Exercise 10-7 (30 minutes)

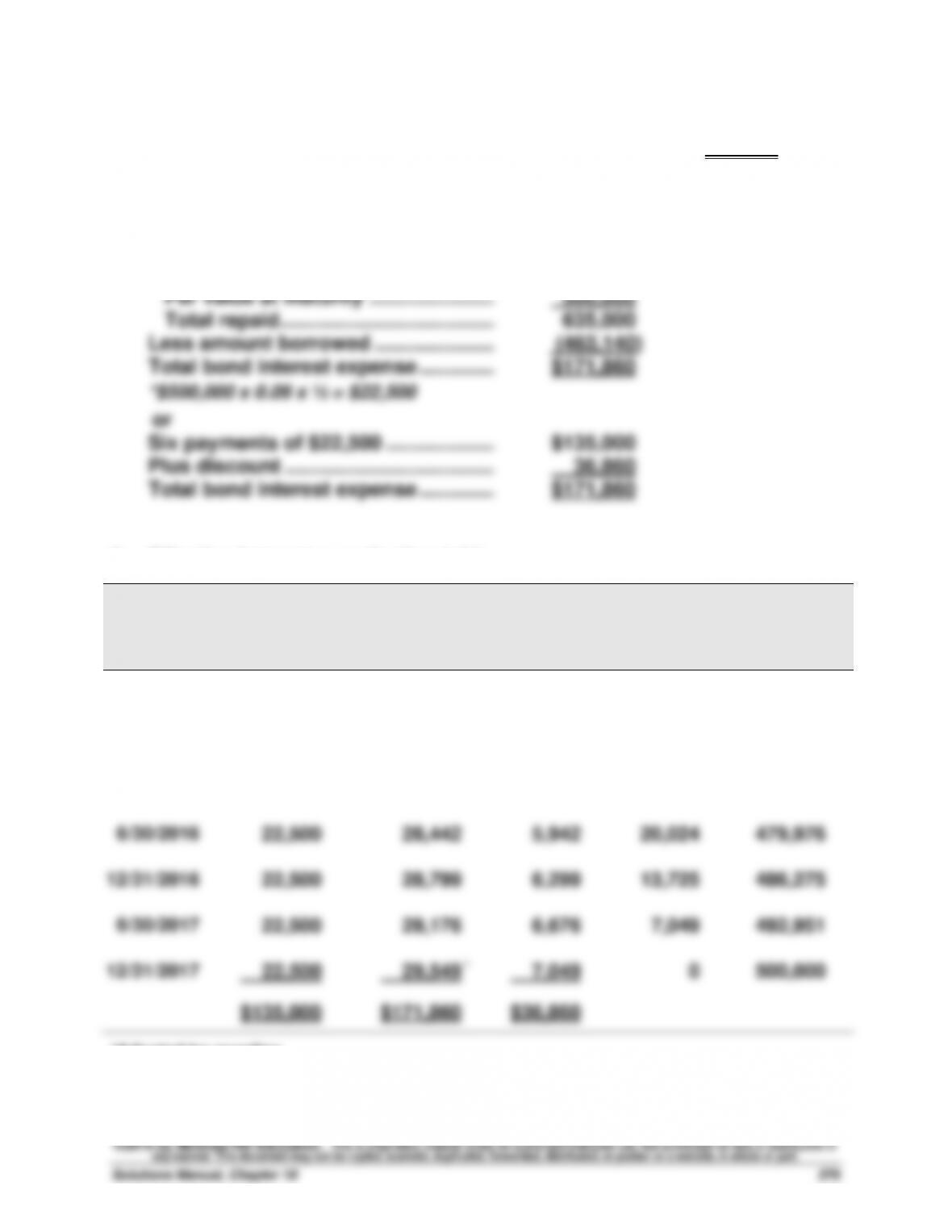

1. Premium = Issue price – Par value = $409,850 – $400,000 = $9,850

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $26,000* ……………

$156,000

Par value at maturity ………………….

400,000

Total repaid ………………………………..

556,000

Less amount borrowed …………………

(409,850)

Total bond interest expense ………….

$146,150

*$400,000 x 0.13 x ½ = $26,000

or

Six payments of $26,000 ……………….

$156,000

Less premium……………………………….

(9,850)

Total bond interest expense ………….

