Problem 4-2A (Concluded)

Aug. 15 Cash ………………………………………………………….. 4,508

Sales Discounts* ……………………………………….. 92

Accounts Receivable—Laird ……………….. 4,600

Collected receivable within 2% discount period.

*[($5,200 – $600) x 2%]

18 Accounts Payable—Waters ………………………… 4,840

Merchandise Inventory * ……………………… 47

Cash …………………………………………………… 4,793

Financial & Managerial Accounting, 5th Edition

262

Problem 4-3A (60 minutes)

Part 1

Adjustment (a)

Jan 31 Store Supplies Expense …………………………..… 4,050

Store Supplies …………………………………….. 4,050

To record store supplies expense

($5,800 – $1,750).

Adjustment (b)

Problem 4-3A (Continued)

Part 2 Multiple-step income statement

NELSON COMPANY

Income Statement

For Year Ended January 31, 2013

Sales ………………………………………………………………. $111,950

Less: Sales discounts …………………………………….. $ 2,000

Sales returns and allowances ………………… 2,200 4,200

Net sales …………………………………………………………. 107,750

Cost of goods sold* ………………………………………… 40,000

Gross profit …………………………………………………….. 67,750

Financial & Managerial Accounting, 5th Edition

264

Problem 4-3A (Concluded)

Part 3 Single–step income statement

NELSON COMPANY

Income Statement

For Year Ended January 31, 2013

Net sales ………………………………………………………. $107,750

Expenses

Cost of goods sold …………………………………… $40,000

Part 4

Current assets

Cash …………………………………………………………………..

$ 1,000

Merchandise inventory ………………………………………..

10,900

Store supplies …………………………………………………….

1,750

Prepaid insurance ……………………………………………….

1,000*

Total current assets …………………………………………….

$ 14,650

Current liabilities …………………………………………………...

$ 10,000

Current ratio ($14,650 / $10,000) ………………………………….

1.47

*$2,400 – $1,400 = $1,000

Quick assets (Cash) ……………………………………………….

$ 1,000

Current liabilities …………………………………………………...

$ 10,000

Acid-test ratio ($1,000 / $10,000) ………………………………...

0.10

Net Sales ……………………………………………………………….

$107,750

Cost of Goods Sold ………………………………………………..

40,000

Gross margin ………………………………………………………...

$ 67,750

Gross margin ratio ($67,750 / $107,750) ……………………….

0.63

Problem 4-4A (40 minutes)

1. Net sales

Sales …………………………..………………………………………...

$225,600

Less: Sales discounts…………………………………………..

(2,250)

Sales returns and allowances ……………………..

(12,000)

Net sales ……………………………………………………………….

$211,350

2. Cost of Merchandise purchased

Invoice cost of merchandise purchased ………………...

$ 92,000

Purchase discounts received ………………………………...

(2,000)

Purchase returns and allowances …………………………..

(4,500)

Costs of transportation–in ……………………………………...

4,600

Total cost of merchandise purchased …………………….

$ 90,100

Financial & Managerial Accounting, 5th Edition

266

Problem 4-4A (Continued)

