Student Name:

Class:

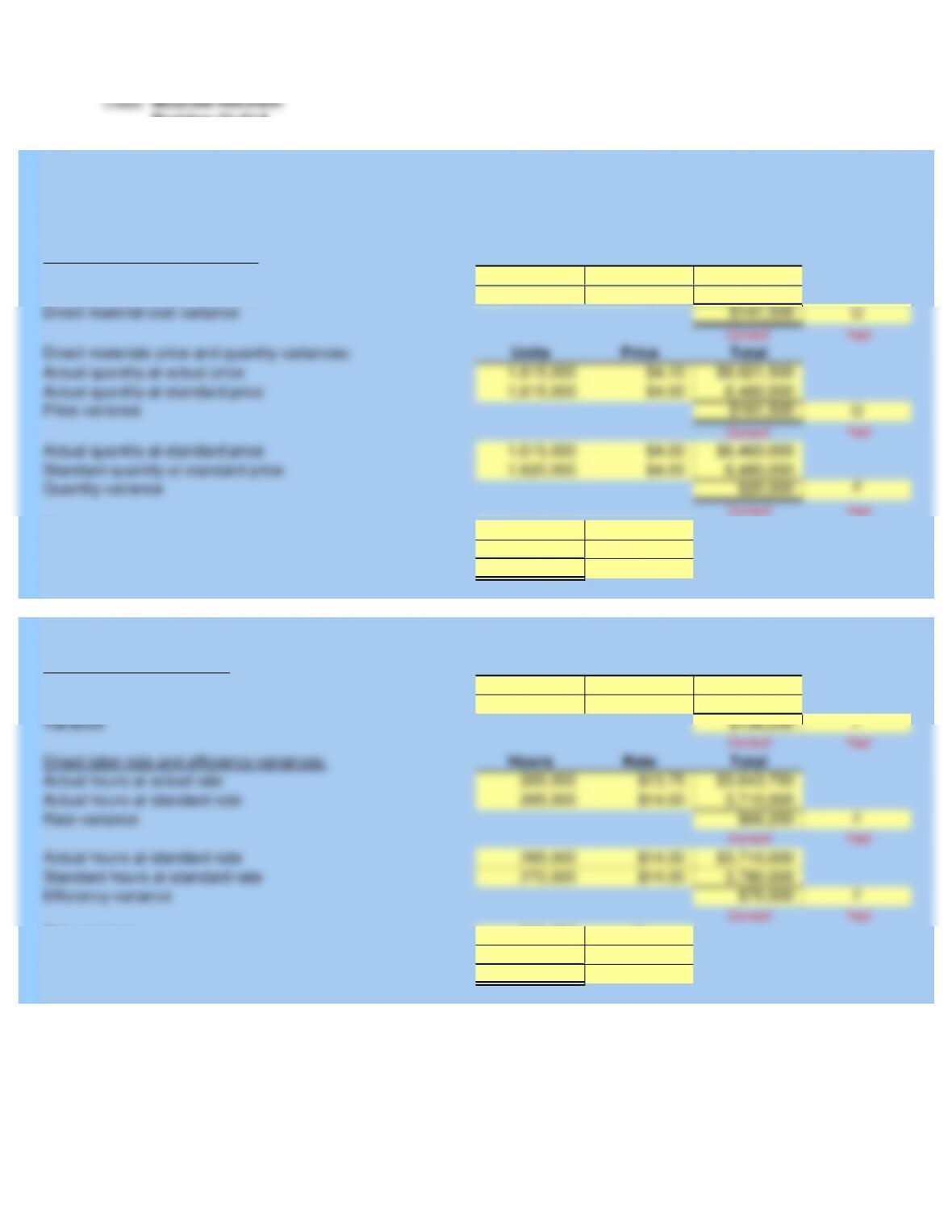

Units Cost Total

1,615,000 $4.10 $6,621,500

1,620,000 $4.00 6,480,000

$141,500 U

Direct material cost variance

Correct! Yes!

Units Price Total

1,615,000 $4.10 $6,621,500

1,615,000 $4.00 6,460,000

$161,500 U

Correct! Yes!

1,615,000 $4.00 $6,460,000

1,620,000 $4.00 6,480,000

$20,000 F

Correct! Yes!

$161,500 U

$20,000 F

$141,500 U

Correct! Yes!

Hours Cost Total

265,000 $13.75 $3,643,750

270,000 $14.00 3,780,000

$136,250 F

Correct! Yes!

