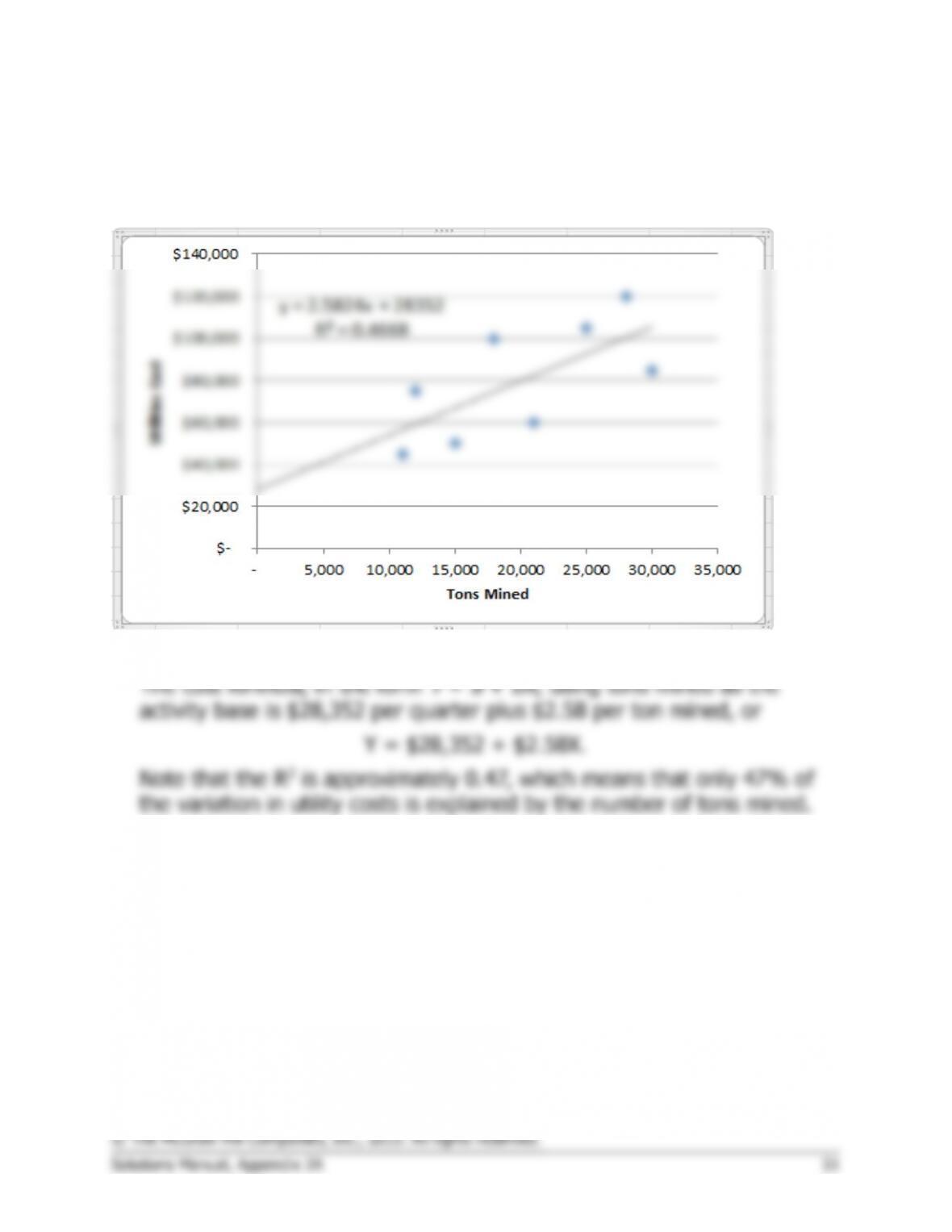

Problem 2A-3 (30 minutes)

1. The scattergraph plot and regression estimates of fixed and variable

costs using Microsoft Excel are shown below:

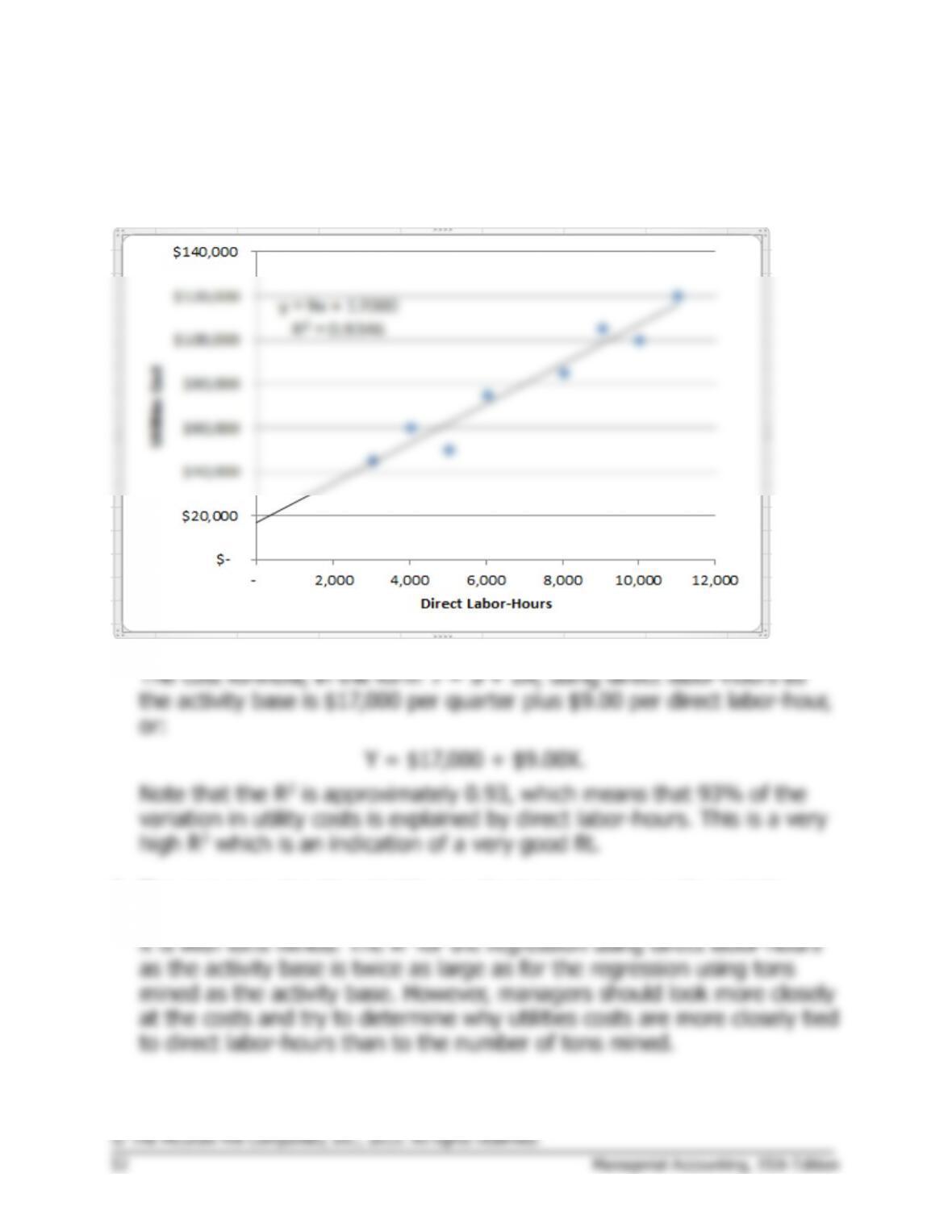

Problem 2A-3 (continued)

2. The scattergraph plot and regression estimates of fixed and variable

costs using Microsoft Excel are shown below:

3. The company should probably use direct labor-hours as the activity

base, since the fit of the regression line to the data is much tighter than

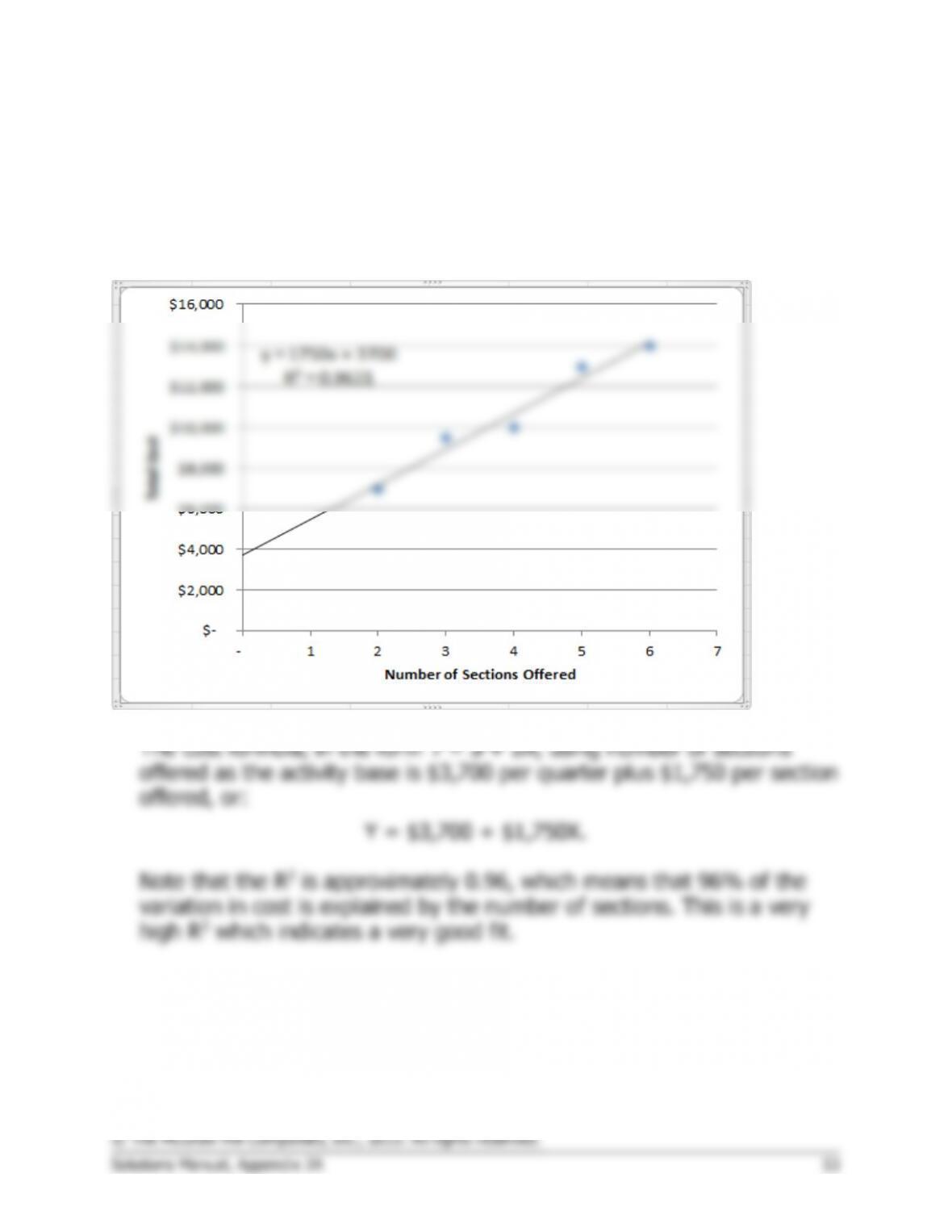

Problem 2A-4 (30 minutes)

1. and 2.

The scattergraph plot and regression estimates of fixed and variable costs

using Microsoft Excel are shown below:

Problem 2A-4 (continued)

3. Expected total cost would be:

Fixed cost ……………………………………………….

$ 3,700

Variable cost (8 sections × $1,750 per section) .

14,000

Total cost ………………………………………………..

$17,700

The problem with using the cost formula from (2) to derive total cost is

that an activity level of 8 sections may lie outside the relevant range—

the range of activity within which the fixed cost is approximately $3,700

per term and the variable cost is approximately $1,750 per section

offered. These approximations appear to be reasonably accurate within

the range of 2 to 6 sections, but they may be invalid outside this range.

