Financial & Managerial Accounting, 5th Edition

364

Serial Problem — SP 5, Success Systems (concluded)

2.

Per Unit

Total

Total

LCM Applied

Inventory Items

Units

Cost

Market

Cost

Market

To Items

Office productivity ……..

3

$ 76

$ 74

$228

$222

$222

Desktop publishing ……

2

103

100

206

200

200

Accounting ………………..

3

90

96

270

288

270

$704

$710

$692

Assuming LCM is applied to the “items of inventory,” the $692 market

value (per items) is less than the $704 total cost of inventory. Thus, the

company must adjust the currently reported inventory value from $704 to

the LCM value of $692.

Part B

1. Ratio computations for the three months ended March 31, 2014:

Inventory Turnover = Cost of Goods Sold / Average Inventory

2. Success Systems outperforms its competitors on both ratios. Its

Reporting in Action — BTN 5-1

($ thousands for all parts)

1. Ending inventories at December 31, 2011: $298,042.

2. December 31, 2011: $298,042/$1,228,024 = 0.243 or 24.3%

3. Polaris’s inventories are its second largest assets (behind cash) at

December 31, 2011. Equipment and tooling has a higher gross value

4. Reviewing notes to its financial statements, we see Note 1 under the

subheading “inventories” that Polaris’s raw materials are stated at the

lower of cost or market. Polaris uses the first–in-first-out basis to

determine cost.

5. a. Inventory turnover =

Average inventory = ($298,042 + $235,927)/2

6. Solution depends on the financial statement information obtained.

Cost of sales

Average inventory

Comparative Analysis — BTN 5-2

($ thousands)

1. Inventory turnover =

Polaris — current year

Inventory turnover = = 7.18 times

Polaris — one year prior

Cost of sales

Average inventory

$1,916,366

($298,042 + $235,927)/2

Comparative Analysis (Concluded)

2. Days’ sales in inventory = x 365

Current year — Polaris’s days’ sales in inventory

x 365 = 56.8 days

One year prior —Polaris’s days’ sales in inventory

$363,142

3. For all years examined here, Polaris manages its inventory more

efficiently than does Arctic Cat. Polaris’s inventory turnover is higher,

Ending Inventory

Costs of Goods Sold

$298,042

$1,916,366

$480,441

Financial & Managerial Accounting, 5th Edition

368

Ethics Challenge — BTN 5-3

1. Profit Margin: In an economic environment of rising costs, the use of

FIFO results in a lower cost of goods sold than LIFO. If cost of goods

sold is lower, then net income will be higher. A higher net income will

2. First, it is true that managers have discretion in choosing an inventory

costing method. It appears, however, that Golf Challenge’s owner does

not understand that changing methods can only be done very

selectively over time. A change in method must be justified by

Communicating in Practice — BTN 5–4

[Note: An acceptable memorandum format should be used.]

The body of the memo would likely recommend use of the LIFO method for

this start-up business. The memo should explain that this would allow for

the matching of the most recent (higher) costs against revenue through

Taking It to the Net — BTN 5-5

1. Apple designs, manufactures, and markets mobile communication and

2. Its summary of significant accounting policies (Note 1) reports:

3. Its gross margin for 2011 is ($ millions)

Sales ……………………………………………………………

$108,249

Cost of sales ………………………………………………..

(64,431)

Gross margin ……………………………………………….

$ 43,818

Gross margin ratio is: $43,818 / $108,249 = 0.405 or 40.5%

Comment: Its gross margin ratio is on par with the industry average

gross margin ratio of 40%.

4. 2011 Inventory turnover* =

$64,431/ [($776 + $1,051)/2] = 70.5 times

2011 Days’ sales in inventory* =

Teamwork in Action — BTN 5-6

Concepts and procedures to illustrate in expert presentation:

