Chapter 03 – Adjusting Accounts and Preparing Financial Statements

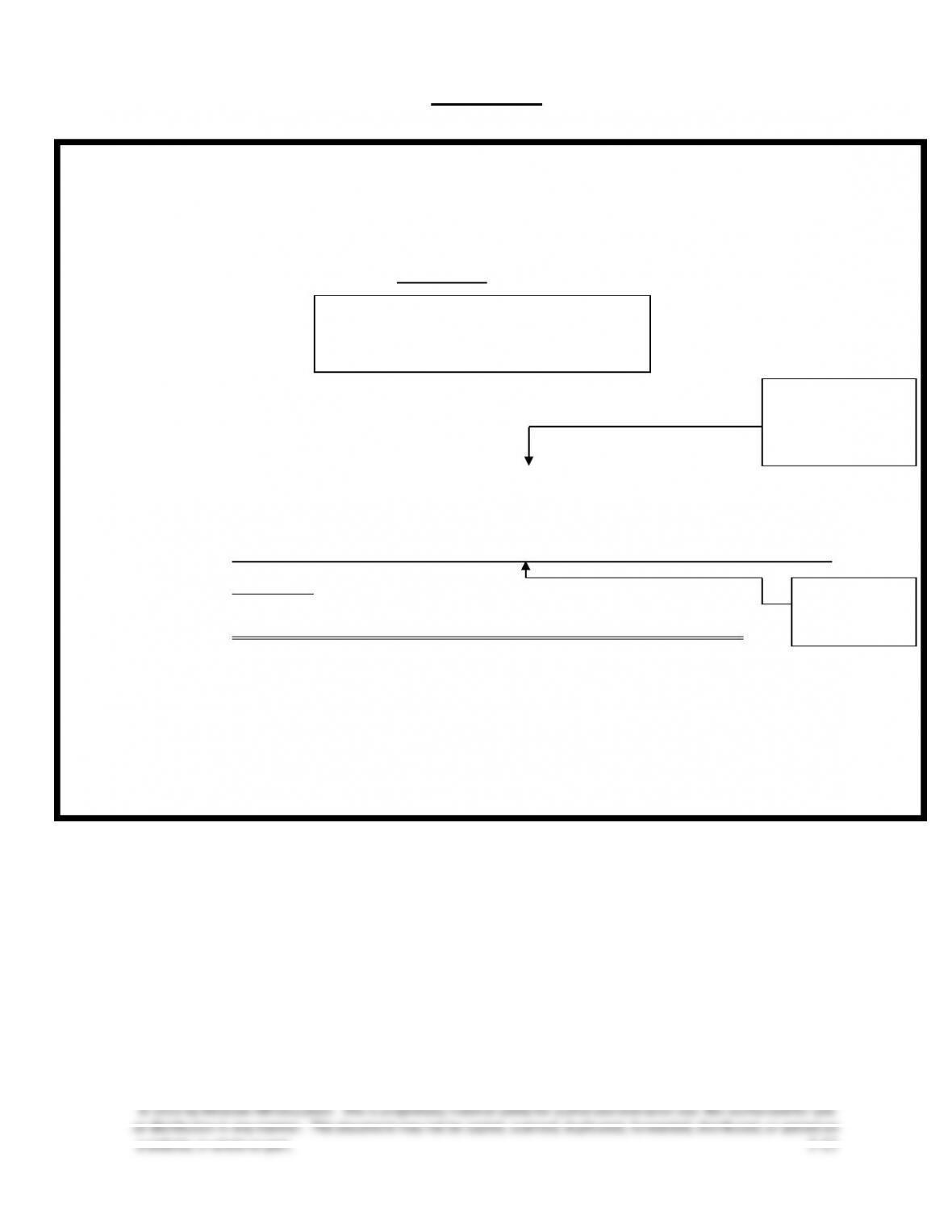

VISUAL #3-1

ACCRUAL BASIS ACCOUNTING

(Follows GAAP)

requires that the

Income Statement

(for a period)

reports

ALL REVENUES EARNED in period (Collected or Not)

Minus ALL EXPENSES INCURRED in period (Paid

or Not)

