Salaries Payable …………………………………..

700

Accounts Receivable …………………………………

500

Revenue ……………………………………………..

500