Financial & Managerial Accounting, 5th Edition

246

Exercise 4-7 (25 minutes)

1. Entries for Sydney Company (BUYER):

May 11 Merchandise Inventory ……………………………. 40,000

Accounts Payable ……………………………… 40,000

Purchased merchandise on credit.

11 Merchandise Inventory ……………………………. 345

2. Entries for Troy Corporation (SELLER):

May 11 Accounts Receivable ……………………………….. 40,000

Sales …………………………………………………. 40,000

Sold merchandise on account.

11 Cost of Goods Sold ………………………………….. 30,000

Exercise 4-8 (30 minutes)

Merchandise Inventory

Balance, Dec. 31, 2012 …………..

25,000

Purchase discounts received ……..……………………

1,700

Invoice cost of purchases ……..

192,500

Purchase returns and allow. ……….………………….

4,000

Returns by customers …………..

2,100

Cost of sales transactions ………….……………….

196,000

Transportation–in ………………….

2,900

Shrinkage ………………………………….……………………

800

Balance, Dec. 31, 2013

20,000

Cost of Goods Sold

Cost of sales transactions……..

Inventory shrinkage

recorded in December 31,

2013, adjusting entry …………..

196,000

800

Returns by customers and

restored to inventory ……………….………….

2,100

Balance, Dec. 31, 2013

194,700

Exercise 4-9 (25 minutes)