Equals Net Income or Net Loss for the period

ACCOUNTS MUST BE ADJUSTED TO FOLLOW

PRINCIPLES

GAAP

Revenue

Recognition

GAAP

Matching

Chapter 03 – Adjusting Accounts and Preparing Financial Statements

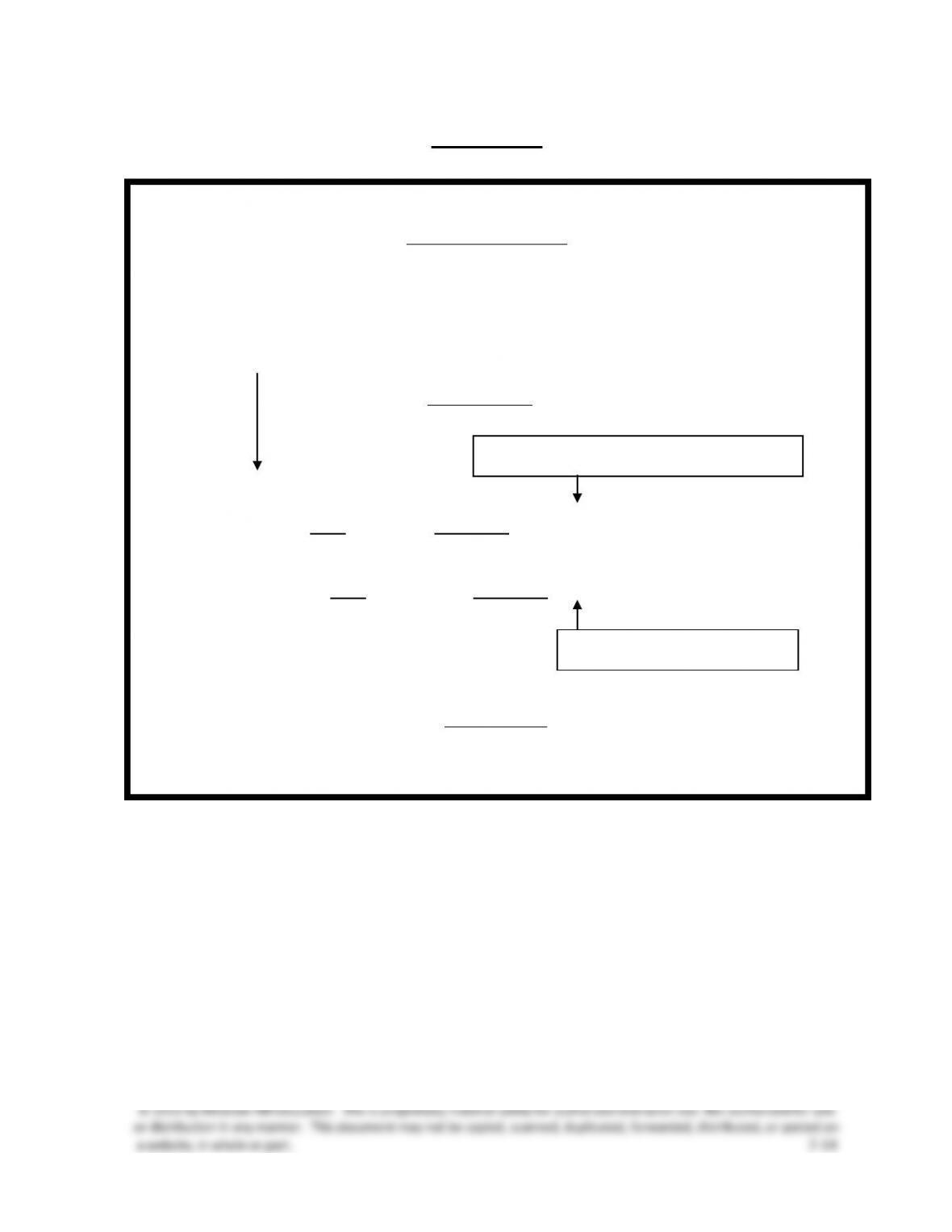

VISUAL #3-2

DEFERRALS

The converse of statements in Visual #3-1 also applies.

Revenue not earned or expense not incurred results in

Deferrals*

UNEARNED = LIABILITY *

A REVENUE not earned cannot be shown, even if collected.

An EXPENSE not incurred cannot be shown, even if paid.