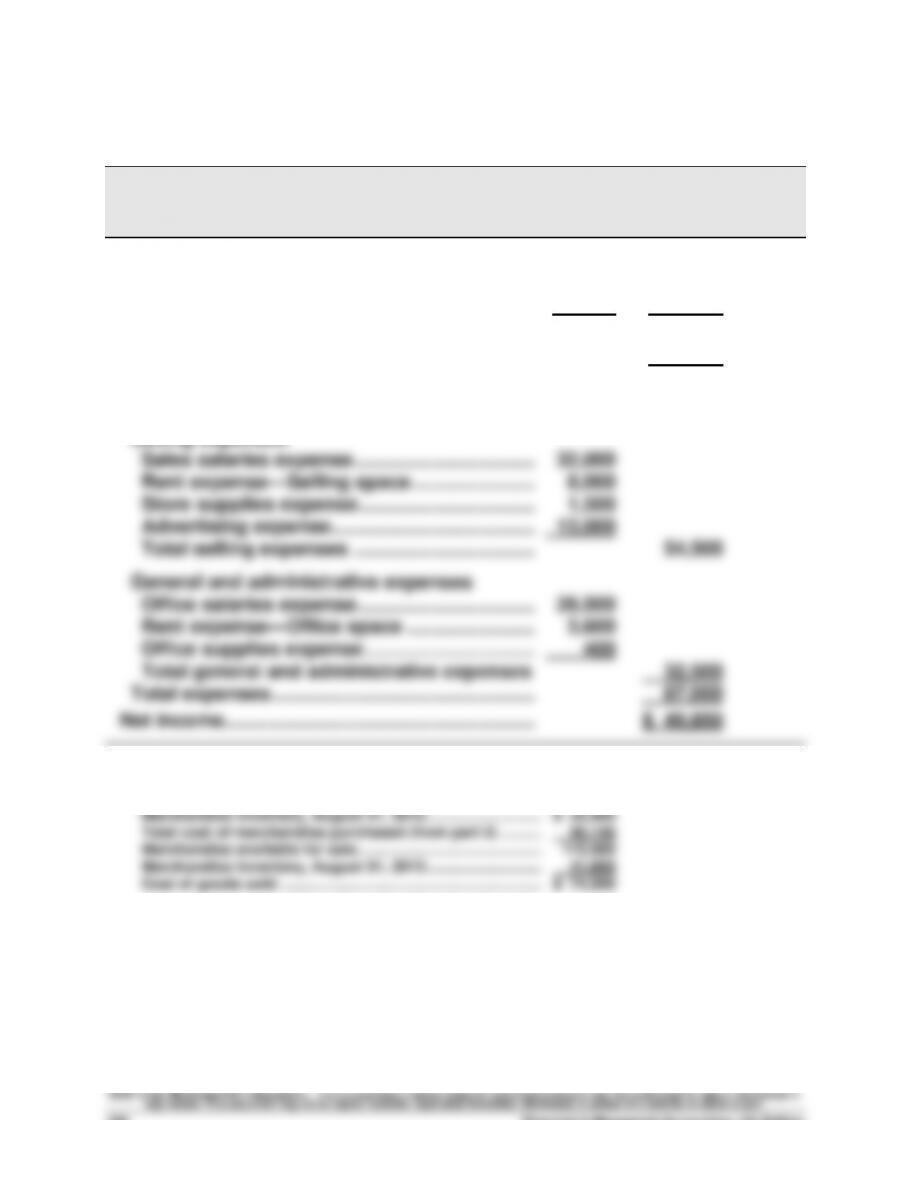

3. Multiple-step income statement

VALLEY COMPANY

Income Statement

For Year Ended August 31, 2013

Sales ………………………………………………………….. $225,600

Less: Sales discounts ………………………………… $ 2,250

Sales returns and allowances …………… 12,000 14,250

Net sales ……………………………………………………. 211,350

Cost of goods sold * …………………………………… 74,500

Gross profit ……………………………………………….. 136,850

Expenses

Selling expenses

*Cost of goods sold (alternative computation):

Problem 4-4A (Concluded)

4. Single-step income statement

VALLEY COMPANY

Income Statement

For Year Ended August 31, 2013

Net sales ………………………………………………………… $211,350

Expenses

Cost of goods sold ……………………………………….. $74,500

Financial & Managerial Accounting, 5th Edition

268

Problem 4-5A (30 minutes)

Part 1

Closing entries

Aug. 31 Sales ……………………………………………………. 225,600

Income Summary ……………………………. 225,600

To close temporary accounts with

credit balances.

Aug. 31 Income Summary ………………………………….. 175,750

Sales Discounts …………………………….. 2,250

Sales Returns and Allowances ……….. 12,000

Cost of Goods Sold ………………………… 74,500

Sales Salaries Expense …………………… 32,000

Problem 4-5A (Concluded)

Part 2

The first step is to determine the amount of purchases that are subject to a

discount during the year:

Invoice cost of merchandise purchases ………..

$92,000

Purchase returns and allowances ………………….

(4,500)

Total cost of merchandise payable ………………..

$87,500

This amount is used to determine the maximum discount, which is then

compared to the actual discount:

Maximum discount available (3% x $87,500) ….

$ 2,625

Purchase discounts received ………………………..

