Chapter 04 Accounting for Merchandising Operations

Chapter 04

Accounting for Merchandising Operations

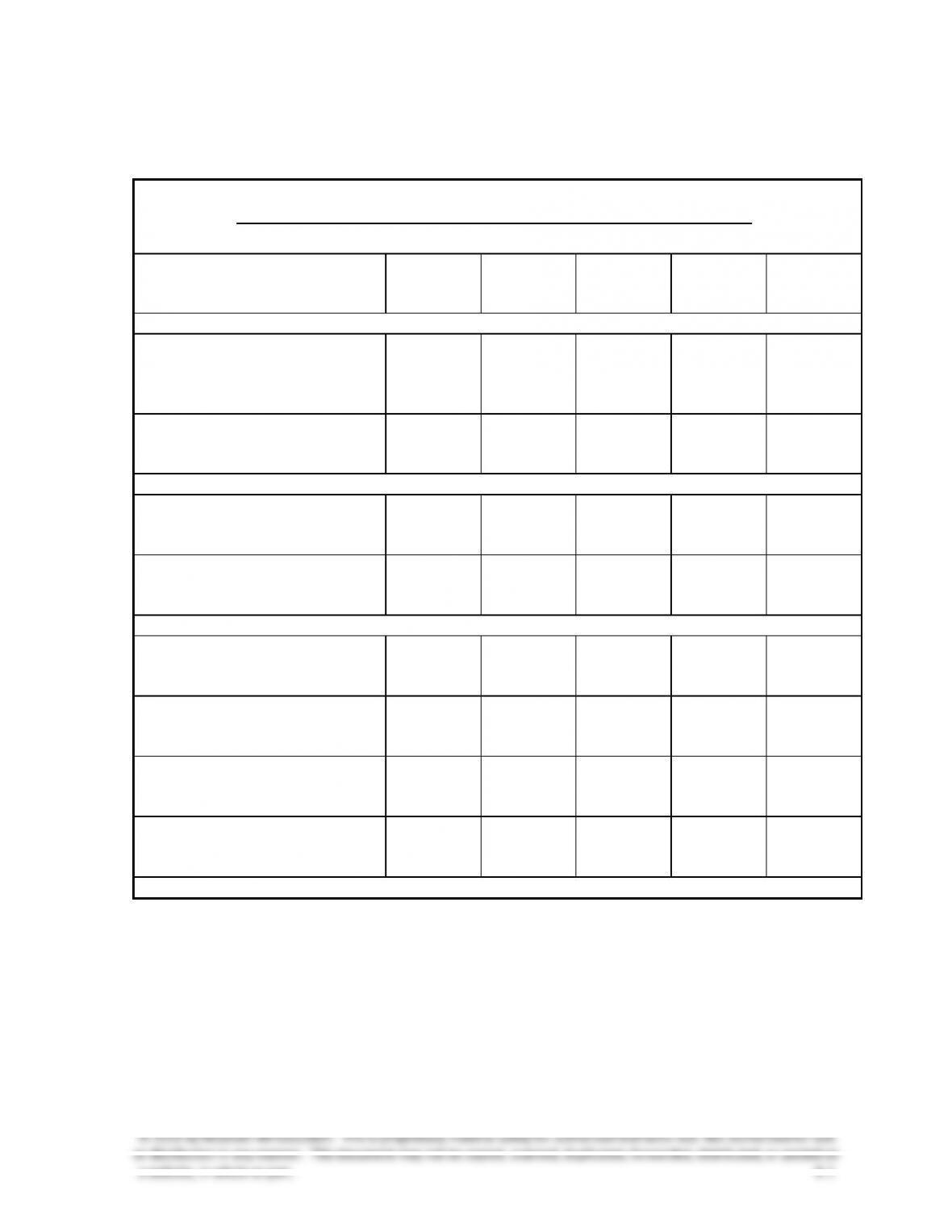

Student Learning Objectives and Related Assignment Materials*

Student Learning Objectives

Discussion

Questions

Quick

Studies

Exercises

Problems

(A &B set)**

Beyond the

Numbers

Conceptual objectives:

C1. Describe merchandising

activities and identify income

components for a

merchandising company.