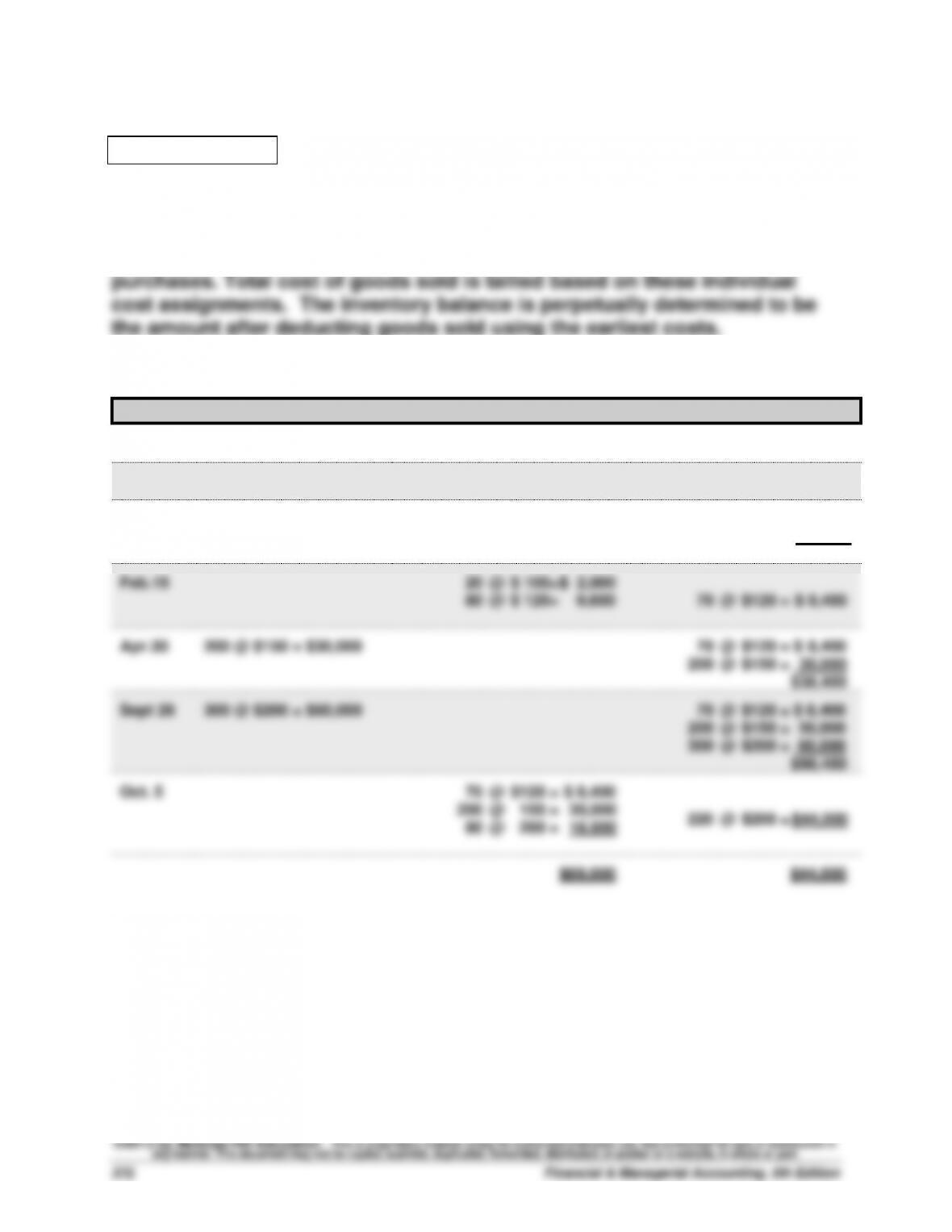

Specific Identification Expert:

(a) and (b) Concept:

Purchases are always recorded at the actual specific costs. The specific

identification cost flow assumption requires units sold be assigned their

actual cost. Total cost of goods sold is tallied based on these individual

cost assignments. The new inventory balance is perpetually determined to

be the amount after sales at actual cost is deducted.

(a) and (b) Procedures:

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Jan. 1

50 @ $100 = $ 5,000

Jan.10

30 @ $ 100 = $ 3,000

20 @ $100 = $ 2,000

Jan.14

150 @ $120 = $18,000

20 @ $100 = $ 2,000

150 @ $120 = 18,000

$20,000

Feb.15

100 @ $ 120 = $12,000

20 @ $100 = $ 2,000

50 @ $120 = 6,000

$ 8,000

Apr.30

200 @ $150 = $30,000

20 @ $100 = $ 2,000

50 @ $120 = 6,000

200 @ $150 = 30,000

$38,000

Sept 26

300 @ $200 = $60,000

20 @ $100 = $ 2,000

50 @ $120 = 6,000

200 @ $150 = 30,000

300 @ $200 = 60,000

$98,000

Oct. 5

100 @ $ 150 = $15,000

250 @ $ 200 = $50,000

20 @ $100 = $ 2,000

50 @ $120 = 6,000

100 @ $150 = 15,000

50 @ $200 = 10,000

$80,000

$33,000

Teamwork in Action (Continued)

