Chapter 24

Capital Budgeting and Investment

Analysis

QUESTIONS

1. Capital budgeting decisions require careful analysis because they are generally

3. Capital budgeting decisions are risky because: (1) the outcomes are uncertain,

5. A shorter payback period is desirable because management prefers to reduce

the risk that the investment might not be profitable over the long run. As a result

6. If net income is earned evenly throughout each year and straight-line

7. When the present value of expected net cash flows, discounted at 10%, exceeds

the amount invested it indicates that the expected rate of return on the

Financial & Managerial Accounting, 5th Edition

1340

QUICK STUDIES

Quick Study 24-1 (10 minutes)

Quick Study 24-2 (10 minutes)

1. If all else is equal, Investment A would be preferred over Investment B

2. However, if the investments are different, then there are at least four

reasons why Investment B might be preferred over Investment A:

i. The present value of cash flows from Investment B might greatly

exceed the present value of cash flows from Investment A.

Quick Study 24-3 (10 minutes)

Quick Study 24-4 (15 minutes)

Net present value of investment*

Present value of seven $10,000 cash inflows (10,000 x 4.8684) ……..……

$48,684

Present value of $6,000 at end of seven years (6,000 x 0.5132) ……..……

3,079

Present value of cash inflows ……………………………………………………….

51,763

Less immediate cash outflow ……………………………………………………….

50,000

Net present value ………………………………………………………………………..……

$ 1,763

*Present value factors from tables at the end of Appendix B:

4.8684 = Present value of an annuity of 1, where n = 7, i = 10% (from Table B.3)

0.5132 = Present value of 1, where n = 7, i = 10% (from Table B.1)

Financial & Managerial Accounting, 5th Edition

1342

Quick Study 24-5 (10 minutes)

Project A: Profitability index = $1,100,000 / 400,000 = 2.75

Quick Study 24-6 (10 minutes)

Quick Study 24-7 (15 minutes)

Year

Net Cash

Flows

Present

Value of

1 at 10%

Present

Value of Net

Cash Flows

1 …………………………………………………..

$ 45,000

0.9091

$ 40,910

2 …………………………………………………..

52,000

0.8264

42,973

3 …………………………………………………..

78,000

0.7513

58,601

Total …………………………………………….

$175,000

$142,484

Initial investment…………………………..

(135,000)

Net present value ………………………….

$ 7,484

Quick Study 24-8 (15 minutes)

Year

Cash flows

Present value

of 1 at 10%

Present value of

cash flows

Cumulative

present value of

cash flows

0

$(90,000)

1.0000

$(90,000)

$(90,000)

1

35,000

0.9091

31,819

(58,181)

2

35,000

0.8264

28,924

(29,257)

3

35,000

0.7513

26,296

(2,961)