1, 2, 3

4-1, 4-15

4-6, 4-10

EC, TTN,

TIA, ED,

HTR

C2. Identify and explain the

inventory asset and cost flows

of a merchandising company.

1, 2

4-2, 4-18

4-1, 4-3,

4-10

4-4, 4-5

CIP, TIA,

ED

Analytical objectives:

A1. Compute the acid-test ratio

and explain its use to assess

liquidity.

4-8, 4-9

4-11, 4-13

4-3

RIA

A2. Compute the gross margin ratio

and explain its use to assess

profitability.

14

4-5

4-12

4-3

CA, TTN,

GD

Procedural objectives:

P1. Analyze and record transactions

for merchandise purchases

using a perpetual system.

6, 7, 9

4-3, 4-16,

4-17

4-2, 4-3, 4-5,

4-7, 4-8,

4-14

4-1, 4-2

P2. Analyze and record transactions

for merchandise sales using

a perpetual system.

4, 6, 7, 8, 9,

15

4-4

4-3, 4-4, 4-7,

4-8, 4-14

4-1, 4-2

EC

P3. Prepare adjustments and close

accounts for a merchandising

company.

4-6, 4-7

4-9

4-3, 4-5, 4-6

CIP

P4. Define and prepare multiple-

step and single-step income

statements.

3, 10, 11, 12,

13, 14

4-10, 4-14

4-15, 4-20

4-3, 4-4

ED, GD

Grid continues on next page.

Chapter 04 Accounting for Merchandising Operations

a website, in whole or part. 4-2

Student Learning Objectives and Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies

Exercises

Problems

(A &B set)*

Beyond the

Numbers

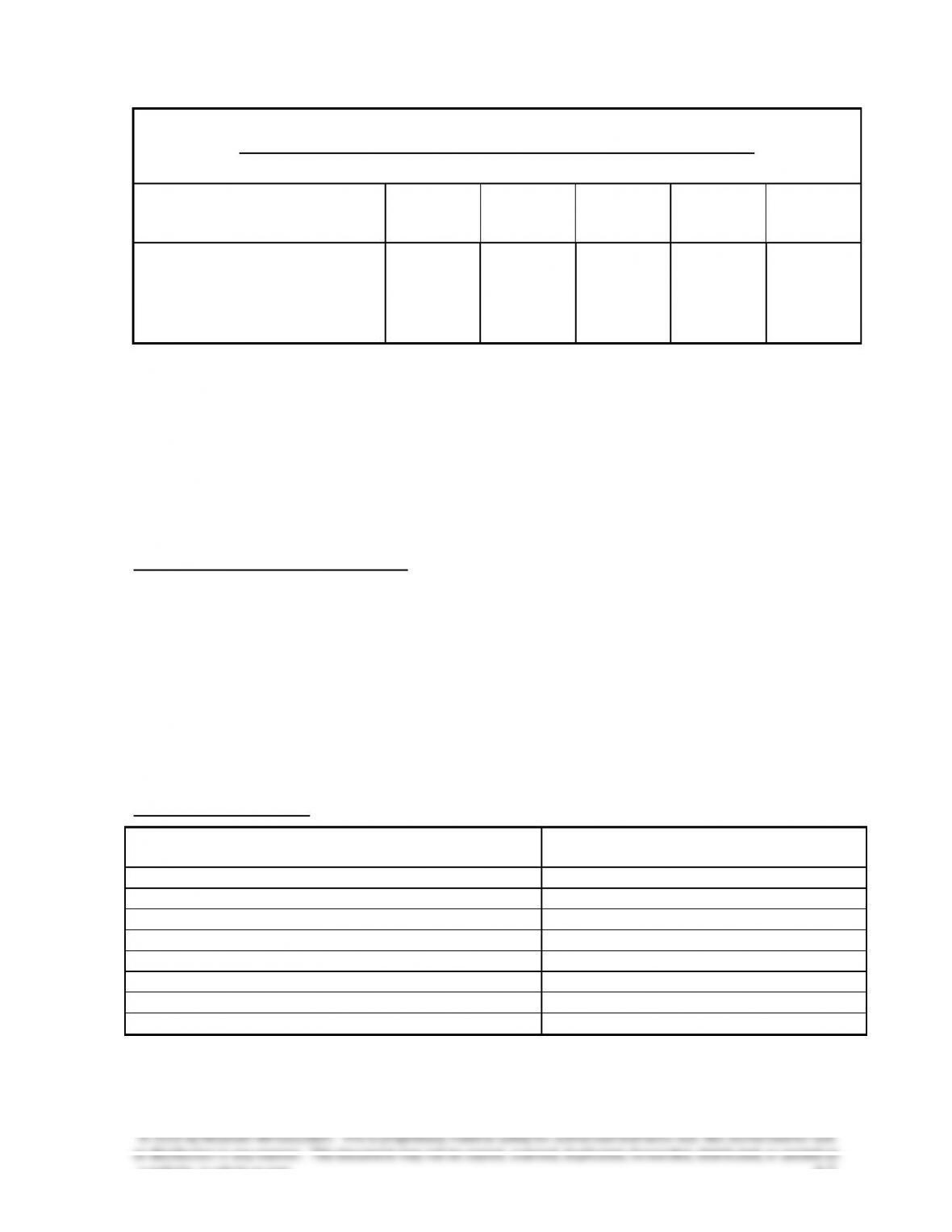

P5. Record and compare

merchandising transactions

using both periodic and

perpetual inventory systems.

(Appendix 4A)

5

4-11, 4-12,

4-13

4-16, 4-17,

4-18, 4-19

CIP

* Assignment materials that can be completed by students using:

Sage 50 and QuickBooks Pro 2013 templates– Problems 4-1A and P4-5A, and the Serial

Problem for Success Systems, which covers numerous learning objectives. (The serial

problem, which began in chapter 1, continues in most of the chapters. Even if previous

segments were not assigned, students can begin the segment of the serial problem that is

included in this chapter.)

Excel templates – Problem 4-3A.

McGraw-Hill’s Connect – All of the Quick Studies, all of the Exercises, and Problems in set A.

Synopsis of Chapter Revisions

• Faithful Fish: NEW opener with new entrepreneurial assignment

• Enhanced exhibit on transportation costs and FOB terms, with inclusion of entries

• New discussion of online ordering, tracking numbers, RFID, and FOB

• Revised the two-step explanation of recording merchandise sales

• New discussion on the importance and risks of accounting for sales returns

• Revised visual display of a sales invoice

• Revised discussion of merchandising purchases and sales

• New Volkswagen example for IFRS income statement

PowerPoint® Slides

Chapter Learning Objective

PowerPoint® Slides

C1

6-8

C2

9-10

P1

11-27

P2

28-34

P3

35-40

P4

41-43

A1

44

A2

45

Chapter 04 Accounting for Merchandising Operations

Chapter Outline

Notes

I. Merchandising Activities

Products that a company acquires to resell to customers are referred to

as merchandise (also called goods). A merchandiser earns net

income by buying and selling merchandise. A wholesaler is an

intermediary that buys products from manufacturers or other

wholesalers and sells them to retailers or other wholesalers.

A. Reporting Income for a Merchandiser

Revenue (net sales) from selling merchandise minus the cost of

goods sold (the expense of buying and preparing the merchandise)

to customers is called gross profit (also called gross margin). This

amount minus expenses (generally called operating expenses)

determines the net income or loss for the period.

B. Reporting Inventory for a Merchandiser

1. A merchandiser’s balance sheet is the same as a service

business with the exception of one additional current asset,

merchandise inventory, or simply inventory.

2. The cost of this asset includes the cost incurred to buy the

goods, ship them to the store, and make them ready for sale.

C. Operating Cycle for a Merchandiser

A merchandising company’s operating cycle begins by purchasing

merchandise and ends by collecting cash from selling the

merchandise. Companies try to keep their operating cycles short

because assets tied up in inventory and receivables are not

productive.