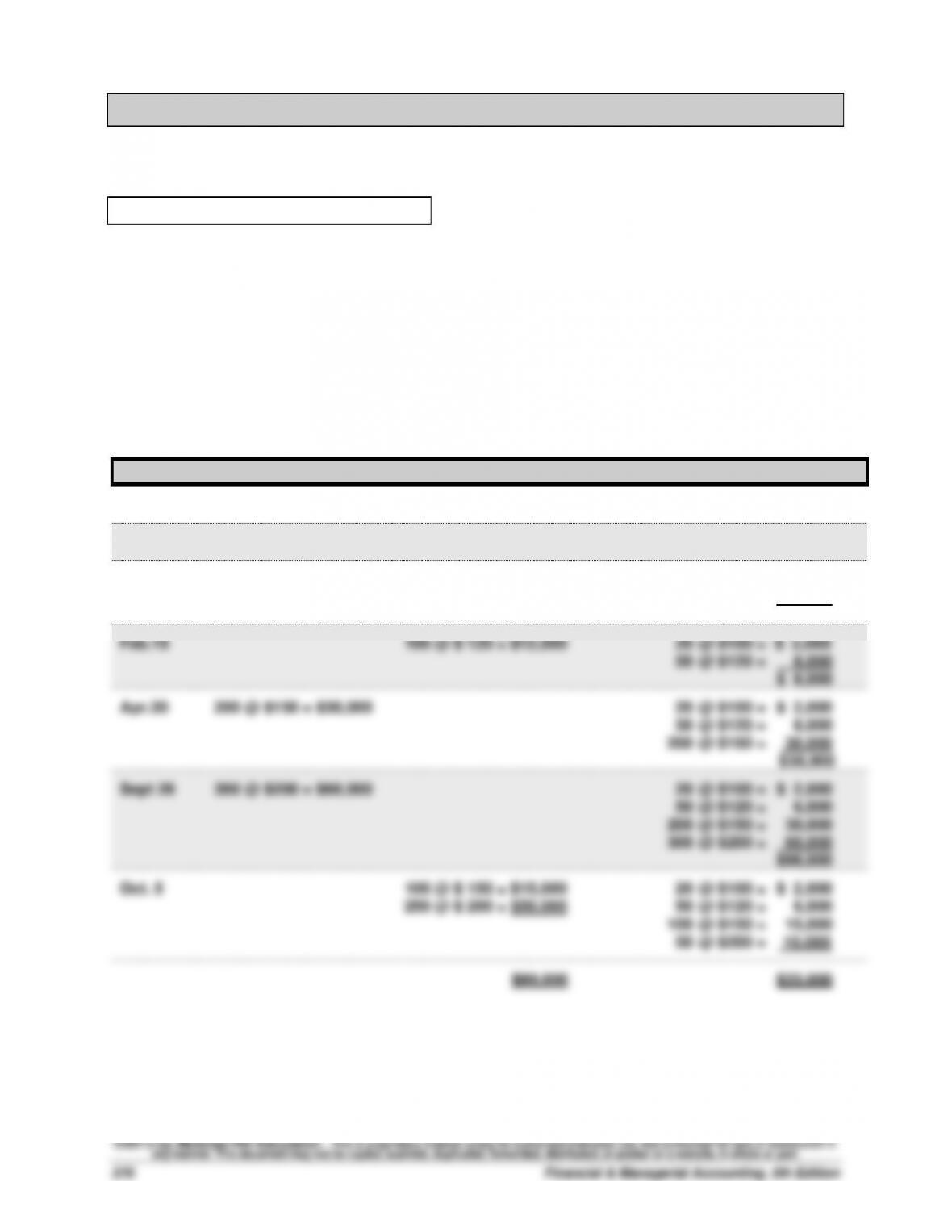

LIFO Expert:

(a) and (b) Concept:

