Exercise 11-10 (25 minutes)

1. (a)

Oct. 11

Treasury Stock (5,000 x $25) …………………………..

125,000

Cash ………………………………………………………………..

125,000

Purchased treasury stock.

(b)

Nov. 1

Cash (1,000 x $31) ………………………………………….……..

31,000

Treasury Stock (1,000 x $25) ……………………..……

25,000

Paid-In Capital, Treasury Stock ………………….……..

6,000

Reissued treasury stock at a price exceeding cost.

(c)

Nov. 25

Cash (4,000 x $20) ………………………………………….……..

80,000

Paid-In Capital, Treasury Stock ……………………….….

6,000

Retained Earnings ………………………………………….……..

14,000

Treasury Stock (4,000 x $25) ……………………..……

100,000

Reissued treasury stock at a price less than cost.

2. Changes to the equity section include the following

(i) The common stock account description line will change. After the

treasury stock purchase, it should read:

Common stock⎯$10 par value; 72,000 shares

authorized and issued; 5,000 shares in treasury ……………..

$720,000

The dollar balance of this account does not change with a treasury

stock purchase.

(ii) The descriptions and dollar amounts for Paid-In Capital in Excess of

Par Value, Common Stock will not change.

(iii) The retained earnings dollar balance will not change but its

description should change to read:

Retained earnings ($125,000 restricted for treasury stock) ………….

$864,000

(iv) After the purchase, a deduction for the cost of treasury stock is

reported immediately before the total line for stockholders’ equity as:

Less cost of treasury stock …………………………………………….…..

$(125,000)

(v) Total stockholders’ equity will change from $1,800,000 to $1,675,000.

Exercise 11-10 (Concluded)

Revised equity section appears as follows

Common stock⎯$10 par value; 72,000 shares authorized

and issued; 5,000 shares in treasury …………………………………….……

$ 720,000

Paid-in capital in excess of par value, Common stock ……………………

216,000

Retained earnings, $125,000 restricted by treasury stock ………………

864,000

Total ……………………………………………………………………………………………

1,800,000

Less cost of treasury stock ……………………………………………………....

(125,000)

Total stockholders’ equity ……………………………………………………….

$1,675,000

Exercise 11-11 (15 minutes)

Amos Company

Statement of Retained Earnings

For Year Ended December 31, 2015

Retained earnings, December 31, 2014, as previously reported ….

$1,375,000

Prior period adjustment

Depreciation expense not recorded in 2013 (net of $4,500 in

tax benefits) ……………………………………………………………………...

($55,500)

Retained Earnings, December 31, 2014, as adjusted ………………...

1,319,500

Plus net income ……………………………………………………………………….

126,000

Less dividends ………………………………………………………………………..

(43,000)

Retained earnings, December 31, 2015 ……………………………………..

$1,402,500

Exercise 11-12 (25 minutes)

1. Net income ………………………………………………………………………….

$2,700,000

Less preferred dividends ……………………………………………………

(388,020)

Net income available to common stockholders ………………..…

$2,311,980

2. Net income available to common stockholders ………………..…

$2,311,980

Divided by weighted-average outstanding shares …………….…

678,000

Basic earnings per share ……………………………………………………

$3.41

Exercise 11-13 (30 minutes)

1. Net income …………………………………………………………………………..

$960,000

Less preferred dividends ……………………………………………………

(120,000)

Net income available to common stockholders ……………..……

$840,000

2. Net income available to common stockholders ……………..…

$840,000

Divided by weighted-average outstanding shares ………….……

400,000

Basic earnings per share ……………………………………………………

$ 2.10

Exercise 11-14 (15 minutes)

Stock

Market Value

per Share

Divided

by

Earnings

per Share

Price-Earnings

Ratio

1…………..

$176.40

$12.00

=

14.7

2…………..

96.00

10.00

=

9.6

3…………..

93.75

7.50

=

12.5

4…………..

250.00

50.00

=

5.0

Analysis: Stocks with PE ratios less than about 5 to 8 are likely viewed as

potentially undervalued by the market. Of the stocks above, an analyst

might investigate stock #4 as possibly undervalued with a PE ratio of 5.0.

