Problem C-3A (Concluded)

Part 2

12/31/2015

12/31/2016

12/31/2017

Long-Term AFS Securities (cost)……………....

$117,100

$85,143

$212,160

Fair Value Adjustment ………………………....

(3,650)

(13,818)

8,040

Long-Term AFS Securities (fair value) ……....

$113,450

$71,325

$220,200

Part 3

2015

2016

2017

Realized gains (losses)

Sale of Johnson & Johnson shares …….

$ 2,235

Sale of Mattel shares …………………………..

(5,080)

Sale of Sara Lee shares ……………………...

$(4,665)

Sale of Sony shares …………………………..

1,055

Sale of Eastman Kodak shares …………...

______

_______

4,352

Total realized gain (loss) ……………………...

$ 0

$ (2,845)

$ 742

Unrealized gains (losses) at year–end*…..

$(3,650)

$(13,818)

$ 8,040

* Equals the balance of the Fair Value Adjustment account.

Problem C-4A (Continued)

2. Carrying value per share, January 1, 2017 (see computations in part 1)

3. Change in Selk’s equity due to stock investment

Earnings from Kildaire (2015) …………………….…….

$232,800

Earnings from Kildaire (2016) …………………….…….

295,200

Gain on sale of investments …………………………..

154,000

Net increase ……………………………………………..………..

$682,000

Part 2

1. Journal entries (assuming NO significant influence)

2015

Jan. 5

Long-Term Investments—AFS (Kildaire) ……….………………….

1,560,000

Cash ……………………………………………………….

1,560,000

Purchased Kildaire shares.

Oct. 23

Cash …………………………..…………………………….……………………

192,000

Dividend Revenue ……………………………….……………………

192,000

Received cash dividend (60,000 x $3.20).

Dec. 31

Fair Value Adjustment—AFS (LT)* ……………..……………

240,000

Unrealized Gain—Equity …………………………..

240,000

Record fair value adjustment.

*60,000 x $30.00 = $1,800,000

$1,800,000 – $1,560,000 = $240,000

Oct. 15

Cash …………………………..…………………………….……………………

156,000

Dividend Revenue ……………………………….……………………

156,000

Dec. 31

Fair Value Adjustment—AFS (LT)* ……………..……………

120,000

Unrealized Gain—Equity …………………………..

120,000

Record fair value adjustment.

$1,920,000 – $1,560,000 = $360,000

Problem C-4A (Concluded)

2017

Jan. 2

Cash …………………………..…………………………….……………………

1,894,000

Long-Term Investments—AFS (Kildaire) ….……………………

1,560,000

Gain on Sale of Investments ………………..…………

334,000

Sold Kildaire shares.

Jan. 2

Unrealized Gain—Equity …………………………………………………

360,000

Fair Value Adjustment—AFS (LT) …………………………..

360,000

To remove fair value adjustment and related

accounts ($240,000 + $120,000 = $360,000).

2. Investment cost per share, January 1, 2017

3. Change in Selk’s equity due to stock investment

Dividend Revenue (2015) ………………………….

$192,000

Dividend Revenue (2016) ………………………….

156,000

Gain on sale of investments ……………………..

334,000

Net increase …………………………………………….

$682,000

Problem C-6AA (60 minutes)

Part 1

2015

Apr. 8

Cash …………………………..………………………………………………….

5,938

Sales …………………………………………………….…

5,938

July 21

Accounts Receivable⎯Sumito …………………….…….

14,100

Sales …………………………………………………….…

14,100

(1,500,000 yen x $0.0094/yen)

Oct. 14

Accounts Receivable⎯Smithers …………………………..

27,675

Sales …………………………………………………….…

27,675

(19,000£ x $1.4566/£)

Nov. 18

Cash …………………………..………………………………………………….

13,800

Foreign Exchange Loss ………………………………………………….

300

Accounts Receivable⎯Sumito ……………….………….

14,100

(1,500,000 yen x $0.0092/yen)

Dec. 20

Accounts Receivable⎯Hamid Albar …………….…………….