(2,000)

Purchase discounts missed ………………………….

$ 625

As a percent of available discounts ($625/$2,625) …………….. 23.8%

This analysis suggests that nearly 24% of available discounts have been

missed. As a result, it would appear that cash is not being well managed.

Management should try to identify a better system for ensuring that all

favorable discounts are taken. It is possible that the 24% of discounts not

taken are actually at rates not favorable to the company (meaning that

management is worse off expending resources on those discounts)—

further information is required to assess this possibility.

Part 3

The first step is to compute this year’s sales returns and allowances rate:

Sales …………………………………………………………….

$225,600

Sales returns and allowances ……………………….

$ 12,000

Percent of returns and allowances to sales ……

5.3%

This calculation shows that the company’s customers are returning or

requiring allowances on items at a higher rate than the 4% rate observed in

prior years. It appears that management should investigate the situation to

see why there are more dissatisfied customers this year than in prior years.

Problem 4-6AB (50 minutes)

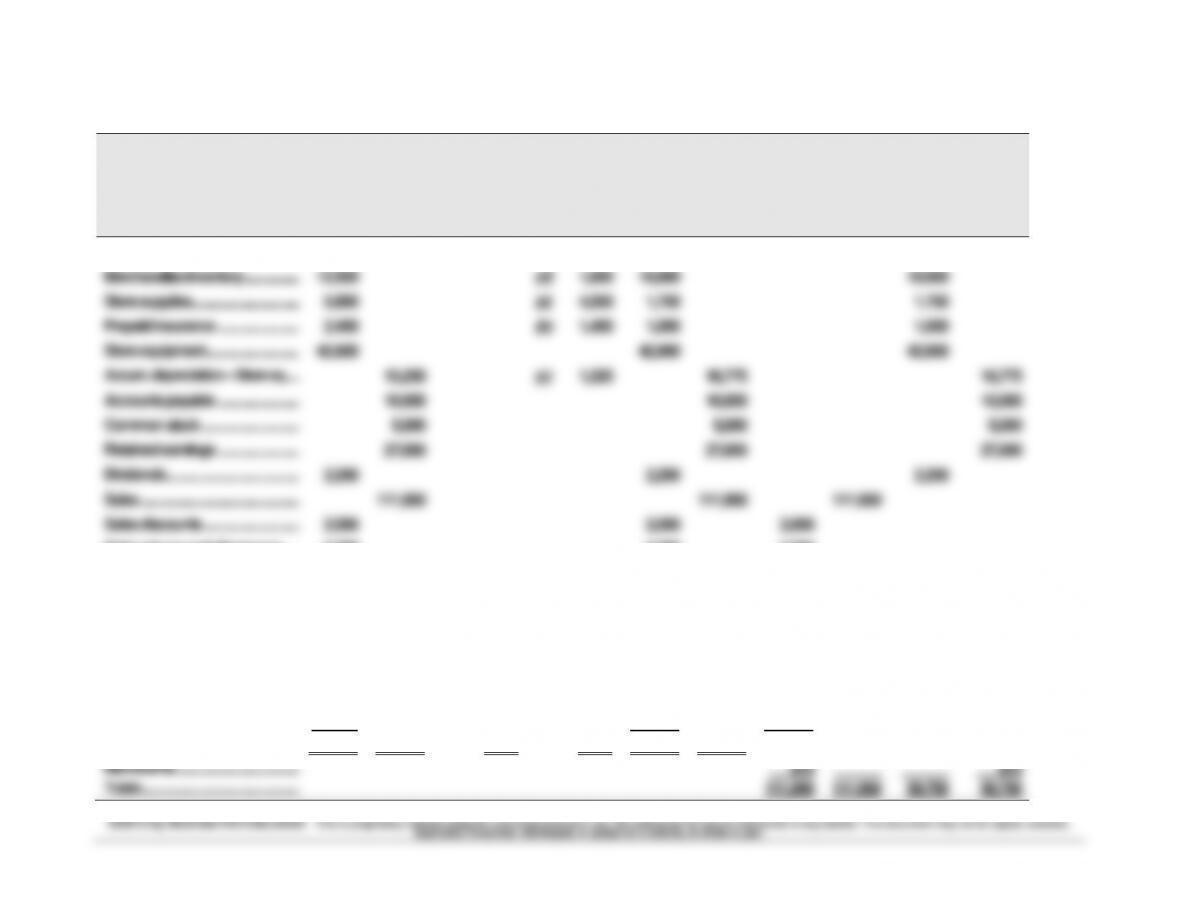

NELSON COMPANY

Work Sheet

For Year Ended January 31, 2013

Unadjusted

Trial Balance

Adjustments

Adjusted

Trial Balance

Income

Statement

Balance Sheet

Account Title

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Cash ………………………………………………………

1,000

1,000

1,000

Merchandise inventory ……………….……

12,500

(d)

1,600

10,900

10,900

Store supplies …………………………..…………

5,800

(a)

4,050

1,750

1,750

Prepaid insurance ………………………..…

2,400

(b)

1,400

1,000

1,000

Store equipment …………………………………

42,900

42,900

42,900

Accum. depreciation—Store eq ………….

15,250

(c)

1,525

16,775

16,775

Accounts payable ………………………..…

10,000

10,000

10,000

Common stock ……………………………..……

5,000

5,000

5,000

Retained earnings ………………………..…

27,000

27,000

27,000

Dividends………………………………………..……

2,200

2,200

2,200

Sales …………………………..…………………………

111,950

111,950

111,950

Sales discounts …………………………....……

2,000

2,000

2,000

Sales returns and allowances …………

2,200

2,200

2,200