Exercise 11-15 (15 minutes)

Dividend yield

1. $16.06 / $220.00 = 7.3%

Exercise 11-16 (20 minutes)

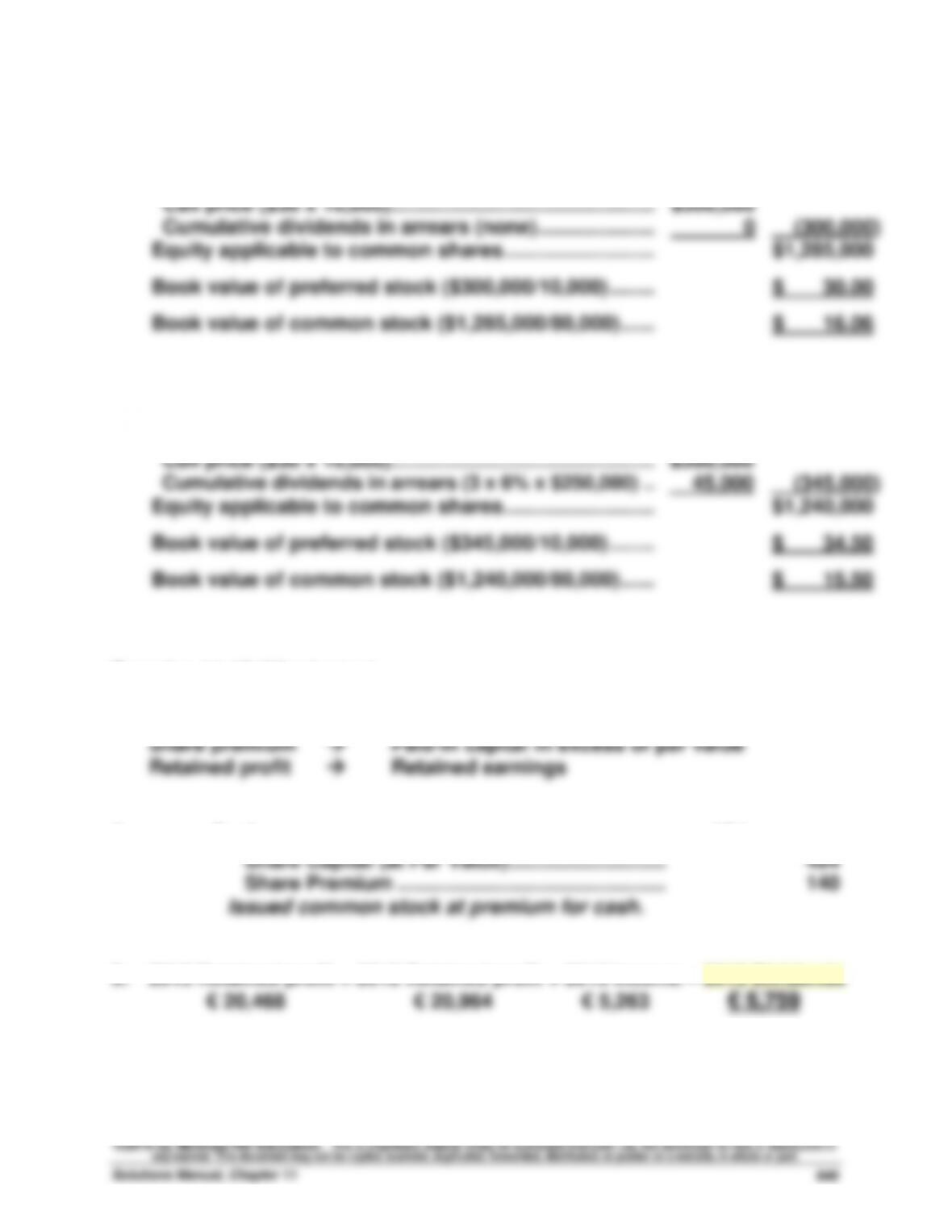

1.

Total stockholders’ equity …………………………..………….

$1,585,000

Less equity applicable to preferred shares

Call price ($30 x 10,000) ………………………………………..

$300,000

Cumulative dividends in arrears (none) …………………

0

(300,000)

Equity applicable to common shares ………………………

$1,285,000

Book value of preferred stock ($300,000/10,000) ……..

$ 30.00

Book value of common stock ($1,285,000/80,000) ……

$ 16.06

2.

Total stockholders’ equity …………………………..………….

$1,585,000

Less equity applicable to preferred shares

Call price ($30 x 10,000) ………………………………………..

$300,000

Cumulative dividends in arrears (3 x 6% x $250,000) ..

