CHAPTER 2

ACCOUNTING FOR BUSINESSTRANSACTIONS

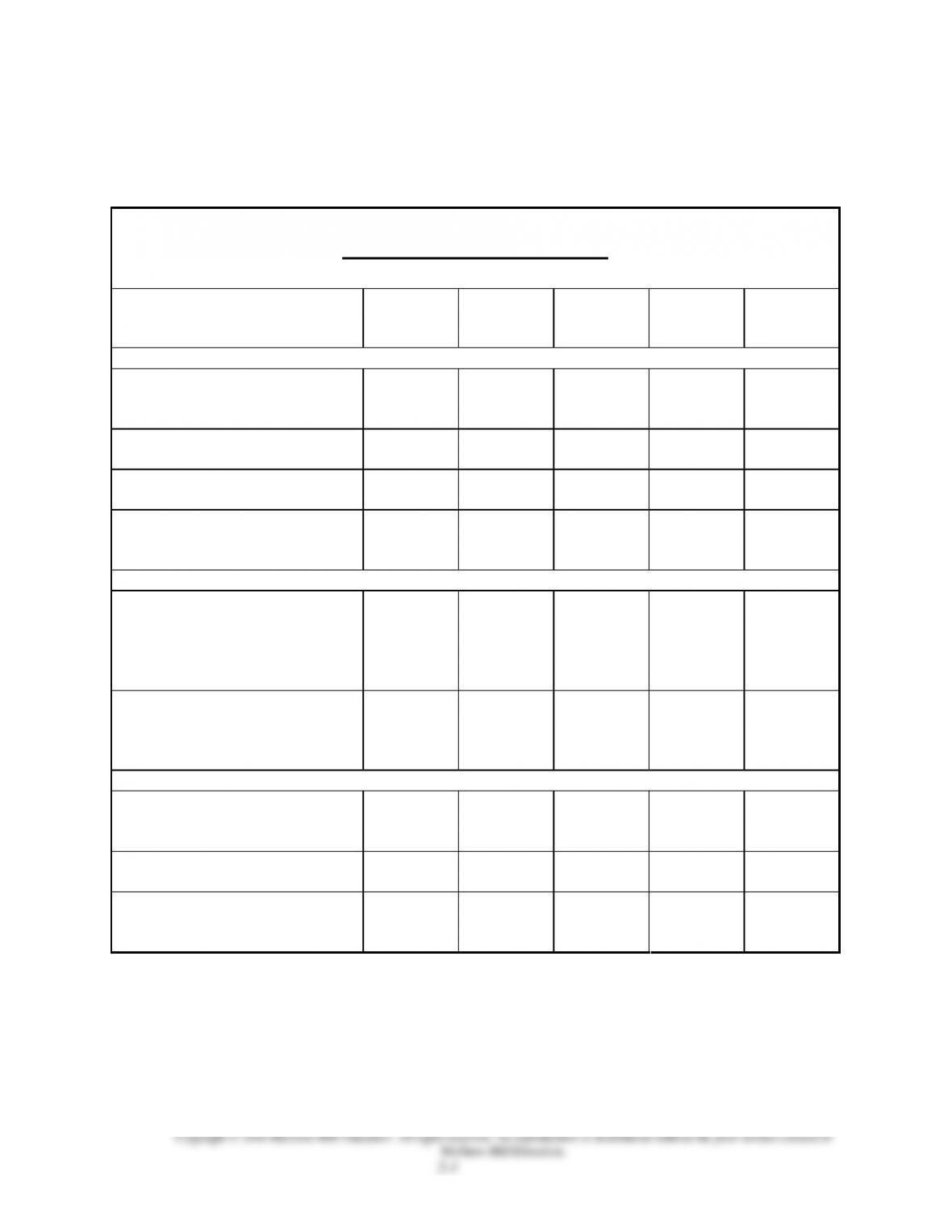

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Explain the steps in processing

transactions and the role of

source documents.

3, 6, 9

2-1

2-1

2-6

2-3, 2-4,

2-6, 2-9

C2. Describe an account and its use

in recording transactions.

1,2, 14

2-2

2-2

2-5

2-4, 2-6

C3. Describe a ledger and a chart of

accounts.

2-3

2-3, 2-16

2-1, 2-2,

2-3, 2-4, 2-6

C4. Define debits and credits and

explain their role in double-

entry accounting.