D. Inventory Systems

1. Merchandise available for sale consists of beginning inventory

and what it purchases (net purchases). The merchandise

available is either sold (cost of goods sold) or kept for future

sales (ending inventory).

2. Two alternative inventory systems are used to collect

information about cost of goods sold and the cost of inventory:

a. Perpetual inventory system—continually updates

accounting records for merchandise transactions,

specifically, for those records of inventory available for

sale and inventory sold.

b. Periodic inventory system—updates the accounting

records for merchandise transactions only at the end of a

period.

c. Some companies use a hybrid system where the perpetual

system is used for tracking units available and the periodic

system is used to compute cost of sales.

Chapter 04 Accounting for Merchandising Operations

Chapter Outline

Notes

The following sections of this outline use the perpetual inventory system.

Appendix 4A uses the period system (with perpetual results on the side). An

instructor can choose to cover either one or both inventory systems.

II. Accounting for Merchandise Purchases

The invoice serves as a source document for this event.

A. Purchase Discounts

Credit terms for a purchase include the amounts and timing of

payments from a buyer to a seller. The amount of time before full

payment is due is called the credit period.

1. Sellers can grant a cash discount to encourage the buyer to

pay earlier. A seller views a cash discount as a sales discount

and a buyer views a cash discount as a purchase discount.

This reduced payment applies only for the discount period.

2. Example: credit terms, 2/10 n/30, offers a 2 % discount if the

invoice is paid within 10 days of invoice date.

3. Entry for buyer for purchase of merchandise on credit: debit

Merchandise Inventory, credit Accounts Payable.

4. Entry for buyer to record payment within discount period:

debit Accounts Payable (full invoice amount), credit Cash

(amount paid = invoice – discount), credit Merchandise

Inventory (amount of discount).

B. Purchase Returns and Allowances

1. Purchase returns refer to merchandise a buyer acquires but

then returns to the seller.

2. A purchase allowance is a reduction in the cost of defective or

unacceptable merchandise that a buyer acquires.

3. The buyer issues a debit memorandum to inform the seller of

a debit made to the supplier’s account.

4. Entry for buyer to record purchase return or allowance: debit

Accounts Payable or Cash (if refund given) and credit

Merchandise Inventory.

5. When goods are returned, a buyer can take a purchase

discount on only the remaining balance of the invoice.

Chapter 04 Accounting for Merchandising Operations

Chapter Outline

Notes

C. Transportation Costs and Ownership Transfer

The buyer and seller must agree on who is responsible for paying

any freight costs and who bears the risk of loss during transit for

merchandising transactions. The point of transfer is called the

FOB (free on board) point.

1. FOB shipping point—buyer accepts ownership when goods

depart sellers’ place of business; buyer pays shipping costs.

a. Shipping costs increase the cost of merchandise acquired

(cost principle).

b. Entry for buyer to record shipping costs: Debit

Merchandise Inventory, credit Cash or Accounts Payable

(if to be paid with merchandise later).

2. FOB destination—ownership of goods transfers to buyer when

goods arrive at buyer’s place of business; seller pays shipping

costs.

a. Shipping costs are an operating (selling) expense for seller

b. Entry for seller to record shipping costs: Debit Delivery

Expense (or Transportation-Out or Freight-Out), credit

Cash.

III. Accounting for Merchandise Sales

A. Sales of Merchandise

Each sales transaction involves two parts and will therefore

require two entries:

1. Recognize revenue received —entry for seller to record: debit

Accounts Receivable (or cash), credit Sales (for the invoice

amount).

2. Recognize cost of merchandise sold— entry for seller to

record: debit Cost of Goods Sold, credit Merchandise

Inventory (for the cost of the merchandise sold).

B. Sales Discounts

Sales discounts are usually not recorded until a customer actually

pays with the discount period.

1. Entry for seller to record collection after discount period—

Debit Cash, Credit Accounts Receivable (full invoice amount).

