Chapter 05 – Inventories and Cost of Sales

Chapter Outline

Notes

1. Subtract sales (general ledger amount) from goods available

measured at retail price (retail data in supplementary records)

to get ending inventory at retail.

2. Find cost ratio by dividing total of goods available at cost by

total of goods available at retail.

3. Apply cost ratio to ending inventory at retail to convert to

ending inventory at cost.

Note: The cost ratio is also used to convert a physical inventory

taken using retail price to cost. Shrinkage can be measured by

comparing converted to estimated inventory.

B. Gross Profit Method

The gross profit method estimates the cost of ending inventory

by applying the gross profit ratio to net sales (at retail). This type

of estimate is often used for insurance claims when inventory is

destroyed, lost or stolen. Steps include:

1. Determine the normal gross profit percentage from recent

years.

2. Find the cost of goods percentage (100% less gross profit

percentage).

3. Multiply actual sales by the cost of goods sold percentage to

get estimated cost of goods sold.

4. Subtract estimated cost of goods sold from the actual amount

of cost of goods available for sale to get estimated ending

inventory at cost.

Chapter 05 – Inventories and Cost of Sales

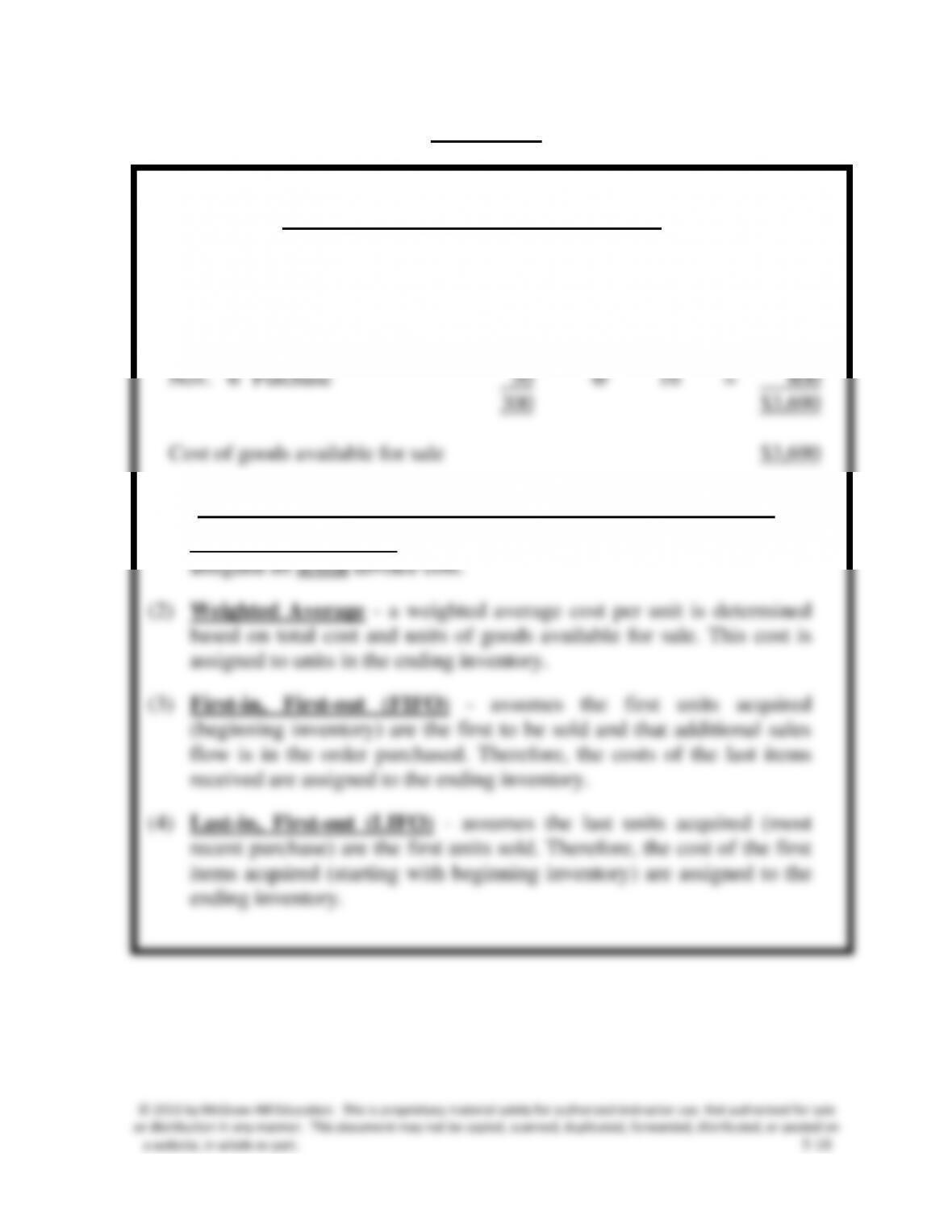

VISUAL #5-1

Schedule of Cost of Goods Available

Units Cost Total

Jan. 1 Beginning Inventory 60 @ $10 = $ 600

Mar. 27 Purchase 90 @ 11 = 990

Aug. 15 Purchase 100 @ 13 = 1,300

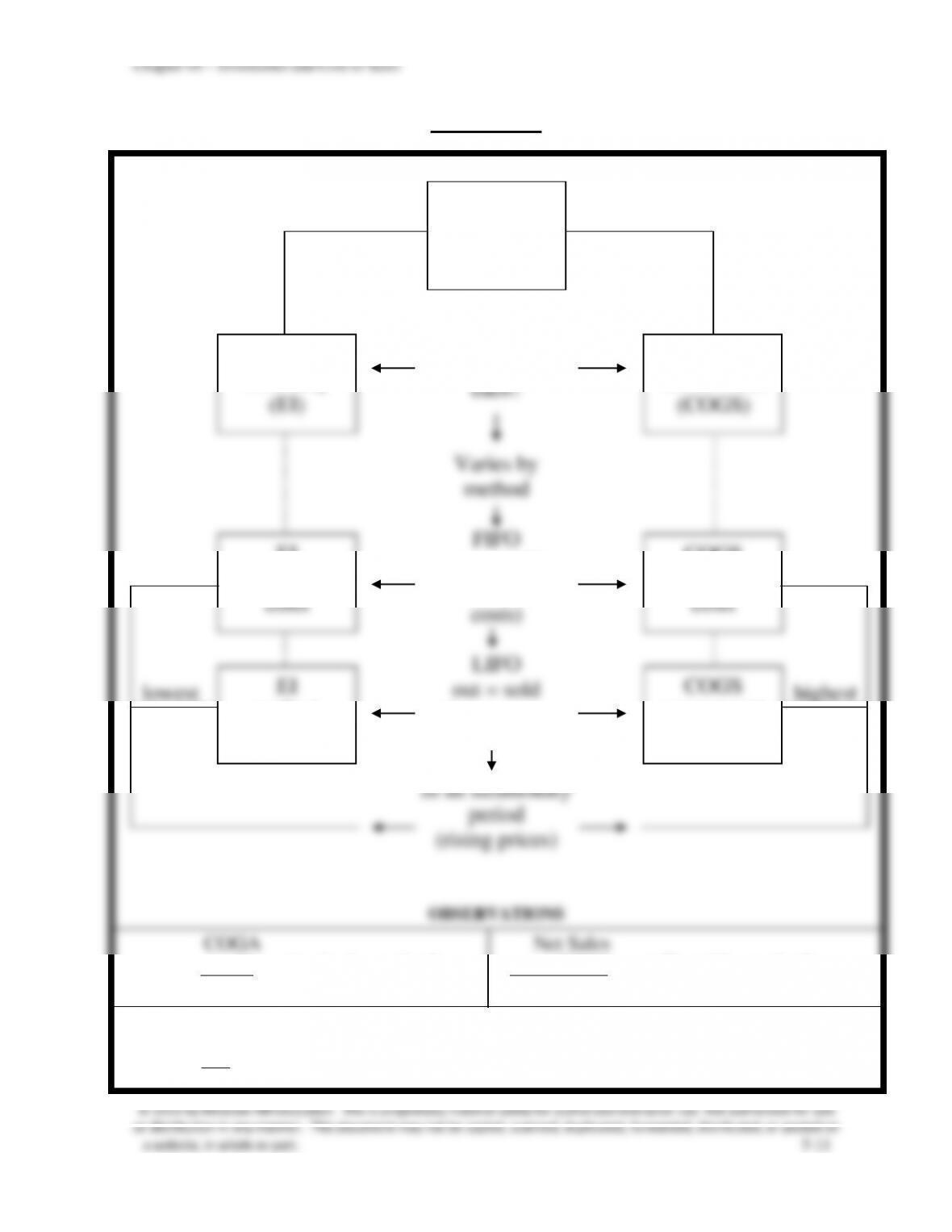

Methods of Assigning Cost to Units in Ending Inventory

(1) Specific Identification – requires that each item in an inventory be

a website, in whole or part. 5-12

Chapter 05 – Inventories and Cost of Sales

a website, in whole or part. 5-13

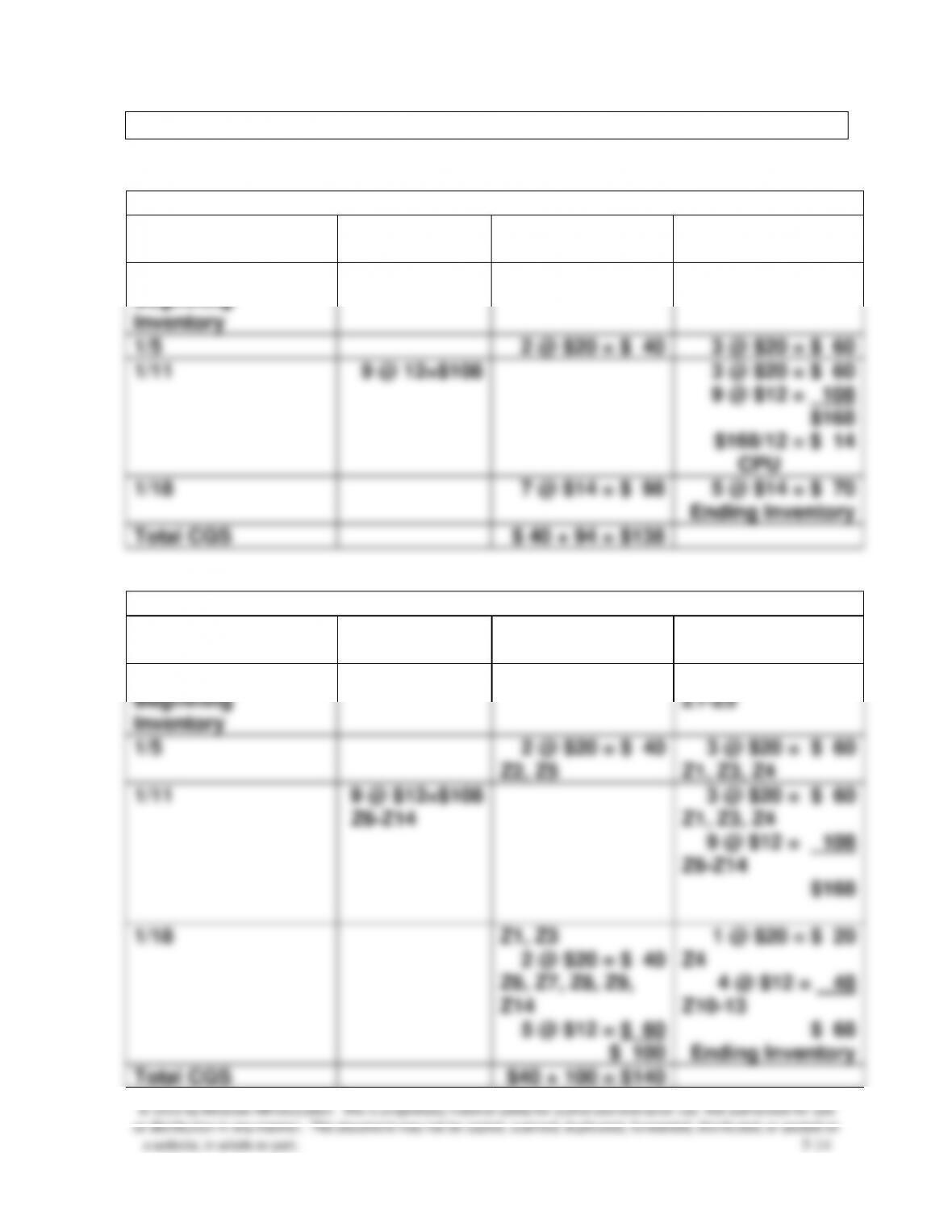

Solution: Chapter 5 – Alternate Demonstration Problem #1

1.

