Financial & Managerial Accounting, 5th Edition

290

Serial Problem — SP 4 (Continued)

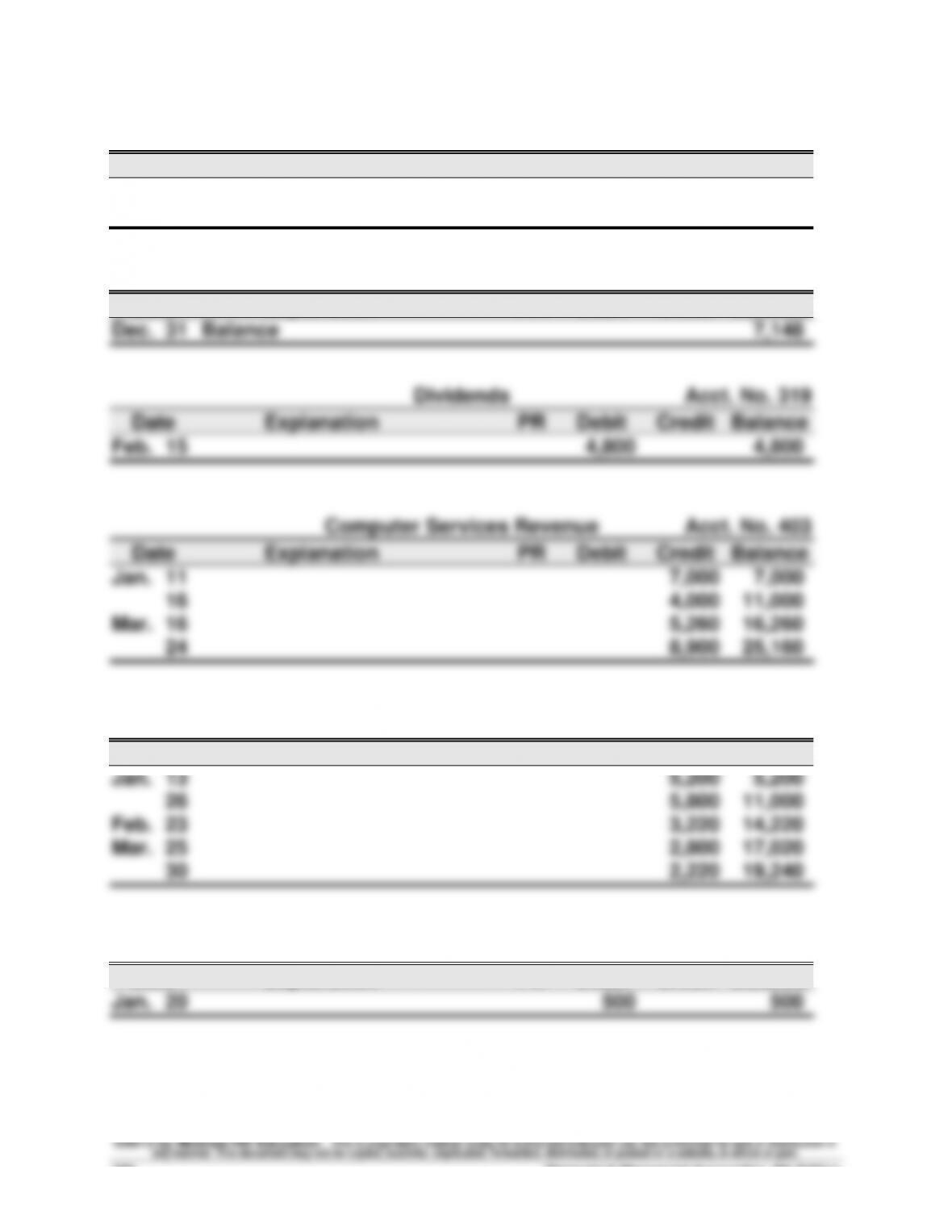

Common Stock Acct. No. 307

Date Explanation PR Debit Credit Balance

Dec. 31 Balance 83,000

Jan. 5 25,000 108,000

Retained Earnings Acct. No. 318

Date Explanation PR Debit Credit Balance

Sales Acct. No. 413

Date Explanation PR Debit Credit Balance

Sales Returns and Allowances Acct. No. 414

Date Explanation PR Debit Credit Balance

Serial Problem — SP 4 (Continued)

