Serial Problem, SP 3 (Continued)

Part 7

Closing entries

2013

Dec. 31 Computer Services Revenue …………………….. 403 31,284

Income Summary ……………………………….. 901 31,284

To close the revenue account.

31 Income Summary ……………………………………… 901 17,036

Depreciation Exp–Office Equipment ……. 612 400

Depreciation Exp–Computer Equipment .. 613 1,250

Wages Expense …………………………………. 623 3,875

Financial & Managerial Accounting, 5th Edition

216

Serial Problem, SP 3 (Continued)

Part 8

SUCCESS SYSTEMS

Post-Closing Trial Balance

December 31, 2013

Debit Credit

Cash ……………………………………………………………………. $ 58,160

Accounts receivable …………………………………………….. 5,668

Computer supplies ………………………………………………. 580

Prepaid insurance ………………………………………………… 1,665

Prepaid rent …………………………………………………………. 825

Serial Problem, SP 3 (Continued)

[Note: Ledger includes all entries from prior three months. The Working Papers shorten

the solution by showing account balances as of November 30.]

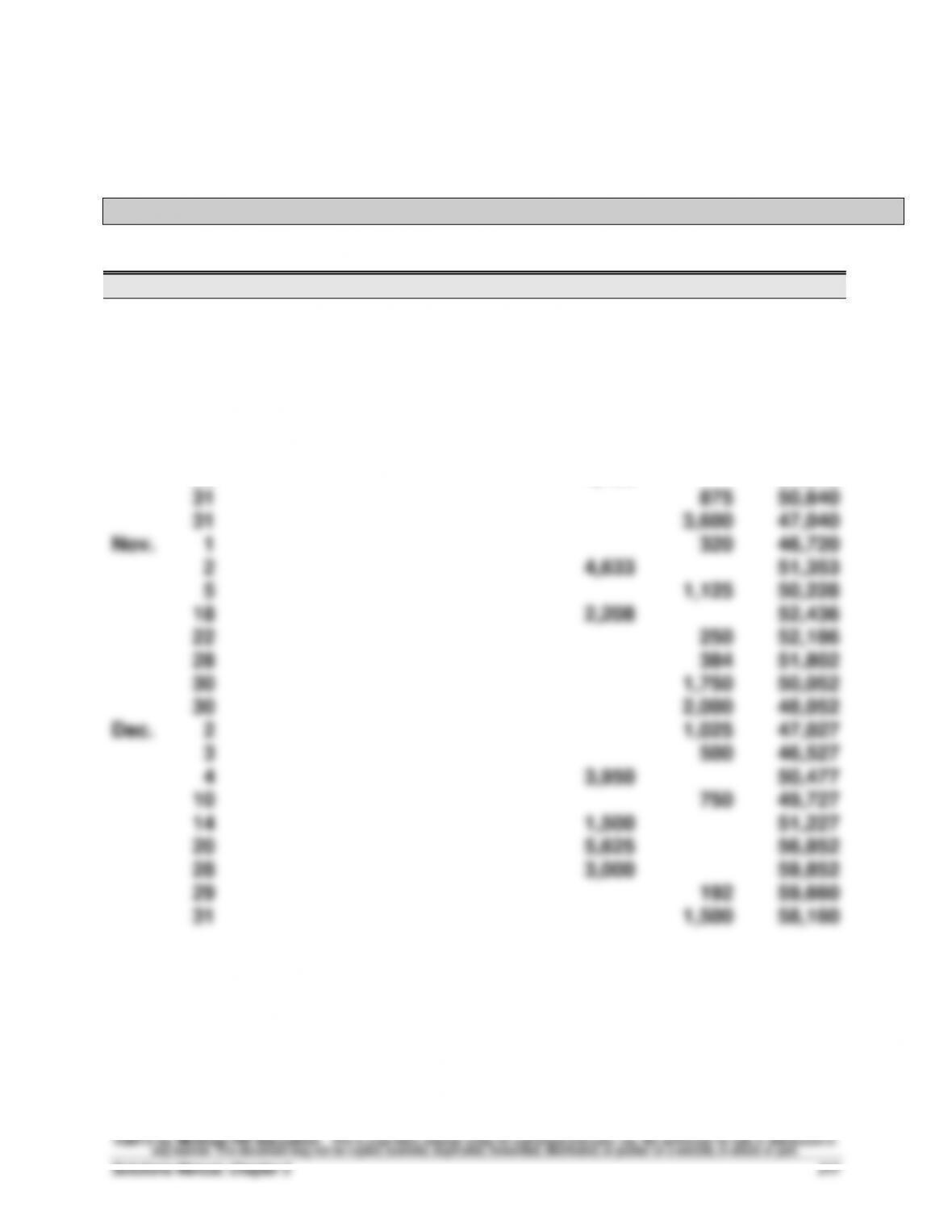

General Ledger

Cash

Acct. No. 101

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

55,000

55,000

2

3,300

51,700

5

2,220

49,480

8

1,420

48,060

15

4,800

52,860

17

805

52,055

20

1,940

50,115

22

1,400

51,515

31

875

50,640

31

3,600

47,040

Nov.

