Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 23-3B (30 minutes)

Part 1

INCREMENTAL COST OF MAKING TH1

Variable costs:

Direct materials (400,000 units x $1.20 per unit) ................................

$ 480,000

Direct labor (400,000 units x $1.50 per unit) ................................

600,000

Variable overhead (2,400,000* x 25%) .....................................................

600,000

Total incremental cost of making 50,000 units ................................

$1,680,000

* Total overhead = 400,000 units x $6 per unit = $2,400,000

INCREMENTAL COST OF BUYING THE PART

Cost per unit to buy .....................................................................................

$ 4.00

Total incremental cost of buying 400,000 units ................................

$1,600,000

Alto is better off buying the TH1 from the outside supplier.

Part 2

Other factors Alto should consider besides cost are:

Problem 23-4B (45 minutes)

Alternative 1: Sell to a wholesaler

Problem 23-5B (55 minutes)

Part 1

Product R

Product T

Selling price per unit .....................................................

$ 60

$ 80

Variable costs per unit ..................................................

20

45

Contribution margin per unit ........................................

$ 40

$ 35

Machine hours to produce 1 unit ................................

0.4

1.0

Contribution per machine hour

(or contribution/[hours per unit]) ..............................

$100

$ 35

Part 2

Sales Mix Recommendation To the extent allowed by production and

market constraints, the company should produce as much of Product R as

possible. With a single shift yielding 176 hours per month (8 x 22), the

company can produce these units of Product R:

Contribution Margin at Recommended Sales Mix

Problem 23-5B (Continued)

Part 3

Sales Mix Recommendation with Second Shift If the second shift is added,

the maximum possible output of R will double:

However, this level of output exceeds the company’s market constraint of

550 units of Product R per month. This means the company should

produce 550 units of Product R, and commit the remainder of the

productive capacity to Product T. This is computed as follows:

Problem 23-5B (Continued)

Part 4

Sales Mix Recommendation By incurring additional marketing cost, the

company can relax the market constraint for sales of Product R up to the

point where 675 units can be sold. This means the company can produce

675 units of Product R, and commit the remainder of its productive

capacity to Product T. These computations are:

Financial & Managerial Accounting, 5th Edition

1326

Problem 23-6B (60 minutes)

Part 1

ESME COMPANY

Analysis of Expenses under Elimination of Department Z

Total

Eliminated

Continuing

Expenses

Expenses

Expenses

Cost of goods sold ..............................................

$586,400

$125,100

$461,300

Direct expenses

Advertising .........................................................

30,000

3,000

27,000

Store supplies used ...........................................

7,000

1,400

5,600

Depreciation of store equip. .............................

21,000

21,000

Allocated expenses

Sales salaries* ....................................................

93,600

46,800

46,800

Rent expense......................................................

27,600

27,600

Bad debts expense ............................................

25,000

4,000

21,000

Office salary* ......................................................

26,000

26,000

Insurance expense* ...........................................

5,600

910

4,690

Miscellaneous office expenses* .......................

4,200

750

3,450

Total expenses .....................................................

$826,400

$181,960

$644,440

Problem 23-6B (Continued)

Part 2

ESME COMPANY

Forecasted Annual Income Statement

Under Plan to Eliminate Department Z

Sales ......................................................................................................

$700,000

Cost of goods sold ..............................................................................

461,300

Gross profit from sales .......................................................................

238,700

Operating expenses

Advertising .........................................................................................

27,000

Store supplies used ..........................................................................

5,600

Depreciation of store equipment .....................................................

21,000

Sales salaries .....................................................................................

59,800*

Rent expense .....................................................................................

27,600

Bad debts expense ............................................................................

21,000

Office salary .......................................................................................

13,000*

Insurance expense ............................................................................

4,690

Miscellaneous office expenses ........................................................

3,450

Total operating expenses ...................................................................

183,140

Net income ............................................................................................

$ 55,560

* Office salary reassignment

Total

Sales

Office

Salaries

Salaries

Salary

Sales clerks ................................................................

$46,800

$46,800

Office clerk ................................................................

26,000

$26,000

Reassign office clerk to sales ................................

0

13,000

(13,000)

Revised salaries................................................................