PREPAID = ASSET *

*We defer or postpone the reporting of the collected revenues

(as revenues) and prepaid expenses (as expenses) until the

revenue is earned and the expense is incurred.

Chapter 03 – Adjusting Accounts and Preparing Financial Statements

a website, in whole or part. 3-15

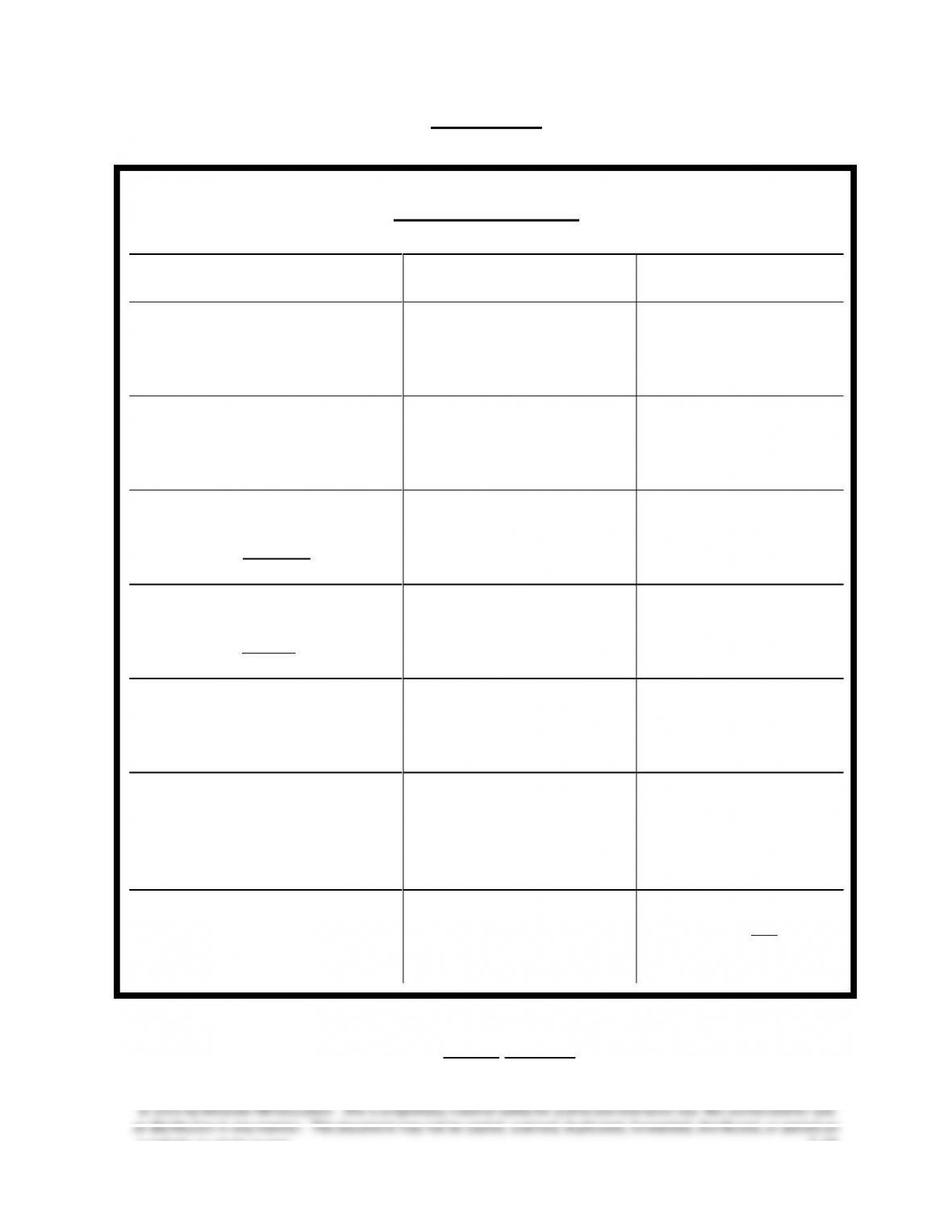

VISUAL #3-3

ADJUSTMENTS

TYPE

GENERALIZED*

ENTRY

AMOUNT

1. Prepaid items or supplies

a) initially recorded as assets

Dr. _________ Expense

Cr. The Asset* acct.

