CHAPTER 1

ACCOUNTING IN BUSINESS

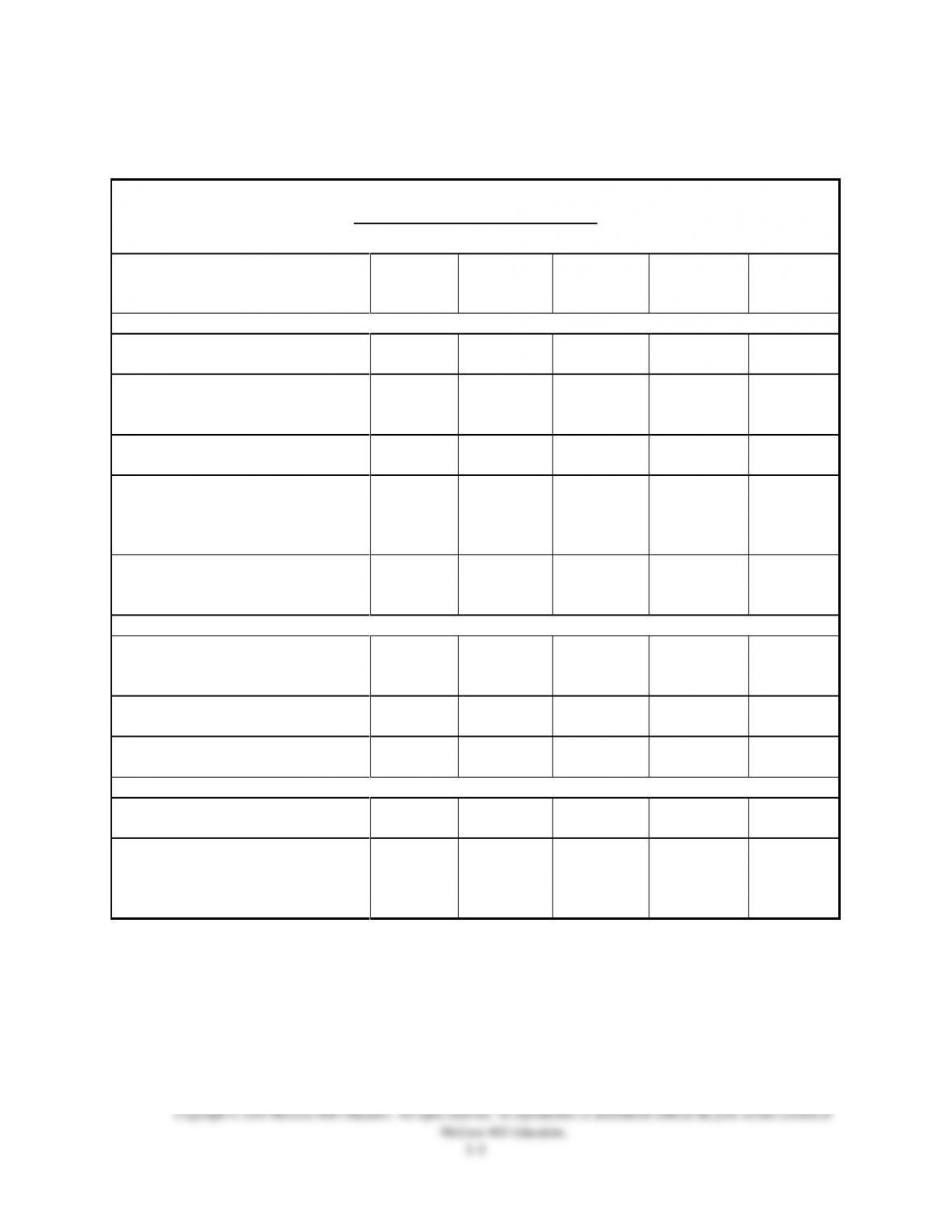

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives

C1. Explain the purpose and

importance of accounting.

1, 5

1-1

1-1, 1-4, 1-6

1-6

C2. Identify users and uses of, and

opportunities in accounting.

