Chapter 22 Decentralization and Performance Evaluation

Chapter 22

Decentralization and

Performance Evaluation

Related Assignment Materials

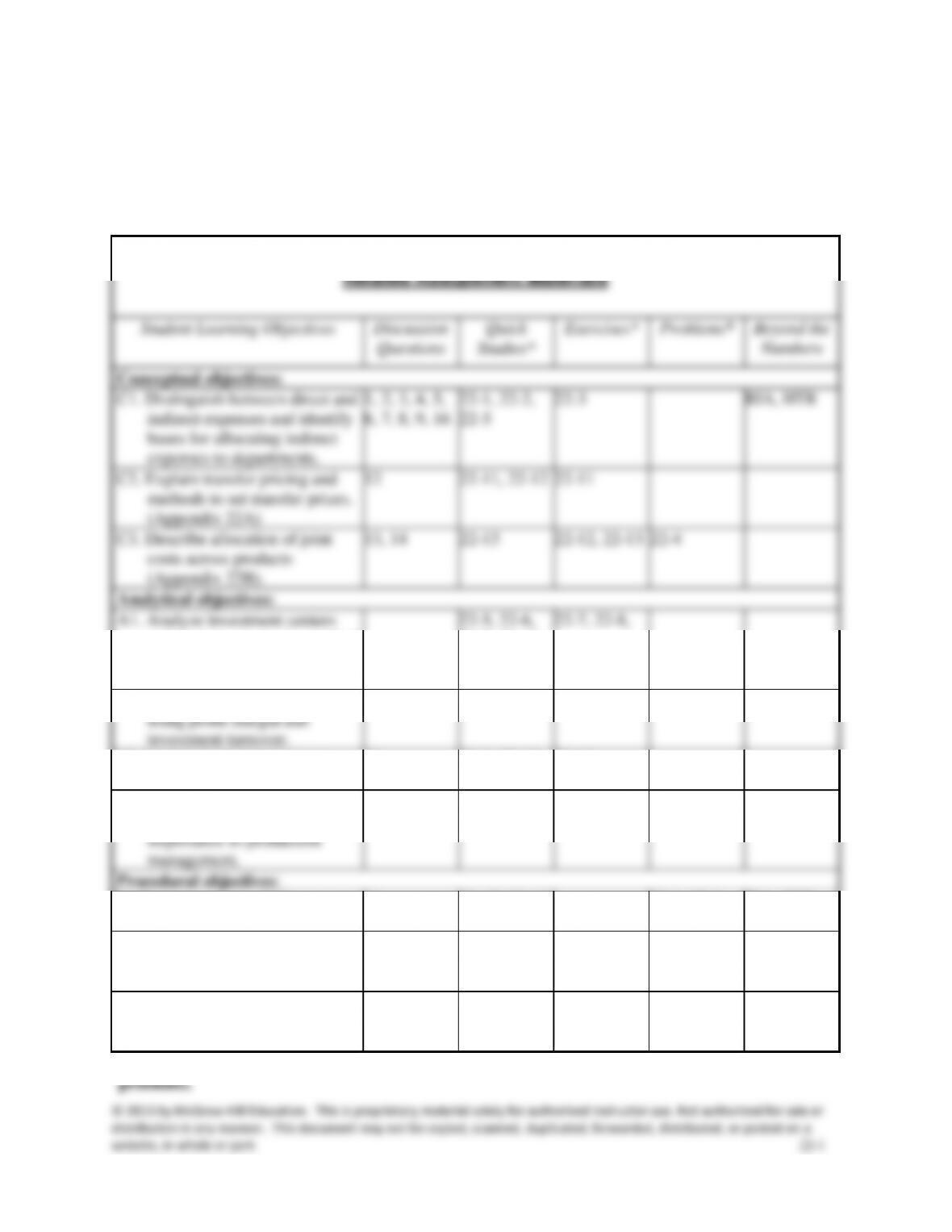

Student Learning Objectives

Discussion

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Distinguish between direct and

indirect expenses and identify

bases for allocating indirect

expenses to departments.

