Appendix 2B

Cost of Quality

Exercise 2B-1 (10 minutes)

1. Quality of conformance

2. Quality costs

Exercise 2B-2 (15 minutes)

1.

Prevention

Cost

Appraisal

Cost

Internal

Failure

Cost

External

Failure

Cost

a.

Product testing ……………….

X

b.

Product recalls ………………..

X

c.

Rework labor and overhead .

X

d.

Quality circles …………………

X

e.

Downtime caused by

defects ……………………….

X

f.

Cost of field servicing ……….

X

g.

Inspection of goods …………

X

h.

Quality engineering ………….

X

i.

Warranty repairs ……………..

X

j.

Statistical process control ….

X

k.

Net cost of scrap ……………..

X

l.

Depreciation of test

equipment …………………..

X

m.

Returns and allowances

arising from poor quality …

X

n.

Disposal of defective

products ……………………..

X

o.

Technical support to

suppliers ……………………..

X

p.

Systems development ………

X

q.

Warranty replacements …….

X

r.

Field testing at customer

site …………………………….

X

s.

Product design …………………

X

Problem 2B-3 (60 minutes)

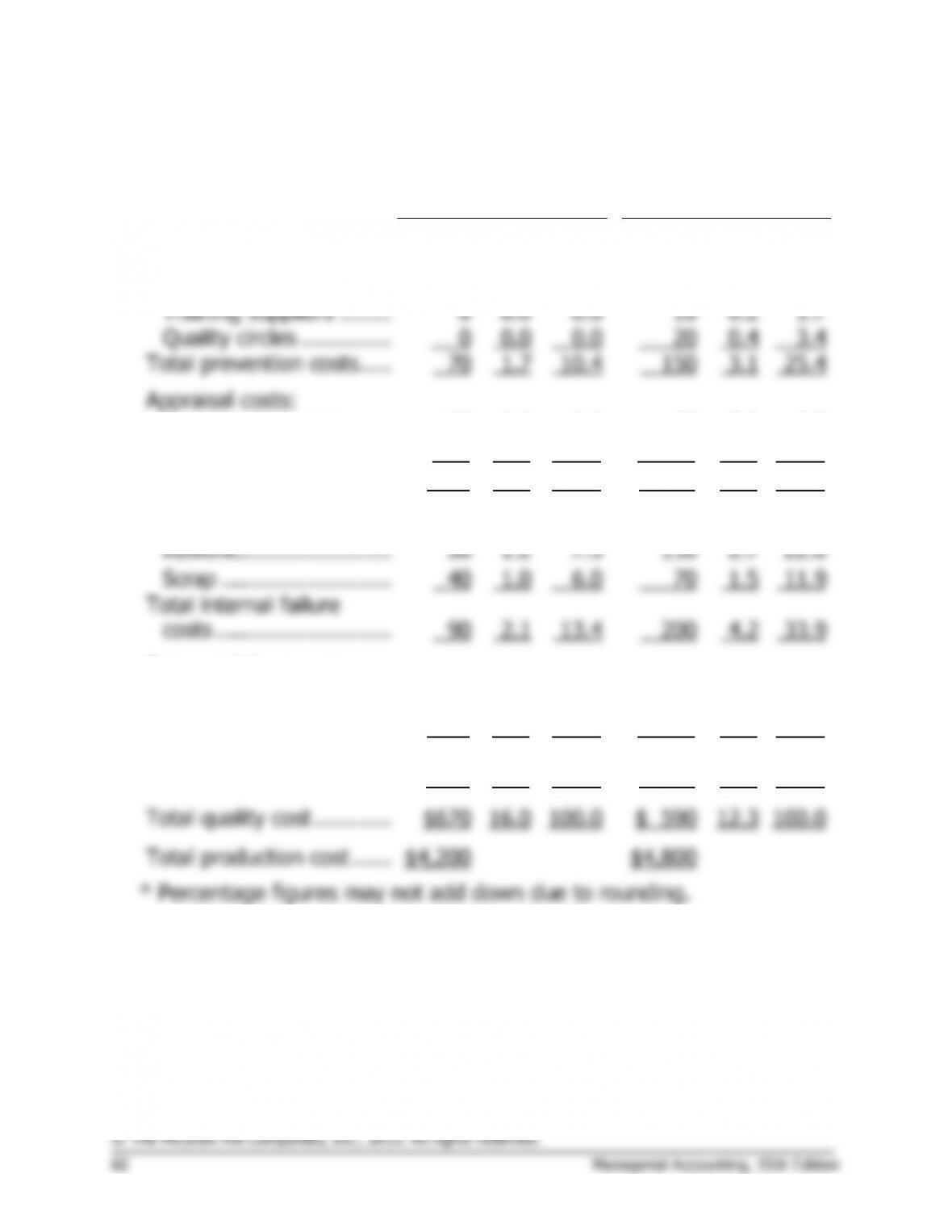

1. An analysis of the company’s quality cost report is presented below:

Last Year

This Year

Amount

Percent*

Amount

Percent*

Prevention costs:

Machine maintenance …

$70

1.7

10.4

$ 120

2.5

20.3

Training suppliers ……..

0

0.0

0.0

10

0.2

1.7

Quality circles …………..

0

0.0

0.0

20

0.4

3.4

Total prevention costs …..

70

1.7

