Problem 22-5B (60 minutes)

Part 1

Process time ……………………………………………………………………

16.0 hours

Inspection time ……………………………………………………………..…

3.5 hours

Move time ……………………………………………………………………..…

9.0 hours

Wait time …………………………………………………………………………

21.5 hours

Manufacturing cycle time …………………………………………………

50.0 hours

Part 2

Manufacturing cycle efficiency (16.0 hours/ 50.0 hours) ……

0.32

Part 3

To increase the manufacturing cycle efficiency to 0.80 Best Ink needs to

reduce the total manufacturing cycle time to 20 hours without changing the

Financial & Managerial Accounting, 5th Edition

1286

Problem 22-6B (45 minutes)

Part 1

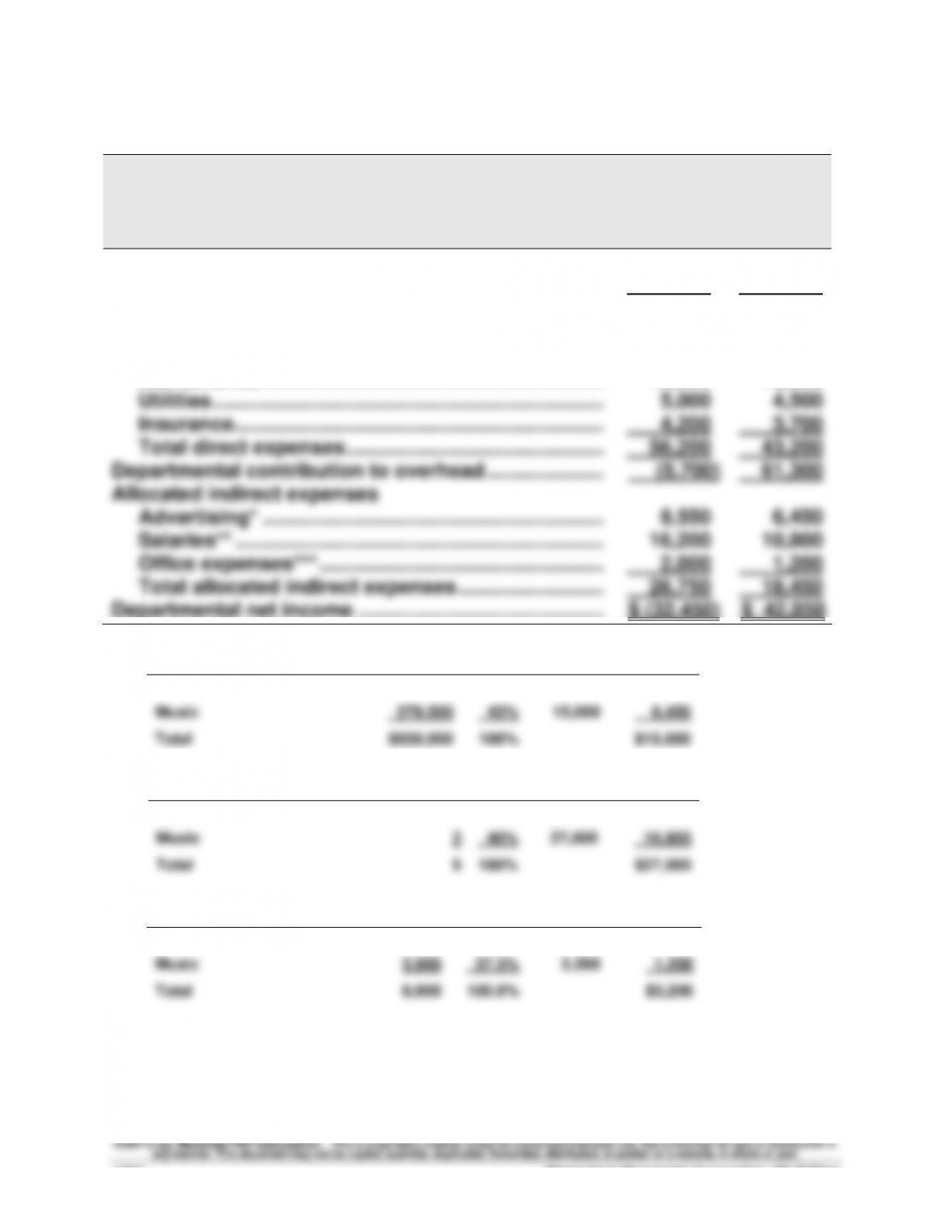

Sadar Company

Departmental Income Statements

Department

Videos

Music

Sales ……………………………………………………………………

$370,500

$279,500

Cost of goods sold ……………………………………………….

320,000

175,000

Gross margin ……………………………………………………….

50,500

104,500

Direct expenses

Salaries ……………………………………………………………

35,000

25,000

Maintenance …………………………………………………….

12,000

10,000

Utilities …………………………………………………………….

5,000

4,500

Insurance …………………………………………………………

4,200

3,700

Total direct expenses ……………………………………….

56,200

43,200

Departmental contribution to overhead …………………

(5,700)

61,300

Allocated indirect expenses

Advertising* …………………………………………………….

8,550

6,450

Salaries** …………………………………………………………

16,200

10,800

Office expenses*** ……………………………………………

2,000

1,200

Total allocated indirect expenses ……………………..

26,750

18,450

Departmental net income ……………………………………..