1, 2, 3, 4, 5,

6, 7, 8, 9, 16

22-1, 22-2,

22-3

22-3

RIA, HTR

C2. Explain transfer pricing and

methods to set transfer prices.

(Appendix 22A)

12

22-11, 22-12

22-11

C3. Describe allocation of joint

costs across products

(Appendix 22B).

13, 14

22-13

22-12, 22-13

22-4

Analytical objectives:

A1. Analyze investment centers

using return on assets, residual

income, and balanced

scorecard.

22-5, 22-6,

22-8, 22-15

22-7, 22-8,

A2. Analyze investment centers

using profit margin and

investment turnover.

15

22-7, 22-8

22-9, 22-14

CA

A3. Analyze investment centers

using the balance scorecard.

18

22-9, 22-10

22-10

A4. Compute cycle time and cycle

efficiency, and explain their

importance to production

management.

17, 19, 20

22-16

22-5

Procedural objectives:

P1. Prepare a responsibility report

for a cost center.

11

22-17, 22-18,

22-19

22-1, 22-3,

22-6

TIA, HTR

P2. Allocate indirect expenses to

departments.

22-14

22-1, 22-2,

22-4, 22-5,

22-6

CIP, TTN

P3. Prepare departmental income

statements and contribution

reports.

10

22-3, 22-4,

22-3

22-1, 22-2,

22-3

EC, ED, GD

*See additional information on next page that pertains to these quick studies, exercises and

website, in whole or part. 22-3

5. Service departments provide support to an organization’s

operating departments and do not generate revenues.

B. Departmental Evaluation

1. Prepared for internal managers to help control operations,

responsibility of each operating department.

a. Profit center⎯incurs costs and generates revenues (e.g.

selling department).

b. Cost center⎯incurs cost or expenses without directly

generating revenues (e.g. manufacturing department).

c. Investment center – incurs costs and generates revenues

and is responsible for effectively using center assets.

C. Controllable versus Uncontrollable Costs

2. Controllable versus Direct Costs⎯ direct costs are readily

traced to a department, but may not be under control of

department manager. All costs are controllable at some level of

activities in terms of controllable costs in which a manager has

the power to determine or significantly affect the amount

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

be readily traced to one department.

2. Allocated across departments benefiting from them.

3. Ideally allocated using a cause-effect relation or, if cause-

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a

website, in whole or part. 22-6

IV. Evaluating Investment Center Performance—financial and

nonfinancial measures of investment center performance.

center managers are typically evaluated using performance

measures that combine income and assets.

evaluate division performance is the investment center

residual income computed as investment center net

income minus target investment center net income.

company answers these questions:

a. How do you compute average invested assets?

4. Investment Center Profit Margin and Investment Turnover

a. Profit margin measures the income earned per dollar of

converted into sales.

c. Higher profit margin and investment turnover indicates

better performance.

Return on investment=Profit margin x Investment turnover.

Investment center net income / Investment center average

assets = (Investment center net income/Investment center

sales) x (Investment center sales/Investment center average

assets)

website, in whole or part. 22-7

Chapter 22 Decentralization and Performance Evaluation

website, in whole or part. 22-8

Chapter Outline

a. Alternative Transfer Prices—The manager of the division

providing the product, in general, would not want to use a

transfer price which is less than the product’s variable

manufacturing cost and the manager of the division receiving the

product would not want to use a transfer price which is greater

than selling price to outside customers (market value). A transfer

price between these two prices should be selected. A determining

factor is whether the department providing the product has excess

capacity to manufacture the product.

1. No Excess Capacity—a market-based transfer price is

preferred in this situation. With no excess capacity, the

manager providing the product will not accept a transfer price

less than the product’s selling price.