FIFO Perpetual

Date

Purchases

Sales at Cost

Inventory

Balance

1/1

Beginning

Inventory

5 @ $20 = $100

1/5

2 @ $20 = $ 40

3 @ $20 = $ 60

1/11

9 @ 12=$108

3 @ $20 = $ 60

9 @ $12 = 108

$168

1/28

3 @ $20 = $ 60

4 @ $12 = 48

$108

5 @ $12 = $ 60

Ending Inventory

Total CGS

$ 40 + 108 = $148

2.

LIFO Perpetual

Date

Purchases

Sales at Cost

Inventory

Balance

1/1

Beginning

Inventory

5 @ $ 20 = $100

1/5

2 @ $20 = $ 40

3 @ $20 = 60

1/11

9 @ $12=$108

3 @ $20 = $ 60

9 @ $12 = 108

$168

1/18

7 @ $12 = $ 84

3 @ $20 = $ 60

2 @ $12 = 24

$ 84

Ending Inventory

Total CGS

$40 + 84 = $124

Chapter 05 – Inventories and Cost of Sales

Solution: Chapter 5 – Alternate Demonstration Problem #1, continued

3.

Weighted Average Perpetual

Date

Purchases

Sales at Cost

Inventory

Balance

1/1

Beginning

Inventory

5 @ $20 = $100

1/5

2 @ $20 = $ 40

3 @ $20 = $ 60

1/11

9 @ 12=$108

3 @ $20 = $ 60

9 @ $12 = 108

$168

$168/12 = $ 14

CPU

1/18

7 @ $14 = $ 98

5 @ $14 = $ 70

Ending Inventory

Total CGS

$ 40 + 94 = $138

4.

Specific Identification Perpetual

Date

Purchases

Sales at Cost

Inventory

Balance

1/1

Beginning

Inventory

5 @ $ 20 = $100

Z1–Z5

1/5

2 @ $20 = $ 40

Z2, Z5

3 @ $20 = $ 60

Z1, Z3, Z4

1/11

9 @ $12=$108

Z6–Z14

3 @ $20 = $ 60

Z1, Z3, Z4

9 @ $12 = 108

Z6–Z14

$168

1/18

Z1, Z3

2 @ $20 = $ 40

Z6, Z7, Z8, Z9,

Z14

5 @ $12 = $ 60

$ 100

1 @ $20 = $ 20

Z4

4 @ $12 = 48

Z10–13

$ 68

Ending Inventory

Total CGS

$40 + 100 = $140

Chapter 05 – Inventories and Cost of Sales

Chapter 5 – Alternate Demonstration Problem #2

The ABC Company had the following inventory record for the month of

January:

# of

Unit

Date

Description

Items

Price

Item

1/1

Beginning

inventory

5

$20

Z1, Z2, Z3, Z4, Z5

1/5

Sale

2

Z2, Z5

1/11

Purchase

9

12

Z6, Z7, Z8, Z9, Z10, Z11,

Z12, Z13, Z14

1/28

Sale

7

Z1, Z3, Z6, Z7, Z8, Z9, Z14

Required:

Assuming a periodic system is in use, determine the following:

1. Cost of goods available for sale.

2. Cost of goods sold and the ending inventory using each of the

following methods:

a. FIFO

b. LIFO

c. Weighted Average

d. Specific Identification

Chapter 05 – Inventories and Cost of Sales

a website, in whole or part. 5-16

Solution: Chapter 5 – Alternate Demonstration Problem #2

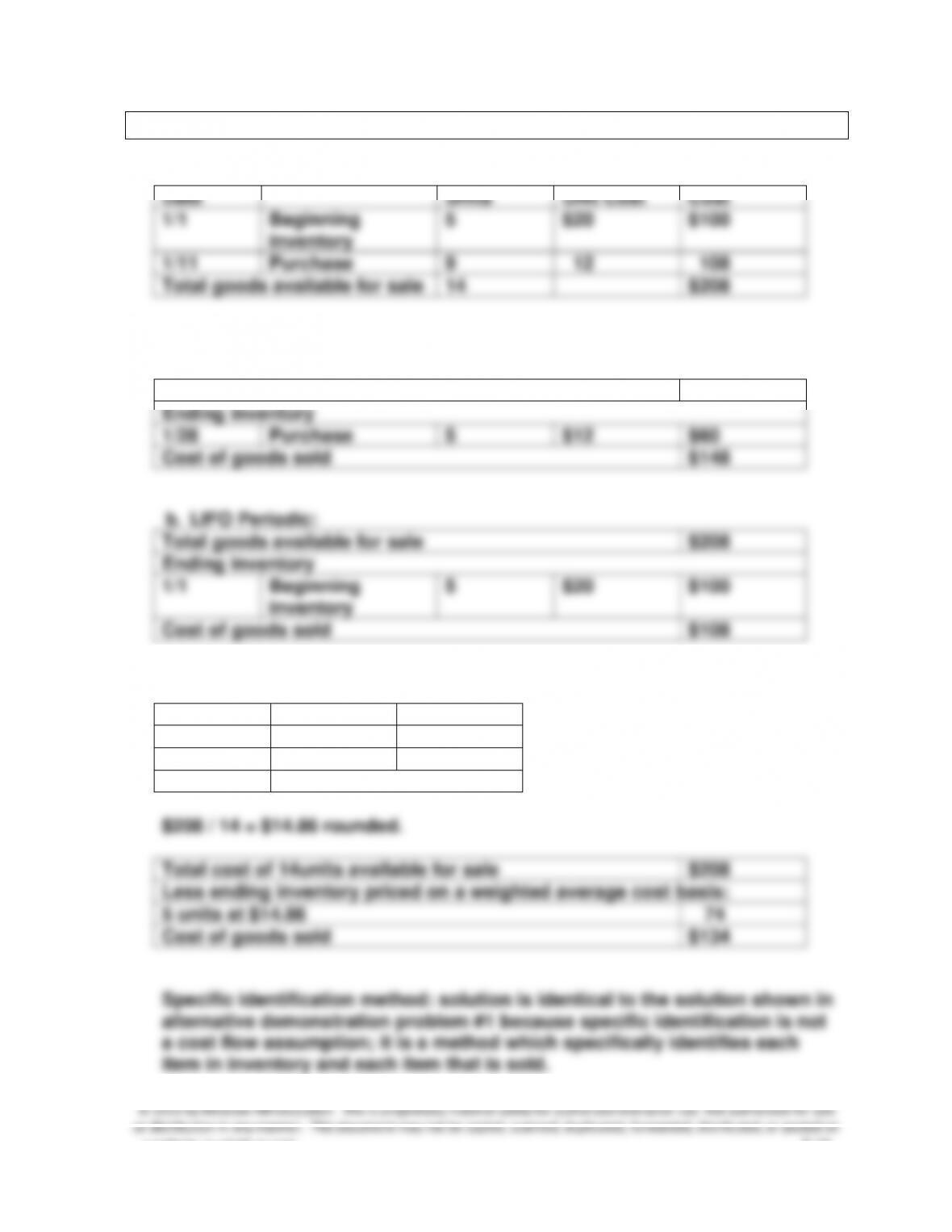

1. Cost of goods available for sale:

Date

Units

Unit Cost

Cost

1/1

Beginning

inventory

5

$20

$100

1/11

Purchase

9

12

108

Total goods available for sale

14

$208

2. a. FIFO Periodic (FIFO under periodic and perpetual yields identical

results).

Total goods available for sale

$208

Ending inventory

1/28

Purchase

5

$12

$60

Cost of goods sold

$148

Total goods available for sale

$208

Ending inventory

1/1

Beginning

inventory

5

$20

$100

Cost of goods sold

$108

c. Weighted Average Periodic:

Units

Unit cost

Total cost

5

$20

$100

9

12

108

14

$208

Total cost of 14units available for sale

$208

Less ending inventory priced on a weighted average cost basis:

5 units at $14.86

74

Cost of goods sold

$134