7

2-4, 2-5,

2-10

2-4

2-1, 2-2, 2-3

2-6

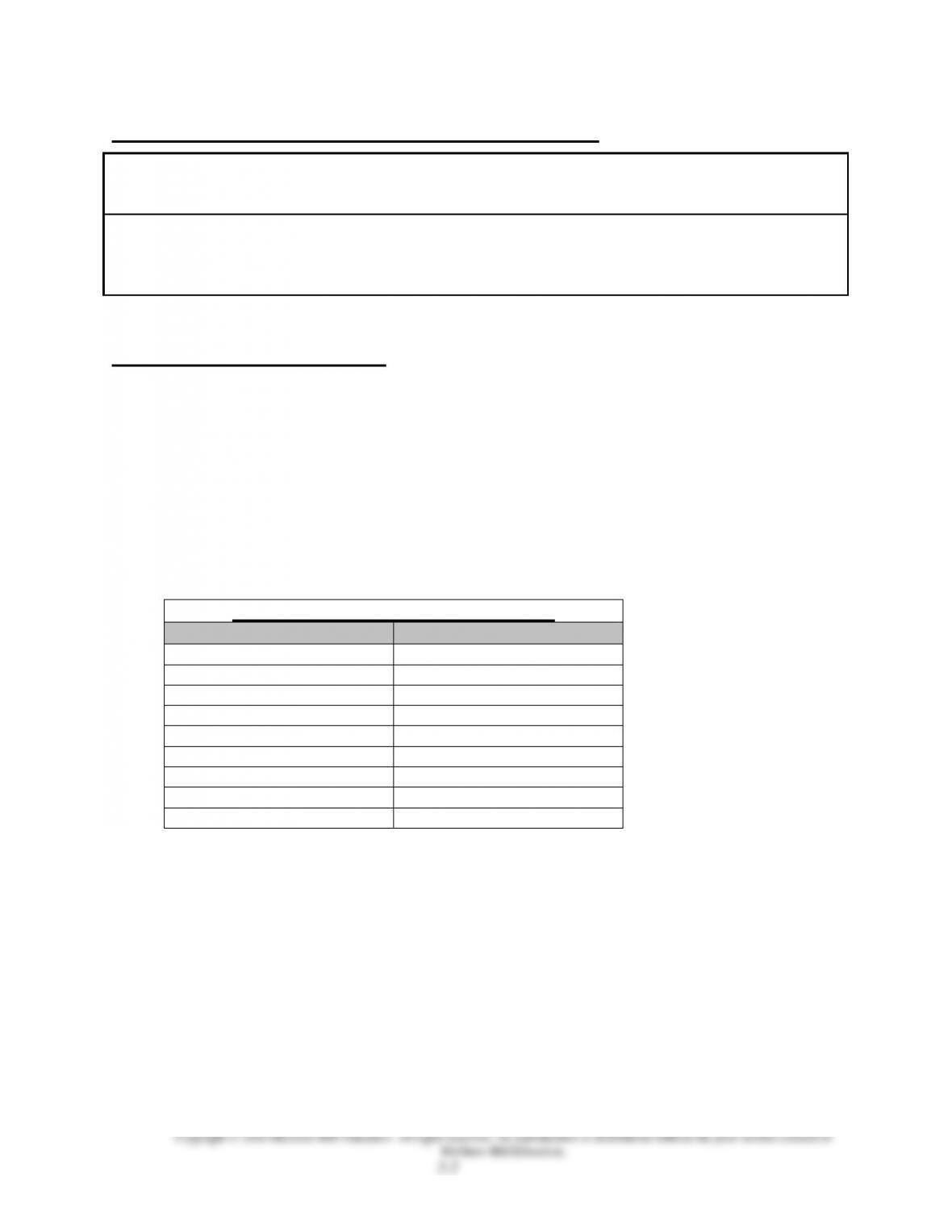

Analytical objectives:

A1. Analyze the impact of

transactions on accounts and

financial statements.

.

2-7

2-5, 2-6,

2-9, 2-11,

2-12, 2-13,

2-15, 2-20,

2-21

2-1, 2-2,

2-3, 2-4,

2-5, 2-6

2-1, 2-2,

2-4, 2-5,

2-6, 2-7,

2-8

A2. Compute the debt ratio and

describe its use in analyzing

financial condition.