45,000

(345,000)

Equity applicable to common shares ………………………

$1,240,000

Book value of preferred stock ($345,000/10,000) ……..

$ 34.50

Book value of common stock ($1,240,000/80,000) ……

$ 15.50

Exercise 11-17 (20 minutes)

1. Share capital → Common stock

2.

Cash ………………………………………………………………..

624

Share Capital (at Par Value) ………………………...

484

Share Premium …………………………………………..

140

Issued common stock at premium for cash.

3. 2013 Retained profit = 2012 Retained profit + 2013 Income – 2013 Dividends

Exercise 11-18 (40 minutes)

Part 1

Jan. 2

Treasury Stock, Common ……………………………….……..

75,000

Cash ………………………………………………………………..

75,000

Purchased treasury stock (3,000 x $25).

Jan. 7

Retained Earnings ………………………………………….……..

40,500

Common Dividend Payable ……………………….….

40,500

Declared $1.50 dividend per share on 27,000

outstanding shares.

Feb. 28

Common Dividend Payable …………………………….……..

40,500

Cash ………………………………………………………………..

40,500

Paid cash dividend.

July 9

Cash* ……………………………………………………………..……..

36,000

Treasury Stock, Common** ……………………….….

30,000

Paid-In Capital, Treasury Stock*** ……………..……..

6,000

Reissued treasury stock.

*(1,200 x $30) **(1,200 x $25) ***(1,200 x $5)

Aug. 27

Cash* ……………………………………………………………..……..

30,000

Paid-In Capital, Treasury Stock ……………………….….

6,000

Retained Earnings ………………………………………….……..

1,500

Treasury Stock, Common** ……………………….….

37,500

Reissued treasury stock.

*(1,500 x $20) **(1,500 x $25)

Sept. 9

Retained Earnings ………………………………………….……..

59,400

Common Dividend Payable ……………………….….

59,400

Declared $2 dividend on 29,700 outstanding shares.

Oct. 22

Common Dividend Payable …………………………….……..

59,400

Cash ………………………………………………………………..

59,400

Paid cash dividend.

Dec. 31

Income Summary …………………………………………………..

52,000

Retained Earnings …………………………………….……..

52,000

Closed Income Summary account.

