Problem 21–6BA (Continued)

Part 3 Overhead Variances

(a) Variable overhead

Preliminary computations

Actual variable overhead (given):

Indirect materials ………………………………………………..

$10,000

Indirect labor ……………………………………………………..

16,000

Power …………………………………………………………..…..

4,500

Maintenance ………………………………………………….…..

3,000

Total …………………………………………………………….…..

$33,500

Actual hours:

37,600

(given)

Standard hours:

36,000

(from part 2)

Variable overhead cost variances

Variable overhead cost incurred [given] ……………………….….

$33,500

Variable overhead cost applied [36,000 hrs. @ $1.00] ……………..

36,000

Variable overhead cost variance…………………………………..………..

$ 2,500 F

Variable Overhead Spending and Efficiency Variances

Actual Overhead

AH x AVR

AH x SVR

Applied Overhead

SH x SVR

37,600 x $1.00

36,000 x $1.00

hours per hr.

hours per hr.

$33,500

$37,600

$36,000

$4,100 F

(Spending variance)

$1,600 U

(Efficiency variance)

$2,500 F

(Total variable overhead variance)

Financial & Managerial Accounting, 5th Edition

1232

Problem 21–6BA (Continued)

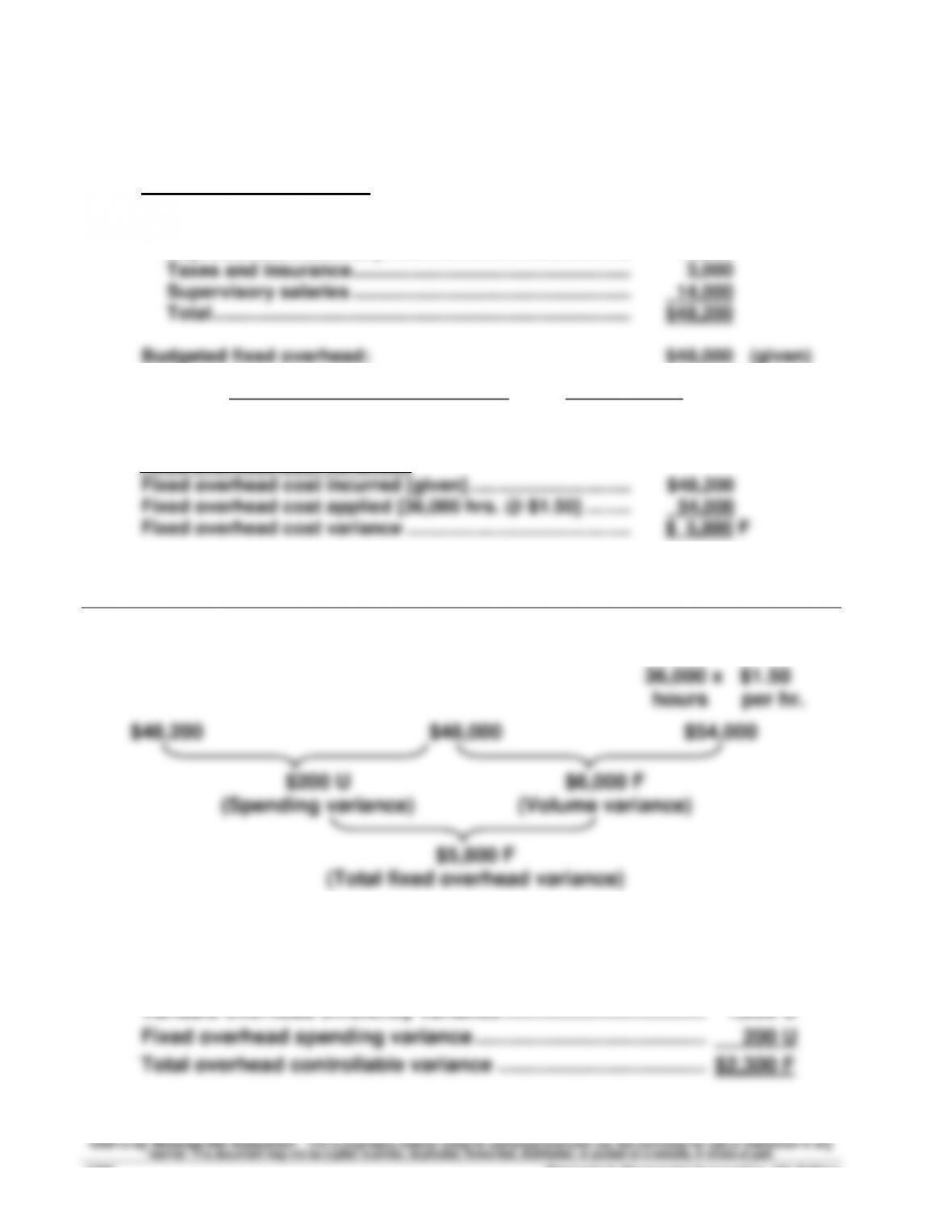

(b) Fixed overhead

Preliminary computations

Actual fixed overhead (given):

Rent of factory building ………………………………………..