$146,150

3. Straight-line amortization table ($9,850/6 = $1,642)

Semiannual

Interest Period–End

Unamortized

Premium

Carrying

Value

1/01/2015

$9,850

$409,850

6/30/2015

8,208

408,208

12/31/2015

6,566

406,566

6/30/2016

4,924

404,924

12/31/2016

3,282

403,282

6/30/2017

1,640*

401,640

12/31/2017

0

400,000

©2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 10

575

Exercise 10-8 (25 minutes)

1. Semiannual cash interest payment = $150,000 x 10% x ½ year = $7,500

4. Estimation of the market price at the issue date

Cash Flow

Table

Table Value*

Amount

Present Value

Par (maturity) value …..…

B.1

0.6756

$150,000

$101,340

Interest (annuity) ……….…

B.3

8.1109

7,500

60,832

Price of bonds …………..…

$162,172

* Table values are based on a discount rate of 4% (half the annual market rate) and

10 periods (semiannual payments).

5.

Cash ………………………………………………………………..……

162,172

Premium on Bonds Payable…………………………..

12,172

Bonds Payable …………………………..……………….……

150,000

Sold bonds at a premium on the stated issue date.

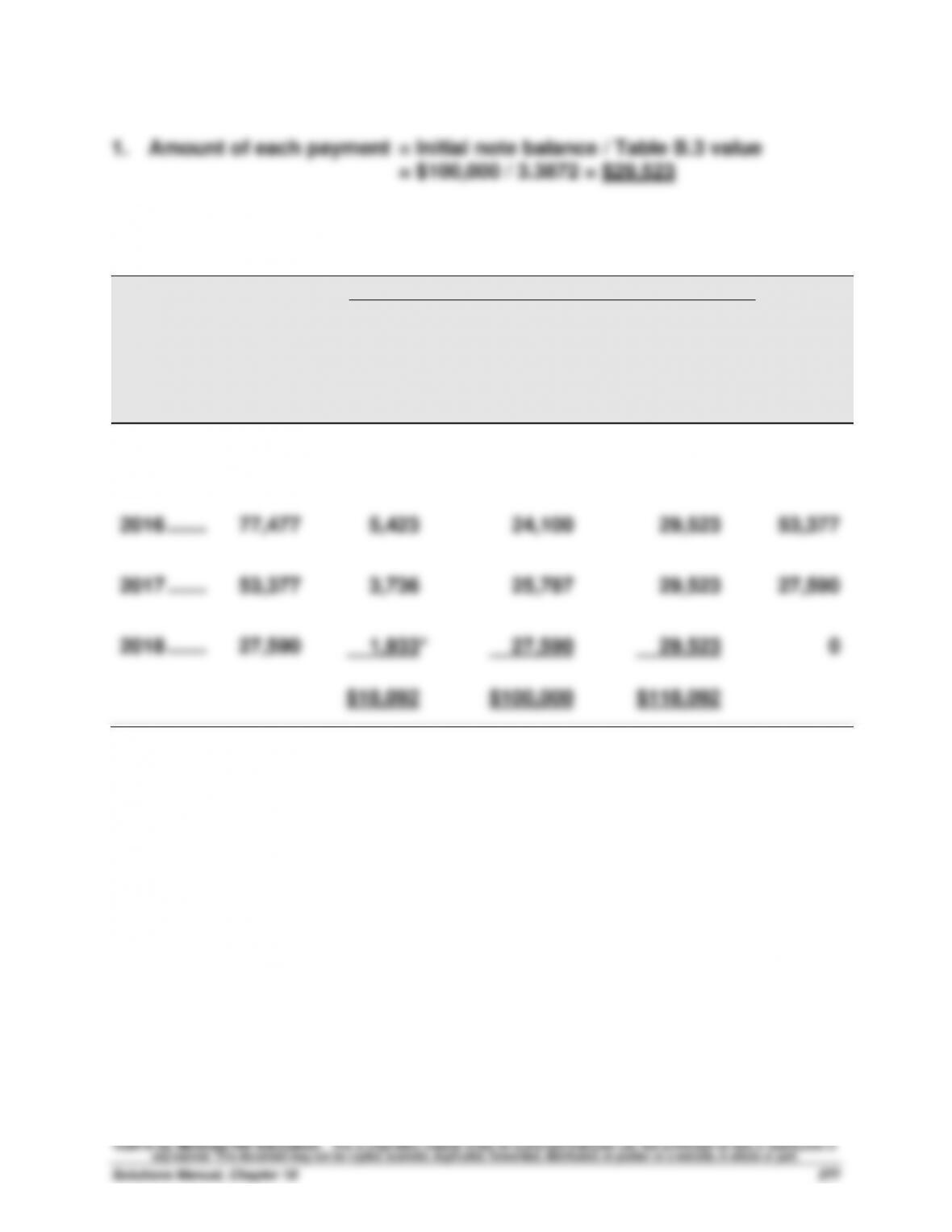

Exercise 10-10 (20 minutes)