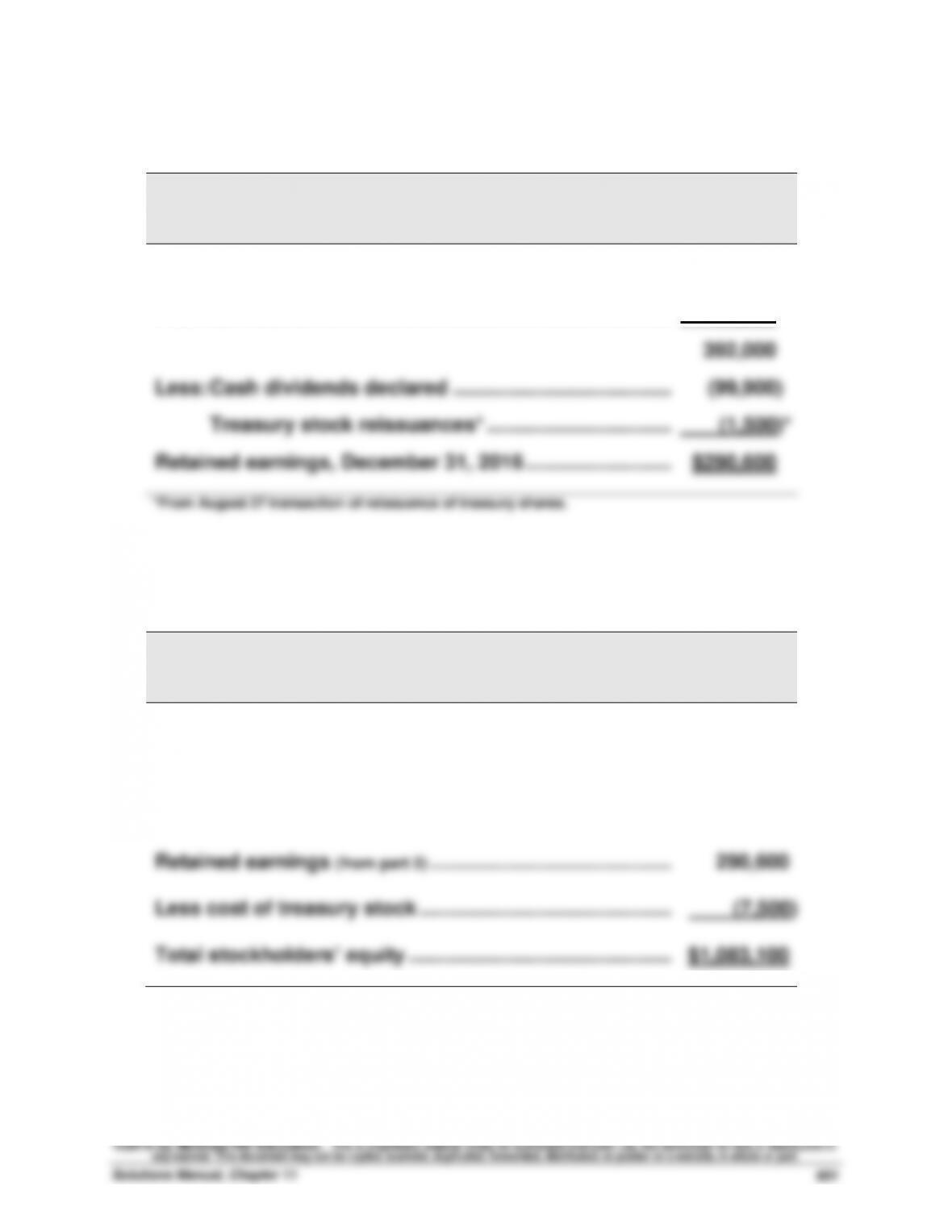

Exercise 11–18 (Concluded)

Part 2

ALEXANDER CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2016

Retained earnings, December 31, 2015 ……………………...

$340,000

Plus net income ……………………………………………………….

52,000

392,000

Less: Cash dividends declared ………………………………….

(99,900)

Treasury stock reissuances* …………………………….

(1,500)*

Retained earnings, December 31, 2016 ……………………...

$290,600

*From August 27 transaction of reissuance of treasury shares.

Part 3

ALEXANDER CORPORATION

Stockholders’ Equity Section of the Balance Sheet

December 31, 2016

Common stock⎯$25 par value, 50,000 shares

authorized, 30,000 shares issued and outstanding;

300 shares in treasury …………………………………………….

$ 750,000

Paid-in capital in excess of par value, common stock ...

50,000

Retained earnings (from part 2) ……………………………………..

290,600

Less cost of treasury stock ……………………………………….

(7,500)

Total stockholders’ equity ………………………………………...

$1,083,100

PROBLEM SET A

Problem 11-1A (30 minutes)

Part 1

a. To record sale of 10,000 ($250,000/$25 per share) shares of $25 par

value common stock for $30 ($300,000/10,000 shares) per share.

Part 2

Number of outstanding shares

Issued in (a) …………………………………

10,000

Issued in (b) …………………………………

5,000

Issued in (c) …………………………………

2,000

Issued in (d) …………………………………

3,000

Total …………………………………………….

20,000

Part 3

Part 4

Total paid-in capital from common stockholders

From transaction (a) ……………………

$300,000

From transaction (b) ……………………

150,000

From transaction (c) ……………………

80,000

From transaction (d) ……………………

120,000

Total paid-in capital …………………….

$650,000

Part 5

Problem 11-2A (60 minutes)

Part 1

Jan. 1

Treasury Stock, Common ……………………………….……..

80,000

Cash ………………………………………………………………..

80,000

Purchased treasury stock (4,000 x $20).

Jan. 5

Retained Earnings ………………………………………….……..

72,000

Common Dividend Payable ……………………….….

72,000

Declared $2 dividend on 36,000 outstanding shares.

Feb. 28

Common Dividend Payable …………………………….……..

72,000

Cash ………………………………………………………………..

72,000

Paid cash dividend.

July 6

Cash* ……………………………………………………………..……..

36,000

Treasury Stock, Common** ……………………….….

30,000

Paid-In Capital, Treasury Stock*** ……………..……..

6,000

Reissued treasury stock.

*(1,500 x $24) **(1,500 x $20) ***(1,500 x $4)

Aug. 22

Cash* ……………………………………………………………..……..

42,500

Paid-In Capital, Treasury Stock ……………………….….

6,000

Retained Earnings ………………………………………….……..

1,500

Treasury Stock, Common** ……………………….….

50,000

Reissued treasury stock.