Purchases are always recorded at actual costs. The LIFO cost flow

assumption requires (i) units sold be assigned the most recent cost—total

(a) and (b) Procedures:

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Jan. 1

50 @ $100 = $ 5,000

Jan.10

30 @ $100 = $ 3,000

20 @ $100 = $ 2,000

Jan.14

150 @ $120 = $18,000

20 @ $100 = $ 2,000

150 @ $120 = 18,000

$20,000

Feb.15

100 @ $120 = $12,000

20 @ $100 = $ 2,000

50 @ $120 = 6,000

$ 8,000

Apr.30

200 @ $150 =$30,000

20 @ $100 = $ 2,000

50 @ $120 = 6,000

200 @ $150 = 30,000

$38,000

Sept 26

300 @ $200 = $60,000

20 @ $100 = $ 2,000

50 @ $120 = 6,000

200 @ $150 = 30,000

300 @ $200 = 60,000

$98,000

Oct. 5

300 @ $200 = $60,000

50 @ $150 = $ 7,500

______

20 @ $100 = $ 2,000

50 @ $120 = 6,000

150 @ $150 = 22,500

$82,500

$30,500

Teamwork in Action (Continued)

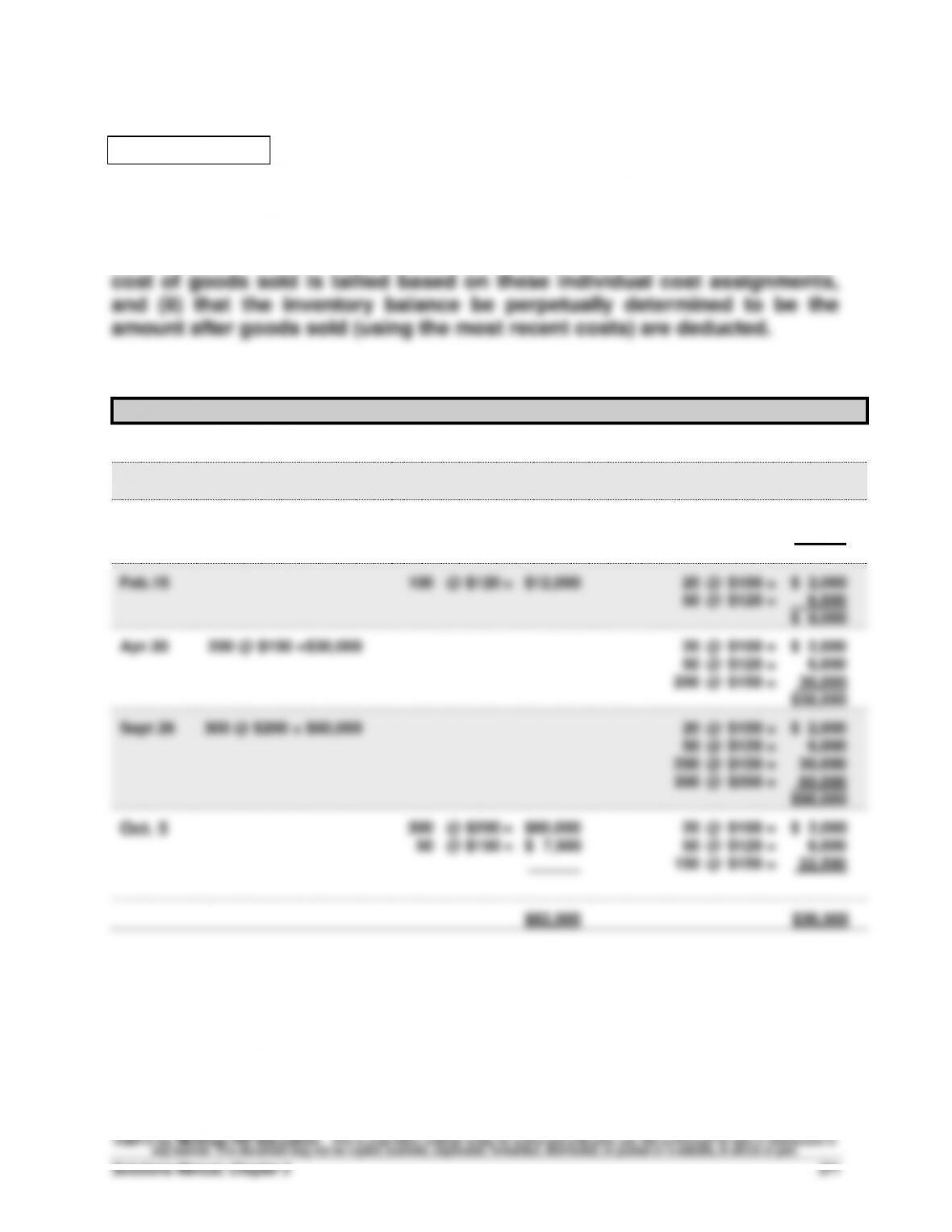

FIFO Expert:

(a) and (b) Concept:

Purchases are always recorded at actual costs. The FIFO cost flow

assumption requires units sold be assigned the first (earliest) cost of

(a) and (b) Procedures:

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Jan. 1

50 @ $100 = $ 5,000

Jan.10

30 @ $100 = $ 3,000

20 @ $100 = $ 2,000

Jan.14

150 @ $120 = $18,000

20 @ $100 = $ 2,000

150 @ $120 = 18,000

$20,000

Feb.15

20 @ $ 100= $ 2,000

80 @ $ 120= 9,600

70 @ $120 = $ 8,400

Apr.30

200 @ $150 = $30,000

70 @ $120 = $ 8,400

200 @ $150 = 30,000

$38,400

Sept 26

300 @ $200 = $60,000

70 @ $120 = $ 8,400

200 @ $150 = 30,000

300 @ $200 = 60,000

$98,400

Oct. 5

70 @ $120 = $ 8,400

200 @ 150 = 30,000

80 @ 200 = 16,000

220 @ $200 = $44,000.

$69,000

$44,000

Teamwork in Action (Continued)