Amount used, or

consumed, or expired

b) initially recorded as

expenses (alternate

treatment)

Dr. the Asset** acct.

Cr. ________ Expense

Amount left, or

not consumed, or

unexpired

2. Accrued expenses

(expenses incurred but not

yet recorded)

Dr. _________ Expense

Cr. _________ Payable

Amount accrued

3. Accrued revenues

(revenues earned but not

yet recorded)

Dr. ________ Receivable

Cr. The Revenue**

acct.

Amount accrued

4. Long-term assets that are

depreciable

Dr. Depreciation Expense

Cr. Accumulated

Depreciation

Portion of cost

allocated to this period

as depreciation

5. Unearned revenues

(received in advance)

a) record initially as liability

(unearned account)

Dr. Unearned ________

Cr. The Revenue**

acct.

Amount earned to date

b) initially recorded as a

revenue (alternate

treatment)

Dr. the Revenue** acct.

Cr. Unearned________

Amount still not

earned

* Note: (1) Each adjustment affects a Balance Sheet Account and an Income

Statement Account (2) CASH NEVER appears in an adjustment.

** Title or account name varies.

Chapter 03 – Adjusting Accounts and Preparing Financial Statements

a website, in whole or part. 3-16

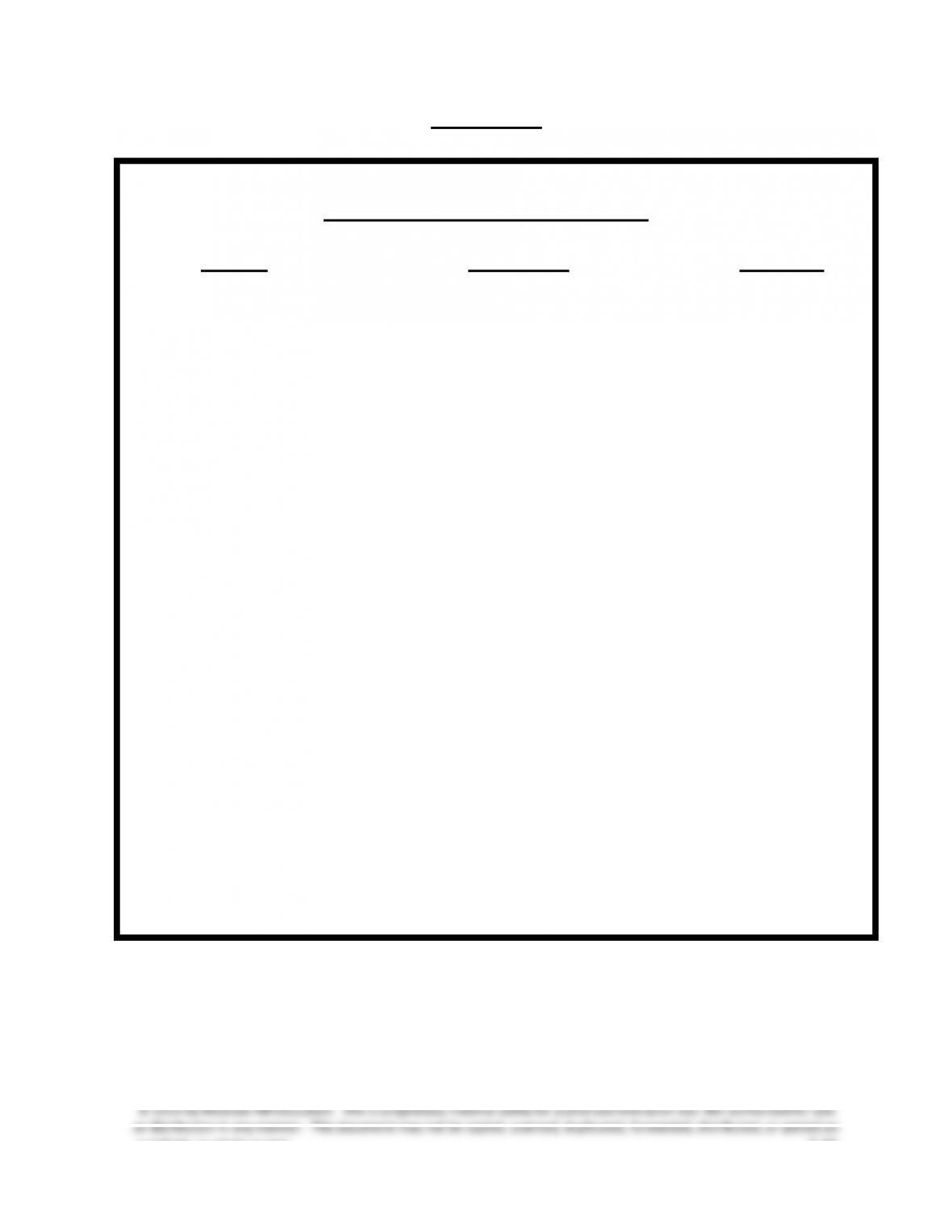

VISUAL #3-4

THE ACCOUNTING CYCLE

STEPS

PURPOSE

TIMING

1. Analyze

transactions

Analyze transactions to prepare for

journalizing.

During the period

2. Journalize

Record accounts, including debits and

credits, in a journal.

During the period

3. Post

Transfer debits and credits from the

journal to the ledger.

During the period

4. Prepare

unadjusted

trial balance

Summarize unadjusted ledger

accounts and amounts.

End of period

5. Adjust

Record adjustments to bring account

balances up to date; journalize and

post adjusting entries.

End of period

6. Prepared adjusted

trial balance

Summarize adjusted ledger accounts

and amounts.

End of period

7. Prepare

statements

Use adjusted trial balance to prepare

financial statements.

End of period

8. Close

Journalize and post entries to close

temporary accounts.

End of year

9. Prepare post-

closing trial

balance

Test clerical accuracy of the closing

procedures.

End of year

10. Reverse

(Optional)

Reverse certain adjustments in the