10.4

150

3.1

25.4

Appraisal costs:

Incoming inspection …..

20

0.5

3.0

40

0.8

6.8

Final testing ……………..

80

1.9

11.9

90

1.9

15.3

Total appraisal costs …….

100

2.4

14.9

130

2.7

22.0

Internal failure costs:

Rework ……………………

50

1.2

7.5

130

2.7

22.0

Scrap ……………………..

40

1.0

6.0

70

1.5

11.9

Total internal failure

costs ………………………

90

2.1

13.4

200

4.2

33.9

External failure costs:

Warranty repairs ……….

90

2.1

13.4

30

0.6

5.1

Customer returns ………

320

7.6

47.8

80

1.7

13.6

Total external failure

costs ………………………

410

9.8

61.2

110

2.3

18.6

Total quality cost …………

$670

16.0

100.0

$ 590

12.3

100.0

Total production cost ……

$4,200

$4,800

* Percentage figures may not add down due to rounding.

Problem 2B-3 (continued)

From the above analysis it would appear that Mercury, Inc.’s program has

been successful.

• Total quality costs have declined from 16.0% to 12.3% as a

to 3.1% and from 10.4% of total quality costs to 25.4%. The

$80,000 increase is more than offset by decreases in other quality

costs.

2. The initial effect of emphasizing prevention and appraisal was to reduce

external failure costs and increase internal failure costs. The increase in

3. To measure the cost of not implementing the quality program,

management could assume that sales and market share would continue

Problem 2B-4 (60 minutes)