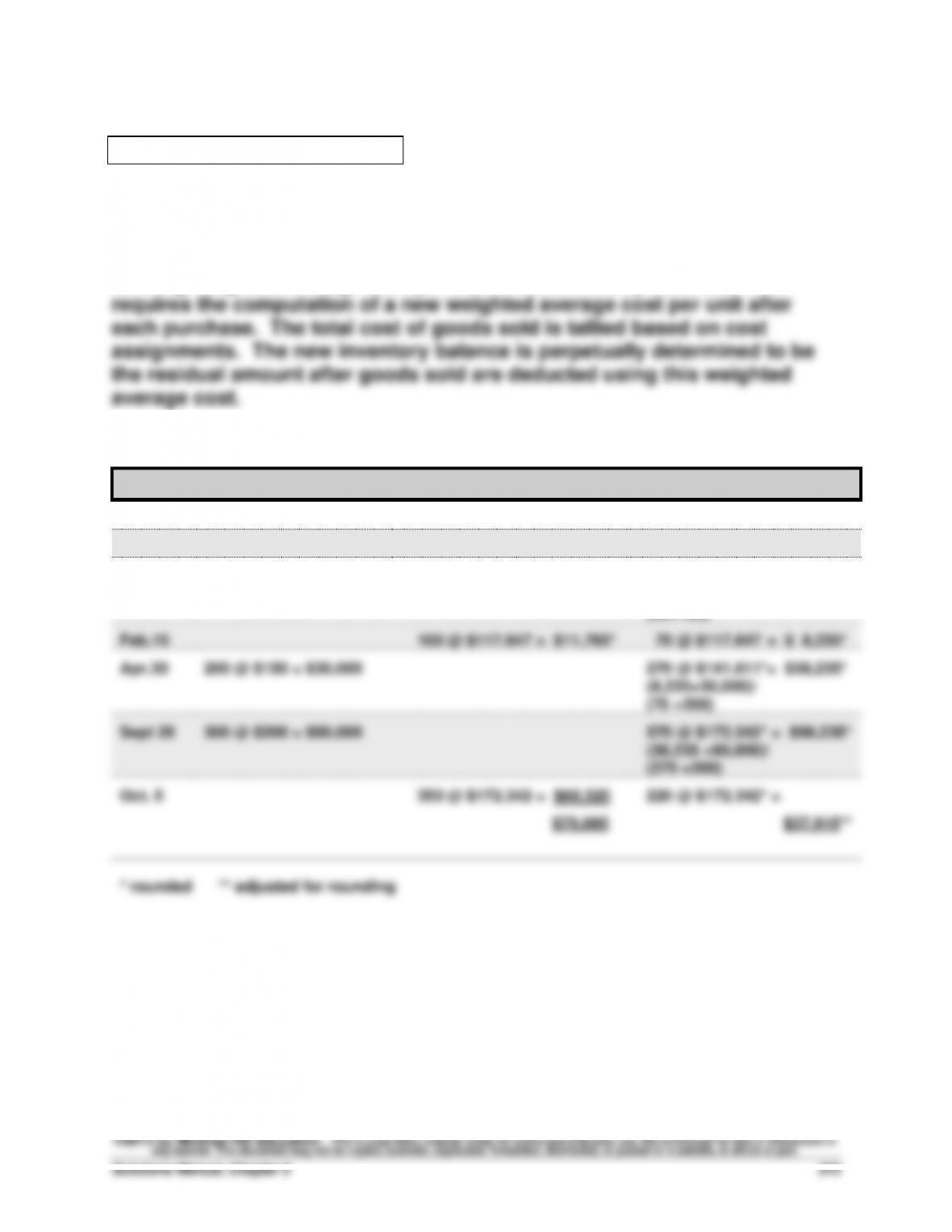

Weighted Average Expert:

(a) and (b) Concept:

Purchases are always recorded at actual costs. The Weighted Average

cost flow assumption requires units sold be assigned a cost based on

running weighted average cost per unit in the inventory balance. This

(a) and (b) Procedures:

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Jan. 1

50 @ $100 = $ 5,000

Jan.10

30 @ $100 = $ 3,000

20 @ $100 = $ 2,000

Jan.14

150 @ $120 = $18,000

170 @ $117.647 = $20,000

(2,000 +18,000)/

(20+150)

Feb.15

100 @ $117.647 = $11,765*

70 @ $117.647 = $ 8,235*

Apr.30

200 @ $150 = $30,000

270 @ $141.611*= $38,235*

(8,235+30,000)/

(70 +200)

Sept 26

300 @ $200 = $60,000

570 @ $172.342* = $98,235*

(38,235 +60,000)/

(270 +300)

Oct. 5

350 @ $172.342 = $60,320

220 @ $172.342* =

$75,085

$37,915**

* rounded ** adjusted for rounding

Financial & Managerial Accounting, 5th Edition

374

Teamwork in Action (Concluded)

(c) Cost Flow versus Actual Physical Flow

Typical comments experts may express in response to (c):

• Physical flow of goods can be affected by the type of products in

inventory and/or the way inventory is stored and/or displayed.

• Actual physical flow of goods is not relevant in selecting an acceptable

method of accounting for inventory. Any one of the four methods is

acceptable. The method chosen should be consistently applied.

More Specific Expert Comments to (c):

Specific Identification—Always reflects the actual cost flow. Electronic

(d) Impact of Methods

Typical comments experts may express in response to (d):

In a period of rising prices LIFO will generally result in the highest cost of

goods sold and therefore the lowest net income and lowest tax. However,

(e) Valuation

Typical comments experts may express in response to (e):

FIFO tends to value ending inventory closest to replacement cost whereas

Entrepreneurial Decision — BTN 5-7

Part 1

(a) Current inventory turnover = $120,000 / $30,000 = 4 times

(b) Proposed inventory turnover = $120,000 / $15,000 = 8 times

Part 2

The owners’ proposal for their company would yield a much improved

inventory turnover of 8 vis-à-vis the current turnover of 4. On the

downside, its days’ sales in inventory would dramatically decline from

future sales could suffer to an extent that would outweigh the benefit of

slashing inventory.

Hitting the Road — BTN 5-8

There is no formal solution for this field activity. The required solution

does allow students to see the relevance of studying merchandise

activities and inventory accounting.