*(2,500 x $17) **(2,500 x $20)

Sept. 5

Retained Earnings ………………………………………….……..

80,000

Common Dividend Payable ……………………….….

80,000

Declared $2 dividend on 40,000 outstanding shares.

Oct. 28

Common Dividend Payable …………………………….……..

80,000

Cash ………………………………………………………………..

80,000

Paid cash dividend.

Dec. 31

Income Summary …………………………………………………..

388,000

Retained Earnings …………………………………….……..

388,000

Closed Income Summary account.

Problem 11-2A (Concluded)

Part 2

KOHLER CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2016

Retained earnings, December 31, 2015 ……………………...

$270,000

Plus net income ……………………………………………………….

388,000

658,000

Less: Cash dividends declared ………………………………….

(152,000)

Treasury stock reissuances ……………………………..

(1,500)

Retained earnings, December 31, 2016 ……………………...

$504,500

Part 3

KOHLER CORPORATION

Stockholders’ Equity Section of the Balance Sheet

December 31, 2016

Common stock⎯$10 par value, 100,000 shares

authorized, 40,000 shares issued and outstanding …..

$400,000

Paid-in capital in excess of par value, common stock ..

60,000

Retained earnings (from part 2) ……………………………………..

504,500

Total stockholders’ equity ………………………………………...

$964,500

Problem 11-3A (45 minutes)

Part 1

Explanations for each of the journal entries

Oct. 2

Declared a cash dividend of $2 per share of common stock.

($60,000 / 30,000 shares)

Oct. 25

Paid the cash dividend on common stock.

Oct. 31

Declared a 10% stock dividend when the market value is $25 per

share. ($36,000/$12 par = 3,000 shares = 10% of 30,000 shares;

$75,000/3,000 shares = $25 per share)

Nov. 5

Distributed the common stock dividend.

Dec. 1

Executed a 3-for-1 stock split. ($12 par / $4 par = 3-for-1 ratio)

Dec. 31

Closed the Income Summary account to Retained Earnings.

Part 2

Oct. 2

Oct. 25

Oct. 31

Nov. 5

Dec. 1

Dec. 31

Common stock ………....

$360,000

$360,000

$360,000

$396,000

$396,000

$396,000

Common stock

dividend distributable

0

0

36,000

0

0

0

Paid-in capital in

excess of par …………..

90,000

90,000

129,000

129,000

129,000

129,000

Retained earnings ……..

260,000

260,000

185,000

185,000

185,000

395,000

Total equity ……………....