2. Excess Capacity—any price greater than variable

manufacturing cost is acceptable since it will recover some or

all of the fixed costs and increase its overall profits. This form

of transfer pricing is called cost-based transfer pricing.

3. Additional Issues in Transfer Pricing—additional issues

include:

rather than actual costs.

c. Division managers’ negotiation – the transfer price reflect

the negotiating skills of the respective division managers.

d. Nonfinancial factors—include quality control, reduced

to produce or purchase two or more products at the same time; similar

to indirect expense in that it’s shared across more than one cost object.

estimate the costs of individual products.

3. Financial statements prepared according to GAAP must assign

joint costs to products.

Notes

4. Allocation bases

Chapter 22 Decentralization and Performance Evaluation

website, in whole or part. 22-9

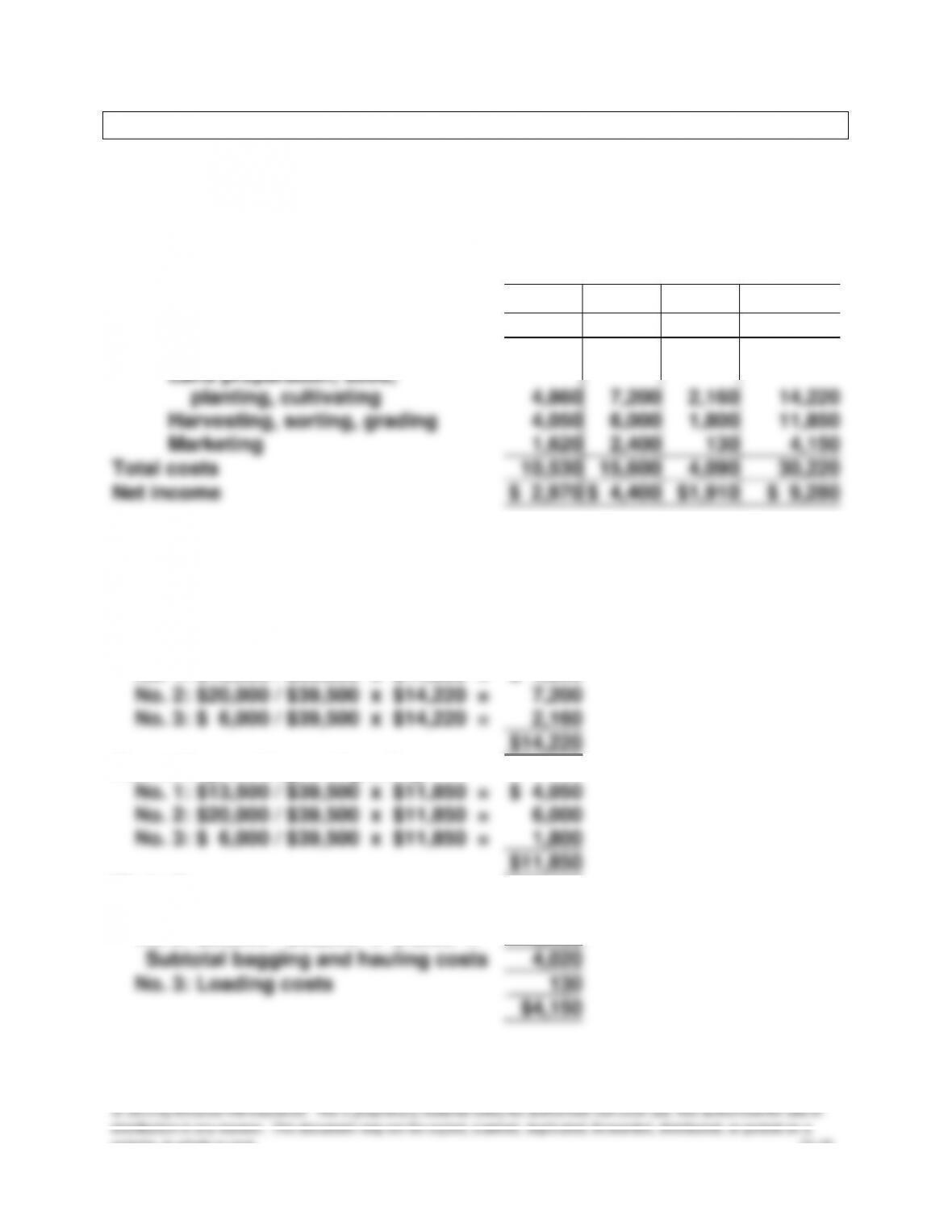

Chapter 22 Alternate Demonstration Problem #1

Jack and Susan Roberts own a farm that produces potatoes. Based on a

review of the income statement shown below, Jack remarked that they

should have fed the No. 3 potatoes to the pigs; then they would have

avoided the loss from the sale of the those potatoes.

JACK AND SUSAN ROBERTS

Income from the Production and Sale of Potatoes

For Year Ended December 31, 2013

Results by Grade

No. 1

No. 2

No. 3

Combined

Sales by grades:

No. 1, 300,000 lbs. $0.045 per lb.

$13,500

No. 2, 500,000 lbs. $0.04 per lb.

$20,000

No. 3, 200,000 lbs. $0.03 per lb.

$6,000

Combined

$39,500

Costs:

Land preparation, seed, planting,

cultivating @ $0.01422 per lb.

4,266

7,110

2,844

14,220

Harvesting, sorting, grading

@ $0.01185 per lb.

3,555

5,925

2,370

11,850

Marketing @ $0.00415 per lb.

1,245

2,075

830

4,150

Total costs

9,066

15,110

6,044

30,220

Net income (or loss)

$ 4,434

$ 4,890

$ (44)