Sales Discounts Acct. No. 415

Date Explanation PR Debit Credit Balance

Jan. 22 47 47

Cost of Goods Sold Acct. No. 502

Date Explanation PR Debit Credit Balance

Jan. 13 3,560 3,560

Insurance Expense Acct. No. 637

Date Explanation PR Debit Credit Balance

Rent Expense Acct. No. 640

Date Explanation PR Debit Credit Balance

Financial & Managerial Accounting, 5th Edition

292

Serial Problem — SP 4 (Continued)

Computer Supplies Expense Acct. No. 652

Date Explanation PR Debit Credit Balance

Advertising Expense Acct. No. 655

Date Explanation PR Debit Credit Balance

Feb. 5 600 600

Mileage Expense Acct. No. 676

Date Explanation PR Debit Credit Balance

Feb. 27 192 192

Mar. 31 128 320

Miscellaneous Expenses Acct. No. 677

Date Explanation PR Debit Credit Balance

Repairs Expense—Computer Acct. No. 684

Date Explanation PR Debit Credit Balance

Mar. 11 960 960

Serial Problem — SP 4 (Continued) Part 3

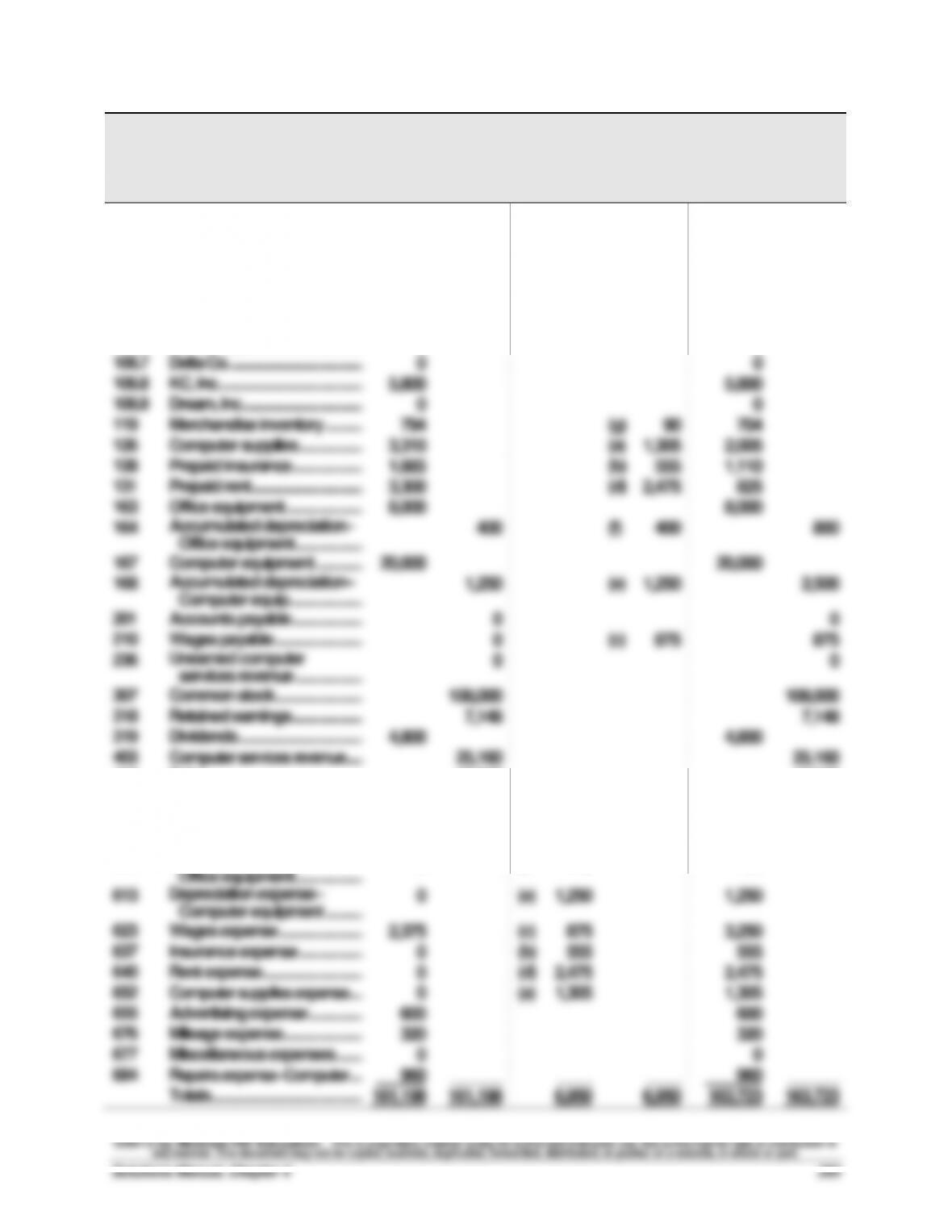

SUCCESS SYSTEMS

Partial Work Sheet

March 31, 2014

Acct.

