Problem C-3B (Concluded)

Part 2

12/31/2015

12/31/2016

12/31/2017

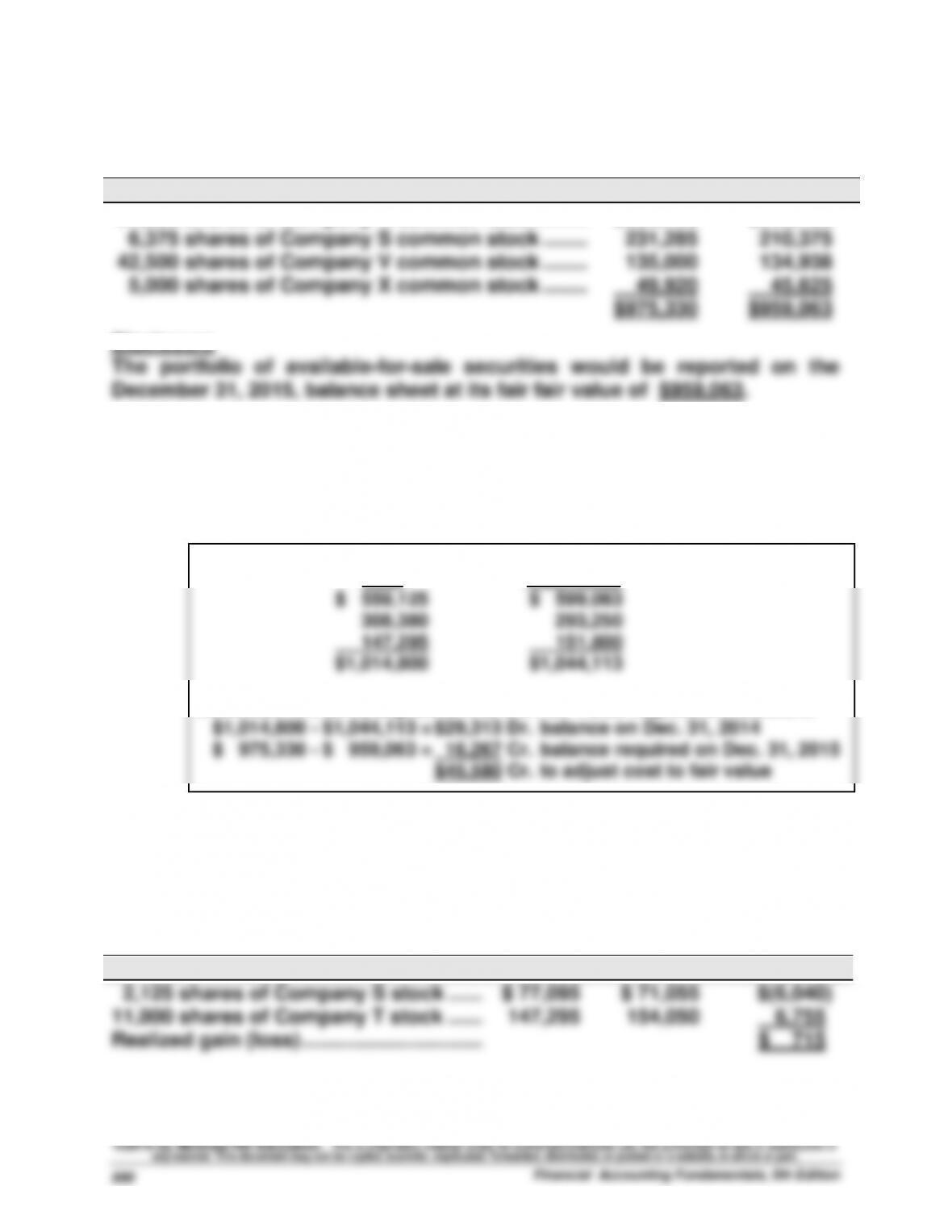

Long-Term AFS Securities (cost)…………...

$117,773

$92,580

$126,260

Fair Value Adjustment ……………………...

(2,873)

2,220

(6,260)

Long-Term AFS Securities (fair value) …...

$114,900

$94,800

$120,000

2015

2016

2017

Realized gains (losses)

Sale of Ford shares ………………………….

$(7,240)

Sale of Polaroid shares …………………….

665

Sale of Duracell shares …………………….

$ (9,598)

Sale of Apple shares ………………………..