1

320

46,720

2

4,633

51,353

5

1,125

50,228

18

2,208

52,436

22

250

52,186

28

384

51,802

30

1,750

50,052

30

2,000

48,052

Dec.

2

1,025

47,027

3

500

46,527

4

3,950

50,477

10

750

49,727

14

1,500

51,227

20

5,625

56,852

28

3,000

59,852

29

192

59,660

31

1,500

58,160

Financial & Managerial Accounting, 5th Edition

218

Serial Problem, SP 3 (Continued)

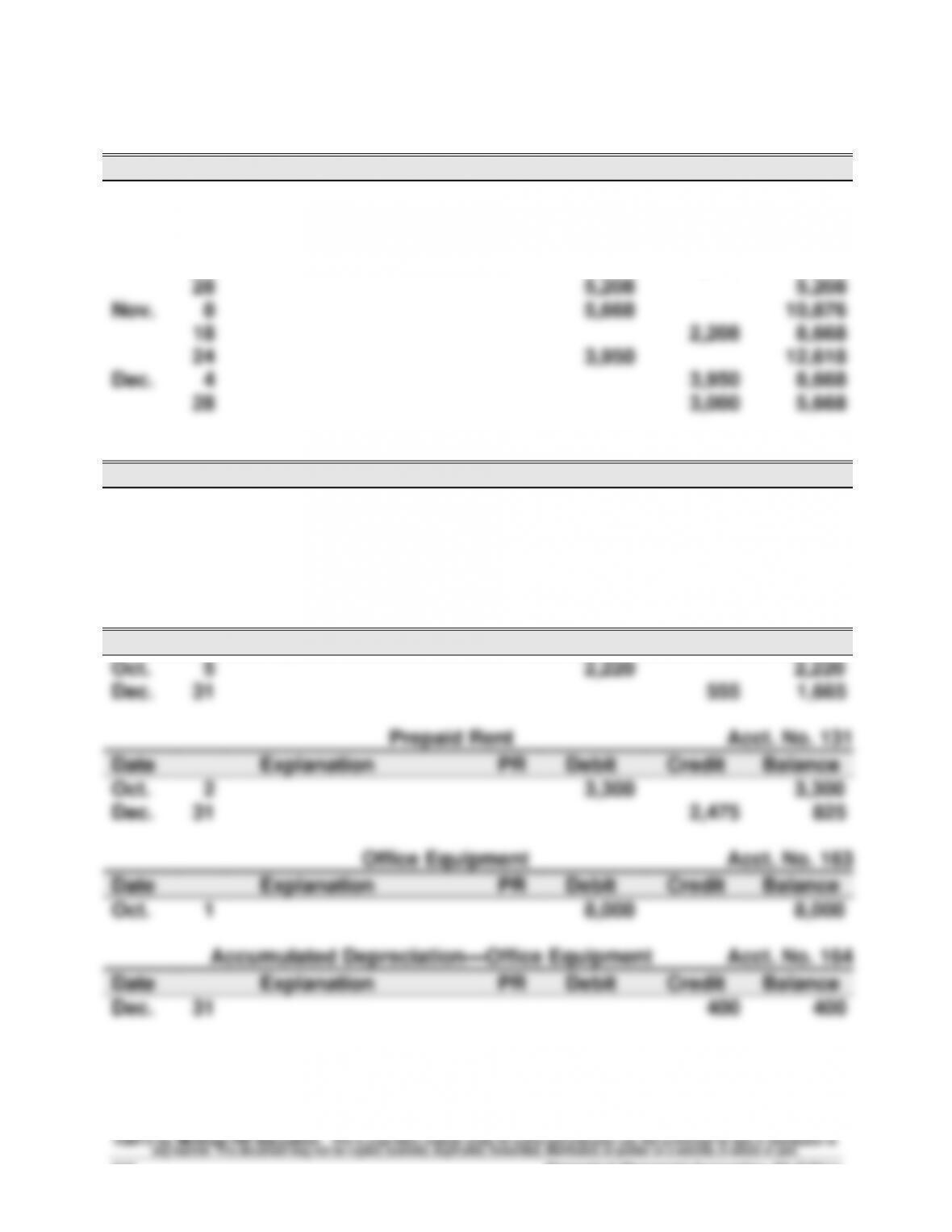

Accounts Receivable

Acct. No. 106

Date

Explanation

PR

Debit

Credit

Balance

Oct.