No.

Account Title

Unadjusted

Trial Balance

Adjustments

Adjusted

Trial Balance

101

Cash………………………………………..…………

77,845

77,845

106.1

Alex’s Engineering Co. ……………………

0

0

106.2

Wildcat Services …………………………..

2,800

2,800

106.3

Easy Leasing …………………………..

8,900

8,900

106.4

IMF Co. ………………………………………………

5,220

5,220

106.5

Liu Corporation ……………………..……

0

0

106.6

Gomez Co. ……………………………..…………

0

0

106.7

Delta Co. ……………………………………………

0

0

106.8

KC, Inc. ………………………………………………

5,800

5,800

106.9

Dream, Inc. ……………………………..…………

0

0

119

Merchandise inventory ………..…………

794

(g)

90

704

126

Computer supplies ……………….…………

3,310

(a)

1,305

2,005

128

Prepaid insurance …………………………..

1,665

(b)

555

1,110

131

Prepaid rent ………………………………………

3,300

(d)

2,475

825

163

Office equipment …………………..………

8,000

8,000

164

Accumulated depreciation–

Office equipment ………………..…………

400

(f)

400

800

167

Computer equipment …………..…………

20,000

20,000

168

Accumulated depreciation–

Computer equip. …………………………..

1,250

(e)

1,250

2,500

201

Accounts payable …………………………..

0

0

210

Wages payable ……………………..……

0

(c)

875

875

236

Unearned computer

services revenue ………………..…………

0

0

307

Common stock ……………………..……

108,000

108,000

318

Retained earnings …………………………..

7,148

7,148

319

Dividends …………………………..…..…………

4,800

4,800

403

Computer services revenue …..…………

25,160

25,160

413

Sales ……………………………………….…………

19,240

19,240

414

Sales returns and allow. ……….…………

500

500

415

Sales discounts …………………….…….

47

47

502

Cost of goods sold ……………….…………

13,962

(g)

90

14,052

612

Depreciation expense–

Office equipment ………………..…………

0

(f)

400

400

613

Depreciation expense–

Computer equipment ………..…………

0

(e)

1,250

1,250

623

Wages expense …………………….…….

2,375

(c)

875

3,250

637

Insurance expense ……………….…………

0

(b)

555

555

640

Rent expense …………………………..

0

(d)

2,475

2,475

652

Computer supplies expense ….…………

0

(a)

1,305

1,305

655

Advertising expense …………….…………

600

600

676

Mileage expense …………………………..

320

320

677

Miscellaneous expenses ……..…………

0

0

684

Repairs expense–Computer ….…………

960

______

____

____

960

______

Totals …………………………………………………

161,198

161,198

6,950

6,950

163,723

163,723

Financial & Managerial Accounting, 5th Edition

294

Serial Problem — SP 4 (Continued)

Part 4

SUCCESS SYSTEMS

Income Statement

For Three Months Ended March 31, 2014

Revenues

Computer services revenue ……………………………….. $25,160

Net sales* ………………………………………………………….. 18,693

Total revenues …………………………………………………… 43,853

Expenses

Cost of goods sold …………………………………………….. $14,052

Part 5

SUCCESS SYSTEMS

Statement of Retained Earnings

For Three Months Ended March 31, 2014

Retained earnings, Dec. 31, 2013………………. $ 7,148

Plus: Net income ……………………………………… 18,686

Serial Problem — SP 4 (Concluded)