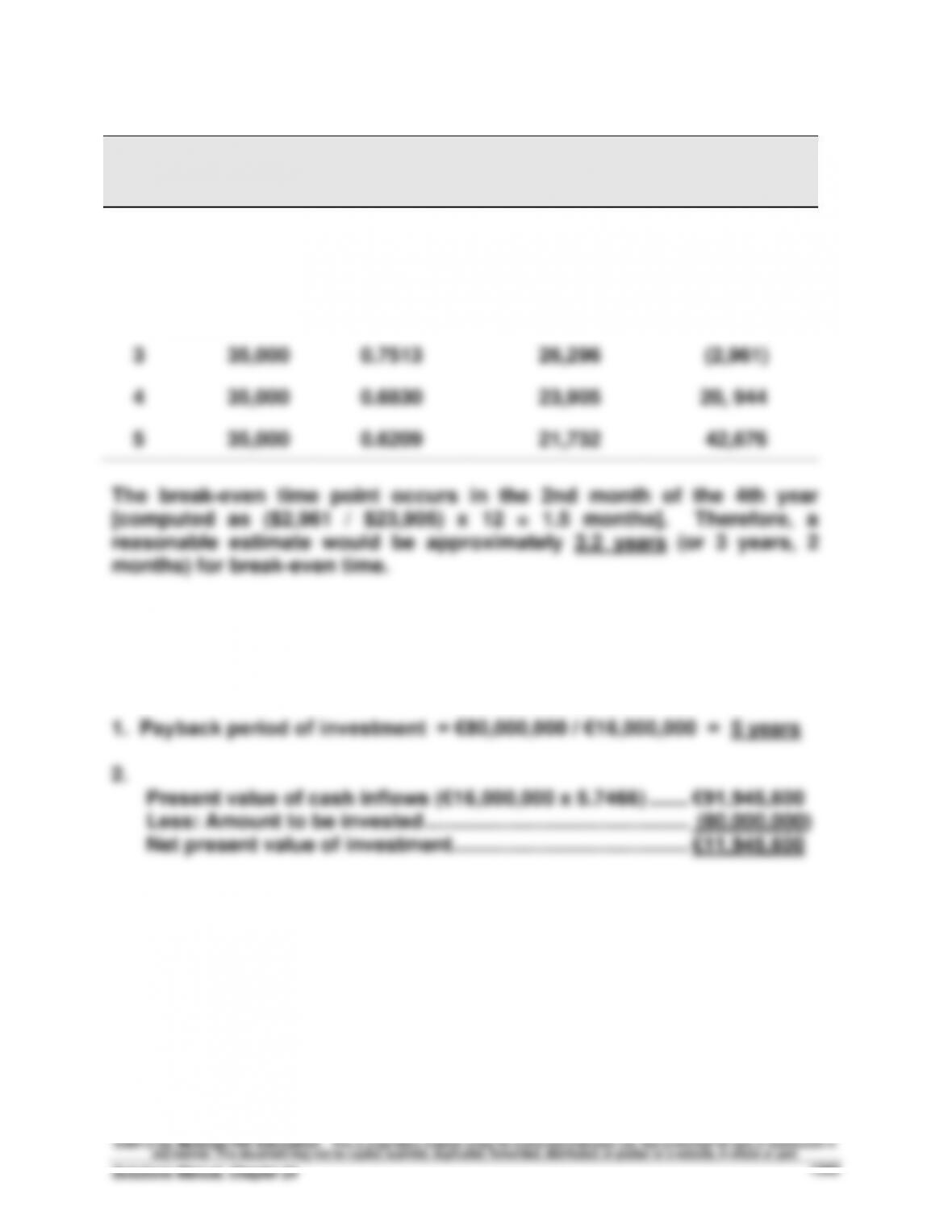

4

35,000

0.6830

23,905

20, 944

5

35,000

0.6209

21,732

42,676

The break-even time point occurs in the 2nd month of the 4th year

[computed as ($2,961 / $23,905) x 12 = 1.5 months]. Therefore, a

reasonable estimate would be approximately 3.2 years (or 3 years, 2

months) for break-even time.

Quick Study 24-9 (15 minutes)

EXERCISES

Exercise 24–1 (20 minutes)

Annual Net

Cumulative

Cash Flows

Cash Flows

Year 1 …………………………..………………………………

$ 60,000

$ 60,000

Year 2 …………………………..………………………………

40,000

100,000

Year 3 …………………………..………………………………

70,000

170,000

Year 4 …………………………..………………………………

125,000

295,000

Year 5 …………………………..………………………………

35,000

330,000

Exercise 24-2 (30 minutes)

COMPUTATION OF ANNUAL DEPRECIATION EXPENSE

Double-declining balance rate = (100% / 5) x 2 = 40%

Annual Depr.

Beginning

(40% of

Accum. Depr.

Ending

Year

Book Value

Book Value)

at Year-End

Book Value

1

$150,000

$60,000

$ 60,000

$90,000

2

90,000

36,000

96,000

54,000

3

54,000

21,600

117,600

32,400

4

32,400

12,960

130,560

19,440

5

19,440

19,440

150,000

0

ANNUAL CASH FLOWS

Net

Income

Depreciation

Net Cash

Flow

Cumulative

Cash Flow

Year 1

$ 10,000

$60,000

$ 70,000

$ 70,000

Year 2

25,000

36,000

61,000

131,000

Year 3

50,000

21,600

71,600

202,600

Year 4

37,500

12,960

50,460

253,060

Year 5

100,000

19,440

119,440

372,500

Cost of machine…………………………………………………………………….……..