2, 3, 4, 6, 7,

8, 9, 10, 11,

12, 23

1-2

1-2, 1-3, 1-4

1-4, 1-8

C3. Explain why ethics are crucial to

accounting.

11

1-3

1-4, 1-5

1-3

C4. Explain generally accepted

accounting principles and define

and apply several accounting

principles.

13, 14, 15,

16, 19, 32

1-4, 1-5,

1-6, 1-16,

1-17

1-6, 1-7

1-7, 1-8, 1-9

1-3

C5. B Identify and describe the three

major activities in organizations.

(Appendix 1B)

16, 30,

31

1-21

1-13, 1-14

Analytical objectives:

A1. Define and interpret the

accounting equation and each of

its components.

17, 33, 34

1-7, 1-8,

1-9

1-8, 1-9

1-1, 1-2,

1-8, 1-10

1-1, 1-2,

1-4, 1-7,

1-9

A2. Compute and interpret return on

assets.

28

1-15

1-18

1-10, 1-11

1-1, 1-2,

1-5, 1-9

A3. A Explain the relation between

return and risk. (Appendix 1A)

29

1-12

1-1, 1-2,

1-9

Procedural objectives:

P1. Analyze business transactions

using the accounting equation.

18

1-10, 1-11

1-10, 1-11,

1-12, 1-13

1-1, 1-2, 1-7,

1-8, 1-9

1-7

P2. Identify and prepare basic

financial statements and explain

how they interrelate.

20, 21, 22,

23, 24, 25,

26, 27, 33,

34, 35

1-12, 1-13,

1-14

1-14, 1-15,

1-16, 1-17,

1-18, 1-19,

1-20

1-3, 1-4, 1-5,

1-6, 1-7, 1-8,

1-9

*See additional information on next page that pertains to these quick studies, exercises and problems.

Additional Information on Related Assignment Material

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode.

Synopsis of Chapter Revisions

• Apple: NEW opener with new entrepreneurial assignment

• Added titles to revenue and expense entries in columnar layout of transaction

analysis

• Streamlined section on Dodd-Frank act

• Bulleted presentation for accounting principles and fraud triangle

• Deleted world map of IFRS coverage

• Bulleted layout for ‘fraud triangle’

• Updated salary information

• New discussion on FASB and IASB convergence

• Updated return on assets for Dell

Chapter Outline

Notes

I. Importance of Accounting—we live in the information age, where

information, and its reliability, impacts the financial well-being of us

all.

A. Accounting Activities

Accounting is an information and measurement system that

identifies, records and communicates relevant, reliable, and

comparable information about an organizations business activities.

B. Users of Accounting Information

1. External Information Users—those not directly involved with

running the company. Examples: shareholders (investors),

lenders, directors, external auditors, non-executive employees,

labor unions, regulators, voters, legislators, government

officials, customers, suppliers, lawyers, brokers, etc.

a. Financial Accounting—area of accounting aimed at

serving external users by providing them with general-

purpose financial statements.

b. General-Purpose Financial Statements—statements that

have broad range of purposes which external users rely on.

2. Internal Information Users—those directly involved in

managing and operating an organization.

a. Managerial Accounting—area of accounting that serves

the decision-making needs of internal users.

b. Internal Reports—not subject to same rules as external

reports. They are designed with special needs of external

users in mind.

C. Opportunities in Accounting

Four broad areas of opportunities are financial, managerial,

taxation, and accounting related.

1. Private accounting offers the most opportunities.

2. Public accounting offers the next largest number of

opportunities

3. Government (and not-for-profit) agencies, including business

regulation and investigation of law violations also offer

opportunities.

II. Fundamentals of Accounting—accounting is guided by principles,

standards, concepts, and assumptions.

A. Ethics—a key concept. Ethics are beliefs that distinguish right

from wrong.

B. Fraud Triangle—model that asserts three factors must exist for

person to commit fraud: opportunity, pressure, and rationalization.

Chapter Outline

Notes

C. Internal Controls—procedures set up to protect company property

and equipment and insure reliable accounting reports, promotes

efficiency, and encourage adherence to company policies.