$ 9,280

Jack and Susan divided their costs among the grades on a per pound

basis, because their records do not show cost per grade. However, their

records did show that $4,020 of the $4,150 of marketing costs represented

the cost of placing the No. 1 and No. 2 potatoes in bags and hauling them

to the warehouse of the produce buyer. Bagging and hauling costs were

the same for both grades. The remaining $130 represented the cost of

loading the No. 3 potatoes into the trucks of the potato starch factory that

bought these potatoes in bulk and picked them up at the farm.

Required:

Prepare an income statement that will better show the results of producing

and marketing each of the grades of potatoes.

Chapter 22 Decentralization and Performance Evaluation

website, in whole or part. 22–10

Solution: Chapter 22 Alternate Demonstration Problem #1

JACK AND SUSAN ROBERTS

Income from the Production and Sale of Potatoes

For Year Ended December 31, 2013

Results by Grade

No. 1

No. 2

No. 3

Combined

Revenue from sales:

$13,500

$20,000

$6,000

$39,500

Costs:

Land preparation, seed,

planting, cultivating

4,860

7,200

2,160

14,220

Harvesting, sorting, grading

4,050

6,000

1,800

11,850

Marketing

1,620

2,400

130

4,150

Total costs

10,530

15,600

4,090

30,220

Net income

$ 2,970

$ 4,400

$1,910

$ 9,280

COST ALLOCATIONS

Land preparation, seed, planting, and

cultivating:

No. 1: $13,500 / $39,500 x $14,220 =

No. 2: $20,000 / $39,500 x $14,220 =

No. 3: $ 6,000 / $39,500 x $14,220 =

$ 4,860

7,200

2,160

$14,220

Harvesting, sorting, and grading:

No. 1: $13,500 / $39,500 x $11,850 =

No. 2: $20,000 / $39,500 x $11,850 =

No. 3: $ 6,000 / $39,500 x $11,850 =

$ 4,050

6,000

1,800

$11,850

Marketing:

No. 1: $13,500 / $33,500 x $4,020 =

No. 2: $20,000 / $33,500 x $4,020 =

$1,620

2,400

Subtotal bagging and hauling costs

4,020

No. 3: Loading costs

130

$4,150