Exercise 12-2 (continued)

2. The segmented report can be improved by eliminating the allocation of

the common fixed expenses. Following the format introduced in Chapter

12 for a segmented income statement, a better report would be:

Total

Dirt

Bikes

Mountain

Bikes

Racing

Bikes

Sales ……………………………..

$300,000

$90,000

$150,000

$60,000

Variable manufacturing and

selling expenses …………….

120,000

27,000

60,000

33,000

Contribution margin ………….

180,000

63,000

90,000

27,000

Traceable fixed expenses:

Advertising ……………………

30,000

10,000

14,000

6,000

Depreciation of special

equipment ………………….

23,000

6,000

9,000

8,000

Salaries of the product line

managers …………………..

35,000

12,000

13,000

10,000

Total traceable fixed

expenses………………………

88,000

28,000

36,000

24,000

Product line segment margin

92,000

$35,000

$ 54,000

$ 3,000

Common fixed expenses …….

60,000

Net operating income ………..

$ 32,000

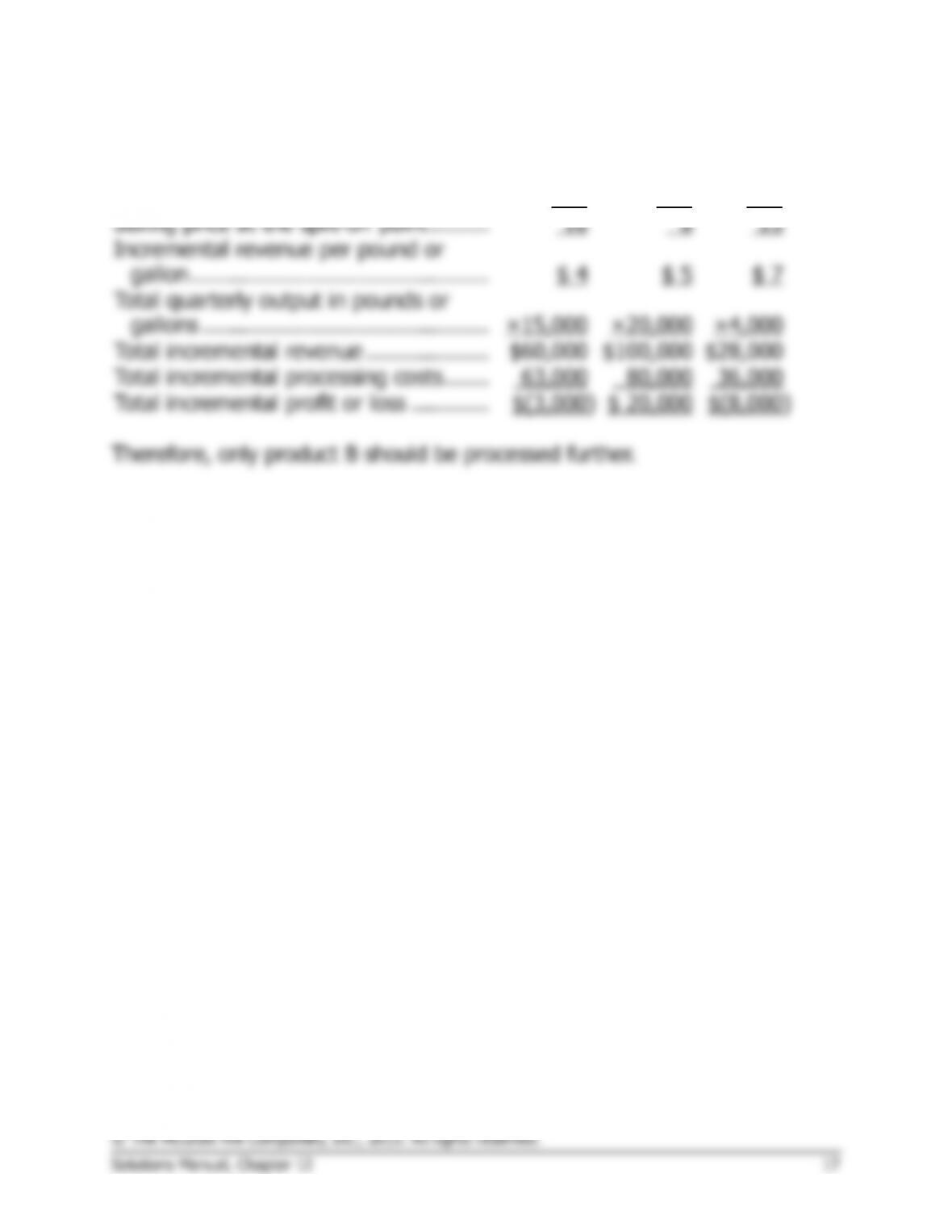

Exercise 12–3 (30 minutes)

1.

Per Unit

Differential

Costs

15,000 units

Make

Buy

Make

Buy

Cost of purchasing …………………..

$35

$525,000

Direct materials ………………………

$14

$210,000

Direct labor …………………………...

10

150,000

Variable manufacturing overhead .

3

45,000

Fixed manufacturing overhead,

traceable1 …………………………...

2

30,000

Fixed manufacturing overhead,

common ……………………………..

Total costs …………………………….

$29

$35

$435,000

$525,000

Difference in favor of continuing to

make the carburetors …………….

$6

$90,000

1

Only the supervisory salaries can be avoided if the carburetors are

purchased. The remaining book value of the special equipment is a

sunk cost; hence, the $4 per unit depreciation expense is not

relevant to this decision.

Based on these data, the company should reject the offer and should

continue to produce the carburetors internally.

2.

Make

Buy

Cost of purchasing (part 1) ……………………….

$525,000

Cost of making (part 1) …………………………...

$435,000

Opportunity cost—segment margin foregone

on a potential new product line ……………….

150,000

Total cost ………………………………………………

$585,000

$525,000

Difference in favor of purchasing from the

outside supplier ……………………………………

$60,000

Thus, the company should accept the offer and purchase the

carburetors from the outside supplier.