next period

Beginning of next

year

Chapter 03 – Adjusting Accounts and Preparing Financial Statements

a website, in whole or part. 3-17

VISUAL #3-5

MUSIC WORLD

BALANCE SHEET

DECEMBER 31, xxxx

Assets

Current Assets

Cash

$30,360

Short-Term Investments

2,000

Notes Receivable

8,000

Accounts Receivable

35,300

Merchandise Inventory

60,400

Prepaid Insurance

6,600

Supplies

1,696

Total Current Assets

$144,356

Investments

Land Held for Future Use

13,950

Property, Plant, and Equipment

Land

$ 4,500

Building

$20,650

Less Accumulated Depreciation

8,640

12,010

Office Equipment

$ 8,600

Less Accumulated Depreciation

5,000

3,600

Total Property, Plant, and Equipment

20,110

Intangible Assets

Trademark

500

Total Assets

$178,916

Liabilities

Current Liabilities

Notes Payable

$15,000

Accounts Payable

25,683

Salaries Payable

2,000

Current Portion of Mortgage Payable

10,200

Total Current Liabilities

$ 52,883

Long-Term Liabilities

Mortgage Payable

27,600

Total Liabilities

$ 80,483

Equity

Common Stock

40,000

Retained Earnings

58,433

Total Liabilities and Equity

$178,916

Chapter 03 – Adjusting Accounts and Preparing Financial Statements

a website, in whole or part. 3-18

Chapter 3 – Alternate Demonstration Problem #1

On July 1, 2013, Howard M. Tenant, Inc., rents office space from John Q.

Landlord for two years, starting immediately, at a rate of $100 per month,

or $2,400 in total. The full $2,400 was paid on this date.

Required:

Record the original transaction on 7/1 and the appropriate adjusting

entries in 2013, 2014, and 2015 from the point of view of Tenant and

Landlord.

Chapter 03 – Adjusting Accounts and Preparing Financial Statements

a website, in whole or part. 3-19

Solution: Chapter 3 – Alternate Demonstration Problem #1

Tenant

Landlord

7/1/13

Prepaid Rent …………….

2,400

Cash ………………………...

2,400

Cash

2,400

Unearned Rent

Rev. ………………...

2,400

12/31/13

Rent Expense …………..

600

Unearned Rent Rev.

600

Prepaid Rent ……..

600

Rent Revenue

600

12/31/14

Rent Expense …………..

1,200

Unearned Rent Rev.

1,200

*Prepaid Rent …….

1,200

Rent Revenue

1,200

12/31/15

*Rent Expense ………….

600

Unearned Rent Rev.