Cost of goods sold ……………………….….

38,400

(d)

1,600

40,000

40,000

Depreciation expense—Store eq ……….

0

(c)

1,525

1,525

1,525

Salaries expense …………………………..

35,000

35,000

35,000

Insurance expense ……………………….….

0

(b)

1,400

1,400

1,400

Rent expense …………………………..…….……

15,000

15,000

15,000

Store supplies expense ……………………

0

(a)

4,050

4,050

4,050

Advertising expense …………………………

9,800

______

____

____

9,800

______

9,800

______

______

______

Totals ……………………………………………….……

169,200

169,200

8,575

8,575

170,725

170,725

110,975

111,950

59,750

58,775

Net income …………………………..………………

975

______

______

975

Totals ……………………………………………….……

111,950

111,950

59,750

59,750

PROBLEM SET B

Problem 4-1B (40 minutes)

May 2 Merchandise Inventory ………………………………. 10,000

Accounts Payable—Havel ……………………. 10,000

Purchased goods on credit, terms 1/15, n/30.

4 Accounts Receivable—Heather ………………….. 11,000

Sales …………………………………………………… 11,000

Sold goods on credit, terms 2/10, n/60.

4 Cost of Goods Sold ……………………………………. 5,600

Financial & Managerial Accounting, 5th Edition

272

Problem 4-1B (Concluded)

May 17 Accounts Payable—Havel …………………………. 10,000

Merchandise Inventory * ……………………… 100

Cash …………………………………………………… 9,900

Paid payable in discount period (*10,000 x 1%).

20 Accounts Receivable—Tameron ……………….. 2,800

Sales …………………………………………………… 2,800

Sold goods on credit, terms 2/15, n/60.

Problem 4-2B (40 minutes)

July 3 Merchandise Inventory ……………………………… 15,000

Accounts Payable—OLB …………………….. 15,000

Purchased goods on credit, terms 1/10, n/30.

4 Accounts Payable—OLB …………………………... 150

Cash ………………………………………………….. 150

Paid freight for OLB Corp.

Financial & Managerial Accounting, 5th Edition

274

Problem 4-2B (Concluded)

July 17 Cash …………………………………………………………. 9,457

Sales Discounts* ………………………………………. 193

Accounts Receivable—Brill ………………… 9,650

Collected receivable within discount period.

*($11,500 – $1,850) x 2%

20 Accounts Payable—Rupert* ………………………. 12,700

Problem 4-3B (60 Minutes)

Part 1

Adjustment (a)

Oct. 31 Store Supplies Expense …………………………….. 6,000

Store Supplies …………………………………….. 6,000

To record store supplies expense

($9,700 – $3,700).

Adjustment (b)