2. Entry for seller to record collection within discount period—

debit Cash (invoice amount less discount), debit Sales

Discounts (discount amount), credit Accounts Receivable

(invoice amount).

3. Sales Discounts is a contra-revenue account; it is subtracted

from Sales when computing a company’s net sales.

4. Sales discounts are monitored to assess the effectiveness and

cost of its discount policy.

Chapter 04 Accounting for Merchandising Operations

Chapter Outline

Notes

C. Sales Returns and Allowances

1. Sales returns—merchandise that a customer returns to the

seller after a sale.

2. Sales allowances—reductions in the selling price of

merchandise sold to customers (usually for damaged or

defective merchandise that a customer is willing to keep at a

reduced price).

3. Entry for seller to record sales returns or allowances: debit

Sales Returns and Allowances and credit Accounts

Receivable; additional entry if returned merchandise is

salable: debit Merchandise Inventory, credit Cost of Goods

Sold.

4. Seller prepares a credit memorandum to inform buyer of the

seller’s credit to the buyer’s Accounts Receivable (on the

seller’s books).

IV. Completing the Accounting Cycle

A. Adjusting Entries for Merchandisers

Generally same as discussed in chapter 3 for a service business.

1. Additional adjustment needed to update inventory to reflect

any loss of merchandise, including theft and deterioration, is

referred to as shrinkage.

2. Shrinkage is determined by comparing a physical count of the

inventory with recorded quantities.

3. Entry to record shrinkage: debit Cost of Goods Sold, credit

Merchandise Inventory.

B. Preparing Financial Statements

The financial statement for a merchandiser are similar to those for

a service company described in chapters 2 and 3.

1. The income statement mainly differs by the inclusion of cost

of goods sold and gross profit. Net sales is affected by

discounts, returns, and allowances, and some additional

expenses are possible such as delivery expense and loss from

defective merchandise.

2. The balance sheet mainly differs by the inclusion of

merchandise inventory as part of current assets.

C. Closing Entries for Merchandisers

Closing entries are similar to a service business except that some

new temporary accounts that arise from merchandising activities

must be closed (e.g., Sales Discount, Sales Returns and

Allowances, and Cost of Goods Sold). These debit balance

accounts are closed with the expense accounts to Income

Chapter 04 Accounting for Merchandising Operations

Chapter Outline

Notes

V. Financial Statement Formats—No specific format is required in

practice. Two common income statement formats:

A. Multiple-Step Income Statement

1. A multiple-step income statement has three main parts:

a. Gross profit—net sales minus cost of goods sold),

b. Income from operations—gross profit less operating

expenses, and

c. Net income—income from operations adjusted for

nonoperating items.

2. Operating expenses are classified into two sections:

a. Selling expenses—the expenses of promoting sales,

making sales, and delivering goods to customers, and

b. General and administrative expenses—expenses related

to accounting, human resource management, and financial

management.

3. Nonoperating activities—consist of other expenses, revenues,

losses, and gains that are unrelated to a company’s operations;

reported in two sections:

a. Other revenues and gains—interest revenue, dividend

revenue, rent revenue, and gains from asset disposals.

b. Other expenses and losses—interest expense, losses from

asset disposals, and casualty losses.

B. Single-Step Income Statement

A single-step income statement includes cost of goods sold as an

operating expense and shows only one subtotal for total expenses,

one subtraction to arrive at net income.

C. Classified Balance Sheet

The merchandiser’s classified balance sheet reports merchandise

inventory as a current asset, usually after accounts receivable.

VI. Global View

A. Accounting and Reporting for Merchandising Purchases and

Sales – Both GAAP and IFRS include similar guidance in

accounting for merchandise purchases and sales. All of the

transactions presented in this chapter, including the closing process,

(or net revenue) followed by cost of goods sold for

merchandisers/manufacturers.

1. GAAP offers little guidance about the presentation or order of

Chapter 04 Accounting for Merchandising Operations

Chapter Outline

financing costs, income tax expense and other special items.

2. Both systems require separate disclosure of items when their

size, nature or frequency are important.