D. Generally Accepted Accounting Principles (GAAP)—concepts

and rules that govern financial accounting. Purpose of GAAP is to

make information in accounting statements relevant, reliable and

comparable.

1. Setting Accounting Principles

a. In U.S. major rule-setting bodies are the Securities and

Exchange Commission (SEC) and the Financial

Accounting Standards Board (FASB). SEC delegated

authority to set U.S. GAAP to the FASB.

b. The International Accounting Standards Board (IASB)

issues standards (International Financial Reporting

Standards or IFRS) that identify preferred accounting

practices in the global economy. IASB hopes to create

harmony among accounting practices in different

countries.

c. Differences between U.S. GAAP and IFRS are decreasing

as the FASB and IASB pursue convergence.

2. Conceptual Framework and Convergence—The FASB and

IASB are attempting to converge and enhance the conceptual

framework that guides standard setting. Framework consists

of:

a. Objectives—to provide information useful to investors,

creditors, and others.

b. Qualitative Characteristics—to require information that is

relevant, reliable and comparable.

c. Elements—to define items that financial statements can

contain.

d. Recognition and Measurement—to set criteria that an item

must meet for it to be recognized as an element; and how

to measure that element.

3. Principles and Assumptions of Accounting—two types are

general principles (basic assumptions, concepts and guidelines

for preparing financial statements; stem from long used

accounting practices) and specific principles (detailed rules

used in reporting transactions; from rulings of authoritative

bodies). The four principles discussed in this chapter are:

Chapter Outline

Notes

a. Measurement principle also called the cost principle—

financial statements are based on actual costs (with a

potential for subsequent adjustments to market) incurred

in business transactions. Cost is measured on a cash or

equal-to-cash basis. This principle emphasizes reliability

and verifiability; information based on cost is considered

objective. Objectivity means information is supported by

independent unbiased evidence: more than someone’s

opinion.

b. Revenue recognition principle—revenue is recognized

(recorded) when earned. Proceeds need not be in cash.

Revenue is measured by cash received plus the cash value

of other items received.

c. Expense recognition principle, also called matching

principle—prescribes that a company records expenses

incurred to generate revenues it reported.

d. Full disclosure principle—prescribes reporting the details

behind the financial statements that would impacts users’

decisions; often in footnotes to the statements.

The four assumptions discussed in this chapter are:

a. Going-concern assumption—accounting information

reflects the assumption that the business will continue

operating instead of being closed or sold.

b. Monetary unit assumption—transactions and events are

expressed in monetary, or money, units. Generally this is

the currency of the country in which it operates but today

some companies express reports in more than one

monetary unit.

c. Time period assumption—the life of the company can be

divided into time periods, such as months and years, and

that useful reports can be prepared for those periods.

d. Business entity assumption—a business is accounted for

separate from other business entities and separate from its

owner. Necessary for good decisions

4. Business Entity Legal Forms

a. Sole proprietorship is a business owned by one person

that has unlimited liability. It is a separate entity for

accounting purposes. The business is not subject to an

income tax but the owner is responsible for personal

income tax on the net income of entity.

b. Partnership is a business owned by two or more people,

called partners, who are subject to unlimited liability. The

business is not subject to an income tax, but the owners

are responsible for personal income tax on their individual

share of the net income of entity.

Chapter Outline

Notes

c. Three special partnership forms that limit liability

i. Limited partnership (LP)—has a general partner(s) with

unlimited liability and a limited partner(s) with limited

liability restricted to the amount invested.

ii. Limited liability partnership (LLP)—restricts partner’s

liabilities to their own acts and the acts of individuals

under their control.

iii. Limited liability company (LLC)—offers the limited

liability of a corporation and the tax treatment of a

partnership.(Note: most proprietorships and

partnerships are now organized as LLC)

e. Corporation is a business that is a separate legal entity

whose owners are called shareholders or stockholders.

These owners have limited liability. The entity is

responsible for a business income tax and the owners are

responsible for personal income tax on profits that are

distributed to them in the form of dividends.