$150,000

Paid back in years 1 and 2 ……………………………………………………....

131,000

Paid back in year 3 ………………………………………………………………..……..

$ 19,000

= = 0.265

Payback period = 2 + 0.265 = 2.265 years

Amount paid back in year 3

Net cash flows in year 3

$19,000

$71,600

Exercise 24-3 (20 minutes)

a.

Payback period = = = 2.21 years

where

Annual after-tax income ………………………………………………………………..

$150,000

Plus depreciation* …………………………………………………………………….…..

85,000

Annual net cash flow ………………………………………………………………..…..

$235,000

*Annual depreciation = = $85,000

b.

Annual after-tax income ………………………………………………………………..

$ 60,000

Plus depreciation* …………………………………………………………………….…..

45,000

Annual net cash flow ………………………………………………………………..…..

$105,000

Exercise 24-4 (15 minutes)

Cost of investment

Annual net cash flow

$520,000

$235,000

$520,000 – $10,000

6

Exercise 24-5 (20 minutes)

COMPUTING NET CASH FLOWS FROM NET INCOME

Net income

Cash flows

Sales ……………………………………………………………….…….

$225,000

$225,000

Materials, labor & overhead ……………………………..…….

120,000

120,000

Depreciation ……………………………………………………….

30,000

Selling and administrative ……………………………….…….

22,500

22,500

Pretax income ……………………………………………………….

52,500

Income taxes (30%) ……………………………………………….

15,750

15,750

Net income ……………………………………………………….

$ 36,750

Net cash flows ……………………………………………………….

$ 66,750

2. Accounting rate of return = = 20.42%

*Average investment

Cost ……………………………………………………….

$360,000

Salvage ……………………………………………………

0

Sum ……………………………………………………….

$360,000

Average (Sum/2) …………………………..………..…

$180,000

Exercise 24-6 (20 minutes)

Annual

Net Cash

Flows

Present

Value of

Annuity at

8%

Present

Value of

Net Cash

Flows

Years 1 through 6…………………………………..……..

$ 66,750

4.6229

$ 308,579

Amount to be invested …………………………..

(360,000)

Net present value of investment …………….……..

$ (51,421)

Based on this net present value analysis, the investment is not acceptable.

$360,000

$66,750

$36,750

$180,000*

Exercise 24-7 (35 minutes)

1.

PROJECT C1

Net Cash

Flows

Present

Value of 1

at 12%

Present

Value of Net

Cash Flows

Year 1 …………………………..……………………….….

$ 12,000

0.8929

$ 10,715

Year 2 …………………………..……………………….….

108,000

0.7972

86,098

Year 3 …………………………..……………………….….

168,000

0.7118

119,582

Totals ……………………………………………………….

$288,000

$216,395

Amount invested …………………………………………..

(228,000)

Net present value …………………………………..……..

$ (11,605)

PROJECT C2

Net Cash

Flows

Present

Value of 1

at 12%

Present

Value of Net

Cash Flows

Year 1 …………………………..……………………….….

$ 96,000

0.8929

$ 85,718

Year 2 …………………………..……………………….….

96,000

0.7972

76,531

Year 3 …………………………..……………………….….

96,000

0.7118

68,333

Totals ……………………………………………………….

$288,000

$230,582

Amount invested …………………………………………..

(228,000)

Net present value …………………………………..……..