6

4,800

4,800

12

1,400

6,200

15

4,800

1,400

22

1,400

0

28

5,208

5,208

Nov.

8

5,668

10,876

18

2,208

8,668

24

3,950

12,618

Dec.

4

3,950

8,668

28

3,000

5,668

Computer Supplies

Acct. No. 126

Date

Explanation

PR

Debit

Credit

Balance

Oct.

3

1,420

1,420

Nov.

5

1,125

2,545

Dec.

15

1,100

3,645

31

3,065

580

Prepaid Insurance

Acct. No. 128

Date

Explanation

PR

Debit

Credit

Balance

Oct.

5

2,220

2,220

Dec.

31

555

1,665

Prepaid Rent

Acct. No. 131

Date

Explanation

PR

Debit

Credit

Balance

Oct.

2

3,300

3,300

Dec.

31

2,475

825

Office Equipment

Acct. No. 163

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

8,000

8,000

Accumulated Depreciation—Office Equipment

Acct. No. 164

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

400

400

Serial Problem, SP 3 (Continued)

Computer Equipment

Acct. No. 167

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

20,000

20,000

Accumulated Depreciation—Computer Equipment

Acct. No. 168

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

1,250

1,250

Accounts Payable

Acct. No. 201

Date

Explanation

PR

Debit

Credit

Balance

Oct.

3

1,420

1,420

8

1,420

0

Dec.

15

1,100

1,100

Wages Payable

Acct. No. 210

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

500

500

Unearned Computer Services Revenue

Acct. No. 236

Date

Explanation

PR

Debit

Credit

Balance

Dec.

14

1,500

1,500

Common Stock

Acct. No. 307

Date

Explanation

PR

Debit

Credit

Balance

Oct.

1

83,000

83,000

Retained Earnings

Acct. No. 318

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

Closing

14,248

14,248

31

Closing

7,100

7,148

Dividends

Acct. No. 319

Date

Explanation

PR

Debit

Credit

Balance

Oct.

31

3,600

3,600

Nov.

30

2,000

5,600

Dec.

