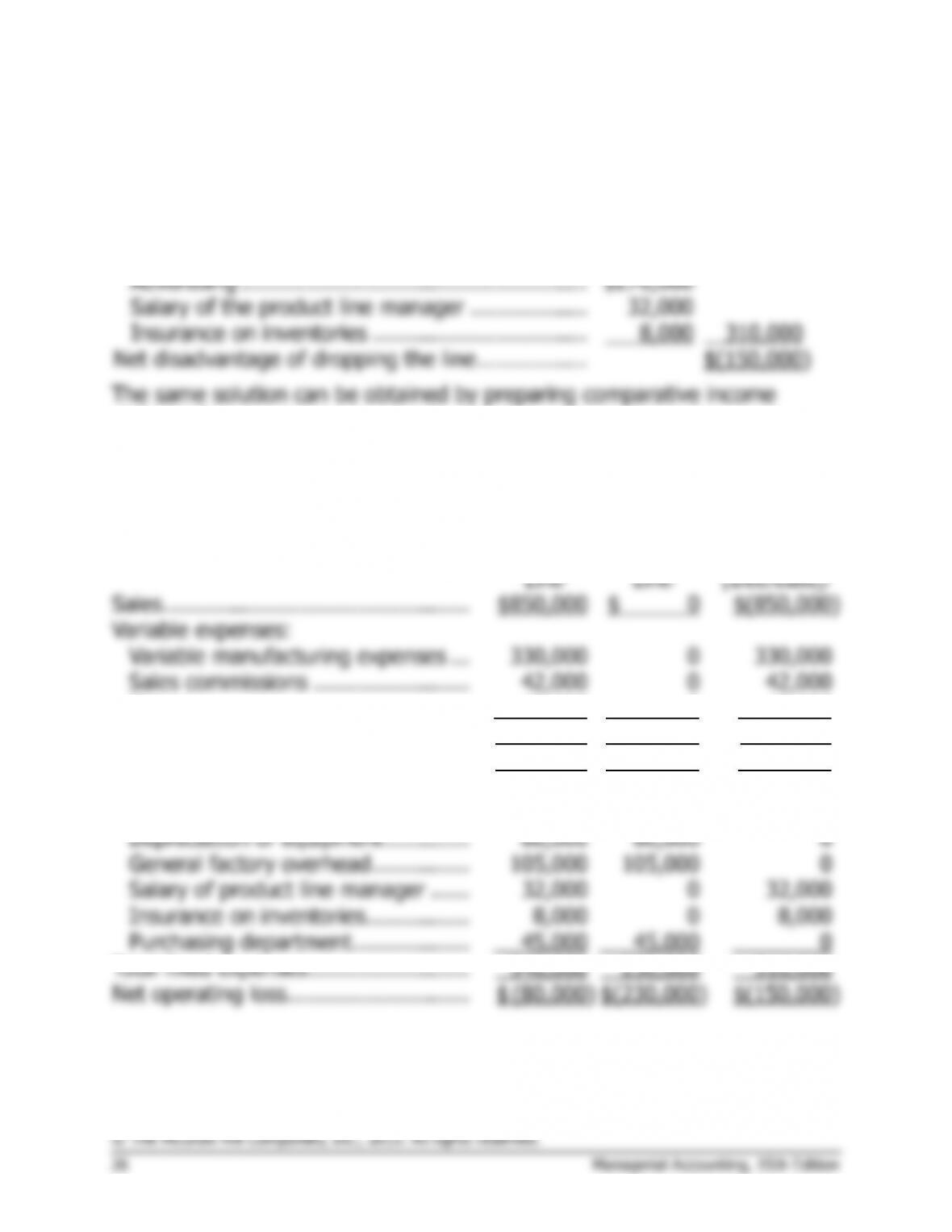

Exercise 12–10 (15 minutes)

The target production level is 40,000 starters per period, as shown by the

relations between per-unit and total fixed costs.

“Cost”

Per

Differential

Costs

Unit

Make

Buy

Explanation

Direct materials ……

$3.10

$3.10

Can be avoided by buying

Direct labor …………

2.70

2.70

Can be avoided by buying

Variable

manufacturing

overhead ………….

0.60

0.60

Can be avoided by buying

Supervision …………

1.50

1.50

Can be avoided by buying

Depreciation

1.00

—

Sunk Cost

Rent ………………….

0.30

—

Allocated Cost

Outside purchase

price ……………….

$8.40

Total cost ……………

$9.20

$7.90

$8.40

The company should make the starters, rather than continuing to buy

from the outside supplier. Making the starters will result in a $0.50 per

starter cost savings, or a total savings of $20,000 per period:

$0.50 per starter × 40,000 starters = $20,000

Exercise 12-11 (20 minutes)

The costs that can be avoided as a result of purchasing from the outside

are relevant in a make-or–buy decision. The analysis is:

Per Unit

Differential

Costs

30,000 Units

Make

Buy

Make

Buy

Cost of purchasing ……………….

$21.00

$630,000

Cost of making:

Direct materials …………………

$ 3.60

$108,000

Direct labor ………………………

10.00

300,000

Variable overhead ……………..

2.40

72,000

Fixed overhead …………………

3.00

*

90,000

Total cost …………………………..

$19.00

$21.00

$570,000

$630,000

*

The remaining $6 of fixed overhead cost would not be relevant,

because it will continue regardless of whether the company makes

or buys the parts.

The $80,000 rental value of the space being used to produce part S-6 is an

opportunity cost of continuing to produce the part internally. Thus, the

complete analysis is:

Make

Buy

Total cost, as above ………………………………….

$570,000

$630,000

Rental value of the space (opportunity cost) …..

80,000

Total cost, including opportunity cost ……………

$650,000

$630,000

Net advantage in favor of buying …………………

$20,000

Profits would increase by $20,000 if the outside supplier’s offer is accepted.