2. Amortization table for the loan

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[7% x (A)]

+

(C)

Debit

Notes

Payable

[(D) – (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

2015 …….

$100,000

$ 7,000

$ 22,523

$ 29,523

$77,477

2016 …….

77,477

5,423

24,100

29,523

53,377

2017 …….

53,377

3,736

25,787

29,523

27,590

2018 …….

27,590

1,933*

27,590

29,523

0

$18,092

$100,000

$118,092

*Adjusted for rounding.

Exercise 10-11 (20 minutes)

2015

Jan. 1

Cash ……………………………………………………………………..

100,000

Notes Payable …………………………………………..……..

100,000

Borrowed $100,000 by signing a 7%

installment note.

2015

Dec. 31

Interest Expense …………………………………………….……..

7,000

Notes Payable ………………………………………………..……..

22,523

Cash ………………………………………………………………..

29,523

To record first installment payment.

2016

Dec. 31

Interest Expense …………………………………………….……..

5,423

Notes Payable ………………………………………………..……..

24,100

Cash ………………………………………………………………..

29,523

To record second installment payment.

2017

Dec. 31

Interest Expense …………………………………………….……..

3,736

Notes Payable ………………………………………………..……..

25,787

Cash ………………………………………………………………..

29,523

To record third installment payment.

2018

Dec. 31

Interest Expense …………………………………………….……..

1,933

Notes Payable ………………………………………………..……..

27,590

Cash ………………………………………………………………..

29,523

To record fourth installment payment.

Exercise 10-12 (15 minutes)

1a. Current debt–to–equity ratio = $220,000 / $400,000* = 0.55

2. Montclair’s risk will increase because it will have more debt. That debt

(plus interest) must be repaid even if the project does not work out as

Exercise 10–14B (30 minutes)