2-23

2-5

2-1, 2-2,

2-7, 2-8,

2-10

Procedural objectives:

P1. Record transactions in a journal

and post entries to a ledger.

3, 4,5

2-6

2-7, 2-11,

2-12, 2-14

2-19

2-1, 2-2,

2-3, 2-4

P2. Prepare and explain the use of a

trial balance.

8

2-8

2-8, 2-10,

2-20, 2-21

2-1, 2-2,

2-3, 2-4, 2-6

P3. Prepare financial statements

from business transactions.

10, 11, 12,

13,15, 16,

17, 18

2-9

2-16, 2-17,

2-18, 2-19,

2-22

2-5

2-4, 2-7,

2-8

*See additional information on next page that pertains to these quick studies, exercises and problems.

Additional Information on Related Assignment Material

The Serial Problem for Success Systems continues in this chapter. Problems 2-3A & 2-5A can be

completed using Excel. Problem 2-1A, 2-3A, and the Serial Problem can be completed with Sage 50

Complete Accounting Software or QuickBooks Software.

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode

Synopsis of Chapter Revisions

• Akola Project: NEW opener with new entrepreneurial assignment

• New layout showing financial statements drawn from trial balance

• New preliminary coverage of classified and unclassifed balance sheets

• Changed selected numbers for FastForward

• Revised Piaggio’s (IFRS) balance sheet

• Updated debt ratio section using Skechers

Narrated PowerPoint Correlation Guide

Learning Objective

Slides

C1

2-3

C2

4-9

C3

10

C4

11-14

P1

15-18

A1

19-24

P2

25-27

P3

28-32

A2

35

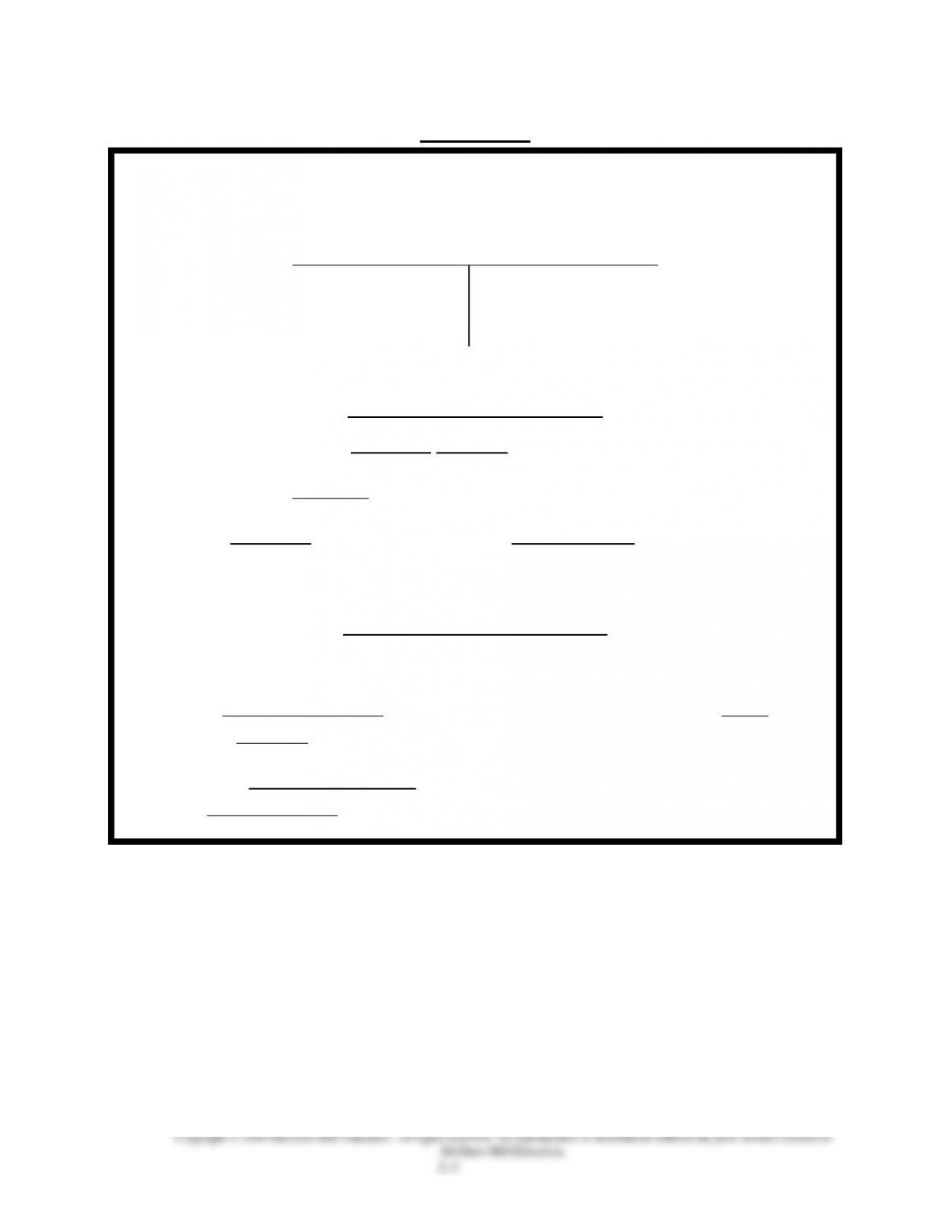

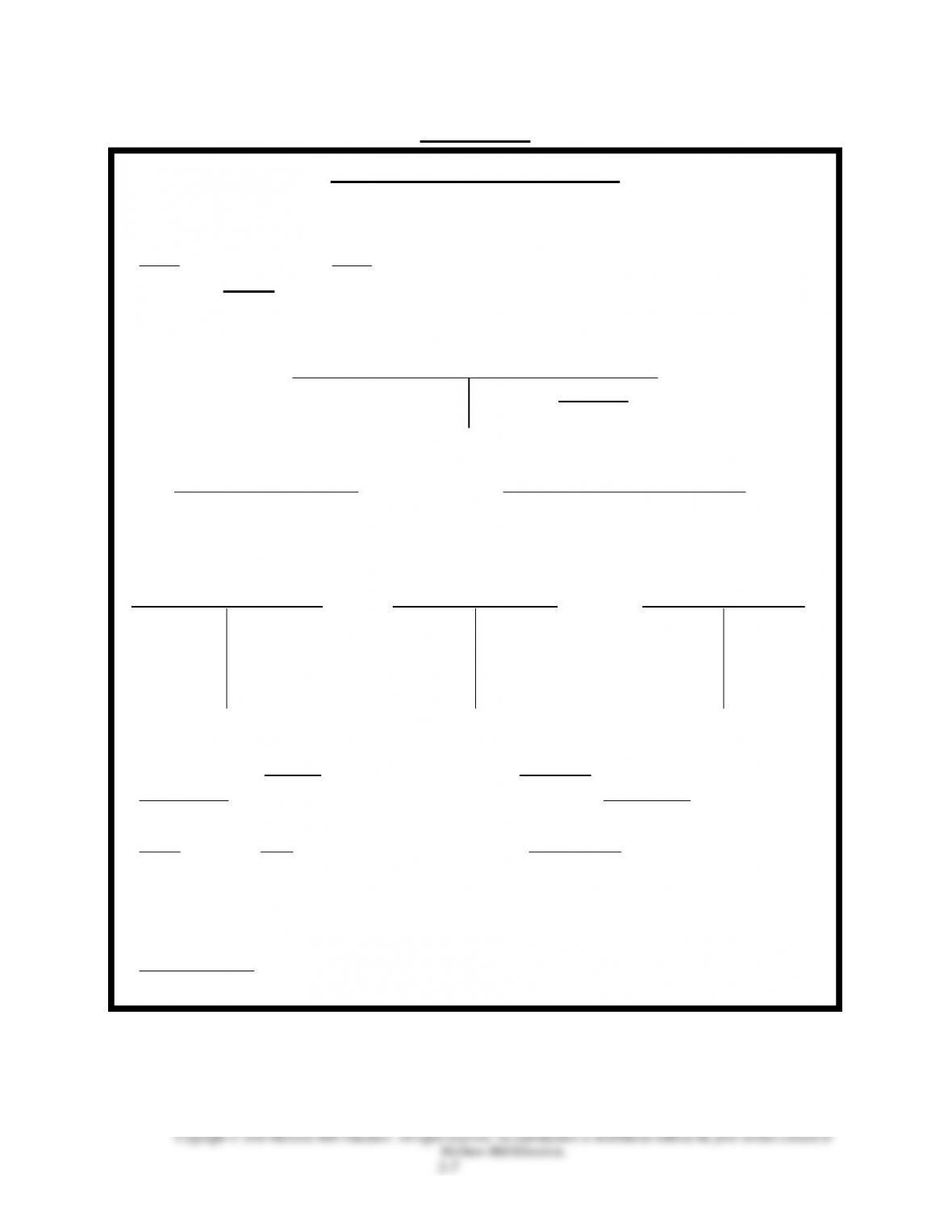

VISUAL #2-1

THREE PARTS OF AN ACCOUNT

(1) ACCOUNT TITLE

Left Side

Right Side

called

called

(2) DEBIT

(3) CREDIT

Rules for using accounts

Accounts are assigned balance sides (Debit or Credit).