7,652

Sales …………………………………………………….…

7,652

(17,000 ringgits x $0.4501/ringgits)

Dec. 31

Accounts Receivable⎯Smithers. ………………..…………

103

Foreign Exchange Gain * ……………………….….

103

*Original measure = (19,000£ x $1.4566/£) = $27,675

Year-end measure = (19,000£ x $1.4620/£) = 27,778

Gain for the period ……………………… = $ 103

Dec. 31

Foreign Exchange Loss* ……………………………..………………….

77

Accounts Receivable⎯Hamid Albar ……….………………….

77

*Original measure = (17,000 ringgits x $0.4501/ ringgits) = $7,652

Year-end measure = (17,000 ringgits x $0.4456/ ringgits) = 7,575

Loss for the period ……………………………………… = $ 77

2016

Jan. 12

Cash* ………………………………………………………….………………….

27,928

Accounts Receivable⎯Smithers** ………….……………….

27,778

Foreign Exchange Gain …………………………..

150

*(19,000£ x $1.4699/£) **($27,675 + $103)

Jan. 19

Cash* ………………………………………………………….………………….

7,514

Foreign Exchange Loss …………………………..….………………….

61

Accounts Receivable⎯Hamid Albar** …….………………….

7,575

*(17,000 ringgits x $0.4420/ ringgits) **($7,652 – $77)

PROBLEM SET B

Problem C-1B (60 minutes)

Part 1

2015

Mar. 10

Short-Term Investments—Trading (AOL) ……………....

143,505

Cash ……………………………………………………….

143,505

Purchased AOL shares

[(2,400 x $59.15) + $1,545].

May 7

Short-Term Investments—Trading (MTV) …………..

184,105

Cash ……………………………………………………….

184,105

Purchased MTV shares

[(5,000 x $36.25) + $2,855].

Sept. 1

Short-Term Investments—Trading (UPS) …………..

69,950

Cash ……………………………………………………….

69,950

Purchased UPS shares

[(1,200 x $57.25) + $1,250].

Dec. 31

Unrealized Loss—Income ……………………………....

17,560

Fair Value Adjustment—Trading (ST) ………...

17,560

Record fair value of securities.

$380,000 fair value – $397,560 cost*; thus,

FVA—Trading s/b $17,560 Cr.

Note: Unadjusted FVA is $0; Ending bal. FVA s/b

$17,560 Cr; thus, entry must $17,560 Cr FVA.

*$397,560 = $143,505 + $184,105 + $69,950

We could also use a T-account to determine the needed adjustment to fair value:

12/31/2015—F.V. Adj—Trading

Unadj.

0

Adj.

17,560

End.

17,560

Problem C-1B (Concluded)

2017

Jan. 28

Short-Term Investments—Trading (Pepsi) …………

88,890

Cash …………………………………………………………

88,890

Purchased PepsiCo shares

[(2,000 x $43.00) + $2,890].

Jan. 31

Cash ………………………………………………………………

602,760

Loss on Sale of Short-Term Investments …………

19,690

Short-Term Investments—Trading (SPW) ……….

622,450

Sold SPW shares [(3,600 x $168) – $2,040].

Aug. 22

Cash ………………………………………………………………

133,720

Loss on Sale of S-T Investments ……………………..

9,785

Short-Term Investments—Trading (AOL) ……….

143,505

Sold AOL shares [(2,400 x $56.75) – $2,480].

Sept. 3

Short-Term Investments—Trading (Voda) ………….

62,430

Cash …………………………………………………………

62,430

Purchased Vodaphone shares

[(1,500 x $40.50) + $1,680].

Oct. 9

Cash ………………………………………………………………

47,155

Gain on Sale of Short-Term Investments ………...

848

Short-Term Investments—Trading (W-M) ………...

46,307

Sold Wal-Mart shares

[(900 x $53.75) – $1,220].

Dec. 31

Unrealized Loss—Income ……………………………….

27,058

Fair Value Adjustment—Trading (ST) …………

27,058

Record fair value of securities.

$140,000 fair value – $151,320 cost*; thus,

FVA—Trading s/b $11,320 Cr.