$710,000

$710,000

$710,000

$710,000

$710,000

$920,000

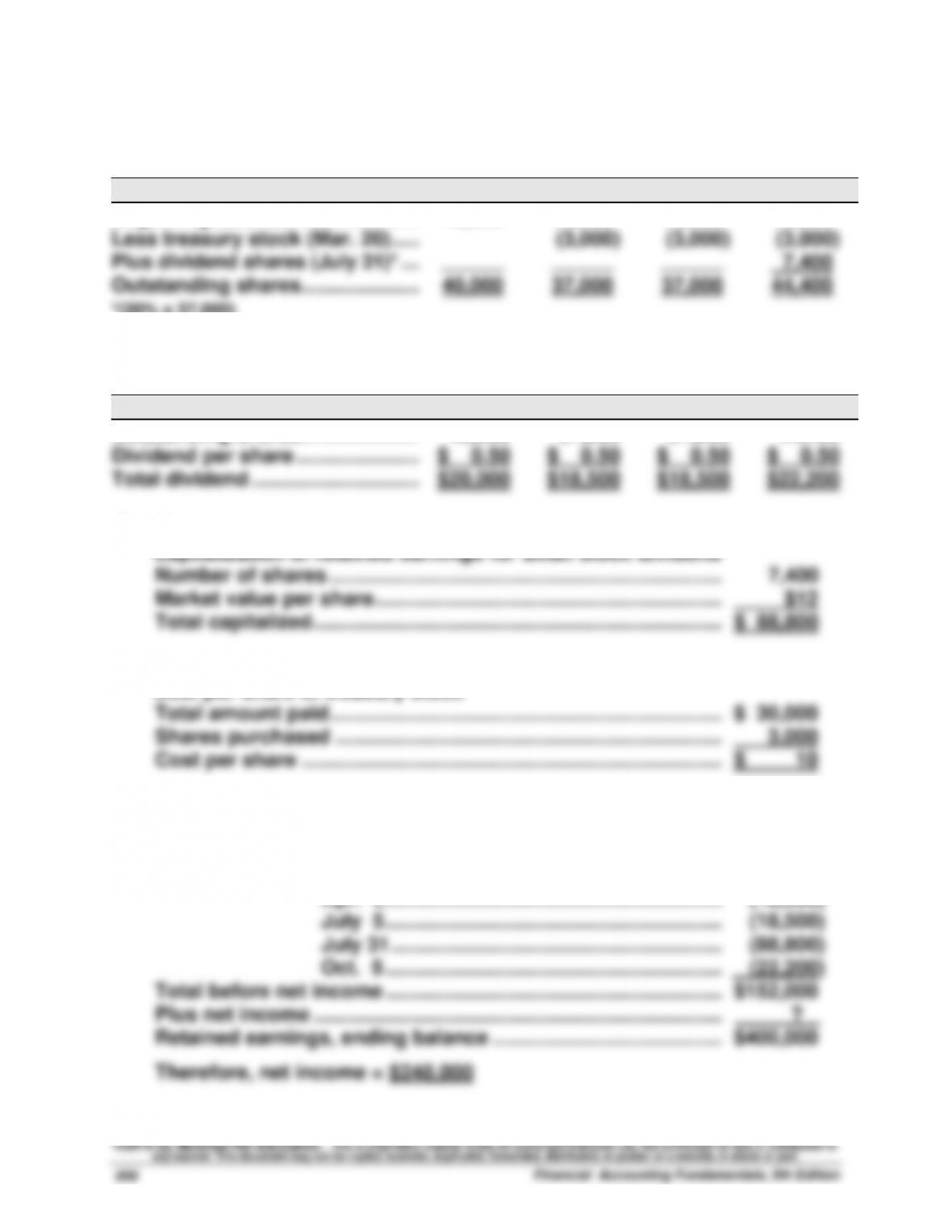

Problem 11-4A (45 minutes)

Part 1

Outstanding common shares

Jan. 5

Apr. 5

July 5

Oct. 5

Beginning balance ………………….…

40,000

40,000

40,000

40,000

Less treasury stock (Mar. 20) …..…

(3,000)

(3,000)

(3,000)

Plus dividend shares (July 31)* ….…

______

______

______

7,400

Outstanding shares ……………………

40,000

37,000

37,000

44,400

*(20% x 37,000)

Part 2

Cash dividend amounts

Jan. 5

Apr. 5

July 5

Oct. 5

Outstanding shares ………………….

40,000

37,000

37,000

44,400

Dividend per share …………………..

$ 0.50

$ 0.50

$ 0.50

$ 0.50

Total dividend ………………………….

$20,000

$18,500

$18,500

$22,200

Part 3

Number of shares ……………………………………………………………...

7,400

Market value per share ……………………………………………………....

$12

Total capitalized ………………………………………………………………...

$ 88,800

Part 4

Cost per share of treasury stock

Total amount paid ……………………………………………………………...

$ 30,000

Shares purchased ……………………………………………………………..

3,000

Cost per share …………………………………………………………………..

$ 10

Part 5

Net income

Retained earnings, beginning balance ………………………………..

$320,000

Less dividends: Jan. 5 ……………………………………………………..

(20,000)

Apr. 5 ……………………………………………………..

(18,500)

July 5 ……………………………………………………..

(18,500)

July 31 …………………………………………………....

(88,800)

Oct. 5 ……………………………………………………..

(22,200)

Total before net income ……………………………………………………..

$152,000

Plus net income ………………………………………………………………...

?

Retained earnings, ending balance …………………………………....

$400,000

Therefore, net income = $248,000

Problem 11-5A (40 minutes)

1. Market price = $85 per share (current stock exchange price given)

2. Computation of par values of stock

3. Book values with no dividends in arrears

Book value per preferred share = par value (when not callable) = $50

Common stock

Total equity ………………………………………...

$280,000

Less equity for preferred ……………………..

(50,000)

Common stock equity ………………………….

$230,000

Number of outstanding shares …………….

4,000

Book value per common share …………….

$ 57.50

($230,000 / 4,000 shares)

4. Book values with two years’ dividends in arrears

Preferred stock

Preferred stock par value ………………………

$ 50,000

Plus two years’ dividends in arrears* ….…

5,000

Preferred equity ………………………………….…

$ 55,000

*2 years’ dividends = 2 x ($50,000 x 5%) = $5,000

Number of outstanding shares ………………

1,000

Book value per preferred share …………..…

$ 55.00

($55,000 / 1,000 shares)

Common stock

Total equity ………………………………………..…

$280,000

Less equity for preferred …………………….…

(55,000)

Common stock equity …………………………..

$225,000

Number of outstanding shares ………………

4,000

Book value per common share ………………

$ 56.25

($225,000/4,000 shares)

Problem 11-5A (Concluded)

5. Book values with call price and two years’ dividends in arrears

Preferred stock

Preferred stock call price (1,000 x $55) …….

$ 55,000

Plus two years’ dividends in arrears* ………

5,000

Preferred equity ………………………………………

$ 60,000

*2 years’ dividends = 2 x ($50,000 x 5%) = $5,000

Number of outstanding shares ………………..

1,000

Book value per preferred share ……………….

$ 60.00

($60,000 / 1,000 sh.)

Common stock

Total equity …………………………………………….

$280,000

Less equity for preferred …………………………

(60,000)

Common stock equity ……………………………..

$220,000

Number of outstanding shares ………………..

4,000

Book value per common share ………………..

$ 55.00

($220,000 / 4,000 sh.)

6. Dividend allocation in total

Preferred

Common

Total

2 years’ dividends in arrears ………..

$ 5,000

$ 0

$ 5,000

Current year dividends …………….…..

2,500

2,500

Remainder to common …………….…..

.

4,000

4,000

Totals …………………………………………..

$ 7,500

$ 4,000

$11,500

7. Equity represents the residual interest of owners in the assets of the

business after subtracting claims of creditors. With few exceptions,

these assets and liabilities are reported at historical cost, not market

PROBLEM SET B

Problem 11-1B (30 minutes)

Part 1

a. To record sale of 3,000 ($3,000/$1 per share) shares of $1 par value

common stock for $40 ($120,000/3,000) per share.

b. To record issuance of 1,000 ($1,000/$1 per share) shares of $1 par value

common stock to the company’s promoters for their efforts in

per share.

Part 2

Number of outstanding shares

Issued in (a) …………………………………...

3,000

Issued in (b)…………………………………...

1,000

Issued in (c) …………………………………...

800

Issued in (d)…………………………………...

1,200

Total ……………………………………………...

6,000

Part 3

Minimum legal capital = Outstanding shares x Par value per share

Part 4

Total paid-in capital from common stockholders

From transaction (a) ……………………....

$120,000

From transaction (b) ……………………....

40,000

From transaction (c) ……………………....

40,000

From transaction (d) ……………………....

60,000

Total paid-in capital ………………………..

$260,000

Part 5

Book value per common share

Total stockholders’ equity (given) …..

$283,000

Outstanding shares (from 2) …………..

6,000

Book value per common share ……....

$ 47.17

($283,000 / 6,000 shares)

Problem 11-2B (60 minutes)

Part 1

Jan. 10

Treasury Stock, Common ………………………………………

480,000

Cash ………………………………………………………..………

480,000

Purchased treasury stock (40,000 x $12).

Mar. 2

Retained Earnings …………………………………………………

240,000

Common Dividend Payable …………………………..

240,000

Declared $1.50 dividend on 160,000 outstanding shares.

Mar. 31

Common Dividend Payable ……………………………………

240,000

Cash ………………………………………………………..………

240,000

Paid cash dividend.

Nov. 11

Cash* …………………………………………………………….………

312,000

Treasury Stock, Common** …………………………..

288,000

Paid-In Capital, Treasury Stock*** ……………..………

24,000

Reissued treasury stock.

*(24,000 x $13) **(24,000 x $12) ***(24,000 x $1)

Nov. 25

Cash* …………………………………………………………….………

152,000

Paid-In Capital, Treasury Stock …………………………..

24,000

Retained Earnings …………………………………………………

16,000

Treasury Stock, Common** …………………………..

192,000

Reissued treasury stock.

*(16,000 x $9.50) **(16,000 x $12)

Dec. 1

Retained Earnings …………………………………………………

500,000

Common Dividend Payable …………………………..

500,000

Declared $2.50 dividend on 200,000 outstanding shares.

Dec. 31

Income Summary …………………………………………………..

1,072,000

Retained Earnings ………………………………….………..

1,072,000

Closed Income Summary account.