$12,000

Depreciation, machinery ……………………………………....

19,200

Taxes and insurance …………………………………………....

3,000

Supervisory salaries …………………………………………....

14,000

Total …………………………………………………………………..

$48,200

Budgeted fixed overhead:

$48,000

(given)

Standard rate: = = $1.50 / hr

Fixed overhead cost variances

Fixed overhead cost incurred [given] …………………………..

$48,200

Fixed overhead cost applied [36,000 hrs. @ $1.50] ………………….

54,000

Fixed overhead cost variance …………………………………….………….

$ 5,800 F

Fixed Overhead Spending and Volume Variances

Actual Overhead

Budgeted Overhead

Fixed Overhead

Applied

36,000 x $1.50

hours per hr.

$48,200

$48,000

$54,000

$200 U

(Spending variance)

$6,000 F

(Volume variance)

$5,800 F

(Total fixed overhead variance)

(c) Total overhead controllable variance

Variable overhead spending variance ……………………………….…

$4,100 F

Variable overhead efficiency variance ……………………………….…

1,600 U

Fixed overhead spending variance ………………………………………

200 U

Total overhead controllable variance ………………………………..…

$2,300 F

Budgeted fixed overhead

Budgeted direct labor hours

$48,000

32,000 hours

Problem 21–6BA (Concluded)

