Student Name:

Class:

March April May

25,000 32,000 35,000

30% 30% 30%

7,500 9,600 10,500

15,000 25,000 32,000

22,500 34,600 42,500

(20,000) (7,500) (9,600)

2,500 27,100 32,900

Correct! Correct! Correct!

March April May

90,000 95,000 90,000

30% 30% 30%

27,000 28,500 27,000

70,000 90,000 95,000

97,000 118,500 122,000

(80,000) (27,000) (28,500)

17,000 91,500 93,500

Correct! Correct! Correct!

March April May

38,000 37,000 25,000

30% 30% 30%

11,400 11,100 7,500

40,000 38,000 37,000

51,400 49,100 44,500

(50,000) (11,400) (11,100)

1,400 37,700 33,400

Correct! Correct! Correct!

Less actual (or budgeted) beginning inventory

Required units of available merchandise

Less actual (or budgeted) beginning inventory

Budgeted purchases

Budgeted purchases

Budgeted sales for next month

Ratio of ending inventory to future sales

Budgeted ending inventory

Add budgeted sales

Budgeted sales for next month

Ratio of ending inventory to future sales

Budgeted ending inventory

Add budgeted sales

Required units of available merchandise

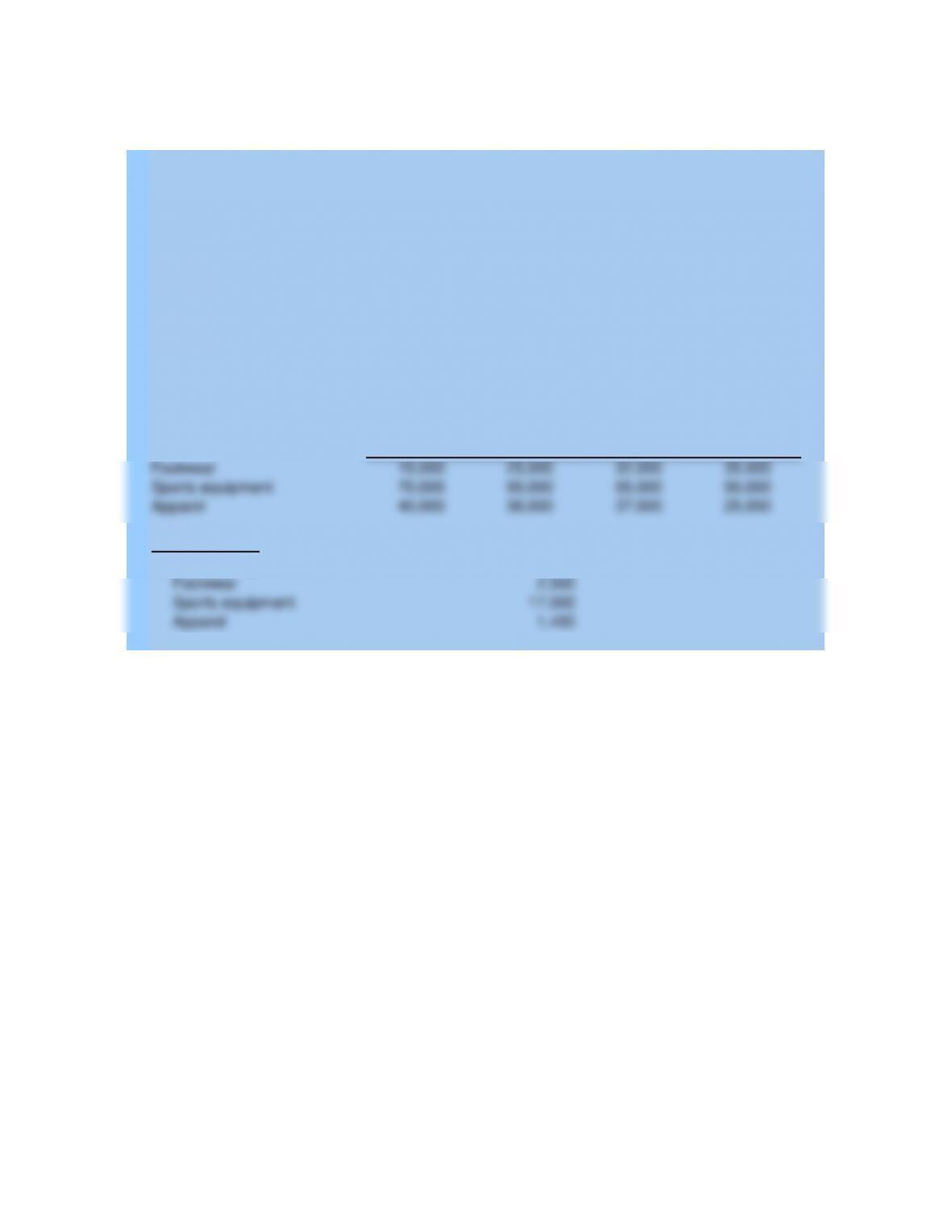

Footwear

Ratio of ending inventory to future sales

Merchandise Purchases Budgets (in units)

For March, April and May

Apparel

Budgeted ending inventory

Add budgeted sales

Required units of available merchandise

Less actual (or budgeted) beginning inventory

Budgeted purchases

McGraw-Hill/Irwin

Instructor

KEGGLER’S SUPPLY

Problem 20-01A

Sports equipment

Budgeted sales for next month

Student Name:

Class:

McGraw-Hill/Irwin

Instructor

Problem 20-01A

Part 2: The purchases budgets in part 1 should reflect fewer purchases of all three products

in March compared to those in April and May. What factor caused fewer purchases to be

planned? Suggest business conditions that would cause this factor to both occur and impact

the company in this way.

