Chapter 12

Differential Analysis: The Key to Decision

Making

Solutions to Questions

12-1 A relevant cost is a cost that differs in

change in cost (or benefit) that will result from

some proposed action. An opportunity cost is

12-3 No. Variable costs are relevant costs

in total amount in direct proportion to changes

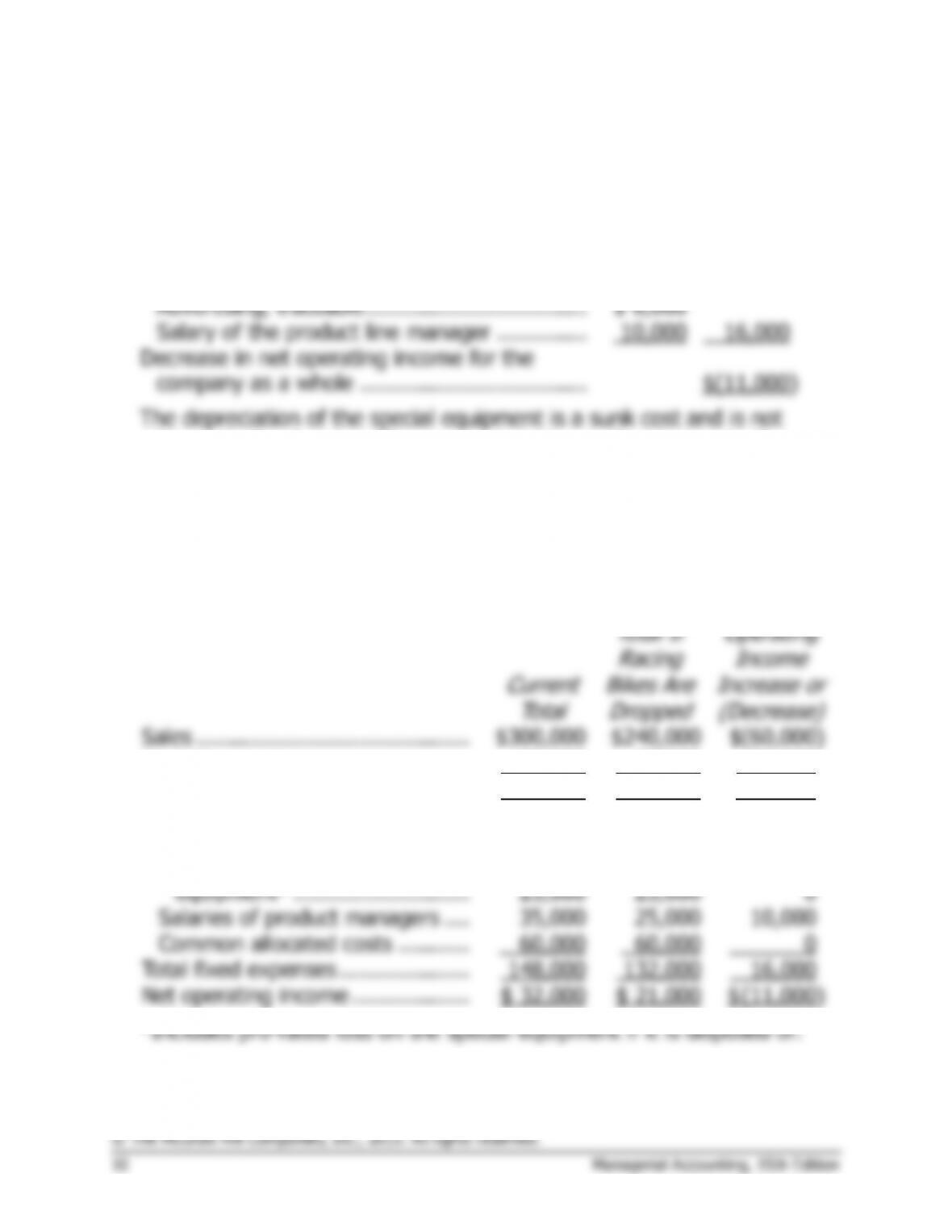

12-8 Not necessarily. An apparent loss may

be the result of allocated common costs or of

as a result of dropping the product is less than

12-9 Allocations of common fixed costs can

12–10 If a company decides to make a part

internally rather than to buy it from an outside

are machine time, direct labor time, floor space,

12–13 Joint products are two or more products

The Foundational 15

1. The total traceable fixed manufacturing overhead for Alpha and Beta is

computed as follows:

Alpha

Beta

Traceable fixed overhead per unit (a) ……..

$16

$18

Level of activity in units (b) …………………..

100,000

100,000

Total traceable fixed overhead (a) × (b) ….

$1,600,000

$1,800,000

2. The total common fixed expenses is computed as follows:

Alpha

Beta

Common fixed expenses per unit (a) ………

$15

$10

Level of activity in units (b) …………………..

100,000

100,000

Total common fixed expenses (a) × (b) …..

$1,500,000

$1,000,000

The company’s total common fixed expenses would be $2,500,000.

3. The profit impact is computed as follows:

Per

Total

Unit

10,000 units

Incremental revenue ……………………….

$80

$800,000

Incremental costs:

Variable costs:

Direct materials ………………………….

30

300,000

Direct labor ……………………………….

20

200,000

Variable manufacturing overhead …..

7

70,000

Variable selling expenses ……………..

12

120,000

Total variable cost ………………………..

$69

690,000

Incremental net operating income ………

$110,000

The Foundational 15 (continued)

4. The profit impact is computed as follows:

Per

Total

Unit

5,000 units

Incremental revenue ……………………….

$39

$195,000

Incremental costs:

Variable costs:

Direct materials ………………………….

12