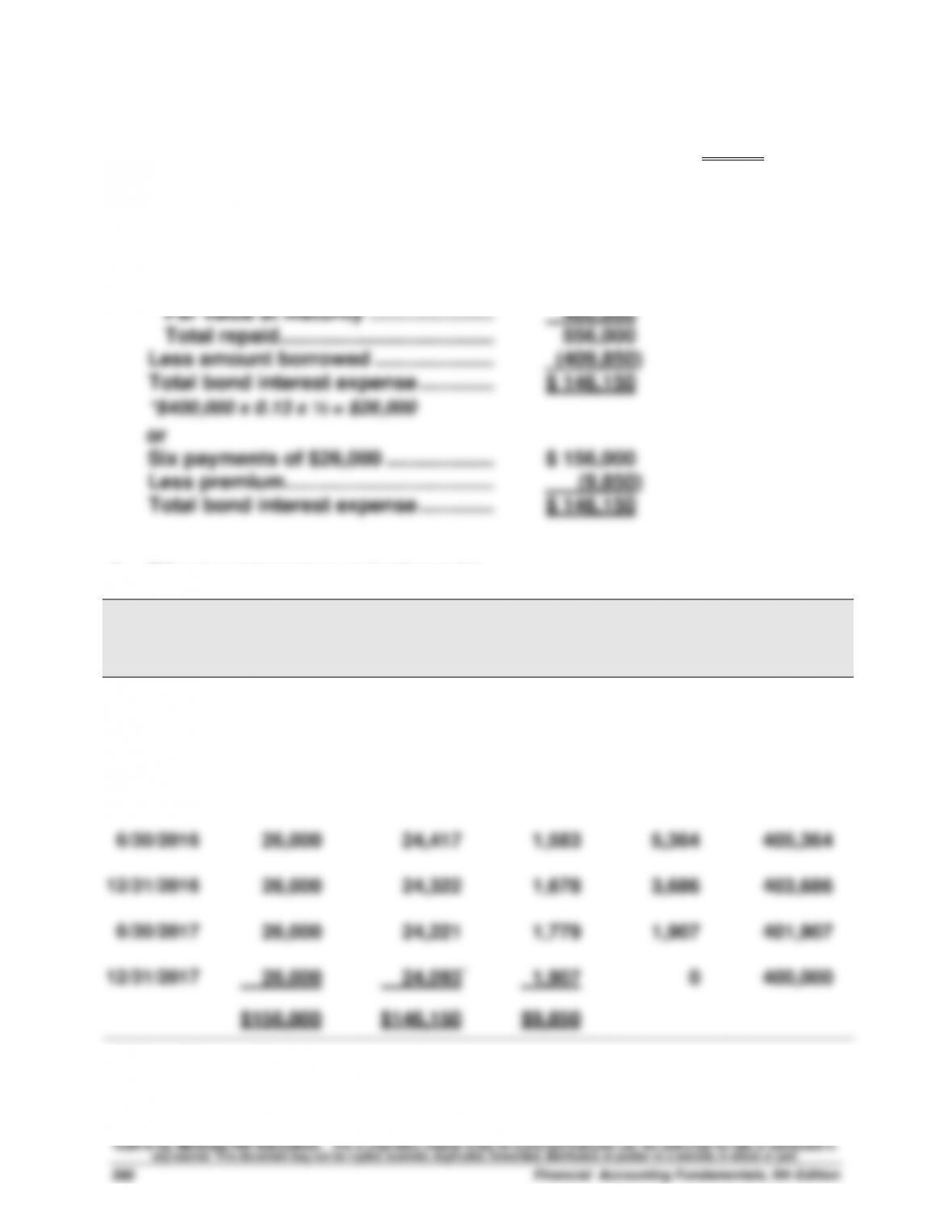

1. Premium = Issue price – Par value = $409,850 – $400,000 = $9,850

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $26,000* …………….…….

$ 156,000

Par value at maturity …………………..…….

400,000

Total repaid ……………………………………….

556,000

Less amount borrowed ………………….…….

(409,850)

Total bond interest expense …………..…….

$ 146,150

*$400,000 x 0.13 x ½ = $26,000

or

Six payments of $26,000 ………………..…….

$ 156,000

Less premium………………………………..…….

(9,850)

Total bond interest expense …………..…….

$ 146,150

3. Effective interest amortization table

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[6.5% x $400,000]

(B)

Bond Interest

Expense

[6% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[400,000 + (D)]

1/01/2015

$9,850

$409,850

6/30/2015

$ 26,000

$ 24,591

$1,409

8,441

408,441

12/31/2015

26,000

24,506

1,494

6,947

406,947

6/30/2016

26,000

24,417

1,583

5,364

405,364

12/31/2016

26,000

24,322

1,678

3,686

403,686

6/30/2017

26,000

24,221

1,779

1,907

401,907

12/31/2017

26,000

24,093*

1,907

0

400,000

$156,000

$146,150

$9,850

*Adjusted for rounding.

PROBLEM SET A

Problem 10-1A (50 minutes)

Part 1

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value …………………

B.1

0.4564

$40,000

$18,256

Interest (annuity) …..…

B.3

13.5903

2,000**

27,181

Price of bonds …………

$45,437

Bond premium …………

$ 5,437

* Table values are based on a discount rate of 4% (half the annual market rate) and 20

periods (semiannual payments).

** $40,000 x 0.10 x ½ = $2,000

b.

Premium on Bonds Payable ……………..……………

Bonds Payable …………………………………………………

Cash Flow

Table

Table Value*

Amount

Present Value

Par value …………………

B.1

0.3769

$40,000

Interest (annuity) …..…

B.3

12.4622

Bonds Payable …………………………………………………

Problem 10-1A (Concluded)

Part 3

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ………………..

B.1

0.3118

$40,000

$12,472

Interest (annuity) …....

B.3

11.4699

2,000

22,940

Price of bonds ………..

$35,412

Bond discount ………..

$ 4,588

* Table values are based on a discount rate of 6% (half the annual market rate) and 20

periods (semiannual payments).

b.

2015

Jan. 1

Cash ……………………………………………………....

35,412

Discount on Bonds Payable …………………..………

4,588

Bonds Payable …………………………………………………

40,000

Sold bonds on stated issue date.