Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 10-3A (Concluded)

Part 4

Semiannual

Period-End

Unamortized

Premium

Carrying

Value

1/01/2015 .....................

$895,980

$4,895,980

6/30/2015 .....................

866,114

4,866,114

12/31/2015 .....................

836,248

4,836,248

6/30/2016 .....................

806,382

4,806,382

12/31/2016 .....................

776,516

4,776,516

Part 5

2015

June 30

Bond Interest Expense ................................

90,134

Premium on Bonds Payable ................................

29,866

Cash ................................................................

120,000

To record six months’ interest and

premium amortization.

2015

Dec. 31

Bond Interest Expense ................................

90,134

Premium on Bonds Payable ................................

29,866

Cash ................................................................

120,000

To record six months’ interest and

premium amortization.

Problem 10-4A (45 minutes)

Part 1

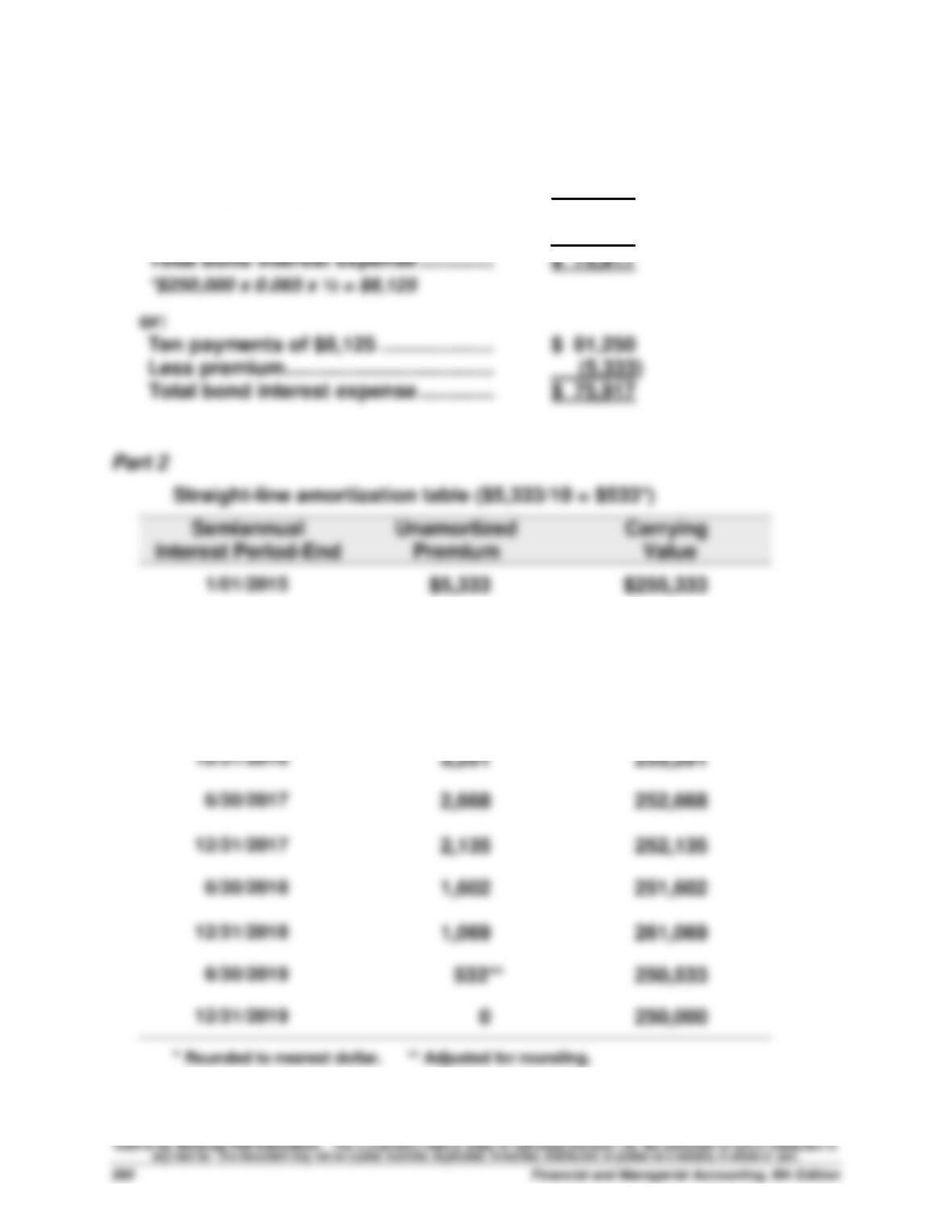

Ten payments of $8,125* ..........................

$ 81,250

Par value at maturity................................

250,000

Total repaid .................................................

331,250

Less amount borrowed .............................

(255,333)

Total bond interest expense .....................

$ 75,917

*$250,000 x 0.065 x ½ = $8,125

or:

Ten payments of $8,125 ............................

$ 81,250

Less premium .............................................

(5,333)

Total bond interest expense .....................

$ 75,917

Part 2

Straight-line amortization table ($5,333/10 = $533*)

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2015

$5,333

$255,333

6/30/2015

4,800

254,800

12/31/2015

4,267

254,267

6/30/2016

3,734

253,734

12/31/2016

3,201

253,201

6/30/2017

2,668

252,668

12/31/2017

2,135

252,135

6/30/2018

1,602

251,602

12/31/2018

1,069

261,069

6/30/2019

533**

250,533

12/31/2019

0

250,000

* Rounded to nearest dollar. ** Adjusted for rounding.

Problem 10-4A (Concluded)

Part 3

2015

June 30

Bond Interest Expense ................................

7,592

Premium on Bonds Payable ................................

533

Cash ................................................................

8,125

To record six months’ interest and

premium amortization.

2015

Dec. 31

Bond Interest Expense ................................

7,592

Premium on Bonds Payable ................................

533

Cash ................................................................

8,125

To record six months’ interest and

premium amortization.

Problem 10-5A (60 minutes)

Part 1

2015

Jan. 1

Cash ................................................................

292,181

Discount on Bonds Payable ................................

32,819

Bonds Payable .........................................................

325,000

Sold bonds on stated issue date.