(7,450)

Sale of Sears shares ………………………..

______

______

2,721

Total realized gain (loss) ……………………

$ 0

$(6,575)

$(14,327)

Unrealized gains (losses) at year–end …

$(2,873)

$ 2,220

$ (6,260)

Problem C-4B (Continued)

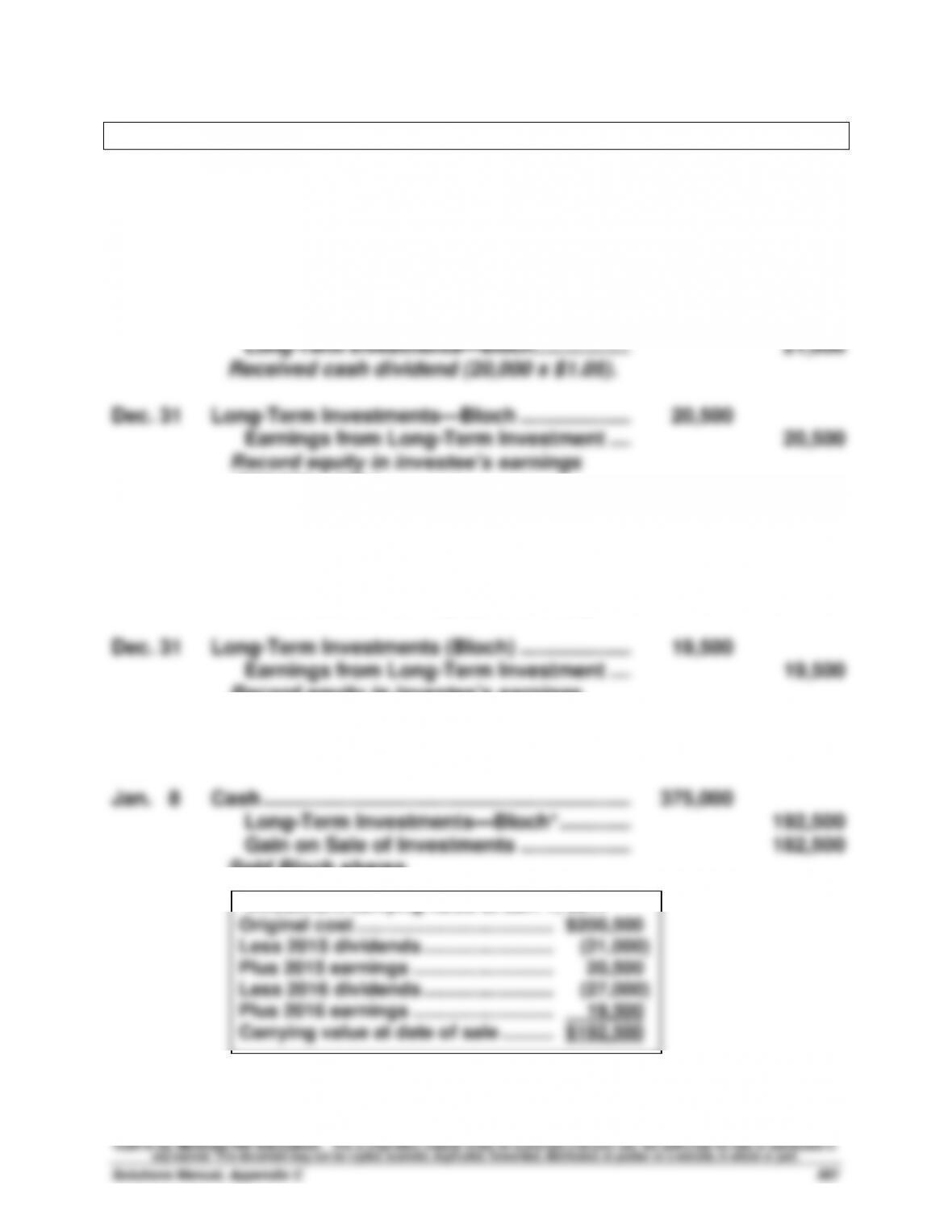

2. Carrying value per share (see computations in part 1)

3. Change in Brinkley’s equity

Earnings from Bloch (for 2015) ………………….….

$ 20,500

Earnings from Bloch (for 2016) ………………….….

19,500

Gain on sale of investments ………………………….