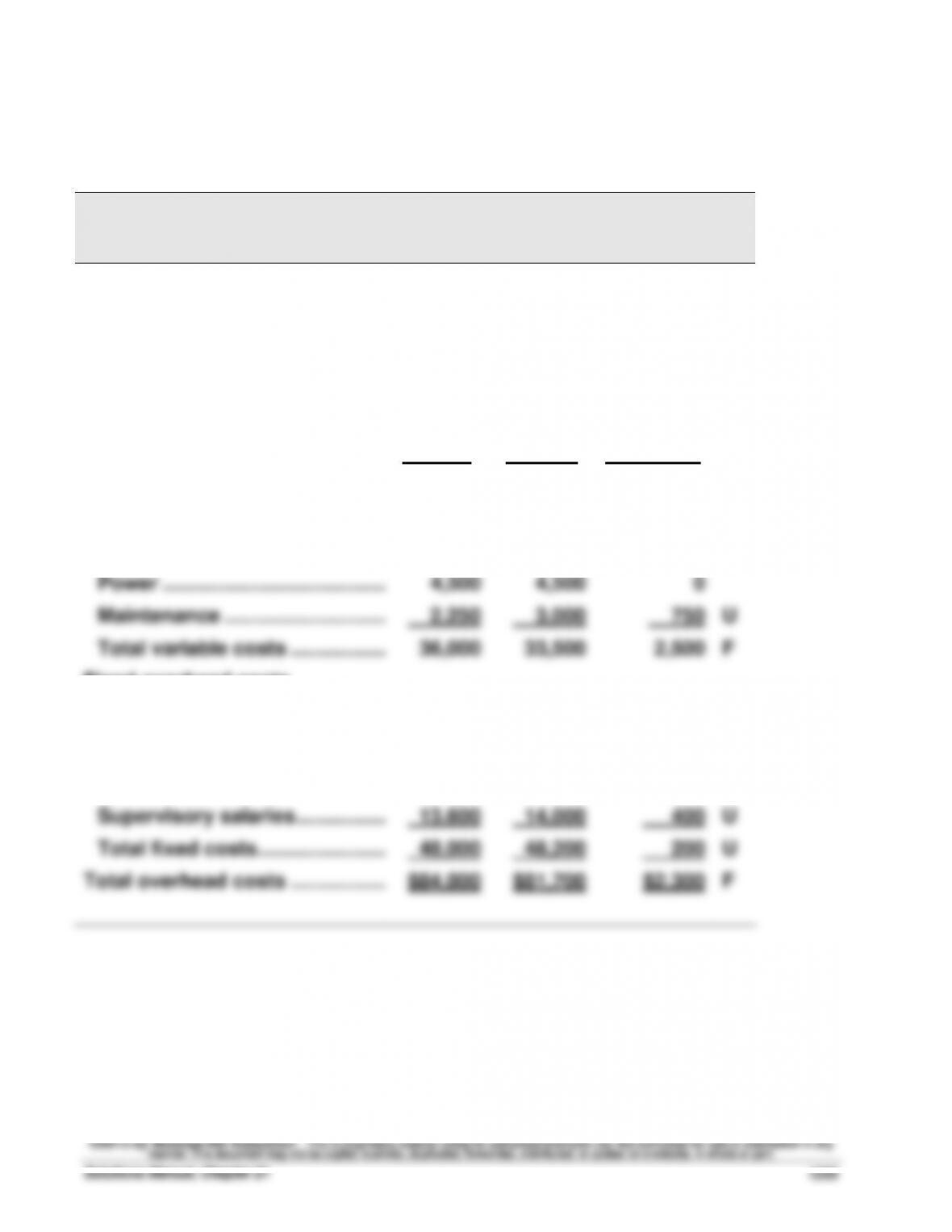

Part 4

GUADELUPE COMPANY

Overhead Variance Report

For Month Ended March 31

Volume Variance

Expected production level ……………………………………

80% of capacity

Production level achieved ……………………………………

90% of capacity

Volume variance …………………………………………….……

$6,000 (favorable)

Flexible

Actual

Controllable Variance

Budget

Results

Variances*

Variable overhead costs

Indirect materials ………………………

$11,250

$10,000

$1,250

F

Indirect labor ……………………….….

18,000

16,000

2,000

F

Power ………………………………….……

4,500

4,500

0

Maintenance ………………………..…

2,250

3,000

750

U

Total variable costs ……………..……

36,000

33,500

2,500

F

Fixed overhead costs

Rent of factory building ……….……

12,000

12,000

0

Depreciation—Machinery ……..……

20,000

19,200

800

F

Taxes and insurance …………………

2,400

3,000

600

U

Supervisory salaries …………….……

13,600

14,000

400

U

Total fixed costs…………………..……

48,000

48,200

200

U

Total overhead costs ……………..……

$84,000

$81,700

$2,300

F

* F = Favorable variance; and U = Unfavorable variance.

Problem 21–7BA (45 minutes)

Part 1

June 30*

Goods in Process Inventory …………………………..

130,000

Direct Materials Quantity Variance ……….………………….

5,000

Direct Materials Price Variance …………………………..

1,500

Raw Materials Inventory …………………………..

123,500

To record materials costs, including

the favorable quantity and

favorable price variances.

June 30

Goods in Process Inventory …………………………..

67,500

Direct Labor Rate Variance …………………………..

500

Direct Labor Efficiency Variance ………….……………….

3,000

Factory Payroll ……………………………………………………….

65,000

To record direct labor costs, including

the favorable efficiency variance and

unfavorable rate variance.

June 30

Goods in Process Inventory …………………………..

230,000

Controllable Variance ………………………………….………………….

8,000

Volume Variance ……………………………………………………….

12,000

Factory Overhead ……………………………….………………….

250,000

To record overhead costs, including

the unfavorable volume and unfavorable

controllable variances.

* Alternatively, some companies compute and record the price variance

when materials are purchased. This would yield two separate entries:

(1) Purchase of materials

Raw Materials Inventory…………………………..

125,000

Direct Materials Price Variance …………………………..

1,500

Accounts Payable …………………………….…………………………

123,500

(2) Issuance of materials into production

Goods in Process Inventory …………………..………

130,000

Direct Materials Quantity Variance …….…………………….

5,000

Raw Materials Inventory …………………………..

125,000

Problem 21–7BA (Concluded)

Part 2

Under management by exception, the manager would first identify the largest

variances, attempt to uncover their causes, and then implement actions aimed

at correcting them. The smaller variances would be tackled after the major

problems were dealt with, if at all.

Financial & Managerial Accounting, 5th Edition

1236

SERIAL PROBLEM — SP 21

Serial Problem, Success Systems (30 minutes)

Success Systems

Flexible Budget Performance Report

For Quarter Ended June 30

Flexible

Actual

Budget

Results

Variances

Desk sales (150 units) …………………..……..

$187,500

$186,000

$1,500

U

Chair sales (80 units) …………………….…….

Variable expenses ………………………..…

40,000

132,500

41,200

132,880

1,200

380

F

U

Contribution margin ……………………..……

95,000

94,320

680

U

Fixed expenses …………………………….……..

30,000

31,000

1,000

U

Income from operations ………………..……..

$ 65,000

$ 63,320

$1,680

U

Supporting computations

Total budgeted desk sales ……………………………………….…………

$180,000

Total units budgeted ………………………………………………..……..