5. Accounting Constraints There are two basic constraints on

financial reporting.

a. The materiality constraint prescribes that only information

that would influence the decisions of a reasonable person

need be disclosed. It looks at both the importance and

relative size of an amount.

b. The cost-benefit constraint prescribes that only

information with benefits of disclosure greater than the

costs of providing it need be disclosed.

c. Conservatism and industry practices are sometimes

referred to as constraints as well.

6. Sarbanes-Oxley (SOX)—Law passed by congress that

requires public companies to apply both accounting oversight

and stringent internal controls to achieve more transparency,

accountability and truthfulness in reporting.

7. Dodd-Frank (Wall Street Reform and Consumer Protection

Act)—Law recently passed as a response to financial systems

near collapse. Details of the law are yet to be set forth by

regulators.

III. Transactions Analysis and the Accounting Equation

A. Accounting equation (Assets = Liabilities + Equity)—elements of

the equation include:

1. Assets—resources a company owns or controls that are

expected to carry future benefits. (i.e. cash, supplies,

equipment and land)

2. Liabilities—creditors’ claims on assets. These claims reflect

obligations to transfer assets or provide products or services to

others.

Chapter Outline

Notes

3. Equity—owner’s claim on assets; assets minus liabilities. Also

called stockholders’ equity, shareholders’ equity or capital, net

assets or residual equity. Changes in Equity—result from stock

issuances or owner investments, revenues, dividends, and

expenses.

a. Common stock—part of contributed capital include cash and

other net assets from stockholders in exchange for stock.

Amounts stockholders invest in the company. Recorded under

the title Common Stock.

b. Revenues—are sales of products or services to customers.

Revenues increase equity (via net income) and result from a

company’s earnings activities.

c. Dividends—outflow of assets such as cash and other assets to

stockholders (results in decrease in equity).

d. Expenses—cost of assets or services used to earn revenues

(results in decrease in equity).

e. Retained earnings — accumulated revenues less accumulated

expenses and dividends since the company began.

B. Expanded Accounting Equation:

Assets = Liabilities + Common Stock – Dividends + Revenues –

Expenses

C. Transaction Analysis—each transaction and event always leaves

the equation in balance. (Assets = Liabilities + Equity)

1. Investment by owner:

ASSET = LIABILITIES + EQUITY

+ Cash + Common Stock

reason: investment

Increase on both sides of equation— keeps equation in balance.

2. Purchase supplies for cash:

ASSET = LIABILITIES + EQUITY

+ Supplies

– Cash

Increase and decrease on one side of the equation keeps the

equation in balance.

3. Purchase equipment for cash:

ASSET = LIABILITIES + EQUITY

+ Equipment

– Cash

Increase and decrease on one side of the equation keeps the

equation in balance.

4. Purchase supplies on credit:

ASSET = LIABILITIES + EQUITY

+ Supplies + Accounts Payable

Increase on both sides of equation keeps equation in balance.

Chapter Outline

Notes

5. Provide services for cash:

ASSET = LIABILITIES + EQUITY

+ Cash + Revenue Earned

Increase on both sides of equation keeps equation in balance.

6. Payment of expense in cash (rent):

ASSET = LIABILITIES + EQUITY

– Cash – (+ Expense)

Decrease on both sides of equation keeps equation in balance.

7. Payment of expense in cash (salaries):

ASSET = LIABILITIES + EQUITY

– Cash – (+ Expense)

Decrease on both sides of equation keeps equation in balance.

8. Provide services for credit:

ASSET = LIABILITIES + EQUITY

+Acct Rec + Revenue Earned

Increase on both sides of equation keeps equation in balance.

9. Receipt of cash from account receivable:

ASSET = LIABILITIES + EQUITY

+ Cash

– Acct Rec

Increase and decrease on one side of the equation keeps the

equation in balance.

10. Payment of accounts payable:

ASSET = LIABILITIES + EQUITY

– Cash – Accounts Payable

11. Payment of cash dividend:

ASSET = LIABILITIES + EQUITY

– Cash – (+ Dividends)

Decrease on both sides of equation keeps equation in balance.

(Note: since dividends are not expenses they are not used in

computing net income.)