Cost of goods sold

Financial & Managerial Accounting, 5th Edition

376

Global Decision — BTN 5-9

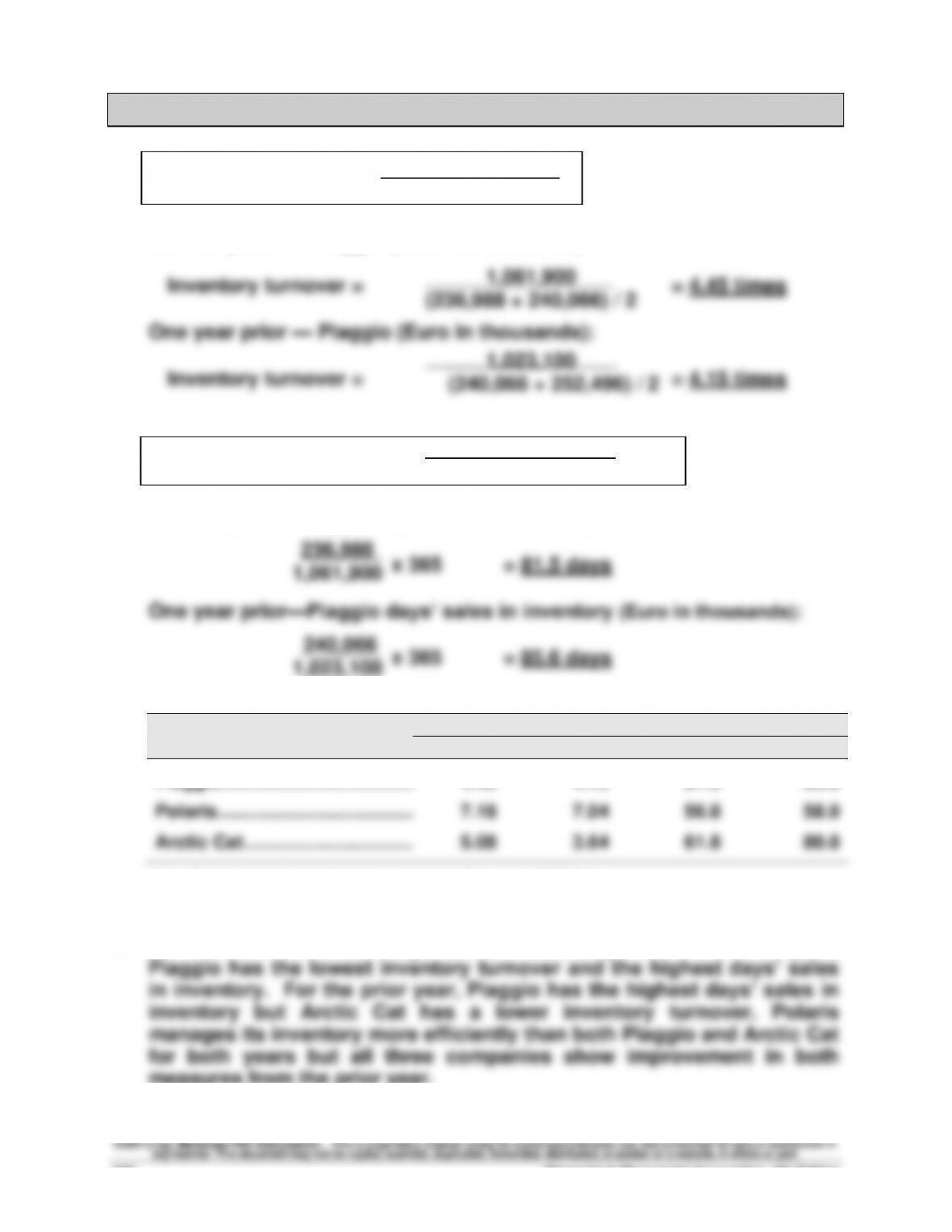

1. Inventory turnover =

Current year — Piaggio (Euro in thousands):

Days’ sales in inventory = x 365

Current year —Piaggio days’ sales in inventory (Euro in thousands):

Inventory Turnover

Days’ Sales in Inventory

Company

Current

Prior Year

Current

Prior Year

Piaggio …………………………….………….

4.45

4.15

81.5

85.6

Polaris …………………………..…………….

7.18

7.04

56.8

58.9

Arctic Cat …………………………..

5.08

3.64

61.8

80.8

Note: Computations for Polaris and Arctic Cat are in BTN 5-2.

2. For the current year and prior years, Polaris has the highest inventory

turnover and the lowest days’ sales in inventory. For the current year,

measures from the prior year.

Cost of sales

Average inventory

(240,066 + 252,496) / 2

Ending Inventory

Costs of Goods Sold

1,023,100