Hours Rate Total

265,000 $13.75 $3,643,750

265,000 $14.00 3,710,000

$66,250 F

Correct! Yes!

265,000 $14.00 $3,710,000

270,000 $14.00 3,780,000

$70,000 F

Correct! Yes!

Rate variance

Efficiency variance

Total labor variance

Direct materials cost variances:

Actual hours at actual rate

Actual hours at standard rate

Rate variance

Efficiency variance

Actual hours at standard rate

Standard hours at standard rate

Price variance

Quantity variance

Actual units at actual cost

Standard units at standard cost

Variance

Direct labor rate and efficiency variances:

Direct labor cost variances:

Price variance

Actual quantity at standard price

Standard quantity at standard price

Quantity variance

Standard units at standard cost

Direct materials price and quantity variances:

Actual quantity at actual price

Actual quantity at standard price

Instructor

Variances

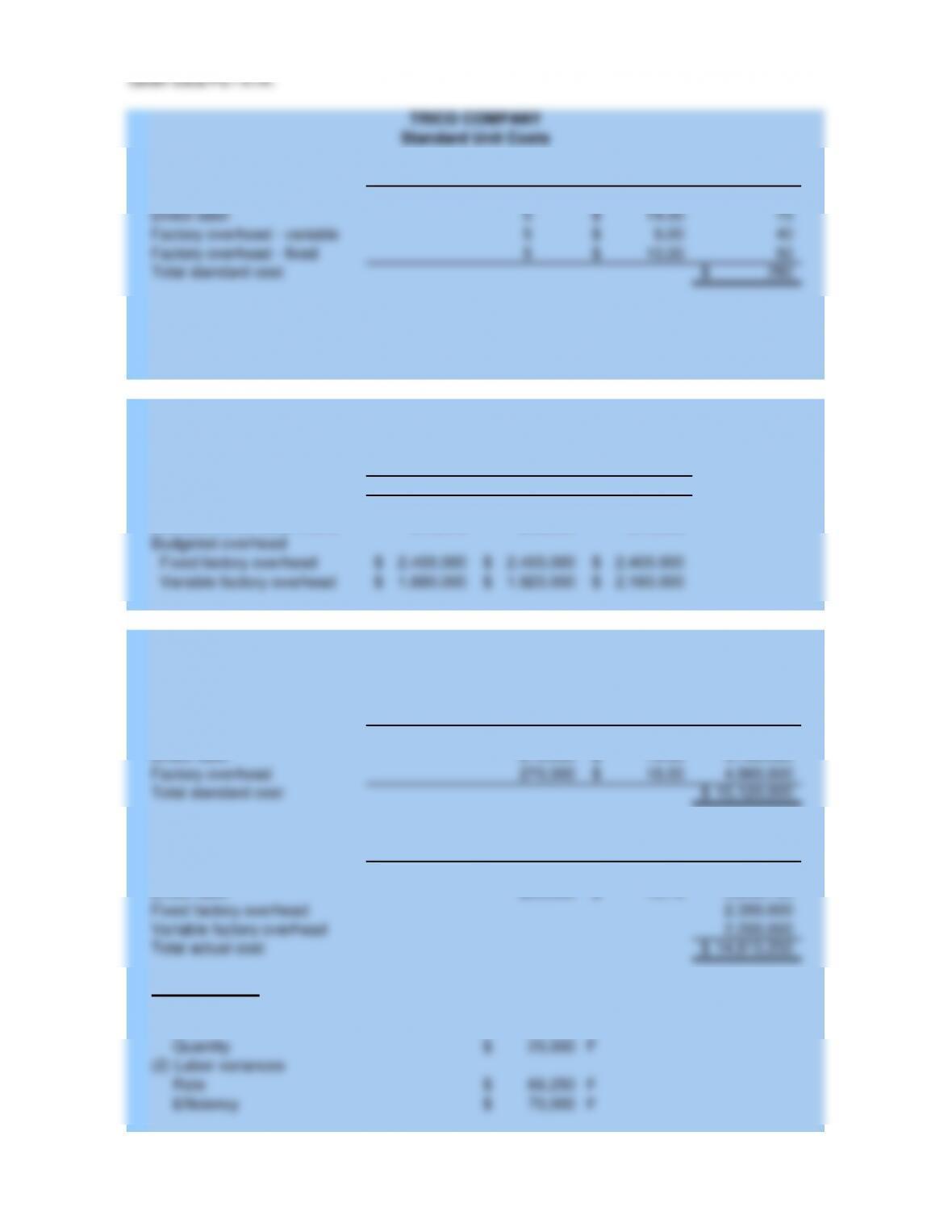

TRICO COMPANY

Problem 21-01A

McGraw-Hill/Irwin

Part 2 Direct Labor Variances:

Part 1 Direct Materials Variances:

Total materials variance

Actual units at actual cost

Student Name:

Class:

Instructor

Problem 21-01A

McGraw-Hill/Irwin

4,550,000$

4,560,000

10,000$ F

Correct! Yes!