3. IFRS permits expenses to be presented by their function or

nature. GAAP provides no direction but the SEC requires

presentation by function.

4. Neither GAAP nor IFRS define operating income, which

results in latitude in reporting.

5. IFRS permits alternative income measures; US GAAP does

not.

C. Balance Sheet Presentation – GAAP balance sheets report

current items first, with assets listed from most liquid to least

liquid and liabilities are listed from nearest to maturity to

furthest from maturity. IFRS balance sheets present noncurrent

items first but this is not a requirement.

Notes

VII. Decision Analysis—Acid-Test and Gross Margin Ratios

A. Acid-Test Ratio

1. The acid-test ratio is used to assess the company’s liquidity or

ability to pay its current debts; it differs from the current ratio

by excluding less liquid current assets.

2. It is calculated by dividing quick assets by current liabilities;

quick assets are cash, short-term investments, and current

receivables.

3. Rule of thumb is that the acid-test ratio should have a value of at

least 1.0 to conclude that a company is unlikely to face near-term

liquidity problems.

B. Gross Margin Ratio

1. The gross margin ratio (also called gross profit ratio) is used

to assess a company’s profitability before considering

operating expenses.

2. It is calculated by dividing gross margin (net sales – cost of

goods sold) by net sales.

VIII. Periodic Inventory System (Appendix 4A)

A. Records merchandise acquisitions, discounts and returns in

temporary accounts (Purchases, Purchase Returns, Purchases

Discounts) rather than the merchandise inventory account.

B. Records only the revenue aspect of sales-related events; updates

inventory and determines cost of goods sold only at the end or the

accounting period.

C. The Merchandise Inventory account can be updated as part of the

adjusting or closing process.

Chapter 04 Accounting for Merchandising Operations

a website, in whole or part. 4-9

Chapter Outline

Notes

D. Requires closing additional temporary accounts.

E. Financial statements of merchandisers using the periodic system

are similar to those of a service company. The cost of goods sold

and gross profit are included in the income statement. The balance

sheet includes merchandise inventory in current assets.

IX. Work Sheet—Perpetual System (Appendix 4B)

Differs slightly from the work sheet layout for a service company in

Chapter 3; includes additional accounts used by a merchandiser:

Merchandise Inventory, Sales, Sales Returns and Allowances, Sales

Discounts, and Cost of Goods Sold.

a website, in whole or part. 4-10

Chapter 04 Accounting for Merchandising Operations

a website, in whole or part. 4-12

Chapter 4 – Alternate Demonstration Problem #1

The following data was taken from ledger account balances and

supplementary data for the Whisk Company for the year ended

December 31, 20xx:

Merchandise inventory, 1/1/20xx ……………………………………………

$ 20,000

Merchandise inventory, 12/31/20xx ………………………………………..

23,000

Purchases …………………………………………………………………………….

215,000

Purchases discounts …………………………………………………………….

6,000

Purchases returns and allowances ………………………………………..

3,000

Sales …………………………………………………………………………………….

400,000

Sales discounts …………………………………………………………………….

3,200

Sales returns and allowances ………………………………………………..

1,800

Transportation-in …………………………………………………………………..

10,000

Required:

1. Compute the total cost of merchandise purchases.

2. Compute the cost of goods sold.

3. Prepare a multiple-step income statement (only through the gross

profit line) for the year ended December 31, 20xx.

Chapter 04 Accounting for Merchandising Operations

a website, in whole or part. 4-13

Solution: Chapter 4 – Alternate Demonstration Problem #1

1.

Purchases

$215,000

Less: Purchase discounts

$6,000

Purchases returns and allowances

3,000

9,000

Net purchases

206,000

Add transportation–in

10,000

Total cost of merchandise purchases

$216,000

2.