Adjusting entries

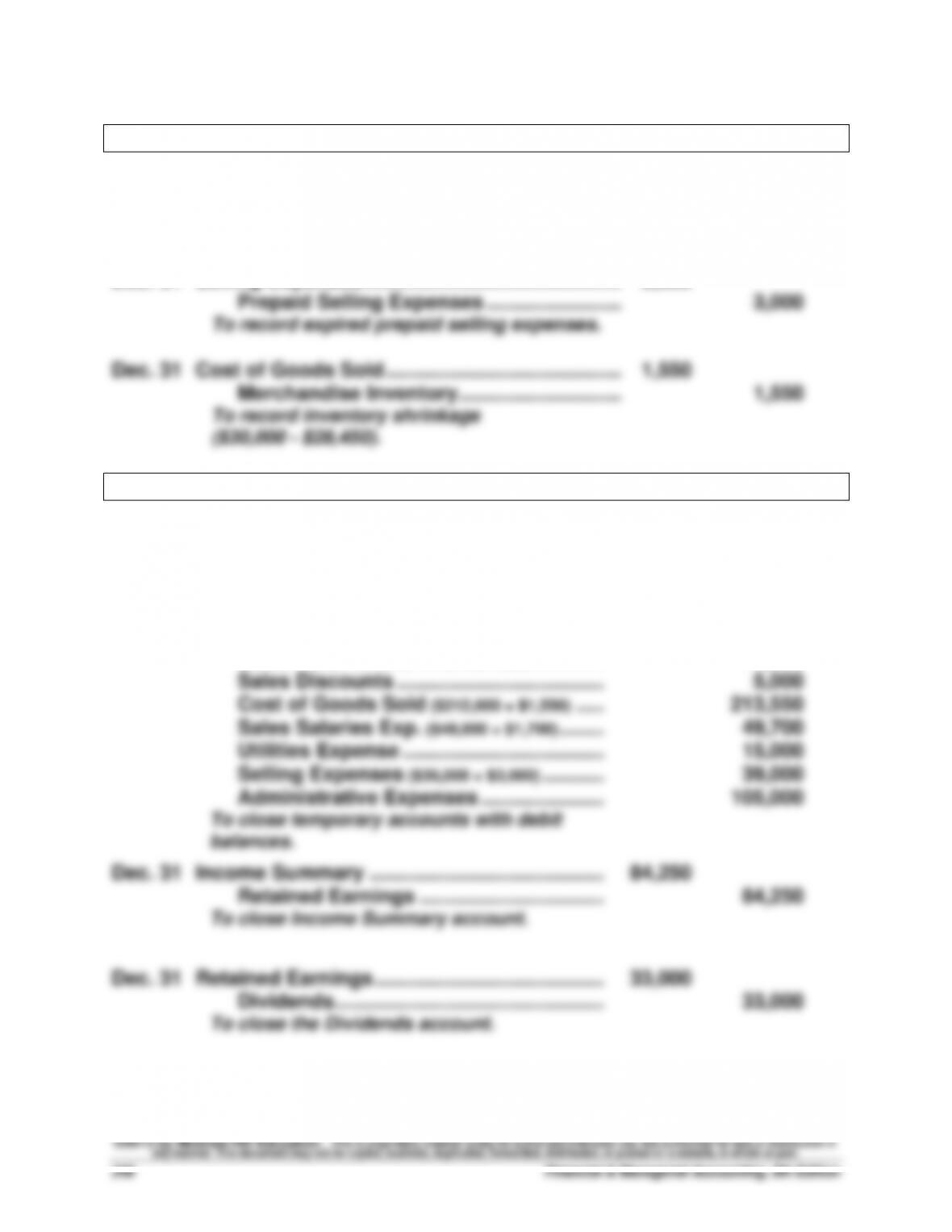

Dec. 31 Sales Salaries Expense …………………………….. 1,700

Salaries Payable…………………………………. 1,700

To record accrued salaries.

Dec. 31 Selling Expenses ………………………………………. 3,000

Closing entries

Dec. 31 Sales …………………………………………………….. 529,000

Income Summary …………………………….. 529,000

To close temporary accounts with

credit balances.