600

Prepaid Rent ……..

600

Rent Revenue

600

Alternative Solution (Reversing Entries)

7/1/13

Rent Expense …………..

2,400

Cash ………………………...

2,400

Cash………………….

2,400

Rent Rev. …………..

2,400

12/31/13

Prepaid Rent ……………

1,800

Rent Rev.

1,800

Rent Expense ……

1,800

Unearned Rent

Revenue …………..

1,800

*12/31/14

Rent Expense …………..

1,200

Unearned Rent Rev.

1,200

Prepaid Rent ……..

1,200

Rent Revenue

1,200

*12/31/15

Rent Expense …………..

600

Unearned Rent Rev.

600

Prepaid Rent ……..

600

Rent Revenue

600

* Notice the adjustment is the same in 10 and 11 under both methods.

This is because the 10 adjustment in the alternative solution (using

reversing entries) places all remaining unexpired/unearned amounts in

the asset/liability accounts to be considered for future adjustment.

a website, in whole or part. 3-20

Chapter 03 – Adjusting Accounts and Preparing Financial Statements

a website, in whole or part. 3-21

Solution: Chapter 3 – Alternate Demonstration Problem #2

Insurance Expense ……………………………………

600

Prepaid Insurance ……………………………….

600

Supplies Expense ……………………………………..

1,300

Supplies ……………………………………………..

1,300

Depreciation Expense Equip. ……………………..

1,000

Accumulated Depreciation Equip. ………..

1,000

Salaries Expense ………………………………………

700

Salaries Payable ………………………………….

700

Chapter 03 – Adjusting Accounts and Preparing Financial Statements

a website, in whole or part. 3-22

Chapter 3 – Alternate Demonstration Problem #3

The trial balance of Large Company, Inc. at the end of its annual

accounting period is as follows:

LARGE COMPANY, INC.

Trial Balance

December 31, 2013

Cash ………………………………………………………………..

$ 4,000

Prepaid Insurance ……………………………………………

1,600

Supplies …………………………………………………………

2,100

Equipment ………………………………………………………

20,000

Accumulated depreciation equipment ………………

$ 2,000

Common stock ……………………………………………….

10,000

Retained earnings ……………………………………………

7,000

Revenue ………………………………………………………….

33,000

Salaries expense ……………………………………………..

18,300

Rent expense …………………………..……………………..

6,000

______

Totals ………………………………………………………………

$52,000

$52,000

Additional information:

▪ Expired insurance, $600.

▪ Unused supplies, per inventory, $800.

▪ Estimated depreciation, $1,000.

▪ Earned but unpaid salaries, $700.

Required:

1. Prepare adjusting entries.

2. Prepare closing entries.

3. Prepare a post-closing trial balance.

Chapter 03 – Adjusting Accounts and Preparing Financial Statements

a website, in whole or part. 3-23

Solution: Chapter 3 – Alternate Demonstration Problem #3

1.

Insurance Expense ………………………………………….

600

Prepaid Insurance …………………………………….

600

Supplies Expense ……………………………………………

1,300

Supplies …………………………..………………………

1,300

Depreciation Expense Equip. …………………………..

1,000

Accumulated Depreciation Equip. ………………

1,000

Salaries Expense …………………………………………….

700

Salaries Payable ……………………………………….

700

2.

Revenue …………………………………………………………

33,000

Income Summary ……………………………………..

33,000

Income Summary ……………………………………………

27,900

Salaries Expense …………………………..………….

19,000

Rent Expense……………………………………………

6,000

Insurance Expense ……………………………………

600

Supplies Expense ……………………………………..

1,300

Depreciation Expense ……………………………….

1,000

Income Summary ……………………………………………

5,100

Retained Earnings …………………………………….

5,100

3.

LARGE COMPANY, INC.

Post-Closing Trial Balance

December 31, 2013

Dr.

Cr.

Cash ………………………………………………………………

$4,000

Prepaid Insurance …………………………………………..

1,000

Supplies …………………………………………………………

800

Equipment………………………………………………………

20,000

Accumulated depreciation, equipment ……………..

$ 3,000

Salaries payable ……………………………………………..

700

Common stock ……………………………………………….

10,000

Retained earnings …………………………………………..

______

12,100

Totals …………………………………………………………….

$25,800

$25,800