2,400,000$

2,700,000

300,000$ F

Correct! Yes!

Applied overhead (90% capacity)

Controllable variance

Controllable variance

Budgeted fixed overhead (70% capacity)

Fixed overhead cost applied

Fixed overhead volume variance

Fixed overhead volume variance

Actual overhead

Part 3 Overhead Variances:

Pounds Hours Unit Cost Total

30 4.00$ 120$

514.00$ 70

58.00$ 40

510.00$ 50

280$

Pounds Hours Unit Cost Total

Pounds Hours Unit Cost Total

(2) Labor variances

Rate

Efficiency

Actual costs incurred during quarter:

(1) Materials variances

Price

Quantity

Direct material

Direct labor

Fixed factory overhead

Variable factory overhead

Total actual cost

Variable factory overhead

Direct material

Direct labor

Factory overhead

Total standard cost

Production in units

Standard direct labor hours

Budgeted overhead

Fixed factory overhead

Productive capacity per quarter in units

of productive capacity per quarter

Operating volume as percentage

TRICO COMPANY

TRICO COMPANY

Given Data P21-01A:

Factory overhead – variable

Direct labor

Direct materials

Standard Unit Costs

TRICO COMPANY

Total standard cost

Factory overhead – fixed

Student Name:

Class:

Flexible Actual

Budget Results Variances

3,600,000$ 3,648,000$ 48,000$ F

1,170,000 1,185,000 15,000 U

270,000 278,000 8,000 U

72,000 63,000 9,000 F

54,000 53,000 1,000 F

90,000 87,500 2,500 F

126,000 118,500 7,500 F

1,782,000 1,785,000 3,000 U

1,818,000 1,863,000 45,000 F

300,000 300,000 –

150,000 147,500 2,500 F

200,000 210,000 10,000 U

250,000 268,000 18,000 U

125,000 132,000 7,000 U

241,000 241,000 –

90,000 93,500 3,500 U

1,356,000 1,392,000 36,000 U

462,000$ 471,000$ 9,000$ F

Correct! Correct! Correct!