$72,800

$59,800

$13,000

Financial & Managerial Accounting, 5th Edition

1328

Problem 23-6B (Continued)

Part 3

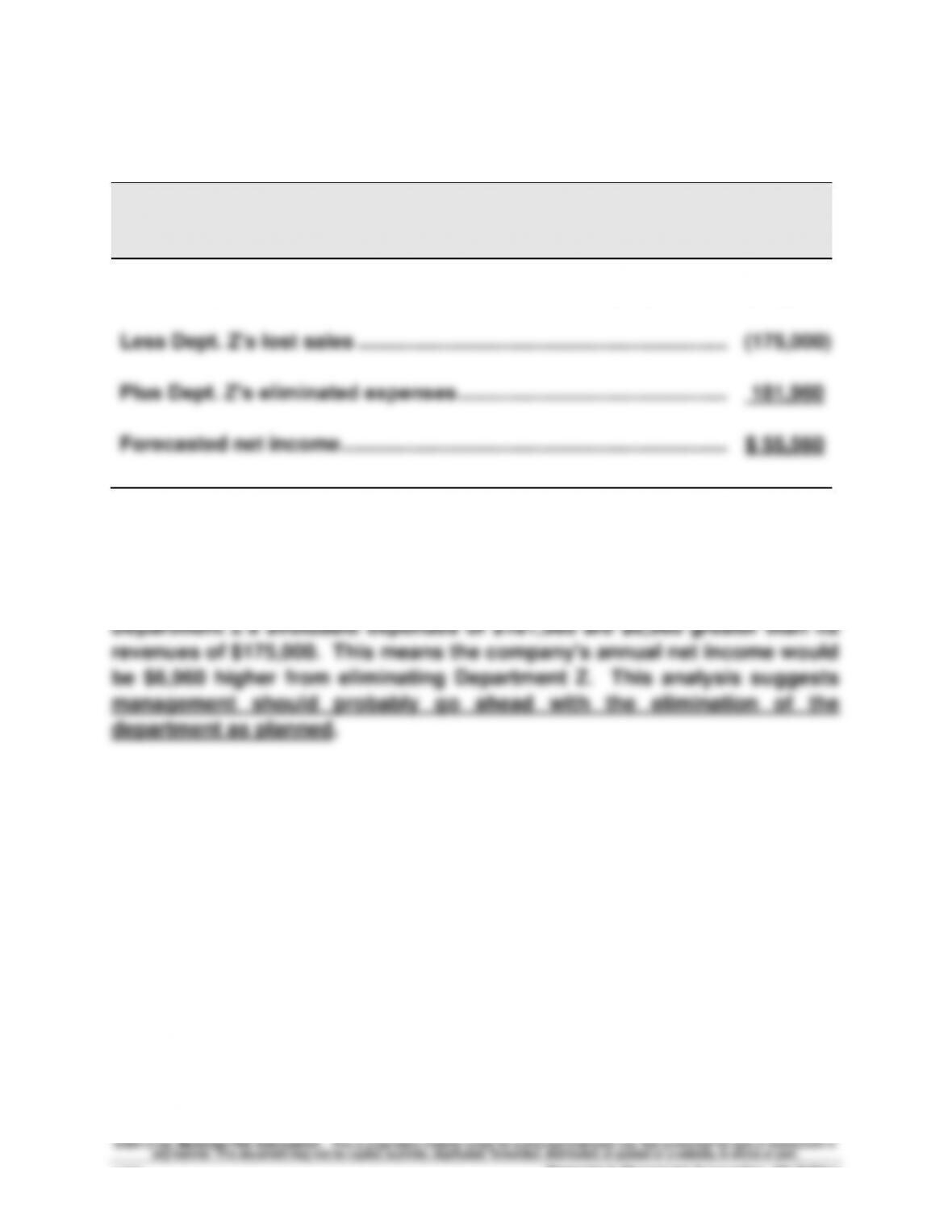

ESME COMPANY

Reconciliation of Combined Income with Forecasted Income

Combined net income ...........................................................................

$ 48,600

Less Dept. Z's lost sales ........................................................................

(175,000)

Plus Dept. Z’s eliminated expenses ......................................................

181,960

Forecasted net income ...........................................................................

$ 55,560

ANALYSIS

SERIAL PROBLEM — SP 23

Serial Problem, Success Systems (50 minutes)