Dec. 31 Income Summary …………………………………… 444,750

Sales Returns and Allowances …………. 17,500

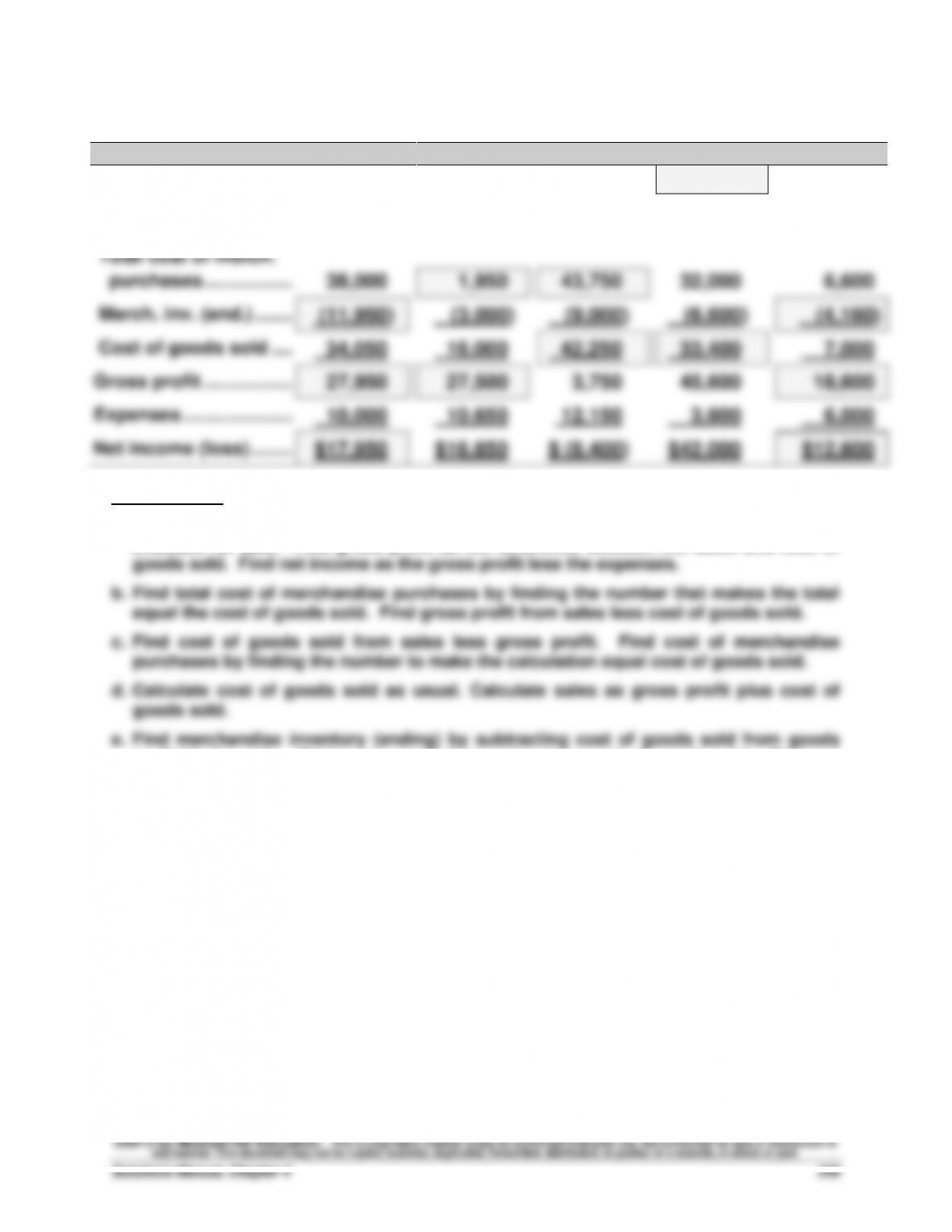

Exercise 4-10 (30 minutes)

Note: The original missing numbers are blocked.

(a)

(b)

(c)

(d)

(e)

Sales ……………………….

$62,000

$43,500

$46,000

$79,000

$25,600

Cost of goods sold

Merch. inv. (beg.) …….

8,000

17,050

7,500

8,000

4,560

Total cost of merch.

purchases ……………..

38,000

1,950

43,750

32,000

6,600

Merch. inv. (end.) …….

(11,950)

(3,000)

(9,000)

(6,600)

(4,160)

Cost of goods sold ….

34,050

16,000

42,250

33,400

7,000

Gross profit ……………..

27,950

27,500

3,750

45,600

18,600

Expenses …………………

10,000

10,650

12,150

3,600

6,000

Net income (loss) ……..

$17,950

$16,850

$ (8,400)

$42,000

$12,600

Explanations:

a. Find merchandise inventory (ending) by subtracting cost of goods sold from goods

available for sale. Find gross profit as the difference between the sales and cost of

available for sale. Find gross profit from sales less cost of goods sold. Find net

income as gross profit less expenses.

Exercise 4-11 (20 minutes)

The employee’s oversight in omitting these goods from the physical count

would cause the cost of the physical count of ending inventory to be

As a result of this error:

• Return on assets would be understated (numerator impact outweighs

the denominator impact).

Exercise 4-12 (20 minutes)

See the solution explanation in Exercise 4-11. As a result of this error:

Exercise 4-13 (15 minutes)

Case X

Case Y

Case Z

Current ratio computation

Current assets ……………………

$5,200

$3,500

$7,300

Current liabilities ………………..

$2,200

$1,200

$3,750

Current ratio ……………………….

2.36

2.92

1.95

Acid-test ratio computation

Cash …………………………………..

$2,000

$ 110

$1,000

Short-term investments ………

0

0

600

Current receivables …………….

350

590

700

Quick assets ………………………

$2,350

$ 700

$2,300

Current liabilities ………………..

$2,200

$1,200

$3,750

Acid-test ratio …………………….

1.07

0.58

0.61

Interpretation:

Case X has the highest acid-test ratio and a healthy current ratio. Since Case

X has enough current assets to cover its current liabilities by more than two

times and enough liquid assets to cover its current liabilities by more than one

time, Case X appears to be in the best position to meet its short-term

obligations.

Specifically, Case Y exhibits the superior ability to meet current year

obligations using the current ratio and Case X has the superior ability to meet

Financial & Managerial Accounting, 5th Edition

252

Exercise 4-14 (20 minutes)

Perpetual

1)

Nov. 1 Merchandise Inventory ………………………………. 1,500

Accounts Payable ……………………………….. 1,500

To record merchandise purchases on credit.