Chapter Outline

Notes

IV. Financial Statements

A. The four financial statements and their purposes are:

1. Income Statement—describes a company’s revenues and

expenses along with the resulting net income or loss over a

period of time. (Net income occurs when revenues exceed

expenses. Net loss occurs when expenses exceed revenues.)

2. Statement of Retained Earnings—explains changes in equity

from net income (or loss) and from owner investment and

dividends over a period of time.

3. Balance Sheet—describes a company’s financial position

(types and amounts of assets, liabilities, and equity) at a point

in time.

4. Statement of Cash Flows—identifies cash inflows (receipts)

and cash outflows (payments) over a period of time.

B. Statement Preparation from Transaction Analysis—prepared in the

following order using the procedure indicated below.

1. Income Statement⎯information about revenues and expenses

is conveniently taken from the equity columns. Total revenues

minus total expenses equals net income or loss. Notice that

stockholders’ investments and dividends are not part of

income (or loss).

2. Statement Retained Earnings⎯reports retained earnings

changes over reporting period. Beginning retained earnings,

net income, from the income statement is added (or the net

loss is subtracted) and dividends are subtracted to arrive at the

ending retained earnings. Ending retained earnings is carried

to the Balance Sheet.

3. Balance Sheet⎯the ending balance of each asset is listed and

the total of this listing equals total assets. The ending balance

of each liability is listed and the total of this listing equals total

liabilities. Equity is separated into common stock and retained

earnings (note that retained earnings is taken from the

statement of retained earnings). Equity is added to total

liabilities to get total liabilities and equity. This total must

agree with total assets to prove the accounting equation. Either

the account form or the report form may be used to prepare

the balance sheet.

4. Statement of Cash Flows⎯the cash column must be carefully

analyzed to organize and report cash flows in categories of

operating, investing, and financing. The net change in cash is

determined by combining the net cash flow in each of the

three categories. This change is combined with the beginning

cash. The resulting figure should be the ending cash that was

shown on the balance sheet.

Chapter Outline

Notes

V. Global View—Financial Accounting using U.S. GAAP is similar, but

not identical to IFRS. Similarities and differences:

A. Basic Principles—both GAAP and IFRS include broad and similar

guidance for accounting.

B. Transaction Analysis—identical as shown in this chapter. Later,

some differences will arise. GAAP is rules-based whereas IFRS is

more principles-based.

C. Financial Statements—both systems require preparation of the same

four basic financial statements

VI. Decision Analysis—Return on Assets (ROA)—a profitability measure.

Also called Return on Investment (ROI)

A. Useful in evaluating management, analyzing and forecasting profits,

and planning activities.

B. The return on assets is: calculated by dividing net income for a

period by average total assets. (Average total assets is determined by

adding the beginning and ending assets and dividing by 2.)

C. As with all analysis tools, results should be compared to previous

business results as well as competitor’s results and industry norms.

VII. Risk and Return Analysis—Appendix 1A

A. Risk—the uncertainty about the return we will earn on an

investment.

B. The lower the risk, the lower the return.

C. Higher risk implies higher, but riskier implied returns.

VIII. Business Activities and the Accounting Equation—Appendix 1B

A. The accounting equation is derived from business activities.

B. Three major business activities are:

1. Financing activities—activities that provide the means

organizations use to pay for resources such as land, buildings, and

equipment to carry out plans. Two types of financing are:

a. Owner financing—refers to resources contributed by owner

including income left in the organization.

b. Non-owner (or creditor) financing—refers to resources

contributed by creditors (lenders).

2. Investing activities—are the acquiring and disposing of resources

(assets) that an organization uses to acquire and sell its products

or services.

3. Operating activities—involve using resources to research,

develop, purchase, produce, distribute, and market products and

services.

C Investing (assets) is balanced by Financing (liabilities and equity).

Operating activities is the result of investing and financing.