60,000

Direct labor ……………………………….

15

75,000

Variable manufacturing overhead …..

5

25,000

Variable selling expenses ……………..

8

40,000

Total variable cost ………………………..

$40

200,000

Incremental net operating income ………

$ (5,000)

5. The profit impact is computed as follows:

Incremental revenue

(10,000 units × $80) (a) …………………….…….

$800,000

Incremental variable costs:

Direct materials (5,000 units × $30) ………………….

$150,000

Direct labor (5,000 units × $20) ……………………….

100,000

Variable manufacturing overhead

(5,000 units × $7) ………………………..…

35,000

Variable selling expenses

(5,000 units × $12) …………………………..

60,000

Total incremental variable cost (b) ………..…………….

345,000

Foregone sales to regular customers

(5,000 units × $120) (c) …………………….…….

600,000

Incremental net operating income

(a) − (b) – (c) ………………………………….…………….

$(145,000)

Note to instructors: Emphasize to students that the variable costs

related to 5,000 units of production are irrelevant to the decision

because they will be incurred whether the special order is accepted or

rejected.

The Foundational 15 (continued)

6. The profit impact of dropping the Beta product line is computed as

follows:

Contribution margin lost if the Beta product line is

dropped* ………………………………………………………..

$(3,600,000)

Traceable fixed manufacturing overhead …………………..

1,800,000

Decrease in net operating income if Beta is dropped ……

$(1,800,000)

* Beta’s contribution margin per unit is $40 ($80 − $40). Therefore, the

decrease in contribution margin if Beta is dropped would be $3,600,000

(90,000 units × $40).

Note to instructors: Emphasize that the traceable fixed manufacturing

overhead is avoidable and the common fixed expenses are not.

7. The profit impact of dropping the Beta product line is computed as

follows:

Contribution margin lost if the Beta product line is

dropped* ………………………………………………………....

$(1,600,000)

Traceable fixed manufacturing overhead …………………....

1,800,000

Increase in net operating income if Beta is dropped ……..