Part 2

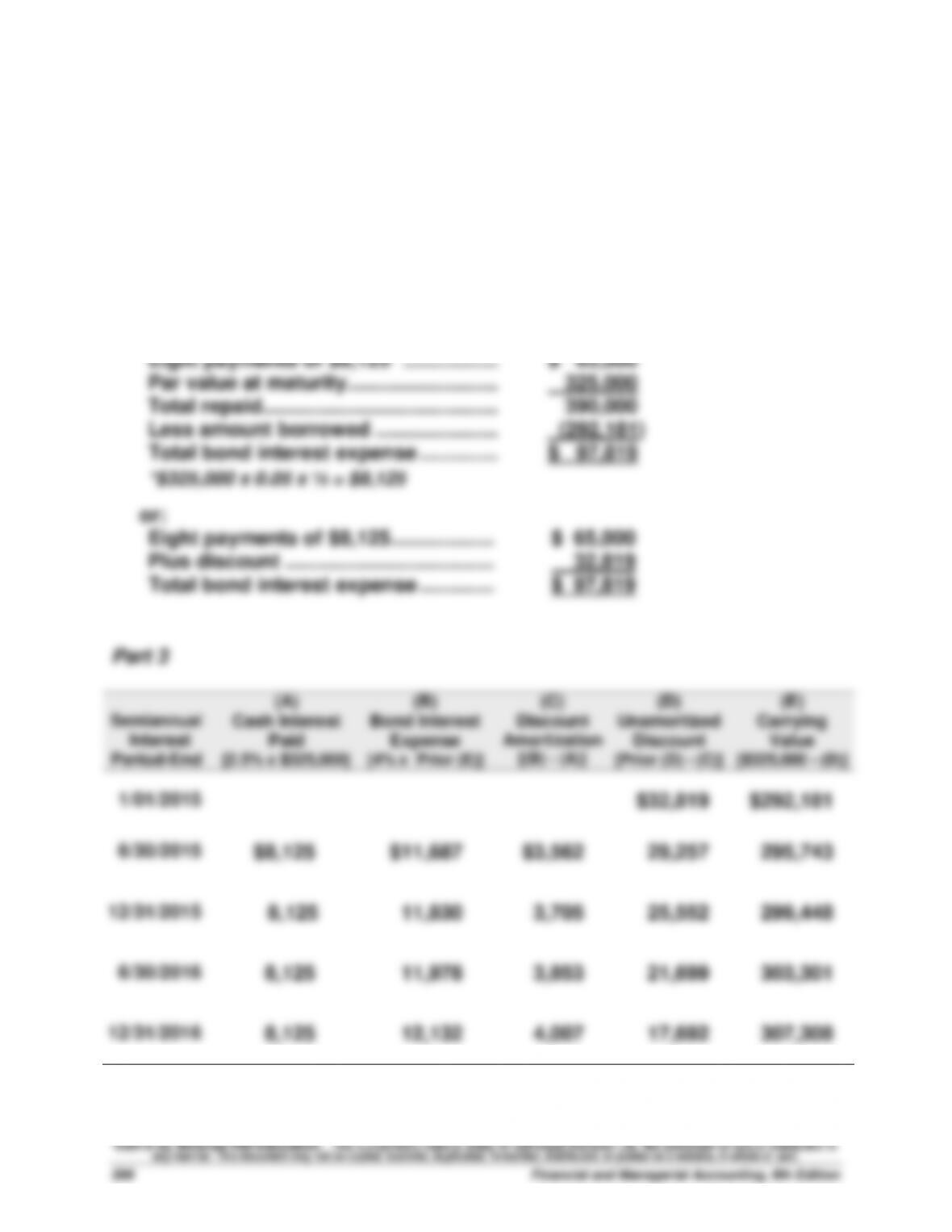

Eight payments of $8,125* ...................

$ 65,000

Par value at maturity.............................

325,000

Total repaid ............................................

390,000

Less amount borrowed ........................

(292,181)

Total bond interest expense ................

$ 97,819

*$325,000 x 0.05 x ½ = $8,125

or:

Eight payments of $8,125 .....................

$ 65,000

Plus discount ........................................

32,819

Total bond interest expense ................

$ 97,819

Part 3 Straight-line amortization table ($32,819/8 =$4,102*)

Semiannual

Interest Period-End

Unamortized

Discount

Carrying

Value

1/01/2015

$32,819

$292,181

6/30/2015

28,717

296,283

12/31/2015

24,615

300,385

6/30/2016

20,513

304,487

12/31/2016

16,411

308,589

*(rounded to nearest dollar)

Problem 10-5A (Concluded)

Part 4

2015

June 30

Bond Interest Expense ................................

12,227

Discount on Bonds Payable ................................

4,102

Cash ................................................................

8,125

To record six months’ interest and

discount amortization.

2015

Dec. 31

Bond Interest Expense ................................

12,227

Discount on Bonds Payable ................................

4,102

Cash ................................................................

8,125

To record six months’ interest and

discount amortization.

Problem 10-6A (45 minutes)

Part 1 Amount of Payment

Note balance ................................................................

$200,000

Number of periods .........................................................

5

Interest rate ................................................................

8%

Value from Table B.3 .....................................................

3.9927

Payment ($200,000 / 3.9927) ................................

$ 50,091

rounded to nearest dollar

Part 2

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[8% x (A)]

+

(C)

Debit

Notes

Payable

[(D) - (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) - (C)]

10/31/2016 ............

$200,000

$ 16,000

$ 34,091

$ 50,091

$165,909

10/31/2017 ............