Part 6

SUCCESS SYSTEMS

Balance Sheet

March 31, 2014

Assets

Current assets

Cash ………………………………………………………………….. $ 77,845

Accounts receivable* ………………………………………….. 22,720

Merchandise inventory ……………………………………….. 704

Computer supplies ……………………………………………… 2,005

Liabilities

Current liabilities

Wages payable …………………………………………………….. $ 875

Equity

Reporting in Action — BTN 4-1

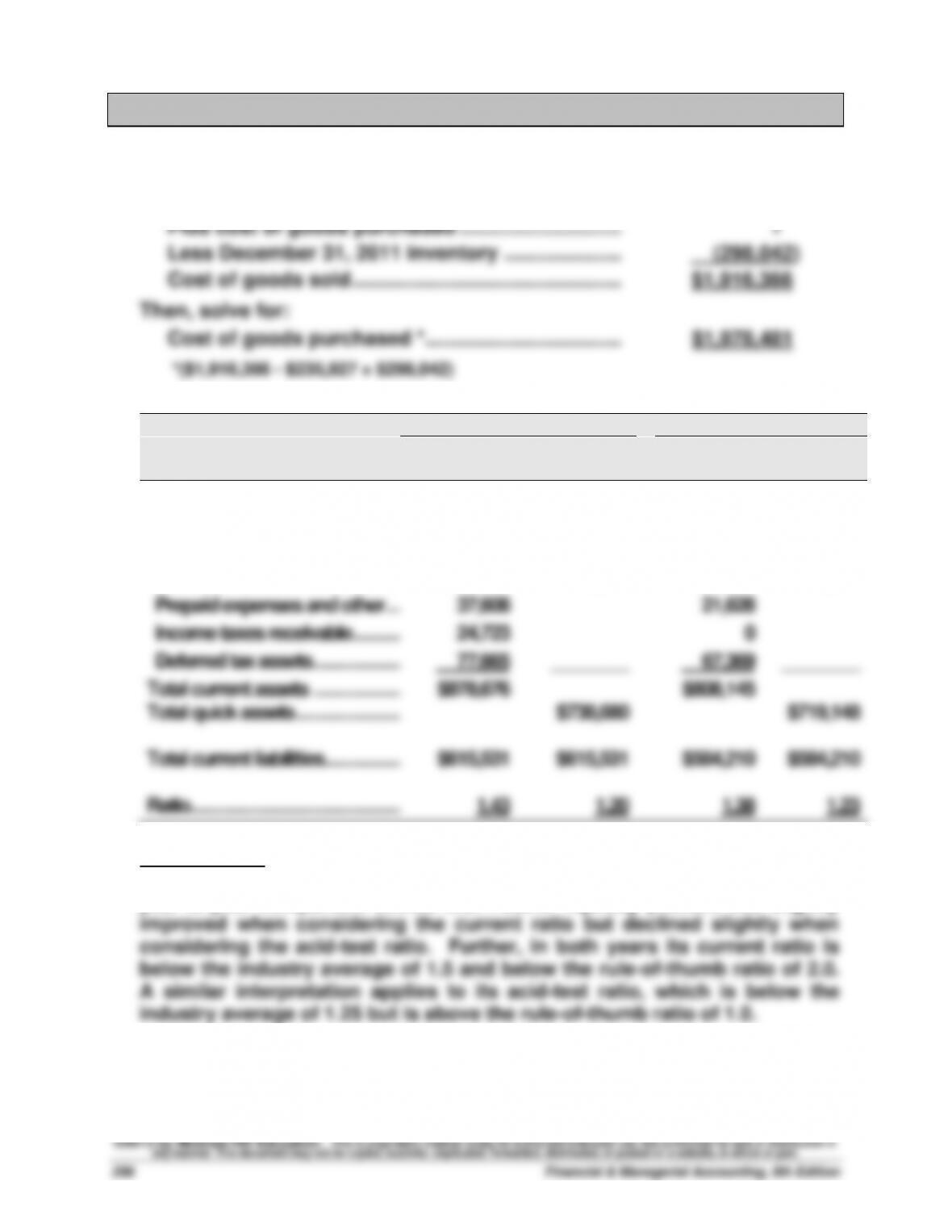

1. Compute cost of sales for 2011 as follows ($ thousands)

December 31, 2010 inventory …………………………. $ 235,927

2.

2011

2010

($ thousands)

Current

Ratio

Acid–Test

Ratio

Current

Ratio

Acid–Test

Ratio

Current assets

Cash and equivalents …………..

$325,336

$325,336

$393,927

$393,927

Trade receivables, net …………..

115,302

115,302

89,294

89,294

Inventories, net …………………...

298,042

298,042

235,927

235,927

Prepaid expenses and other …..

37,608

21,628

Income taxes receivable ………..

24,723

0

Deferred tax assets ……………...

77,665

________

67,369

________

Total current assets ……………...

$878,676

$808,145

Total quick assets ………………...

$738,680

$719,148

Total current liabilities …………....

$615,531

$615,531

$584,210

$584,210

Ratio ………………………………....

1.43

1.20

1.38

1.23

Interpretation: The current ratio increased from 1.38 in 2010 to 1.43 in

2011. The acid-test ratio decreased from 1.23 in 2010 to 1.20 in 2011. The

year–to–year comparison shows that Polaris’ liquidity position has slightly

3. Solution depends on the financial statement data obtained.

Comparative Analysis — BTN 4-2

1.