To increase any account, use the balance side.

To decrease any account, use the side opposite the balance.

Finding account balances

If total debits = total credits, the account balance is zero.

If total debits are greater than total credits, the account has a debit

balance equal to the difference of the two totals.

If total credits are greater than total debits, the account has a

credit balance equal to the difference of the two totals.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

VISUAL #2-2

REAL ACCOUNTS

ALL ACCOUNTS ARE ASSIGNED BALANCE SIDES

BALANCE SIDES FOR ASSETS, LIABILITIES, AND

EQUITY ACCOUNTS ARE ASSIGNED BASED ON

SIDE OF EQUATION THEY ARE ON.

ASSETS

=

LIABILITIES + EQUITY

are on the

left side of the equation

therefore they are

are on the

right side of the equation

therefore they are

ASSIGNED LEFT SIDE

BALANCE

ASSIGNED RIGHT SIDE

BALANCE

DEBIT BALANCE

CREDIT BALANCE

All Asset Accts

All Liability Accts

All Equity Accts

Normal

Normal

Normal

Debit

Credit

Debit

Credit

Debit

Credit

Balance

Balance

Balance

+ side

– side

– side

+ side

– side

+ side

*In a sole proprietorship, there is only one equity account, which is called

capital. For that reason, the terms equity and capital are often used

interchangeably. (When corporations are discussed in detail, you will learn

many stockholders’ equity accounts.) Equity is an account classification

like assets. Owner’s Name, Capital, is the account title.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

VISUAL #2-3

TEMPORARY ACCOUNTS

Temporary accounts are established to facilitate efficient accumulation of

data for statements. Temporary accounts are established for withdrawals,