Note: Unadjusted FVA is $15,738 Dr; Ending bal. FVA s/b

$11,320 Cr; thus, entry must $27,058 Cr FVA.

*$812,262 +$88,890 -$622,450 -$143,505 +$62,430 -$46,307

We could also use a T-account to determine the needed adjustment to fair value:

12/31/2017—F.V. Adj—Trading

Unadj.

15,738

Adj.

27,058

End.

11,320

Problem C-2B (Concluded)

Part 2

Comparison of Cost and Fair Values of AFS Portfolio

Unrealized

Cost Fair Value Gain (Loss)

Nokia (2,550 x $41.25) + $2,250a ……… $107,437

2,550 x $40.25 (rounded) ……… $102,638

a Brokerage fee attached to remaining 2,550 shares: $3,000 x (3,400 sh.– 850 sh.)/ 3,400 sh. = $2,250.

b Brokerage fee attached to remaining 1,200 shares: Entire $1,255 (none sold).

c Brokerage fee attached to remaining 2,500 shares: Entire $2,890 (none sold).

Part 3

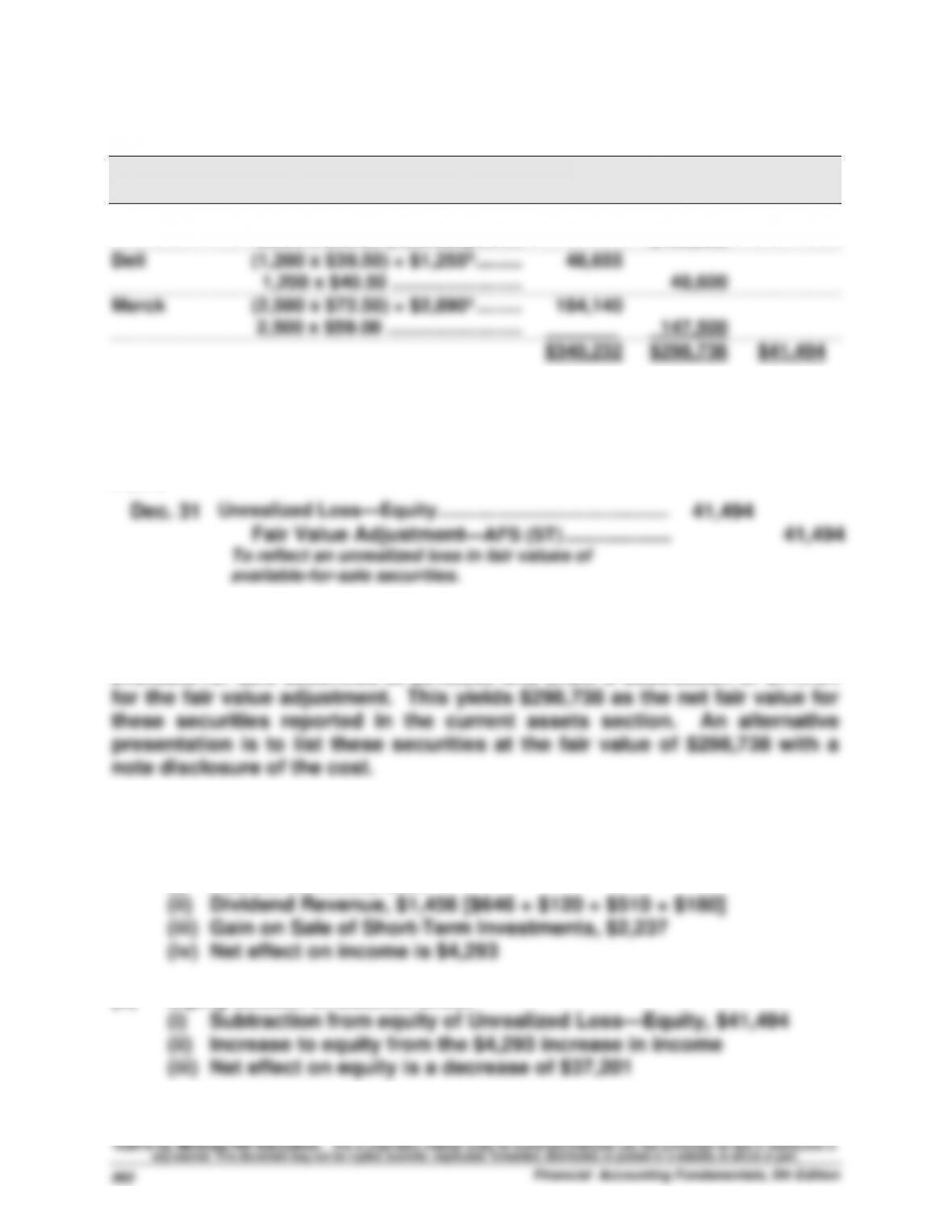

Dec. 31

Unrealized Loss—Equity ……………………………………..

41,494

Fair Value Adjustment—AFS (ST) ……………….

41,494

To reflect an unrealized loss in fair values of

available-for-sale securities.