31

1,500

7,100

31

Closing

7,100

0

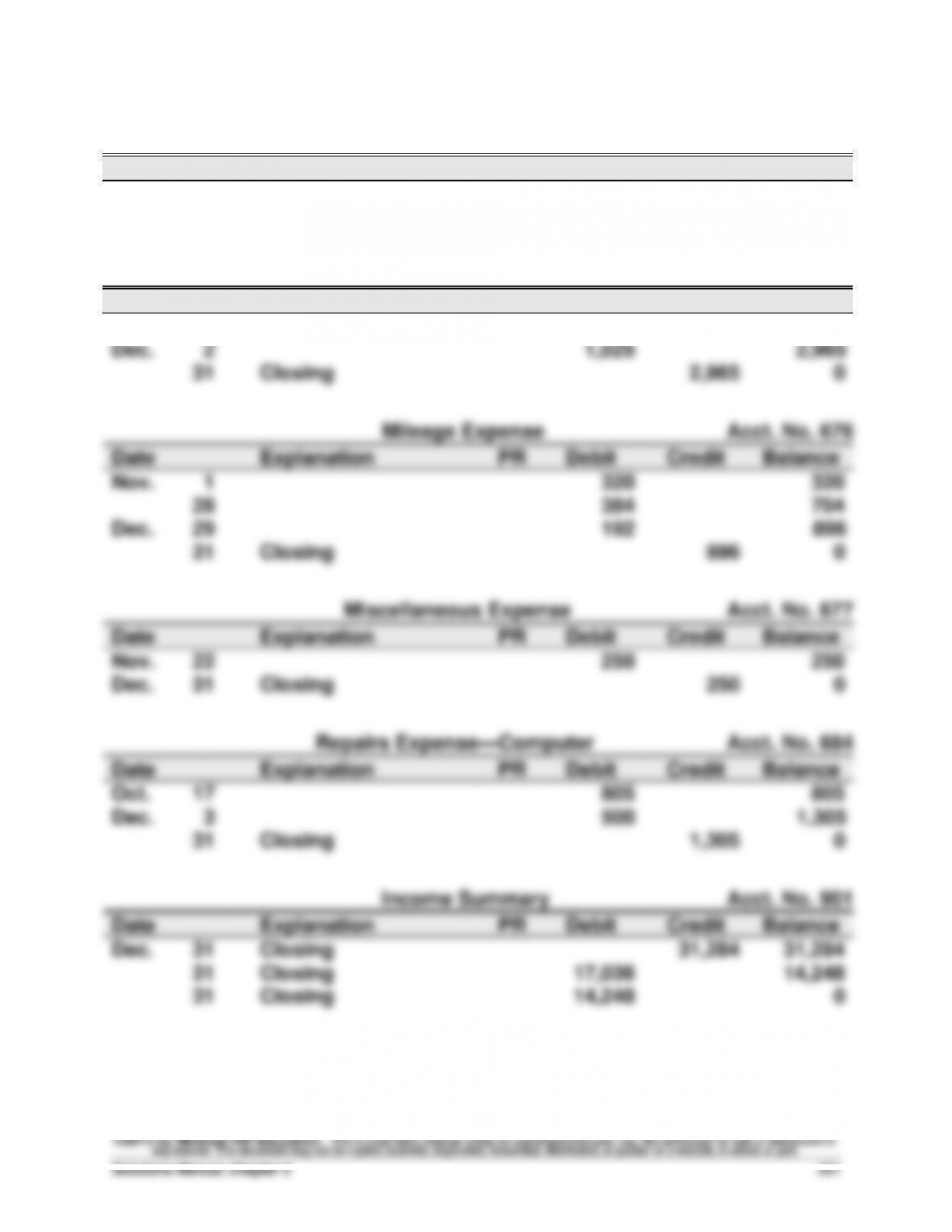

Serial Problem, SP 3 (Continued)

Computer Services Revenue

Acct. No. 403

Date

Explanation

PR

Debit

Credit

Balance

Oct.

6

4,800

4,800

12

1,400

6,200

28

5,208

11,408

Nov.

2

4,633

16,041

8

5,668

21,709

24

3,950

25,659

Dec.

20

5,625

31,284

31

Closing

31,284

0

Depreciation Expense—Office Equipment

Acct. No. 612

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

400

400

31

Closing

400

0

Depreciation Expense—Computer Equipment

Acct. No. 613

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

1,250

1,250

31

Closing

1,250

0

Wages Expense

Acct. No. 623

Date

Explanation

PR

Debit

Credit

Balance

Oct.

31

875

875

Nov.

30

1,750

2,625

Dec.

10

750

3,375

31

500

3,875

31

Closing

3,875

0

Insurance Expense

Acct. No. 637

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

555

555

31

Closing

555

0

Rent Expense

Acct. No. 640

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

2,475

2,475

31

Closing

2,475

0

Serial Problem, SP 3 (Concluded)

Computer Supplies Expense

Acct. No. 652

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

3,065

3,065

31

Closing

3,065

0

Advertising Expense

Acct. No. 655

Date

Explanation

PR

Debit

Credit

Balance

Oct.

20

1,940

1,940

Dec.

2

1,025

2,965

31

Closing

2,965

0

Mileage Expense

Acct. No. 676

Date

Explanation

PR

Debit

Credit

Balance

Nov.

1

320

320

28

384

704

Dec.

29

192

896

31

Closing

896

0

Miscellaneous Expense

Acct. No. 677

Date

Explanation

PR

Debit

Credit

Balance

Nov.

22

250

250

Dec.

31

Closing

250

0

Repairs Expense—Computer

Acct. No. 684

Date

Explanation

PR

Debit

Credit

Balance

Oct.

17

805

805

Dec.

3

500

1,305

31

Closing

1,305

0

Income Summary

Acct. No. 901

Date

Explanation

PR

Debit

Credit

Balance

Dec.

31

Closing

31,284

31,284

31

Closing

17,036

14,248

31

Closing

14,248

0

Reporting in Action — BTN 3-1

1. The revenue recognition principle requires that revenue be recorded

when realized or realizable and earned, not before and not after. Most

companies earn revenue when they provide services and products to

customers.

2. Polaris provides information on revenue recognition in its Note 1 titled

“Organization and Significant Accounting Policies.” They report that

products are sold to the dealer or distributor customer.

3. For year-end December 31, 2010, the profit margin is ($ thousands):

4. The revenue items from its income statement must be identified, and

those would be credited to Income Summary as step 1 in the closing

5. The total expenses that would be debited to Income Summary as step 2

in the closing entry process must be computed. Polaris’s total

expenses for the year ended December 31, 2011, are (in thousands):

Cost of sales ………………………………………………………… $ 1,916,366