144

Budgeted selling price …………………………………………….…………

$1,250 per unit

Flexible budget units …………………………..…………………..………

150

Flexible budget sales ……………………………………………….………

$187,500

Total budgeted chair sales……………………………………….…………

$ 36,000

Total units budgeted ………………………………………………..……..

72

Budgeted selling price …………………………………………….…………

$500 per unit

Flexible budget units …………………………..…………………..………

80

Flexible budget sales ……………………………………………….………

$ 40,000

Total budgeted variable costs for desks …………………..………

$108,000

Total units budgeted ………………………………………………..……..

144

Budgeted variable expenses per desk ……………………..……

$750

Flexible budget units …………………………..…………………..………

150

Flexible budget variable expenses for desks ………………………

$112,500

Serial Problem, Success Systems (concluded)

Total budgeted variable costs for chairs …………………..………

$18,000

Total units budgeted ………………………………………………..……..

72

Budgeted variable expenses per chair ……………………..……

$250

Flexible budget units …………………………..…………………..………

80

Flexible budget variable expenses for chairs ………………………

$20,000

Total budgeted variable expenses* …………………………..

$132,500

*($112,500 + $20,000), from calculation above

Total actual expenses ……………………………………………………….

$163,880

Actual fixed expenses ……………………………………………..………..

31,000

Actual variable expenses ……………………………………………………

$132,880

Financial & Managerial Accounting, 5th Edition

1238

Reporting in Action — BTN 21-1

1. Polaris reports the annual adjustment (remeasurement adjustment or

2. As reported in its footnote, the assets and liabilities of foreign subsidiaries

(e.g. cash and property, plant and equipment) are translated at exchange

rates in effect at the balance sheet date and revenues and expenses are

Comparative Analysis — BTN 21-2

1. Polaris and Arctic Cat sales figures for the most recent 3 years—data

available from Appendix A—are shown below ($ thousands):

Two Years

Prior

One Year

Prior

Current

Year

One

Year

Ahead

Two

Years

Ahead

Polaris

$1,565,887

$ 1,991,139

$2,656,949

_______

_______

27% incr.

33% incr.

Arctic Cat

$563,613

$450,728

$464,651

_______

_______

20% decr.

3% incr.

2. Predictions will vary among students. Generally, predictions should

reflect both the trend in the company’s sales data and current industry

and economy-wide conditions. Polaris’s sales increased in each of the

Ethics Challenge — BTN 21-3

A typical answer might include four individuals selected from the following

specialty areas (answers will vary among students):

Specialty

Information Input and Explanation

Engineer …………………………..

Scientific support for quantity standard.

Production manager ………..…

Actual amount or quantity used in production.

Supplier …………………………..

Identify reasonable price of inputs.

Purchasing manager ……….…

Identify reasonable price of inputs.

Market research analyst …..…

Market research to support quantity and price

standards.

Communicating in Practice — BTN 21-4

MEMORANDUM

TO:

FROM:

DATE:

SUBJECT:

Variance

Cost of Goods Sold

Gross Margin

Part 1.

Favorable

Decrease

Increase

Part 2.

Unfavorable

Increase

Decrease

Part 3. A favorable (unfavorable) variance means that actual costs are

lower (higher) than the budgeted or expected amounts. It also

helps to point out the link between a favorable (unfavorable)

variance and an increase (decrease) in gross margin and net

income.

Financial & Managerial Accounting, 5th Edition

1240

Taking It to the Net — BTN 21-5

1. Benchmarking is a method whereby organizations try to look to other

organizations to identify “best practices” so as to improve and attain

2. Given that a benchmark can be considered as a standard, companies

Teamwork in Action — BTN 21–6

Answers will vary depending on the two industries selected. Two examples

are identified and briefly described below:

Entrepreneurial Decision — BTN 21-7

To: Mike McCabe, President

Folsom Custom Skis

Re: Management Accounting Quote Interpretations

Quote 1: “Variances are not explanations”

the variances to understand why they occurred.

Quote 2: “Management’s goal is not to minimize variances.”

Financial & Managerial Accounting, 5th Edition

1242

Hitting The Road — BTN 21-8

1. A typical cheese pizza has three main raw materials: dough, sauce, and

cheese.

2. Observe that the national chain probably follows specific measurement

components.

3. These observations reflect an important issue for pizza businesses and for

smaller, local businesses in particular. Excess raw materials applied to

Global Decision — BTN 21-9

1. Piaggio’s sales figures for the most recent 2 years — data available from its

Website — are shown below (€ thousands)

Sales

One Year

Prior

Current

Year

One Year

Ahead

Two Years

Ahead

Piaggio ……………………..

€1,485,351

€1,516,463

_______

_______

2.1% increase

from prior year

2. Predictions will vary among students. Generally, predictions should reflect