$ 2,582

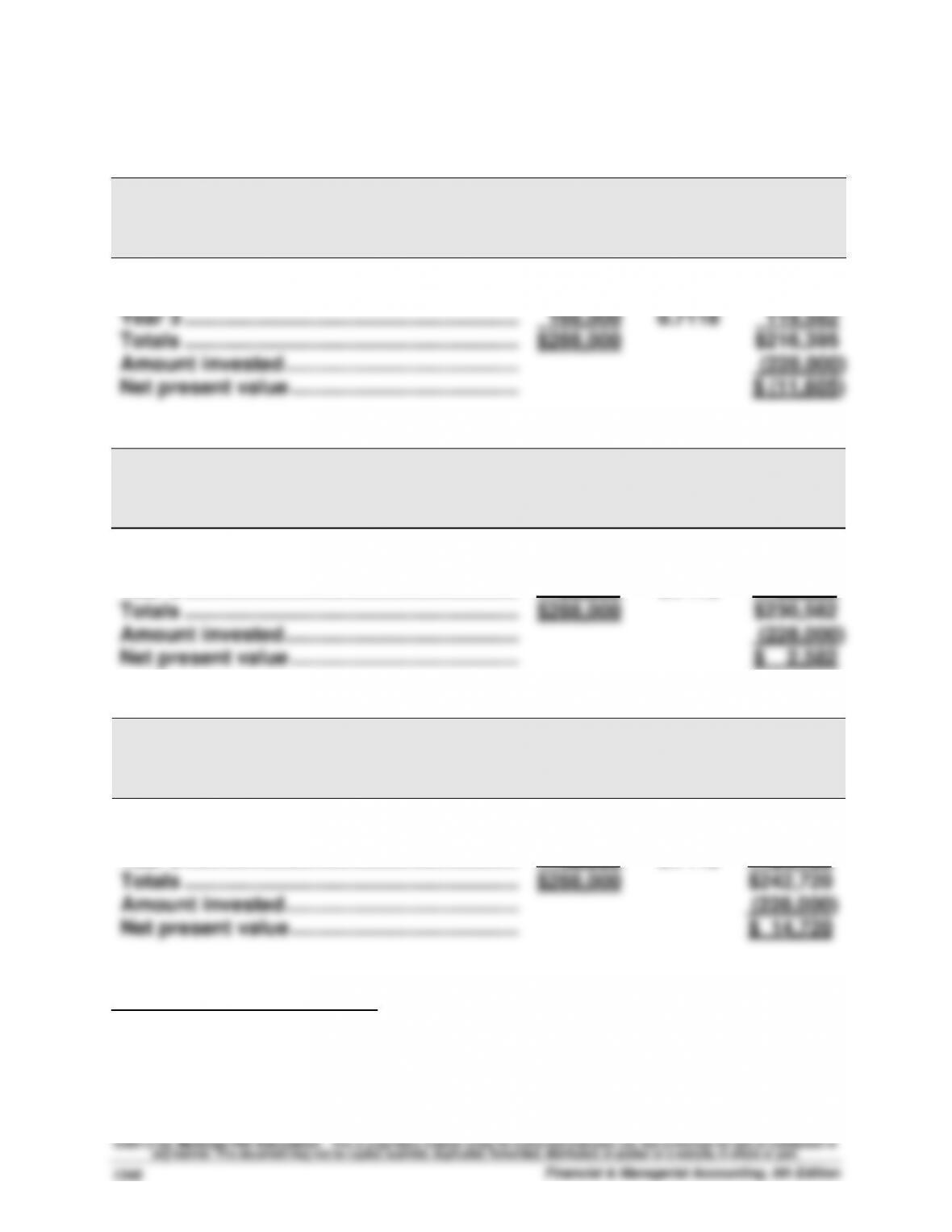

PROJECT C3

Net Cash

Flows

Present

Value of 1

at 12%

Present

Value of Net

Cash Flows

Year 1 ……………………………………………………….

$180,000

0.8929

$160,722

Year 2 ……………………………………………………….

60,000

0.7972

47,832

Year 3 ……………………………………………………….

48,000

0.7118

34,166

Totals ……………………………………………………….

$288,000

$242,720

Amount invested …………………………………………..

(228,000)

Net present value …………………………..……………..

$ 14,720

Analysis and Interpretation: Both Project C2 and C3 yield a positive net

present value. Accordingly, both C2 and C3 are acceptable investments.