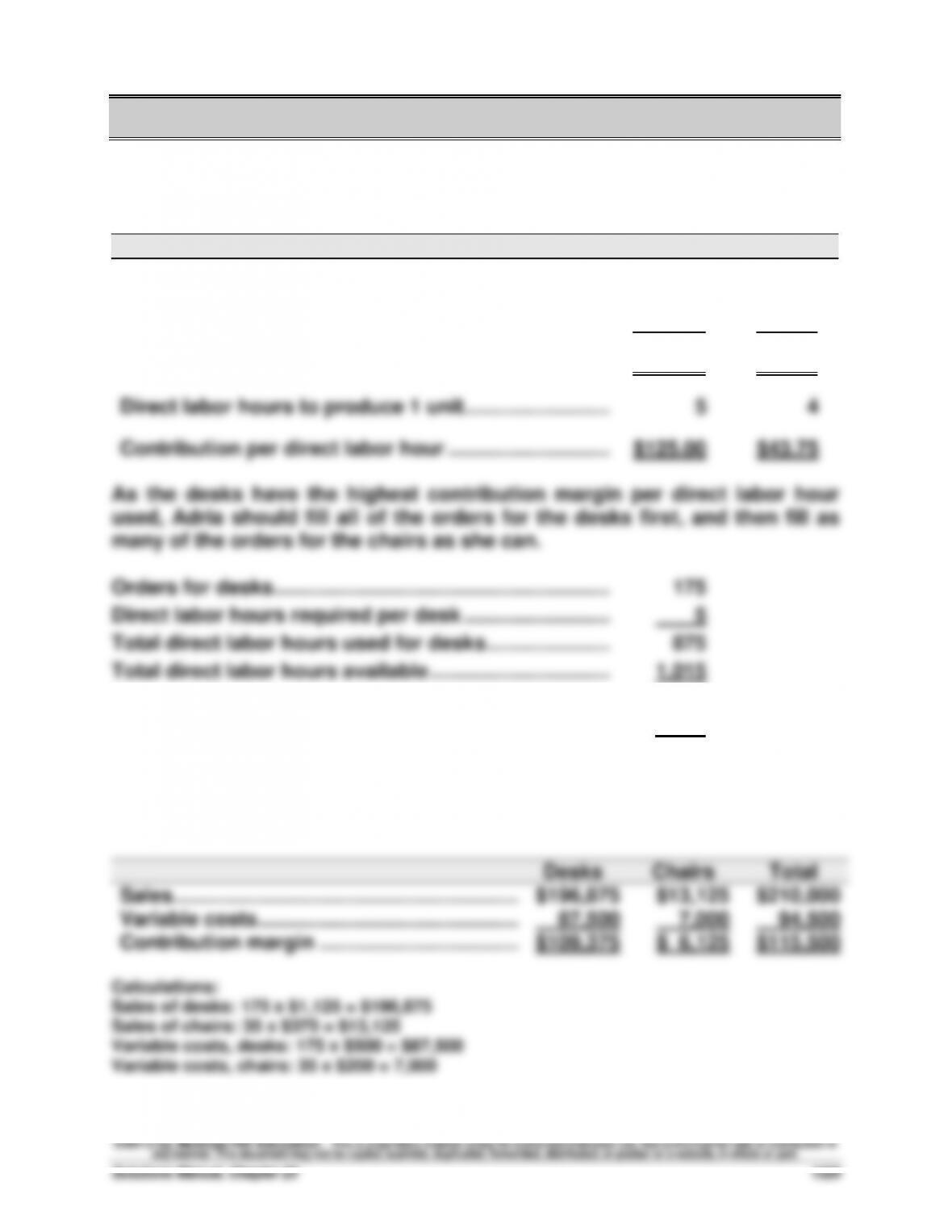

Desks

Chairs

Selling price per unit ...............................................................

$ 1,125

$ 375

Variable costs per unit ............................................................

500

200

Contribution margin per unit ..................................................

$ 625

$ 175

Direct labor hours to produce 1 unit ................................

5

4

Contribution per direct labor hour ................................

$125.00

$43.75

As the desks have the highest contribution margin per direct labor hour

used, Adria should fill all of the orders for the desks first, and then fill as

many of the orders for the chairs as she can.

Orders for desks ................................................................

175

Direct labor hours required per desk ................................

5

Total direct labor hours used for desks ................................

875

Total direct labor hours available ................................

1,015

Hours available to produce chairs................................

140

Direct labor hours required per chair ................................

4

Chairs that can be produced in that time ..............................

35

Therefore, Adria should produce 175 desks and 35 chairs. Her contribution

margin for that level is:

Desks

Chairs

Total

Sales ................................................................

$196,875

$13,125

$210,000

Variable costs.......................................................

87,500

7,000

94,500

Contribution margin ............................................

$109,375

$ 6,125

$115,500

Calculations:

Sales of desks: 175 x $1,125 = $196,875

Sales of chairs: 35 x $375 = $13,125

Variable costs, desks: 175 x $500 = $87,500

Variable costs, chairs: 35 x $200 = 7,000