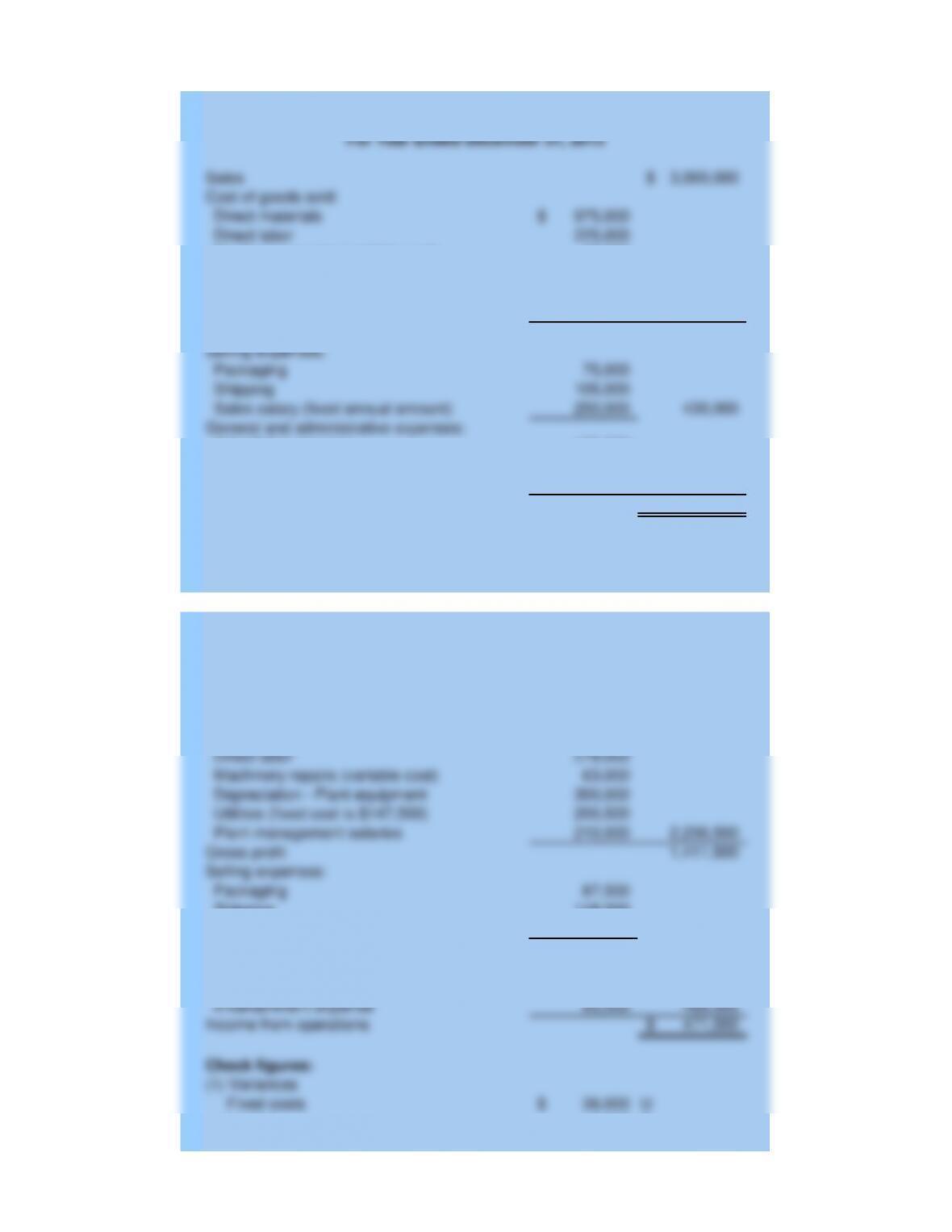

Advertising expense

Salaries

Entertainment expense

Total fixed costs

Income from operations

Contribution margin

Fixed costs:

Depreciation – plant equipment

Utilities

Plant management salaries

Sales salary

Direct labor

Machinery repairs

Utilities

Packaging

Shipping

Total variable costs

Instructor

For Year Ended December 31, 2013

Flexible Budget Performance Report

PHOENIX COMPANY

Problem 21-04A

Sales

McGraw-Hill/Irwin

Variable costs:

Direct materials

Student Name:

Class:

Instructor

Problem 21-04A

McGraw-Hill/Irwin

Total Per unit

3,600,000$ 200.00$

3,648,000 202.67

48,000$ 2.67$

Correct! Correct!

Total Per unit

1,170,000$ 65.00$

1,185,000 65.83

15,000$ 0.83$

Correct! Correct!

Interpretation:

Actual sales

Sales variance

Interpretation:

(b) Analysis of direct materials variance:

(a) Analysis of sales variance:

Budgeted sales

Actual materials used

Direct materials variance

(b) direct materials variance.

Part 2: Analyze and interpret both the (a) sales variance and

The sales variance is favorable because the actual price was higher than planned.

The direct materials variance is unfavorable for two possible reasons. (1) The quantity of materials used may

have been more than the quantity budgeted, and/or (2) the amount paid for the materials might have been

more than the budgeted purchase price.

Budgeted materials

3,000,000$

975,000$

225,000

60,000

300,000

1,045,000

75,000

105,000

250,000 430,000

Salaries

Entertainment expense

Advertising expense

Utilities ($45,000 is variable)

Plant management salaries

159,000$

15,000

3,648,000$

1,185,000$

278,000

63,000

300,000

200,500

Plant management salaries

Gross profit

Shipping

Sales salary (annual)

General and administrative expenses:

Advertising expense

Selling expenses:

Packaging

241,000

93,500 466,500

471,000$

36,000$ U

9,000 F

Given Data P21-04A:

Income from operations

Check figures:

(1) Variances

Fixed costs

Depreciation – Plant equipment

Utilities (fixed cost is $147,500)

Income

Salaries

Entertainment expense

Sales (18,000 units)

Cost of goods sold:

Direct materials

Direct labor

Machinery repairs (variable cost)

For Year Ended December 31, 2013

Statement of Income from Operations

PHOENIX COMPANY

Income from operations

Based on production and sales volume

Units

Selling expenses:

Packaging

Shipping

Sales salary (fixed annual amount)

General and administrative expenses:

Direct labor

Machinery repairs (variable cost)

Depreciation – plant equipment

Gross profit

Direct materials

For Year Ended December 31, 2013

Fixed Budget Report

PHOENIX COMPANY

Sales

Cost of goods sold: