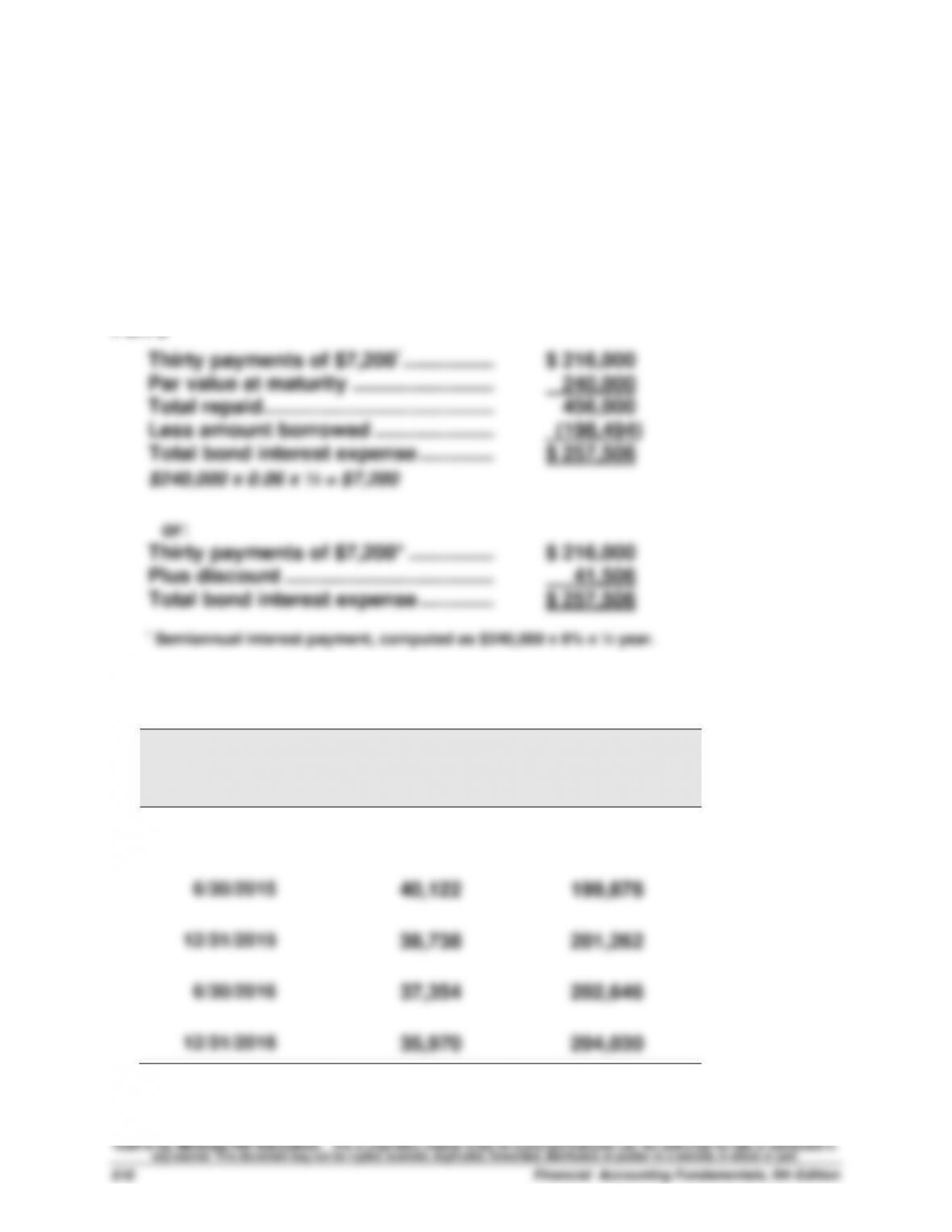

Problem 10-1B (Concluded)

Part 3

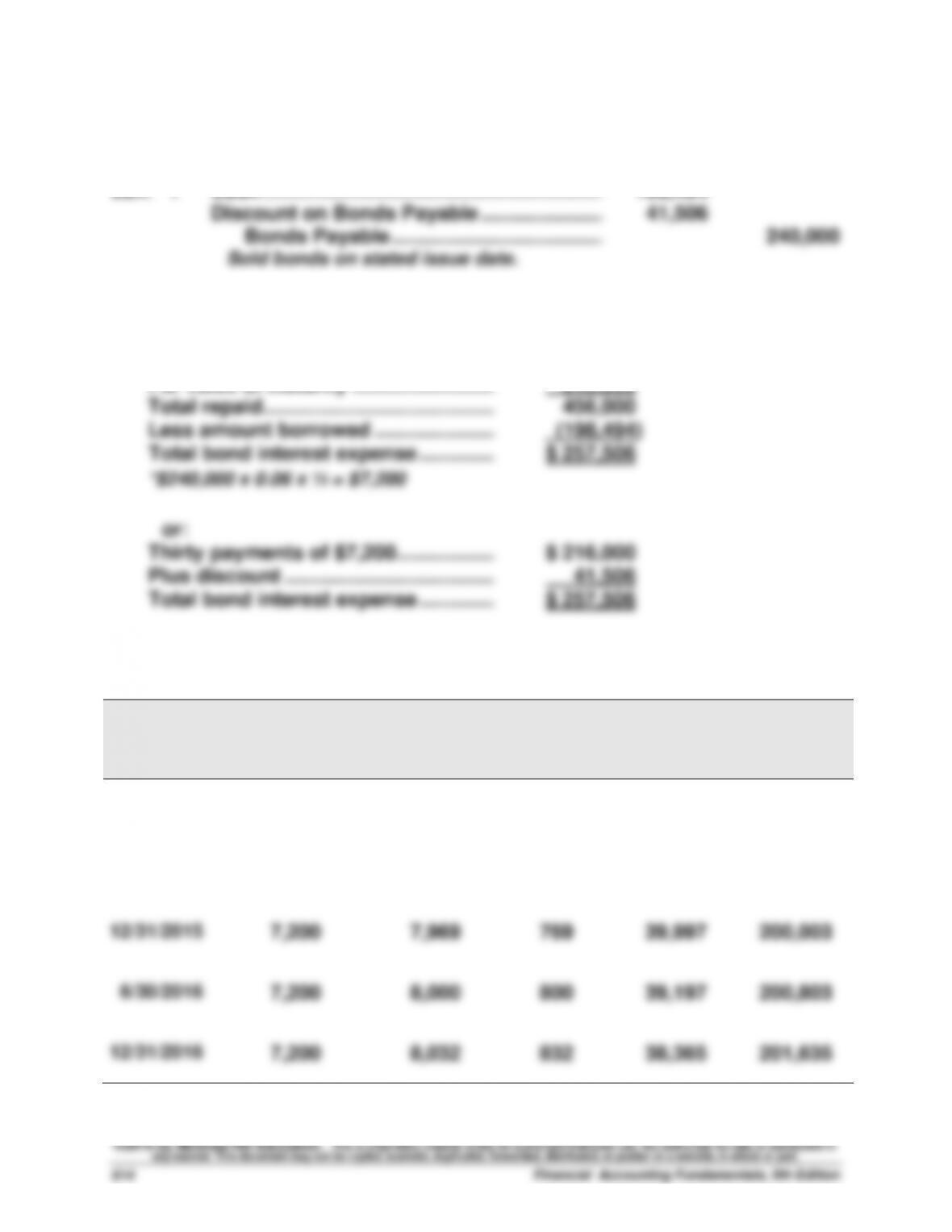

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ……………..

B.1

0.5083

$90,000

$45,747

Interest (annuity) ….

B.3

7.0236

5,400

37,927

Price of bonds ……..

$83,674

Bond discount ……..

$ 6,326

* Table values are based on a discount rate of 7% (half the annual market rate)

and 10 periods (semiannual payments).

b.

2015

Jan. 1

Cash ……………………………………………………....

83,674

Discount on Bonds Payable …………………..………

6,326

Bonds Payable …………………………………………………

90,000

Sold bonds on stated issue date.

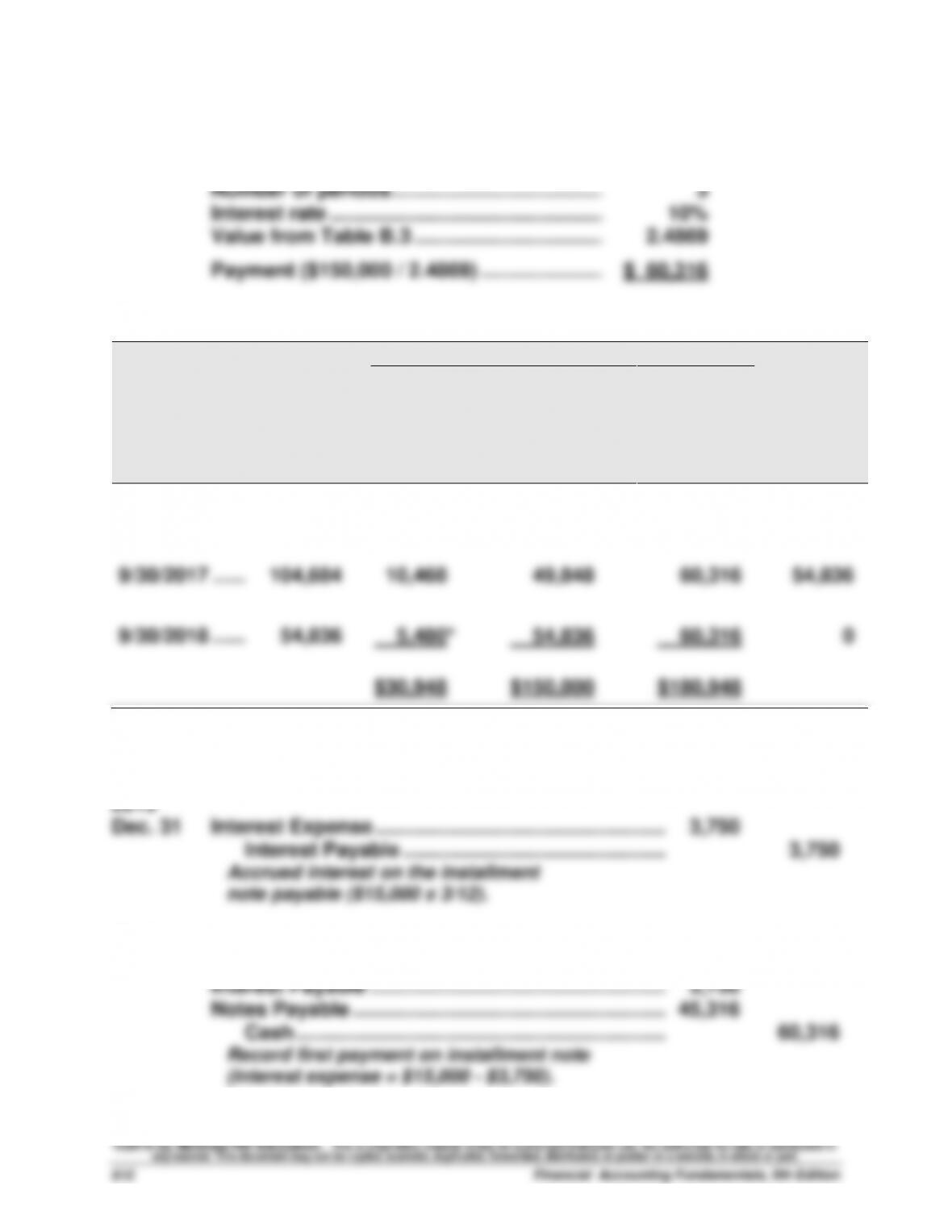

Problem 10-2B (40 minutes)

Part 1

2015

Jan. 1

Cash ……………………………………………………....

3,010,000

Discount on Bonds Payable …………………..………

390,000

Bonds Payable …………………………………………………

3,400,000

Sold bonds on stated issue date.

Part 2

[Note: The semiannual amounts for (a), (b), and (c) below are the same throughout

the bonds’ life because the company uses straight-line amortization.]

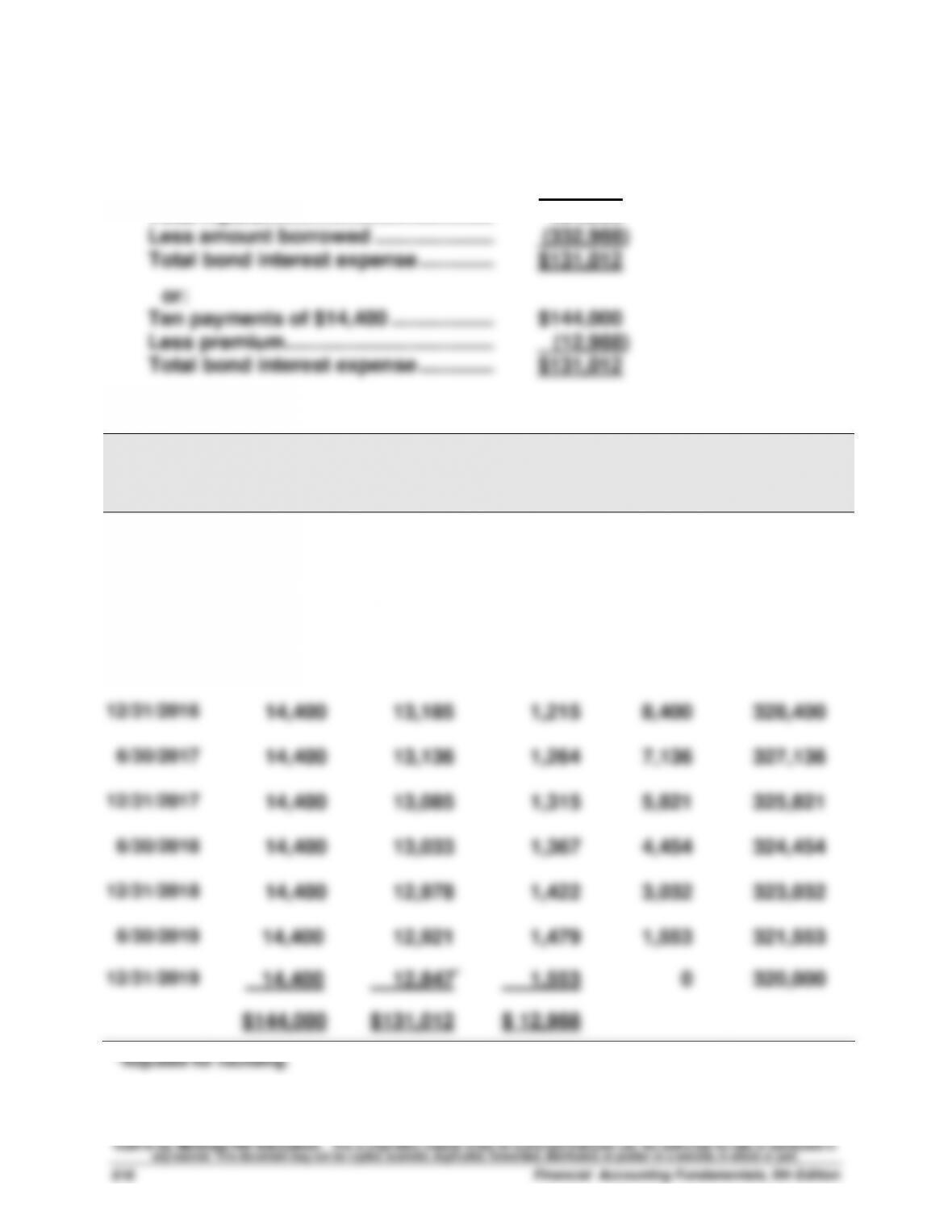

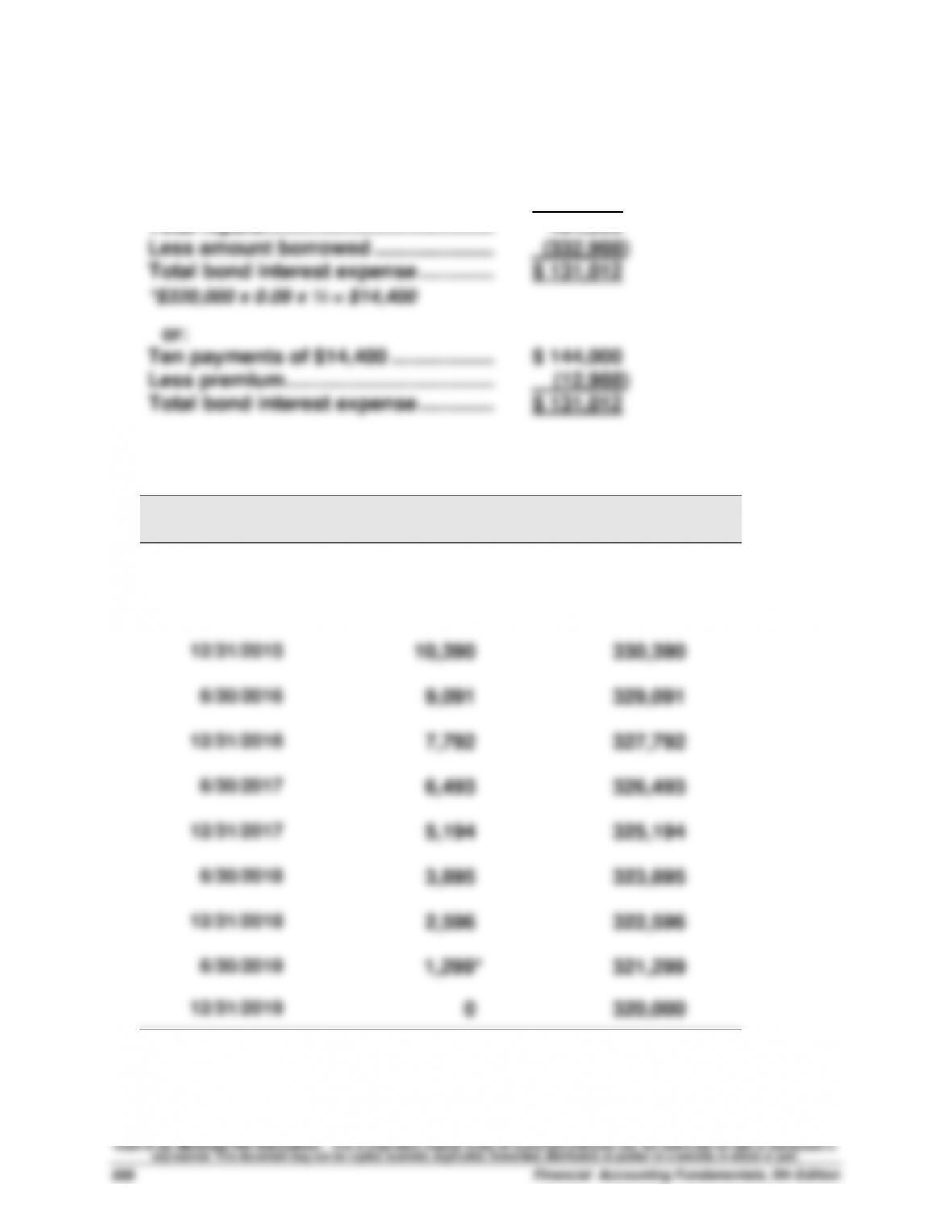

Problem 10-4B (Concluded)

Part 3

2015

June 30

Bond Interest Expense …………………………..

13,101

Premium on Bonds Payable ………………….……….

1,299

Cash ……………………………………………….………

14,400

To record six months’ interest and

premium amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

13,101

Premium on Bonds Payable ………………….……….

1,299

Cash ……………………………………………….………

14,400

To record six months’ interest and

premium amortization.