Exercise 24–7 (Continued)

2. INTERNAL RATE OF RETURN VS. NET PRESENT VALUE FOR C2

3. INTERNAL RATE OF RETURN FOR PROJECT C2

(i) Present value factor = Amount invested / Net cash flows

Financial & Managerial Accounting, 5th Edition

1350

Exercise 24-8 (20 minutes)

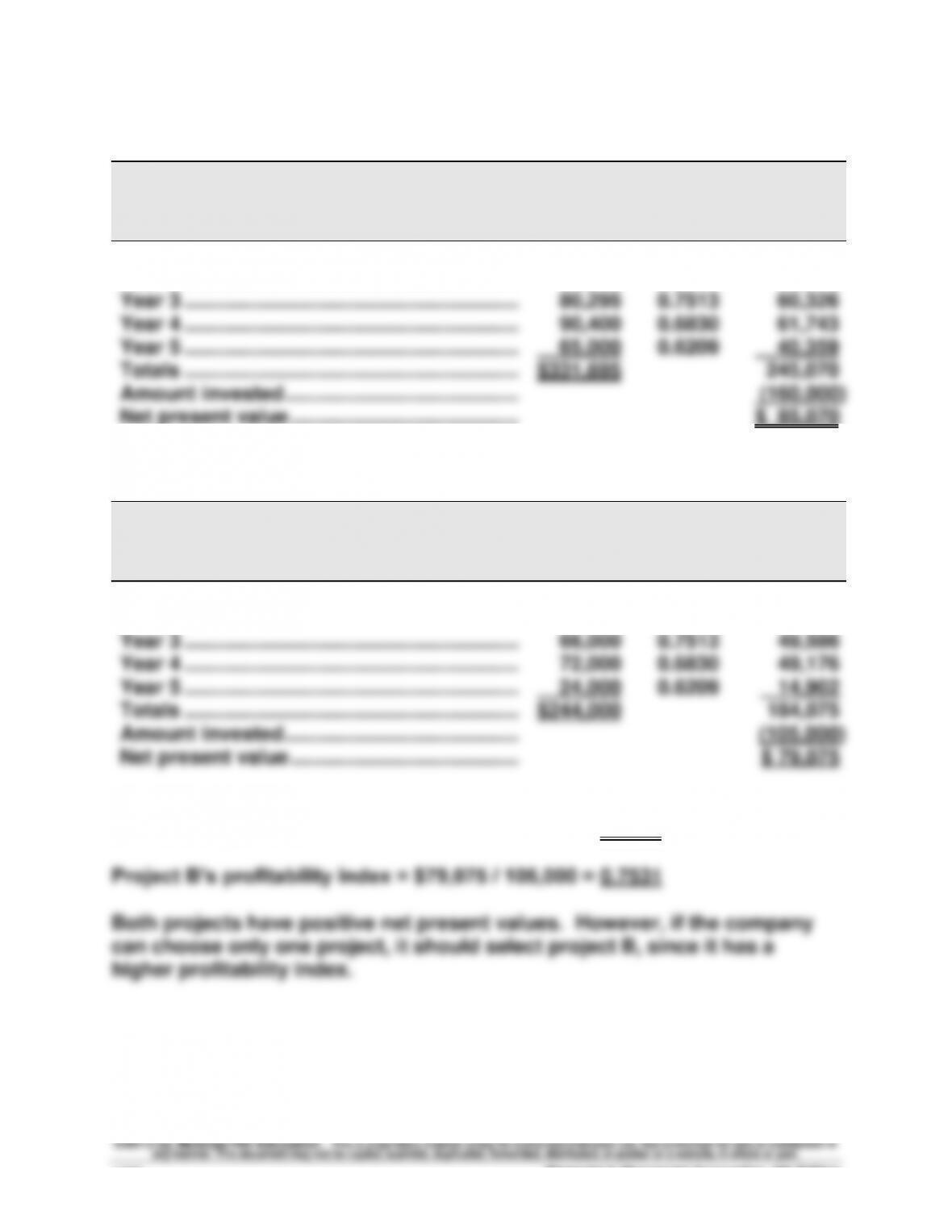

PROJECT A

Net Cash

Flows

Present

Value of 1

at 10%

Present

Value of Net

Cash Flows

Year 1 …………………………..……………………….….