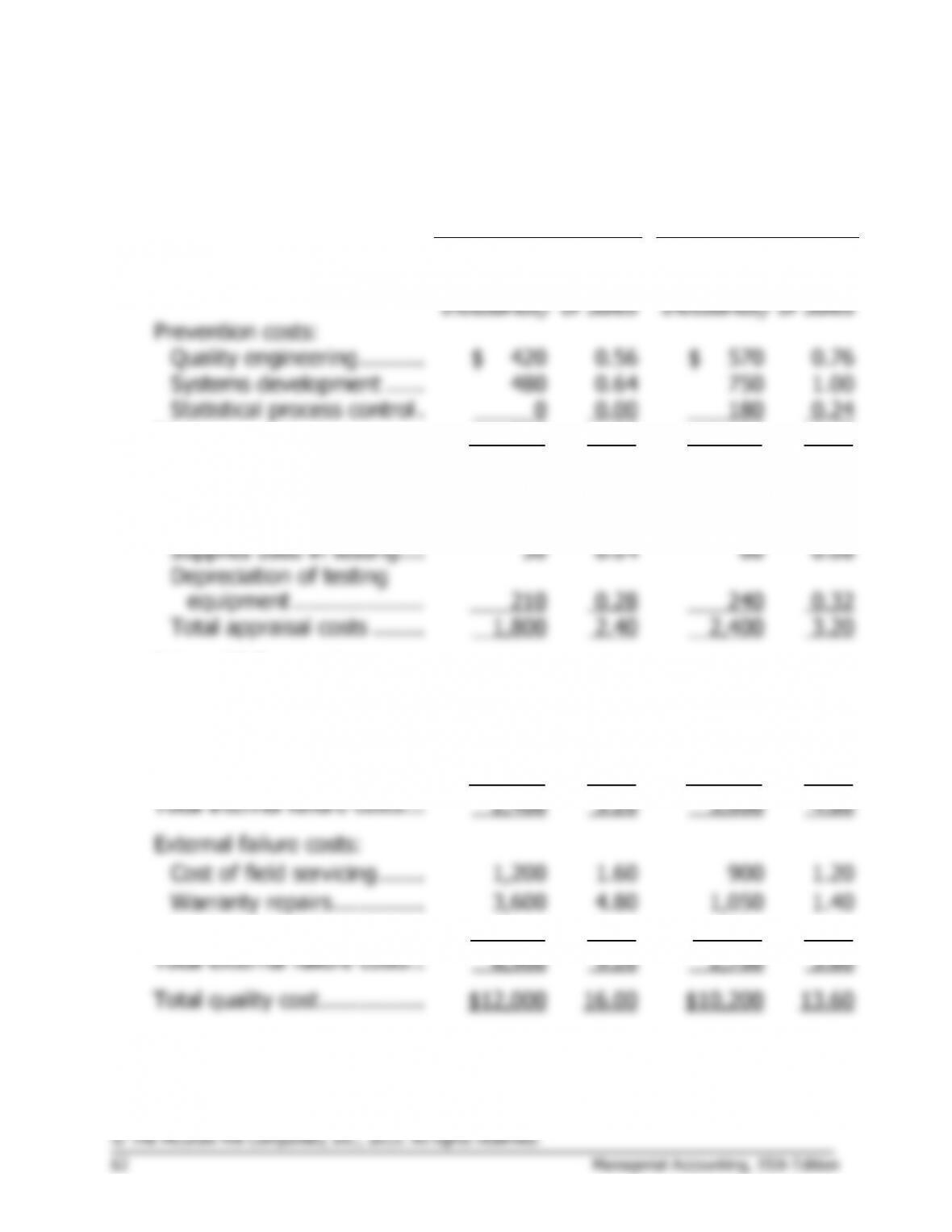

1.

Florex Company

Quality Cost Report

Last Year

This Year

Amount

(in

thousands)

Percent

of Sales

Amount

(in

thousands)

Percent

of Sales

Prevention costs:

Quality engineering ……….

$ 420

0.56

$ 570

0.76

Systems development ……

480

0.64

750

1.00

Statistical process control .

0

0.00

180

0.24

Total prevention costs ……..

900

1.20

1,500

2.00

Appraisal costs

Inspection …………………..

750

1.00

900

1.20

Product testing …………….

810

1.08

1,200

1.60

Supplies used in testing….

30

0.04

60

0.08

Depreciation of testing

equipment ………………..

210

0.28

240

0.32

Total appraisal costs ……..

1,800

2.40

2,400

3.20

Internal failure costs:

Net cost of scrap ………….

630

0.84

1,125

1.50

Rework labor ……………….

1,050

1.40

1,500

2.00

Disposal of defective

products …………………..

720

0.96

975

1.30

Total internal failure costs …

2,400

3.20

3,600

4.80

External failure costs:

Cost of field servicing …….

1,200

1.60

900

1.20

Warranty repairs …………..

3,600

4.80

1,050

1.40

Product recalls ……………..

2,100

2.80

750

1.00

Total external failure costs ..

6,900

9.20

2,700

3.60

Total quality cost …………….