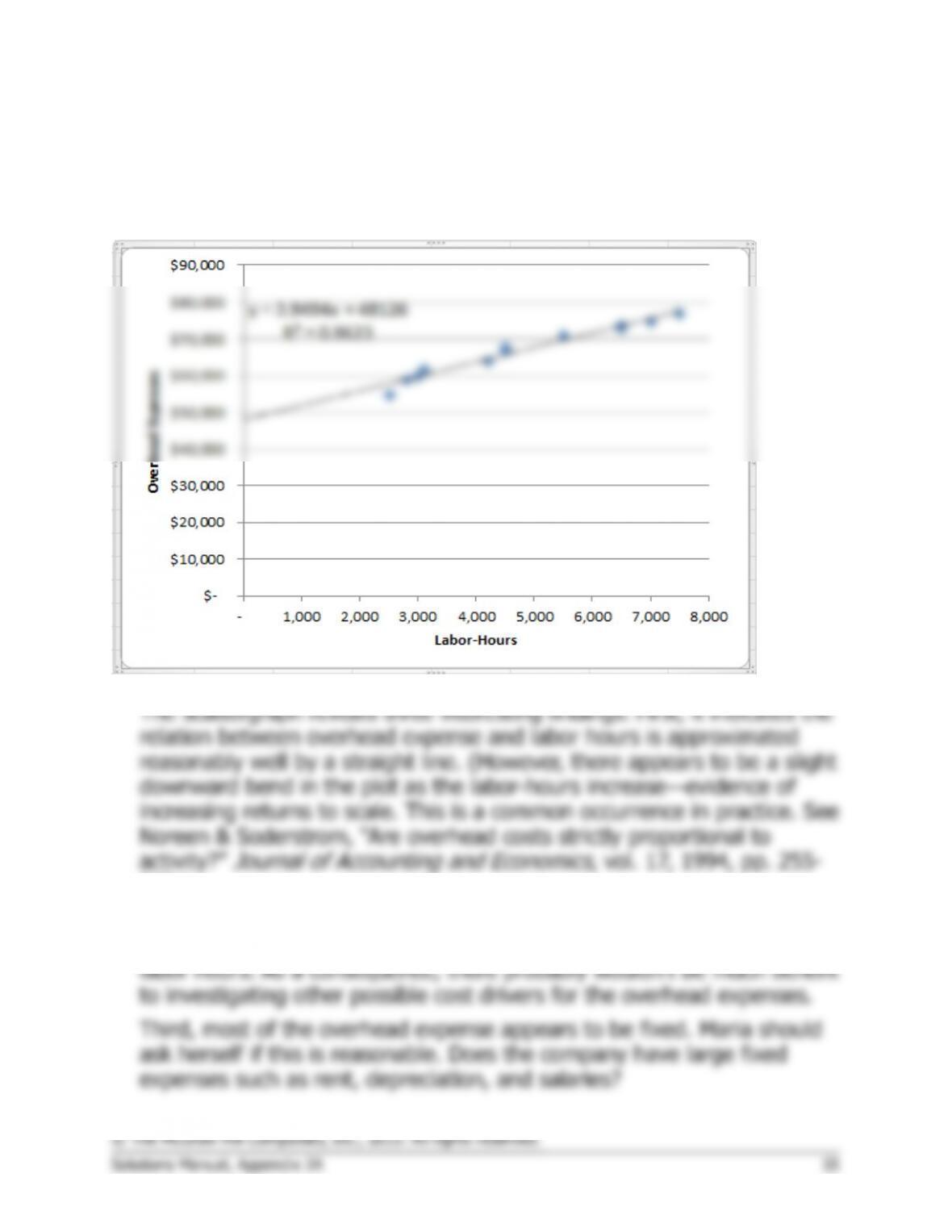

CASE 2A-5 (45 minutes)

1. and 2.

The scattergraph plot and regression estimates of fixed and variable

costs using Microsoft Excel are shown below:

278.)

Second, the data points are all fairly close to the straight line. This

indicates that most of the variation in overhead expenses is explained by

CASE 2A-5 (continued)

3. Using the least-squares regression estimate of the variable overhead

cost, the total variable cost per guest is computed as follows:

Food and beverages ………………………..

$15.00

Labor (0.5 hour @ $10 per hour) ……….

5.00

Overhead (0.5 hour @ $3.95 per hour) .

1.98

Total variable cost per guest ……………..

$21.98

The total contribution from 180 guests paying $31 each is computed as

follows:

Sales (180 guests @ $31.00 per guest) …………..

$5,580.00

Variable cost (180 guests @ $21.98 per guest) …

3,956.40

Contribution to profit…………………………………..

$1,623.60

Fixed costs are not included in the above computation because there is

no indication that any additional fixed costs would be incurred as a

consequence of catering the cocktail party. If additional fixed costs were

incurred, they should also be subtracted from revenue.

4. Assuming that no additional fixed costs are incurred as a result of

catering the charity event, any price greater than the variable cost per

guest of roughly $22 would contribute to profits.

CASE 2A-5 (continued)

5. We would favor bidding slightly less than $30 to get the contract. Any

bid above $22 would contribute to profits and a bid at the normal price

of $31 is unlikely to land the contract. And apart from the contribution

to profit, catering the event would show off the company’s capabilities