$ 200,000

* Beta’s contribution margin per unit is $40 ($80 − $40). Therefore, the

decrease in contribution margin if Beta is dropped would be $1,600,000

(40,000 units × $40).

8. The profit impact of dropping the Beta product line is computed as

follows:

Contribution margin lost if the Beta product line is

dropped …………………………………………………………...

$(2,400,000)

Traceable fixed manufacturing overhead …………………....

1,800,000

Contribution margin on additional Alpha sales* …………

765,000

Increase in net operating income if Beta is dropped ……..

$ 165,000

* Alpha’s contribution margin per unit is $51 ($120 − $69). Therefore,

the increase in Alpha’s contribution margin if Beta is dropped would be

$765,000 (15,000 units × $51).

The Foundational 15 (continued)

9. The profit impact of buying 80,000 Alphas from a supplier rather than

making them is computed as follows:

Make

Buy

Cost of purchasing (80,000 units × $80) ……..

$6,400,000

Direct materials (80,000 units × $30) …………

$2,400,000

Direct labor (80,000 units × $20) ………………

1,600,000

Variable manufacturing overhead

(80,000 units × $7) ……………………………..

560,000

Traceable fixed manufacturing overhead ……..

1,600,000

Total costs ……………………………………………

$6,160,000

$6,400,000

Difference in favor of continuing

to make the Alphas ……………….

$240,000

Note to instructors: Emphasize that the variable selling expenses are

irrelevant to this decision because they will be incurred regardless of

whether the company makes or buys its Alphas.

10. The profit impact of buying 50,000 Alphas from a supplier rather than

making them is computed as follows:

Make

Buy

Cost of purchasing (50,000 units × $80) ……..

$4,000,000

Direct materials (50,000 units × $30) …………

$1,500,000

Direct labor (50,000 units × $20) ………………

1,000,000

Variable manufacturing overhead

(50,000 units × $7) ……………………………..

350,000

Traceable fixed manufacturing overhead ……..

1,600,000

Total costs ……………………………………………

$4,450,000

$4,000,000

Difference in favor of buying

Alphas from the supplier ……..…

$450,000

Note to instructors: Emphasize that the variable selling expenses are

irrelevant to this decision because they will be incurred regardless of

whether the company makes or buys its Alphas.

The Foundational 15 (continued)

11. The pounds of raw material per unit are computed as follows:

Alpha

Beta

Direct material cost per unit (a) ……………………….

$30

$12

Cost per pound of direct materials (b) ……………….

$6

$6

Pounds of direct materials per unit (a) ÷ (b) ……….

5

2

12. The contribution margins per pound of raw materials are computed as

follows:

Alpha

Beta

Selling price per unit………………………….

$120

$80

Variable cost per unit ………………………..

69

40

Contribution margin per unit (a) …………..

$ 51

$40

Pounds of direct material required to

produce one unit (b) ……………………….

5 pounds

2 pounds

Contribution margin per pound (a) ÷ (b) .

$10.20

$20.00

13. The optimal number of units to produce would be computed as

follows:

Product

Pounds

Per Unit

Units

Produced

Total

Pounds

Beta ……………………………..

2

60,000

120,000

Alpha …………………………….

5

8,000

40,000

Total pounds available ………

160,000

The Foundational 15 (continued)

14. The total contribution margin would be computed as follows:

Alpha

Beta

Number of units produced (a) ………………………….

8,000

60,000

Contribution margin per unit (b) ……………………….

$51

$40

Total contribution margin (a) × (b) …………..……….

$408,000

$2,400,000

The company’s total contribution margin would be $2,808,000

($408,000 + $2,400,000).

15. The maximum price per pound is computed as follows:

Alpha

Regular direct material cost per pound ………………………..

$ 6.00

Contribution margin per pound of direct materials ………….

10.20

Maximum price to be paid per pound…………………………..

$16.20

Because the company has satisfied all demand for Betas, it would use

additional raw materials to produce Alphas.