182,500

Net increase ……………………………………………..….

$222,500

Part 2

1. Journal entries (assuming NO significant influence)

2015

Jan. 5

Long-Term Investments—AFS (Bloch) ……….………………….

200,500

Cash ……………………………………………………….

200,500

Purchased Bloch shares.

Aug. 1

Cash ………………………………………………………...……………………

21,000

Dividend Revenue ……………………………….……………………

21,000

Received cash dividend (20,000 x $1.05).

Dec. 31

Fair Value Adjustment—AFS (LT)* ……………..……………

37,500

Unrealized Gain—Equity …………………………..

37,500

Record fair value adjustment.

*20,000 x $11.90 = $238,000

$238,000 – $200,500 = $37,500

Problem C-6BA (60 minutes)

Part 1

2015

May 26

Accounts Receivable—Fuji ……………………….….

60,450

Sales …………………………………………………..…..

60,450

(6,500,000 yen x $0.0093/yen)

June 1

Cash ………………………………………………………...……………………

64,800

Sales …………………………………………………..…..

64,800

July 25

Cash* ………………………………………………………..……………………

59,800

Foreign Exchange Loss …………………………….……………………

650

Accounts Receivable—Fuji ………………….……….

60,450

*(6,500,000 yen x $0.0092/yen)

Oct. 15

Accounts Receivable—Martinez Brothers ….……………………

38,556

Sales …………………………………………………..…..

38,556

(378,000 pesos x $0.1020/peso)

Dec. 6

Accounts Receivable—Chi–Ying ………………..…………

35,975

Sales …………………………………………………..…..

35,975

(250,000 yuans x $0.1439/yuan)

Dec. 31

Accounts Receivable—Martinez Brothers …..……………………

1,512

Foreign Exchange Gain* …………………………..

1,512

*Original measure = (378,000 pesos x $0.1020/peso) = $38,556

Year-end measure = (378,000 pesos x $0.1060/peso) = 40,068

Gain for the period …………………………. = $ 1,512

Dec. 31

Accounts Receivable—Chi–Ying ………………..…………

275

Foreign Exchange Gain* …………………………..

275

*Original measure = (250,000 yuans x $0.1439/yuan) = $35,975

Year-end measure = (250,000 yuans x $0.1450/yuan) = 36,250

Gain for the period ………….……………… = $ 275

Jan. 5

Cash* ………………………………………………………..……………………

39,500

Accounts Receivable—Chi-Ying** ………..…………………

36,250

Foreign Exchange Gain ……………………….….

3,250

*(250,000 yuans x $0.1580/yuan) **($35,975 + $275)

Jan. 13

Cash* ………………………………………………………..……………………

39,274

Foreign Exchange Loss …………………………….……………………

794

Accounts Receivable—Martinez Bros** ….……………………

40,068

* (378,000 pesos x $0.1039/peso) ** ($38,556 + $1,512)

Problem C-6BA (Concluded)

Part 2

Foreign exchange gain reported on 2015 income statement

July 25 …………………………………………....

$ (650)

December 31…………………………………...

1,512

December 31…………………………………...

275

Total ……………………………………………....

$1,137

Part 3

To reduce the risk of foreign exchange gain or loss, Datamix could attempt

to negotiate foreign customer sales that are denominated in U.S. dollars.

Serial Problem — SP C

Serial Problem, Business Solutions (35 minutes)

Part 1

2016

April 16

Short-Term Investments—Trading (J&J) ……………...

20,300

Cash ……………………………………………………….

20,300

Purchased Johnson & Johnson shares

[(400 x $50) + $300].

30

Short-Term Investments—Trading (Starbucks) …....

4,650

Cash ……………………………………………………….

4,650

Purchased Starbucks shares

[(200 x $22) + $250].

Part 2 Adjusting entry at June 30, 2016

June 30

Fair Value Adjustment—Trading* …………………...

850

Unrealized Gain—Income ………………………....

850

To reflect an unrealized gain in fair values of

trading securities.

* Fair Value Adjustment computations

Trading securities’

portfolio

Shares

Share Price

at 6/30/2016

Fair

Value

Cost

Unrealized

Gain (Loss)

J & J ………………….

400

$55

$22,000

$20,300

$1,700

Starbucks……………

200

$19

3,800

4,650

(850)

Totals ………………..

$25,800

$24,950

$ 850