$12,000

16.00

$10,200

13.60

Problem 2B-4 (continued)

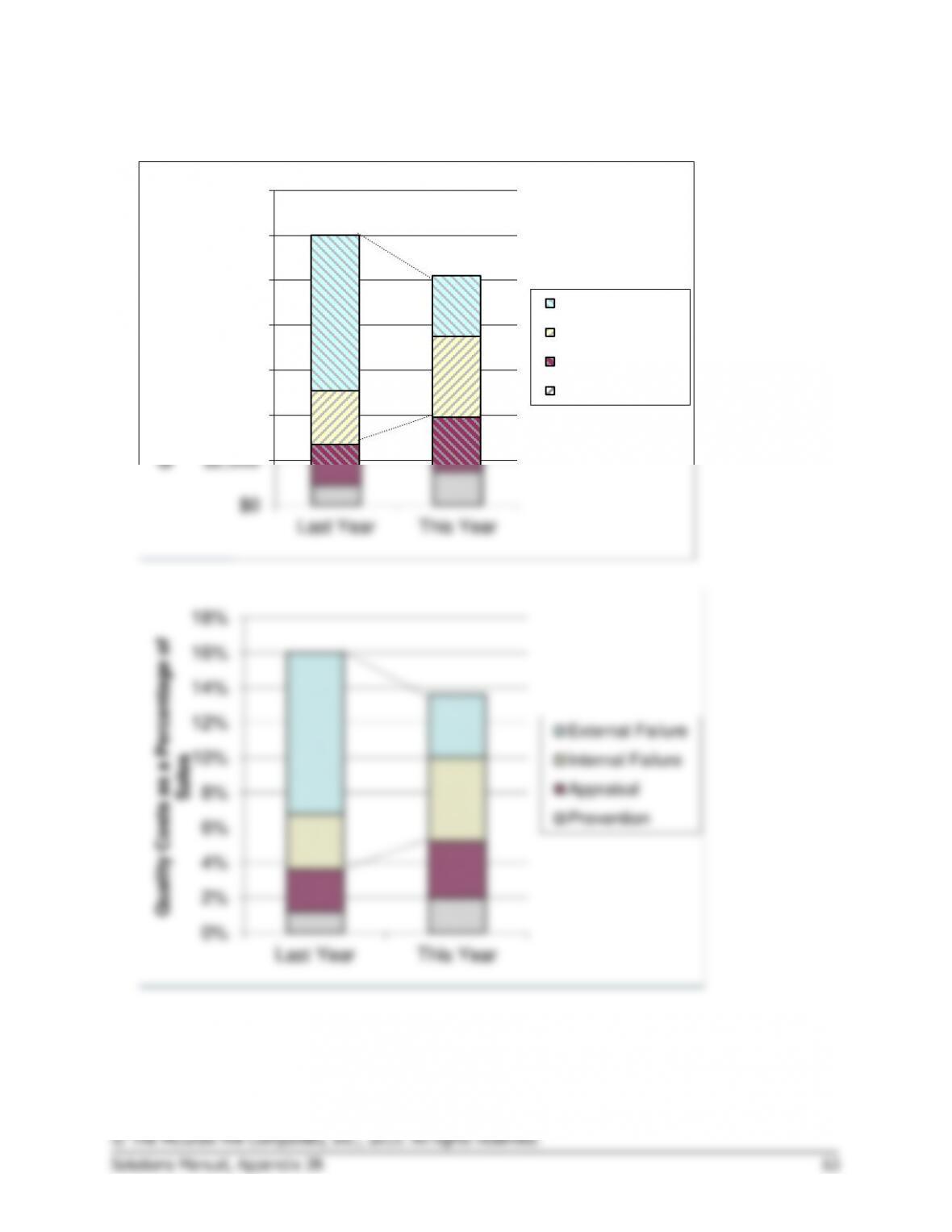

2.

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

Last Year This Year

Quality Costs (in thousands)

External Failure

Internal Failure

Appraisal

Prevention

Problem 2B-4 (continued)

3. The overall impact of the company’s increased emphasis on quality over

the past year has been positive in that total quality costs have

decreased from 16% of sales to 13.6% of sales. Despite this

improvement, the company still has a poor distribution of quality costs.

for the moment, these costs should decrease in time as better quality is