165,909

13,273

36,818

50,091

129,091

10/31/2018 ............

129,091

10,327

39,764

50,091

89,327

10/31/2019 ............

89,327

7,146

42,945

50,091

46,382

10/31/2020 ............

46,382

3,709*

46,382

50,091

0

$ 50,455

$200,000

$250,455

* Adjusted for rounding

Part 3

2015

Dec. 31

Interest Expense ............................................................

2,667

Interest Payable .......................................................

2,667

Accrued interest on the installment

note payable ($16,000 x 2/12) (rounded).

2016

Oct. 31

Interest Expense ............................................................

13,333

Interest Payable .............................................................

2,667

Notes Payable ................................................................

34,091

Cash ..........................................................................

50,091

Record first payment on installment note

(interest expense = $16,000 - $2,667).

Problem 10-7A (20 minutes)

Part 1

Pulaski Company debt-to-equity = $360,000 / $500,000 = 0.72

Problem 10-8AB (60 minutes)

Part 1

2015

Jan. 1

Cash ................................................................

292,181

Discount on Bonds Payable ................................

32,819

Bonds Payable .........................................................

325,000

Sold bonds on stated issue date.

Part 2

Eight payments of $8,125* ...................

$ 65,000

Par value at maturity.............................

325,000

Total repaid ............................................

390,000

Less amount borrowed ........................

(292,181)

Total bond interest expense ................

$ 97,819

*$325,000 x 0.05 x ½ = $8,125

or:

Eight payments of $8,125 .....................

$ 65,000

Plus discount ........................................

32,819

Total bond interest expense ................

$ 97,819

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[2.5% x $325,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Discount

Amortization

[(B) - (A)]

(D)

Unamortized

Discount

[Prior (D) - (C)]

(E)

Carrying

Value

[$325,000 - (D)]

1/01/2015

$32,819

$292,181

6/30/2015

$8,125

$11,687

$3,562

29,257

295,743

12/31/2015

8,125

11,830

3,705

25,552

299,448

6/30/2016

8,125

11,978

3,853

21,699

303,301

12/31/2016

8,125

12,132

4,007

17,692

307,308

Problem 10-8AB (Concluded)

Part 4

2015

June 30

Bond Interest Expense ................................

11,687

Discount on Bonds Payable ................................

3,562

Cash ................................................................

8,125

To record six months’ interest and

discount amortization.

2015

Dec. 31

Bond Interest Expense ................................

11,830

Discount on Bonds Payable ................................

3,705

Cash ................................................................

8,125

To record six months’ interest and

discount amortization.

Problem 10-9AB (45 minutes)