Polaris

Arctic Cat

($ thousands)

Current

Prior

Current

Prior

Net sales ………………

$2,656,949

$1,991,139

$464,651

$450,728

Cost of sales …………

1,916,366

1,460,926

363,142

367,492

Gross margin ………..

$ 740,583

$ 530,213

$101,509

$ 83,236

Gross margin ratio ….

27.9%

26.6%

21.8%

18.5%

2. In both years, Polaris’ gross margin ratio was higher than that for Arctic

Cat. For both years, Arctic Cat’s gross margin ratio was below the

3. Artic Cat’s gross margin ratio improved from 18.5% to 21.8% and

Ethics Challenge — BTN 4-3

1. A few students sometimes feel that Amy has devised a clever way to

beat the system. She appears to be succeeding in getting something for

free. However, most students fortunately feel that Amy is abusing the

system and that her ethical conduct needs an overhaul. The instructor

may wish to point out that customer abuses such as Amy’s usually

Financial & Managerial Accounting, 5th Edition

298

Ethics Challenge, BTN 4-3 — (Concluded)

2. The merchandising company accounts for sales returns using a contra

revenue account called Sales Returns and Allowances. A dress

returned with a sales bill of $200 would be accounted for as follows:

Communicating in Practice — BTN 4-4

Note: While responses will vary, the essence of its content follows:

TO: Mr. V. Velakturi

FROM:

DATE:

SUBJECT: Reply to inventory shrinkage question

At the end of each accounting period, we take an actual physical inventory

and compare this amount to our inventory records. These accounting

procedures for verifying inventory available have disclosed that the

amount of inventory loss is not abnormally large. Accounting procedures

allow this immaterial shrinkage to be directly charged to cost of goods

more specific information regarding inventory shrinkage, please let me

know. The supporting information is available in the accounting records.

Taking It to the Net — BTN 4-5

Fiscal Year ($ thousands)

2010

2011

2012

Net sales …………………………..

$1,578,042

$1,722,227

$1,854,988

Cost of goods sold …………..…………

882,385

975,230

1,112,481

Gross margin …………………..………

$ 695,657

$ 746,997

$ 742,507

Gross margin ratio …………..…………

44.1%

43.4%

40.0%

Analysis: J. Crew’s gross margin ratio declined from 44.1% in 2010 to

43.4% in 2011 to 40.0% in 2012. Its net sales increased in both 2011 and

2012, albeit with a lower gross margin for both periods.

Financial & Managerial Accounting, 5th Edition

300

Teamwork in Action — BTN 4-6

1.

a. Net sales computation

Sales …………………………..…………………………………….. $600,000

Less: Sales discounts ……………………………………… $ 13,000

Sales returns and allowances …………………. 20,000 33,000

Gross profit ……………………………………………………….. $191,000

Teamwork in Action (Concluded)

e. Net income computation

decrease in both gross profit and net income. This means that net

income would decline to $133,000.

Entrepreneurial Decision — BTN 4-7

1.

Faithful Fish

Forecasted Income Statement

For Year Ended January 31, 2013

Net sales ($1,000,000 x 1.09) ………………………………………. $1,090,000

2. The proposal yields a forecasted net income of $213,100. This compares

3. There are many issues that should be considered. Among them are:

• First, there is the issue of the prediction itself. That is, are estimates

reasonable or could reality be markedly different from these estimates?

• Second, and related to the first, there is a need to consider “ranges” of

before payments are overdue. This may motivate customers to pay

sooner.

In sum, we must consider alternative possibilities, both good and bad,

with these proposed policy changes.

Hitting the Road — BTN 4-8

There is no formal solution for this field activity. As the discussion

facilitator, the instructor should try to develop a sense of how willing retail

managers are in granting sales allowances, the range of return policies

employed, and strategies managers use to stem return abuses.

Global Decision — BTN 4-9

1.

(in thousands)

KTM

Polaris

Arctic Cat

Net sales …………………………..

€526,801

$2,656,949

$464,651

Cost of sales …………………………..

371,752

1,916,366

363,142

Gross margin ……………..……………

€155,049

$ 740,583

$101,509

Gross margin ratio ……..……………….

29.4%

27.9%

21.8%

Gross Margin %

Rank

KTM ……………………………….….

29.4%

1

Polaris ……………………………….

27.9%

2

Arctic Cat ……………………….….

21.8%

3

2. KTM, Polaris, and Arctic Cat each use the multiple-step format for their

income statements. KTM’s income statement is somewhat different from

what most U.S. companies use in that the term net result is used instead

of net income or net earnings and they report in EUR instead of dollars.