each revenue, and each expense. Temporary accounts are assigned

balances based on how they affect equity.

(Equity Account)

Owner’s Name, Capital

Debit

Credit Balance

– side

+ side

Temporary Accounts Effect on equity? E or E

Owner, Withdrawals* E = Dr

Revenues E = Cr

Expenses E = Dr

All Withdrawal Accts

All Revenue Accts

All Expense Accts

Normal

Normal

Normal

Debit

Credit

Debit

Credit

Debit

Credit

Balance

Balance

Balance

+ side

– side

– side

+ side

+ side

– side

Note:

Transactions during the period always increase the balances of these

temporary accounts since the transaction represent additional withdrawals,

revenues, and expenses. We will later learn how to move these amounts

back to the real account they affect → CAPITAL. At the end of the

accounting period, transferring withdrawals, revenues, and expenses back to

capital is the main use for the decrease side of the temporary accounts.

*The “Owner’s Name, Withdrawals” is the account title and the

classification of account is a contra-equity.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

VISUAL #2-4

USING ACCOUNTS – SUMMARY

Real Accounts

All Asset Accts

All Liability Accts

All Equity Accts

Debit +

⎯

⎯

Credit +

⎯

Credit +

Balance

Balance

Balance

RULE REVIEW

Temporary Accounts

Transaction analysis rules

• Each transaction affects at least 2

accounts.

• Each transaction must have equal

debits and credits.

All Withdrawal

Accounts

Debit +

⎯

Balance

General account use rules

• To increase any account, use balance

All Revenue Accounts

side.

⎯

Credit +

• To decrease any account, use side

Balance

opposite the balance

All Expense Accounts

Debit +

⎯

Balance