Part 1

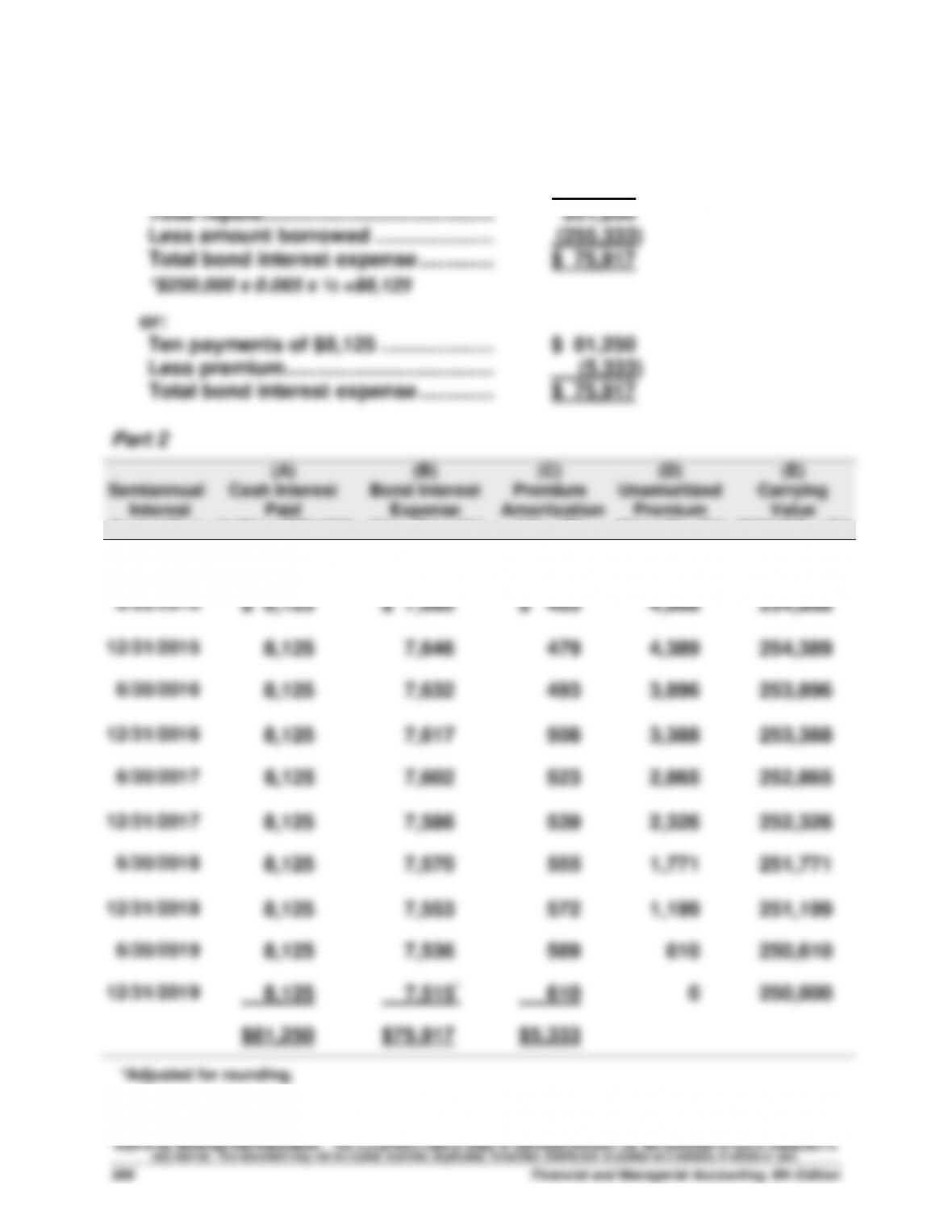

Ten payments of $8,125* ...........................

$ 81,250

Par value at maturity................................

250,000

Total repaid ..................................................

331,250

Less amount borrowed ..............................

(255,333)

Total bond interest expense ......................

$ 75,917

*$250,000 x 0.065 x ½ =$8,125

or:

Ten payments of $8,125 ............................

$ 81,250

Less premium .............................................

(5,333)

Total bond interest expense .....................

$ 75,917

Part 2

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[3.25% x $250,000]

(B)

Bond Interest

Expense

[3% x Prior (E)]

(C)

Premium

Amortization

[(A) - (B)]

(D)

Unamortized

Premium

[Prior (D) - (C)]

(E)

Carrying

Value

[$250,000 + (D)]

1/01/2015

$5,333

$255,333

6/30/2015

$ 8,125

$ 7,660

$ 465

4,868

254,868

12/31/2015

8,125

7,646

479

4,389

254,389

6/30/2016

8,125

7,632

493

3,896

253,896

12/31/2016

8,125

7,617

508

3,388

253,388

6/30/2017

8,125

7,602

523

2,865

252,865

12/31/2017

8,125

7,586

539

2,326

252,326

6/30/2018

8,125

7,570

555

1,771

251,771

12/31/2018

8,125

7,553

572

1,199

251,199

6/30/2019

8,125

7,536

589

610

250,610

12/31/2019

8,125

7,515*

610

0

250,000

$81,250

$75,917

$5,333

*Adjusted for rounding.