Merchandise inventory, January 1, 20xx

$ 20,000

Total cost of merchandise purchases

216,000

Goods available for sale

236,000

Merchandise inventory, December 31, 20xx

23,000

Cost of goods sold

$213,000

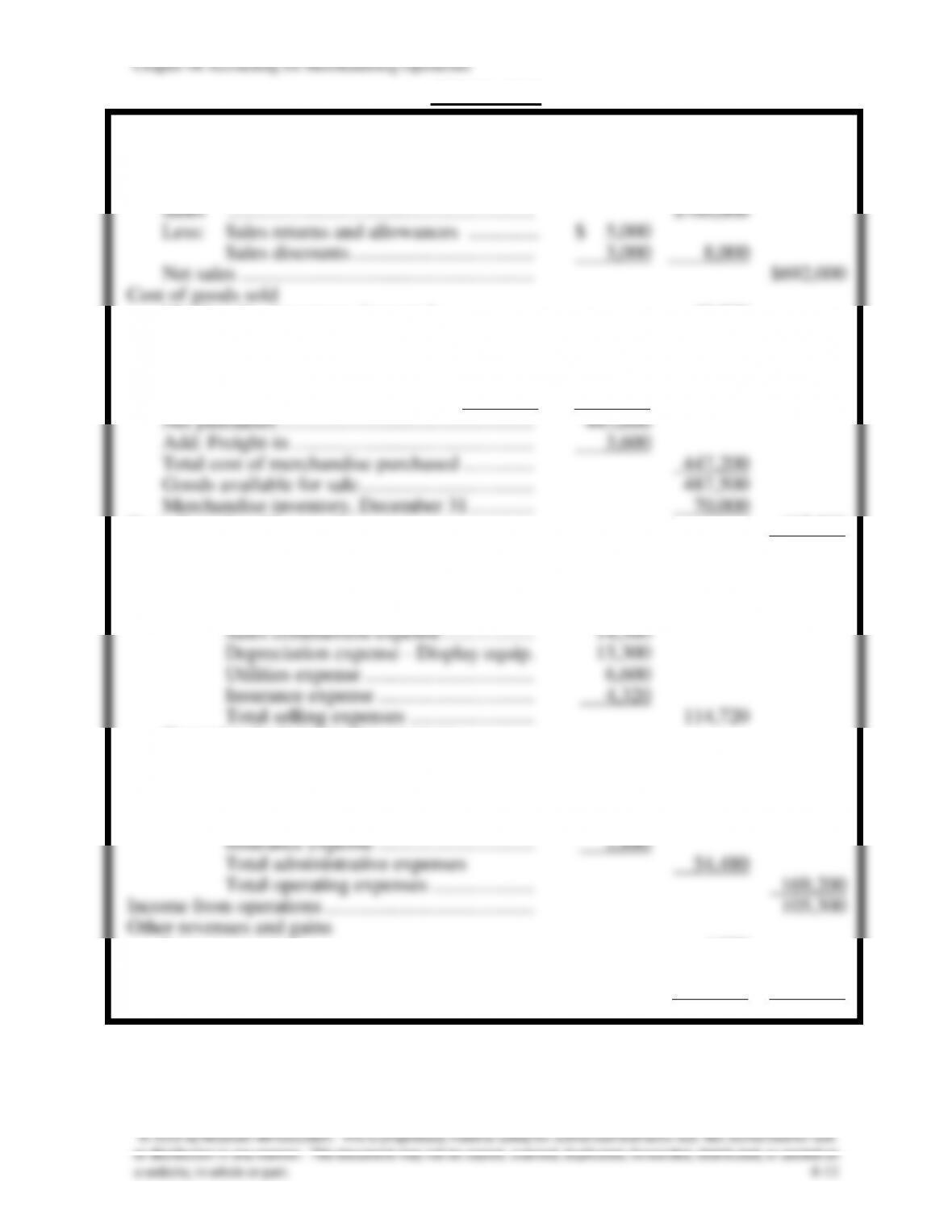

3.

WHISK COMPANY

Partial Income Statement

For the Year Ended December 31, 20xx

Revenue from sales:

Gross sales

$400,000

Less: Sales discounts

$ 3,200

Sales returns and

allowances

1,800

5,000

Net sales

395,000

Cost of goods sold

213,000

Gross profit

$182,000