2)

Nov. 5 Accounts Payable ……………………………………… 1,500

Merchandise Inventory ………………………… 30

Instructor note: This second entry changes if the goods returned are defective. In this

case the returned inventory is recorded at its estimated value, not its cost. To illustrate, if

the goods (costing $130) returned are defective and estimated to be worth, say, $50, the

following entry is made: Dr. Merchandise Inventory for $50, Dr. Loss from Defective

Merchandise for $80, and Cr. Cost of Goods Sold for $130.

Exercise 4-15 (10 minutes)

Multiple-Step Income Statement — Sales Related Information Only

Sales (gross) ……………………………………………………… $200,000

Exercise 4-16A (30 minutes)

Apr. 2 Purchases …………………………………………………. 4,600

Accounts Payable—Lyon …………………….. 4,600

Purchased merchandise on credit.

3 Transportation–In ……………………………………….. 300

Cash …………………………………………………… 300

Paid shipping charges on purchased

Financial & Managerial Accounting, 5th Edition

254

Exercise 4-17A (30 minutes)

1. BUYER – Santa Fe Company

Credit Purchase

Purchases ………………………………………………… 24,000

Accounts Payable ………………………………. 24,000

Purchased merchandise on credit.

2. SELLER – Mesa Company

Credit Sale

Accounts Receivable ………………………………… 24,000

Sales ………………………………………………….. 24,000

Sold merchandise on account.

Exercise 4-18A (25 minutes)

1. Entries for Sydney Company (BUYER):

May 11 Purchases ……………………………………………….. 40,000

Accounts Payable ……………………………… 40,000

Purchased merchandise on credit.

11 Transportation–In ……………………………………… 345

2. Entries for Troy Corporation (SELLER):

May 11 Accounts Receivable ……………………………….. 40,000

Sales …………………………………………………. 40,000

Sold merchandise on account.

Financial & Managerial Accounting, 5th Edition

256

Exercise 4-19A (20 minutes)

Periodic Inventory System

1)

Nov. 1 Purchases …………………………………………………. 1,500

Accounts Payable ……………………………….. 1,500

To record purchases on credit.

2)

Nov. 5 Accounts Payable ……………………………………… 1,500

Purchases Discount* …………………………... 30

6)

Nov. 16 Sales Returns and Allowances …………………… 300

Accounts Receivable …………………………... 300

To record return of merchandise sold on credit.

Exercise 4-20 (20 minutes)

L´Oréal

Income Statement (€ millions)

For Year Ended December 31, 2011

Net sales ……………………………………………………………………….. €20,343.1

Cost of sales ………………………………………………………………….. 5,851.5

Gross profit…………………………..…………………………………… 14,491.6

Financial & Managerial Accounting, 5th Edition

258

PROBLEM SET A

Problem 4-1A (40 minutes)

July 1 Merchandise Inventory ………………………………. 6,000

Accounts Payable—Boden ………………….. 6,000

Purchased goods on credit, terms 1/15, n/30.

2 Accounts Receivable—Creek……………………… 900

Sales …………………………………………………… 900

Sold goods on credit, terms 2/10, n/60.

2 Cost of Goods Sold ……………………………………. 500

Accounts Receivable—Creek ………………. 900

Collected receivable within the discount period.

Problem 4-1A (Concluded)

July 16 Accounts Payable—Boden …………………………. 6,000

Merchandise Inventory (1%) ………………… 60

Cash …………………………………………………… 5,940

Paid payable within discount period.

19 Accounts Receivable—Art …………………………. 1,200

Sales …………………………………………………… 1,200

Sold goods on credit, terms 2/15, n/60.

19 Cost of Goods Sold ……………………………………. 800

Financial & Managerial Accounting, 5th Edition

260

Problem 4-2A (40 minutes)

Aug. 1 Merchandise Inventory ………………………………. 7,500

Accounts Payable—Arotek ………………….. 7,500

Purchased goods on credit, terms 1/10, n/30.

4 Accounts Payable—Arotek ………………………… 200

Cash …………………………………………………… 200

Paid freight for Arotek.

5 Accounts Receivable—Laird ………………………. 5,200

Sales …………………………………………………… 5,200

Received a credit memorandum for August 8

purchase.