Part 4

The balance sheet would report the cost of these short-term investments in

available-for-sale securities at $340,232 and show a subtraction of $41,494

Part 5

(a) Income statement

(i) Interest Revenue, $600

(b) Equity section of Balance sheet

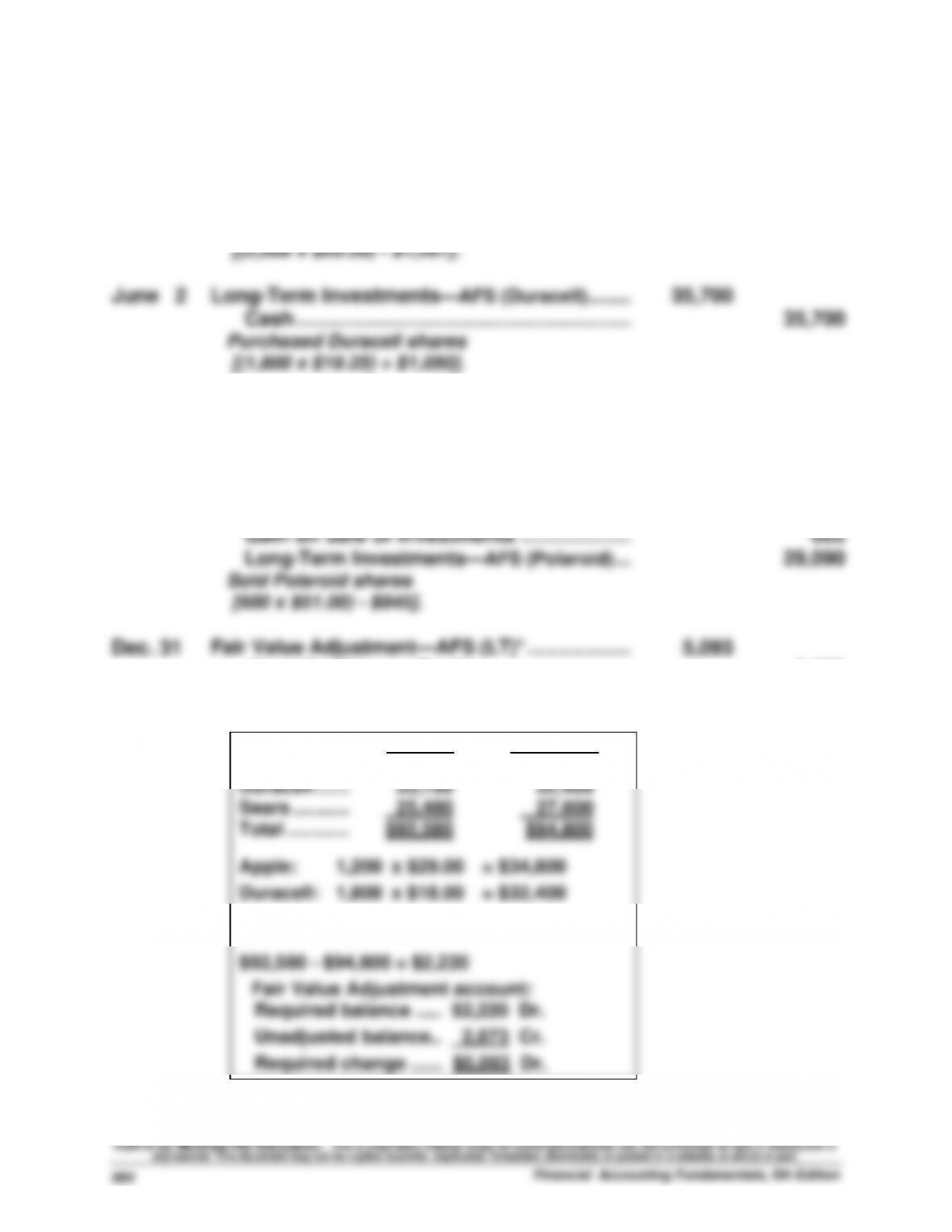

Problem C-3B (60 minutes)

Part 1

2015

Mar. 10

Long-Term Investments—AFS (Apple) …………………………..

31,400

Cash ……………………………………………………….

31,400

Purchased Apple shares

[(1,200 x $25.50) + $800].

April 7

Long-Term Investments—AFS (Ford) ……………..……………

57,283

Cash ……………………………………………………….

57,283

Purchased Ford shares

[(2,500 x $22.50) + $1,033].

Sept. 1

Long-Term Investments—AFS (Polaroid) ………..………………..

29,090

Cash ……………………………………………………….

29,090

Purchased Polaroid shares

[(600 x $47.00) + $890].

Dec. 31

Unrealized Loss—Equity ……………………………….………………..

2,873

Fair Value Adjustment—AFS (LT)* …………………………..

2,873

Annual adjustment to fair values.

*

Cost _

Fair Value

Apple …………..…….

$ 31,400

$ 33,000

Ford …………….…….

57,283

52,500

Polaroid ……….…….

29,090

29,400

Total…………….…….