The factor that causes the first month’s purchases to be so much smaller is the excess inventory that

accumulated just prior to the budgeting period. For example, 20,000 units of footwear are in March’s

beginning inventory; however, March sales are budgeted at only 15,000 units. Accordingly, budgeted

purchases are smaller because it is management’s goal to reduce the inventory to only 30% of the next

month’s sales. This overstocking factor could exist for a number of reasons, including: 1) Management may

have simply lost sight of inventory levels, thereby allowing them to reach inappropriately high levels. 2)

There may have been some potentially disruptive factor (such as a strike, bad weather, or political

uncertainty) that would have temporarily interrupted the smooth delivery of products from the supplier. Thus,

management would have found it prudent to accumulate an excess as a temporary safety stock against an

interrupted supply. 3) The company’s suppliers may have only recently become more dependable than they

were in the past. 4) A supplier may have recently located a new distribution facility nearby, with the result

that the merchandise can be delivered more promptly. 5) Competition among suppliers may have caused

them to become more customer oriented, with the result that they will deliver products in smaller lots more

quickly.

20,000

80,000

50,000

30%

March April May June

15,000 25,000 32,000 35,000

70,000 90,000 95,000 90,000

40,000 38,000 37,000 25,000

2,500

17,000

1,400

Apparel

Sports equipment

Footwear

(1) March budgeted purchases:

Check figures:

Given Data P20-01A:

Apparel

Sports equipment

KEGGLER’S SUPPLY

Footwear

Budgeted Sales in Units

KEGGLER’S SUPPLY

February 28

Units in Inventory

of expected sales for following month

Footwear

Sports equipment

Apparel

Desired ending inventory as percentage

Student Name:

Class:

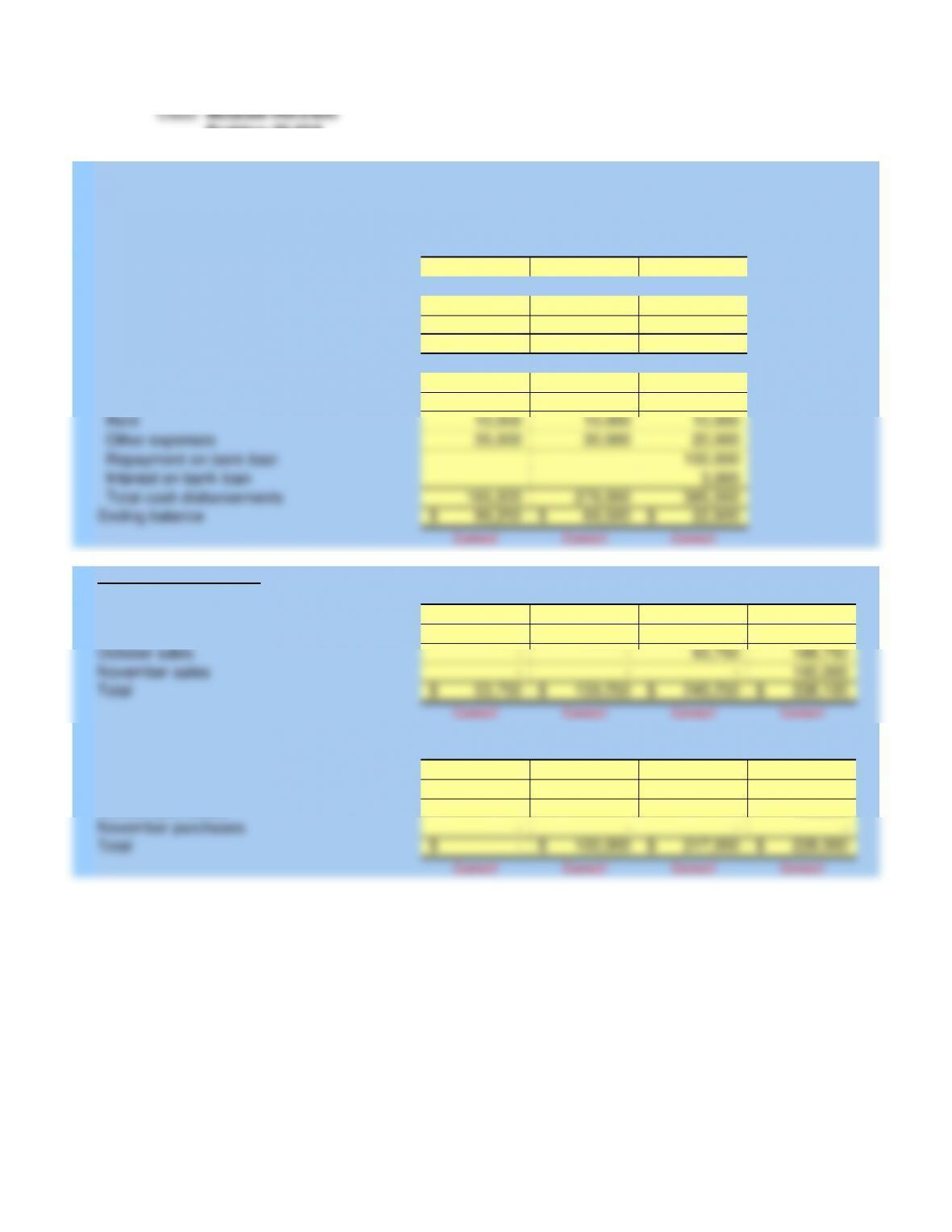

September October November

5,000$ 99,250$ 69,500$

159,250 249,250 338,100

100,000

264,250 348,500 407,600

100,000 217,000 228,000

20,000 22,000 24,000

10,000 10,000 10,000

35,000 30,000 20,000

100,000

3,000

165,000 279,000 385,000

99,250$ 69,500$ 22,600$

Correct! Correct! Correct!

August September October November

53,750$ 96,750$ 43,000$ 19,350$

– 62,500 112,500 50,000

– – 93,750 168,750

– – – 100,000

53,750$ 159,250$ 249,250$ 338,100$

Correct! Correct! Correct! Correct!

August September October November

–$ 100,000$ 25,000$ –$

November purchases

Total

September purchases

October purchases

Collections of credit sales:

Supporting schedules

Payments on credit purchases:

Total

August purchases

Total cash disbursements

Ending balance

August sales

September sales

October sales

November sales

Payments on accounts payable

Payroll

Rent

Other expenses

Repayment on bank loan

Interest on bank loan

Beginning balance

Cash receipts:

Collection on accounts receivable

Receipts from bank loan

Total cash available

Cash disbursements:

Problem 20-02A

McGraw-Hill/Irwin

Instructor

For September, October and November

Cash Budget

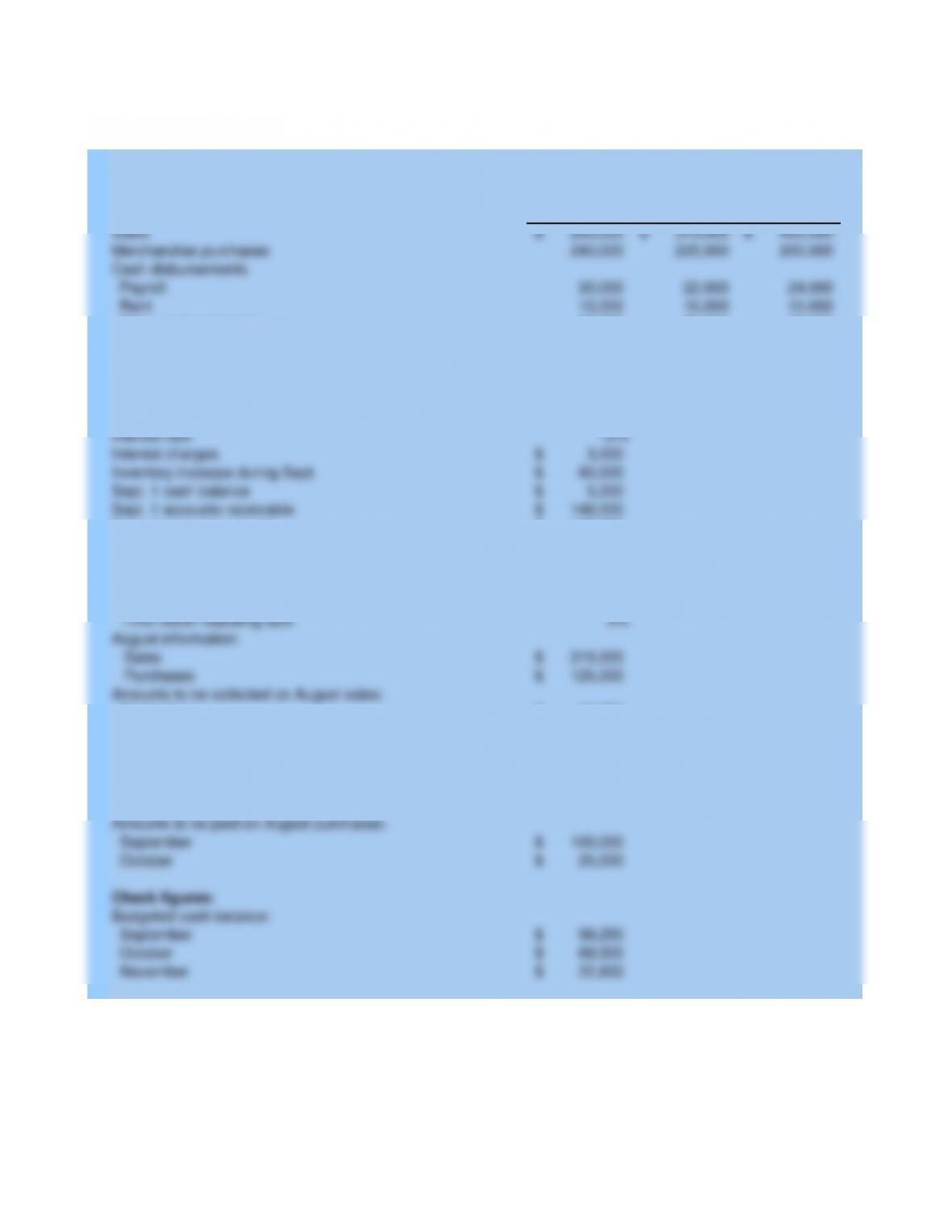

ONEIDA COMPANY

September October November

250,000$ 375,000$ 400,000$

240,000 225,000 200,000

20,000 22,000 24,000

10,000 10,000 10,000

35,000 30,000 20,000

100,000

3,000

100,000$

12%

3,000$

80,000$

5,000$

148,000$

125,000$

25%

45%

20%

9%

215,000$

125,000$

96,750$

43,000$

19,350$

80%

20%

100,000$

25,000$

99,250$

69,500$

22,600$

Given Data P20-02A:

October

November

September

October

Check figures:

Budgeted cash balance:

September

October

Amounts to be paid on August purchases:

Third month following sale

August information:

Sales

Purchases

Amounts to be collected on August sales:

Month following sale

Second month following sale

November

Amounts paid on purchases (as percentage):

Month following purchase

Second month following purchase

Bank loan requested

Interest rate

Interest charges

Inventory increase during Sept.

Sept. 1 cash balance

September

Sept. 1 accounts receivable

Sept. 1 accounts payable

Amounts collected on credit sales (as percentage):

Month of sale

Rent

Other cash expenses

Repayment of bank loan

Interest on the bank loan

Additional information:

Selected Budgets for Three Months

ONEIDA COMPANY

Sales

Merchandise purchases

Cash disbursements

Payroll