$ 40,000

0.9091

$ 36,364

Year 2 …………………………..……………………….….

56,000

0.8264

46,278

Year 3 …………………………..……………………….….

80,295

0.7513

60,326

Year 4 …………………………..……………………….….

90,400

0.6830

61,743

Year 5 …………………………..……………………….….

65,000

0.6209

40,359

Totals ……………………………………………………….

$331,695

245,070

Amount invested …………………………………………..

(160,000)

Net present value …………………………………..……..

$ 85,070

PROJECT B

Net Cash

Flows

Present

Value of 1

at 10%

Present

Value of Net

Cash Flows

Year 1 …………………………..……………………….….

$ 32,000

0.9091

$ 29,091

Year 2 …………………………..……………………….….

50,000

0.8264

41,320

Year 3 …………………………..……………………….….

66,000

0.7513

49,586

Year 4 …………………………..……………………….….

72,000

0.6830

49,176

Year 5 …………………………..……………………….….

24,000

0.6209

14,902

Totals ……………………………………………………….

$244,000

184,075

Amount invested …………………………………………..

(105,000)

Net present value …………………………………..……..

$ 79,075

Project A’s profitability index = $85,070 / 160,000 = 0.5317

Exercise 24-9A (20 minutes)

Using Excel, Project A (B) has an internal rate of return of 26.96 (35.00%).

Project A Project B

A

B

C

D

1

Initial investment

–160000

–105000

2

Annual cash flows,

end of period

3

1

40000

32000

4

2

56000

50000

5

3

80295

66000

6

4

90400

72000

7

5

65000

24000

8

Formula for IRR

=IRR(C1:C7)

=IRR(D1:D7)

Exercise 24-10 (15 minutes)

1. Recovery time computation

Payback Period

Break-Even Time

$90,000 / $35,000 = 2.57 years

3.2 years (see answer for QS 24-8)

2. The advantage of break-even time is that it considers the time value of

3. When (1) the interest rate is very low, 1% for example, and (2) the

PROBLEM SET A

Problem 24-1A (50 minutes)

Part 1

Part 2

Net

Net Cash

Income

Flow

Expected annual sales of new product ……………...

$1,840,000

$1,840,000

Expected costs of new product

Direct materials ……………………………………………...

(480,000)

(480,000)

Direct labor …………………………………………………....

(672,000)

(672,000)

Overhead excluding depr. on new asset ………....

(336,000)

(336,000)

Depreciation on new asset ……………………………..

(115,000)

Selling and administrative expenses ……………....

(160,000)

(160,000)

Income before taxes ………………………………………....

77,000

Income taxes (30%) …………………………………………..

(23,100)

(23,100)

Net income ……………………………………………………….

$ 53,900

Net cash flow* …………………………………………………..

$ 168,900

* Alternatively, annual net cash flow can be computed as

Net income + Depreciation = $53,900 + $115,000 = $168,900

Part 3

Problem 24-1A (Continued)

Part 4

* Average investment

Asset cost ………………………………………………………………..……..

$480,000

Final year’s book value ……………………………………………..……..

20,000

Sum ………………………………………………………………………………..

$500,000

Average (Sum /2) ……………………………………………………….

$250,000

Part 5

Present Value of Net Cash Flows

Present

Present

Net Cash

Value of

Value of Net

Flows

1 at 7%

Cash Flows

Year 1 …………………………..………………….….

$168,900

0.9346

$ 157,854

Year 2 …………………………..………………….….

168,900

0.8734

147,517

Year 3 …………………………..………………….….

168,900

0.8163

137,873

Year 4* ……………………………………………..….

188,900

0.7629

144,112

Totals ………………………………………………….

$695,600

587,356

Amount invested ………………………………….

(480,000)

Net present value ……………………………..….

$ 107,356

* Year 4’s cash flow includes the $20,000 salvage value.

$250,000*