$117,773

$114,900

Apple: 1,200 x $27.50 = $33,000

Ford: 2,500 x $21.00 = 52,500

Polaroid: 600 x $49.00 = 29,400

$117,773 – $114,900 = $2,873

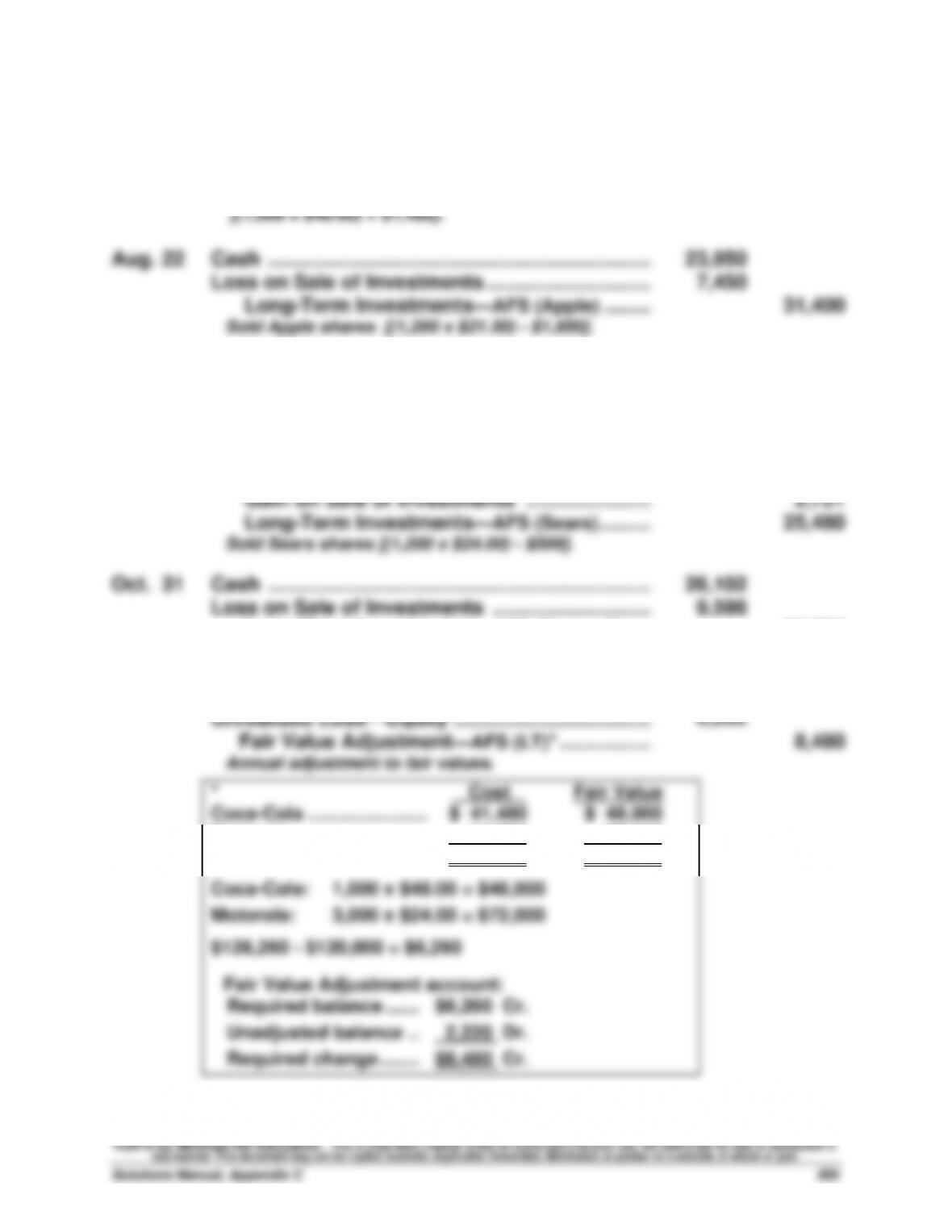

Problem C-3B (Continued)

2017

Jan. 28

Long-Term Investments—AFS (Coca-Cola) ……..………………..

41,480

Cash ……………………………………………………….

41,480

Purchased Coca-Cola shares

[(1,000 x $40.00) + $1,480].

Aug. 22

Cash …………………………..……………………………….………………..

23,950

Loss on Sale of Investments …………………………..

7,450

Long-Term Investments—AFS (Apple) ………………………..

31,400

Sold Apple shares [(1,200 x $21.50) – $1,850].

Sept. 3

Long-Term Investments—AFS (Motorola) ………..………………..

84,780

Cash ……………………………………………………….

84,780

Purchased Motorola shares

[(3,000 x $28) + $780].

Oct. 9

Cash …………………………..……………………………….………………..

28,201

Gain on Sale of Investments …………………..………

2,721

Long-Term Investments—AFS (Sears) ……….………………..

25,480

Sold Sears shares [(1,200 x $24.00) – $599].

Oct. 31

Cash …………………………..……………………………….………………..

26,102

Loss on Sale of Investments ………………………..…

9,598

Long-Term Investments—AFS (Duracell) ……………………..

35,700

Sold Duracell shares [(1,800 x $15.00) – $898].

Dec. 31

Unrealized Gain⎯Equity ……………………………….………………..

2,220

Unrealized Loss⎯Equity ………………………………………………..

6,260

Fair Value Adjustment—AFS (LT)* ……………..……………

8,480

Annual adjustment to fair values.

*

Cost _

Fair Value

Coca-Cola …………………...

$ 41,480

$ 48,000

Motorola ……………………...

84,780

72,000

Total…………………………….

$126,260

$120,000

Coca-Cola: 1,000 x $48.00 = $48,000

Motorola: 3,000 x $24.00 = $72,000

$126,260 – $120,000 = $6,260

Fair Value Adjustment account:

Required balance …… $6,260 Cr.

Unadjusted balance .. 2,220 Dr.

Required change ……. $8,480 Cr.