$ (32,450)

$ 42,850

*

Advertising allocation:

Sales

%

Amount

Allocated

Videos

$370,500

57%

$15,000

$ 8,550

Music

279,500

43%

15,000

6,450

Total

$650,000

100%

$15,000

**

Salaries allocation:

Employees

%

Amount

Allocated

Videos

3

60%

$27,000

$16,200

Music

2

40%

27,000

10,800

Total

5

100%

$27,000

***

Office expenses allocation:

Sq. ft.

%

Amount

Allocated

Videos

5,000

62.5%

$3,200

$2,000

Music

3,000

37.5%

3,200

1,200

Total

8,000

100.0%

$3,200

P

Problem 22-6B (Concluded)

Part 2

The video department has both a negative contribution to overhead and a

negative departmental net income. It is not even covering its own direct costs,

Financial & Managerial Accounting, 5th Edition

1288

SERIAL PROBLEM — SP 22

Serial Problem, Success Systems (20 minutes)

1. The balance scorecard is a system of performance measures that

requires managers to think of their company from four perspectives:

Customer, internal process, innovation and learning, and financial.

2. Below are some examples of balanced scorecard measures that

Adria could use. Other examples are possible:

Customer: Percentage of computer workstations returned, number of

on-time workstation deliveries, number of on-time

computer system installations, customer satisfaction

survey ratings, number of new customers acquired.

Reporting in Action — BTN 22–1

1. Polaris revenues by product line

($ thousands)

December

31, 2011

December

31, 2010

December

31, 2009

Total revenues ………………………………………

$2,656,949

$1,991,139

$1,565,887

Off-Road Vehicles* (69%) ………………………

1,833,296

1,373,886

1,080,462

Snowmobiles (11%) ………………………………

292,264

219,025

172,248

On-Road Vehicles (5%) ……………………….…

132,847

99,557

78,294

Parts, Garments & Accessories (15%) ……

398,542

298,671

234,883

* Revenue rounded up so product line total revenues sum to total revenues of $2,656,949.

2. Polaris can divide up the operating expenses into product line direct

and indirect expenses. Some of the direct expenses of a particular

Financial & Managerial Accounting, 5th Edition

1290

Comparative Analysis — BTN 22-2

($ in thousands)

1. Profit margin = Net income/Sales

Polaris = $227,575 / $2,656,949 = 8.6%

2. Investment turnover = Investment center sales

Investment center average assets

3. Polaris’s profit margin (8.6%) is higher than Arctic Cat’s (2.8%).

Ethics Challenge — BTN 22-3

1. There is an ethical concern in this situation. Pincus is taking actions

she would not otherwise take. She believes that “minor compromises”

in her behavior do not significantly affect clients. However, the

2. Given that Pincus is aware of her behavior, its potential consequences,

and the source of what’s behind her behavior (in this case the focus by

management on meeting the quarterly responsibility performance

budget), she can approach her superiors (at least one or two she

3. Senior Security (the employer) is ultimately responsible for any action

taken by its employees, including Pincus. Management must establish

an ethical code of conduct to ensure that department managers do not

suggest some revision in the system to mitigate this trade–off.

Financial & Managerial Accounting, 5th Edition

1292

Communicating in Practice — BTN 22-4

Sample solution

MEMORANDUM

TO: Name, Store Manager

FROM: Your Name, National Office Manager

SUBJECT: New Performance Reporting

DATE: Current Date

All current and future periods’ performance reports for all managers

include an allocation of home office expenses. These expenses will be

assigned as a percent of store sales.

Taking It to the Net — BTN 22-5

Instructor note: The objective of this assignment is for students to be exposed to the

different accounting and business applications with spreadsheets.

1. The tutorials identified and read by the students will vary. For example,

2. Student responses regarding the usefulness of spreadsheets will

depend on the tutorials accessed. For example, the tutorial “Return on

Investment and Return on Equity Business Model” shows how a

Teamwork in Action — BTN 22–6

1. The student must make decisions about geographic area, type of

business segment, and reporting structure. The objective is to have

2. Having comparable responsibility accounting reports is necessary to

reliably compare performance within a company (and across different

companies). Differences in performance reports can substantially

Financial & Managerial Accounting, 5th Edition

1294

Entrepreneurial Decision — BTN 22-7

1. Departmental income statements can be prepared for each department

once expenses have been allocated to it. The expenses will include both

2. If the indirect expenses are a large portion of total expenses, a

departmental income statement might not be the best measure of each

department’s performance. While the department’s income or loss is

department is helping to cover the indirect expenses.

3. United By Blue could use ratings from customer satisfaction surveys,

the number of repeat customers, the percentage of orders returned, and

Hitting the Road — BTN 22-8

1. [Student answers will vary for part (1).] One suggested responsibility

accounting reporting framework is to have (1) concessions and (2)

2. One suggested proposal is

Expense

Allocation Basis

Heat ………………………….

Square footage occupied

Rent ………………………….

Sales dollars

Insurance ………………….

Square footage occupied

Maintenance …….……….

Time in process—with a standard time to clean a

theater after a show

Global Decision — BTN 22-9

1. Net sales percentage growth [non-percents in € thousands]

Segment

Net sales % change from 2010 to 2011

Two-wheeler …………………………..

(€1,025.3 – €988.1) / €988.1 = 3.8%

Commercial Vehicles ………………….

(€491.1 – €497.3) / €497.3 = -1.2%

2. Percentage growth in net sales is higher in the Two-wheeler segment

(3.8% increase) than in the Commercial Vehicles segment (-1.2%

decrease).

3. The Two–wheeler segment earned more gross margin (profit) in both

4. Piaggio’s management can use this information to help establish long–

term goals and strategies and for resource allocation decisions. An

important factor in the valuation of any company is its ability to grow