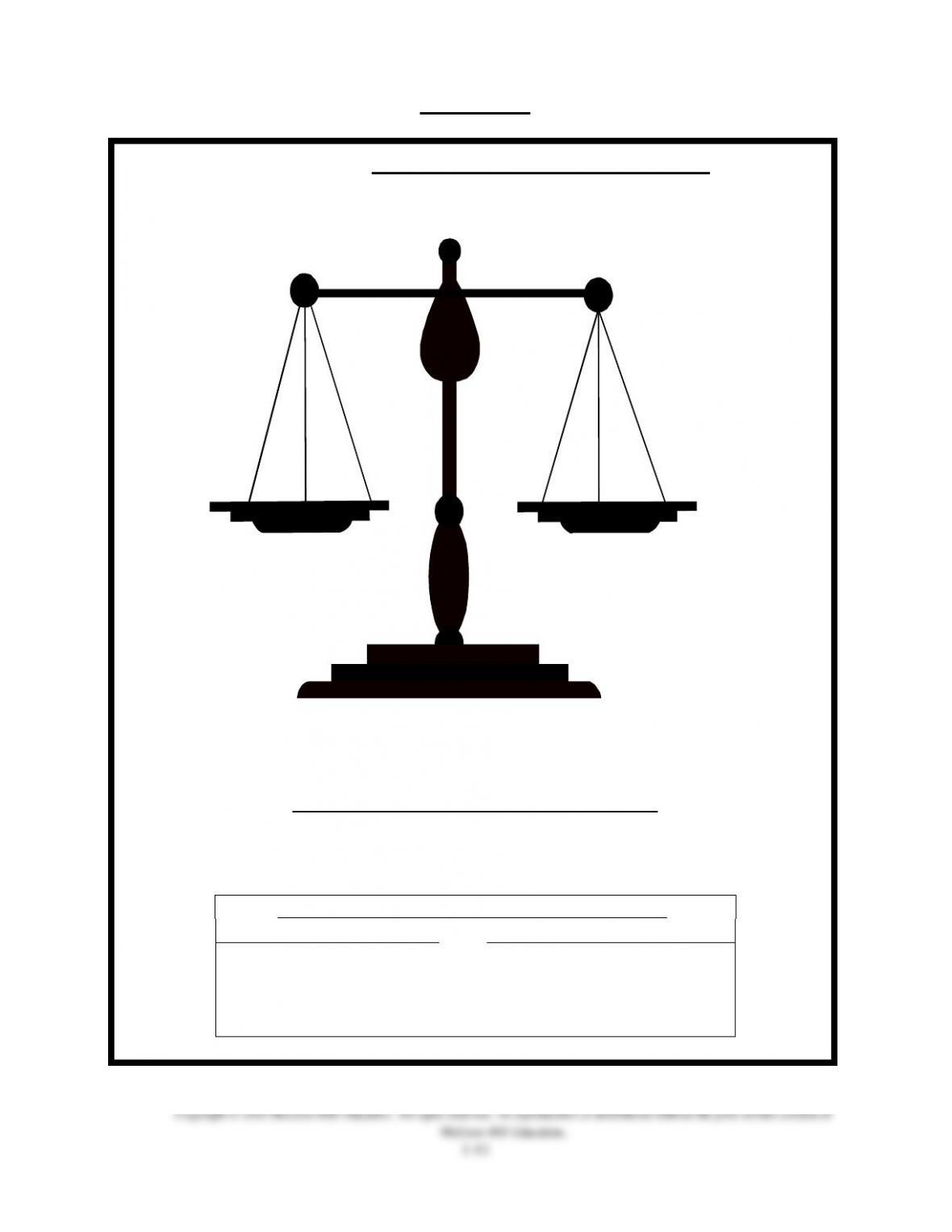

VISUAL #1-1

WARNING: NO MATTER WHAT HAPPENS

ALWAYS KEEP THIS SCALE

IN BALANCE

ASSETS L + E

Basic Accounting Equation

ASSETS = LIABILITIES + EQUITY

TRANSACTION ANALYSIS RULES

1) Every transaction affects at least two items.

2) Every transaction must result in a balanced equation.

TRANSACTION ANALYSIS POSSIBILITIES:

A

=

L

+

E

(1)

+

and

+

OR(2)

–

and

–

OR(3)

+ and –

and

No change

OR(4)

No change

and

+ and –