Financial & Managerial Accounting, 5th Edition

72

Exercise 2-17 (15 minutes)

(a)

(b)

(c)

(d)

Answers

$(28,000)

$42,000

$73,000

$(45,000)

Computations:

Equity, Dec. 31, 2012 …………..

$ 0

$ 0

$ 0

$ 0

Owner’s investments …..……..

110,000

42,000

87,000

210,000

Dividends …………………………..

(28,000)

(47,000)

(10,000)

(55,000)

Net income (loss) ………..……..

22,000

90,000

(4,000)

(45,000)

Equity, Dec. 31, 2013 …………..

$104,000

$85,000

$73,000

$110,000

Exercise 2-18 (25 minutes)

a. Belle created a new business and invested $6,000 cash, $7,600 of

Exercise 2-19 (30 minutes)

a. Cash ………………………………………………………………… 6,000

Equipment ……………………………………………………….. 7,600

b. Prepaid Insurance …………………………………………….. 4,800

Cash ………………………………………………………….. 4,800

Purchased insurance coverage.

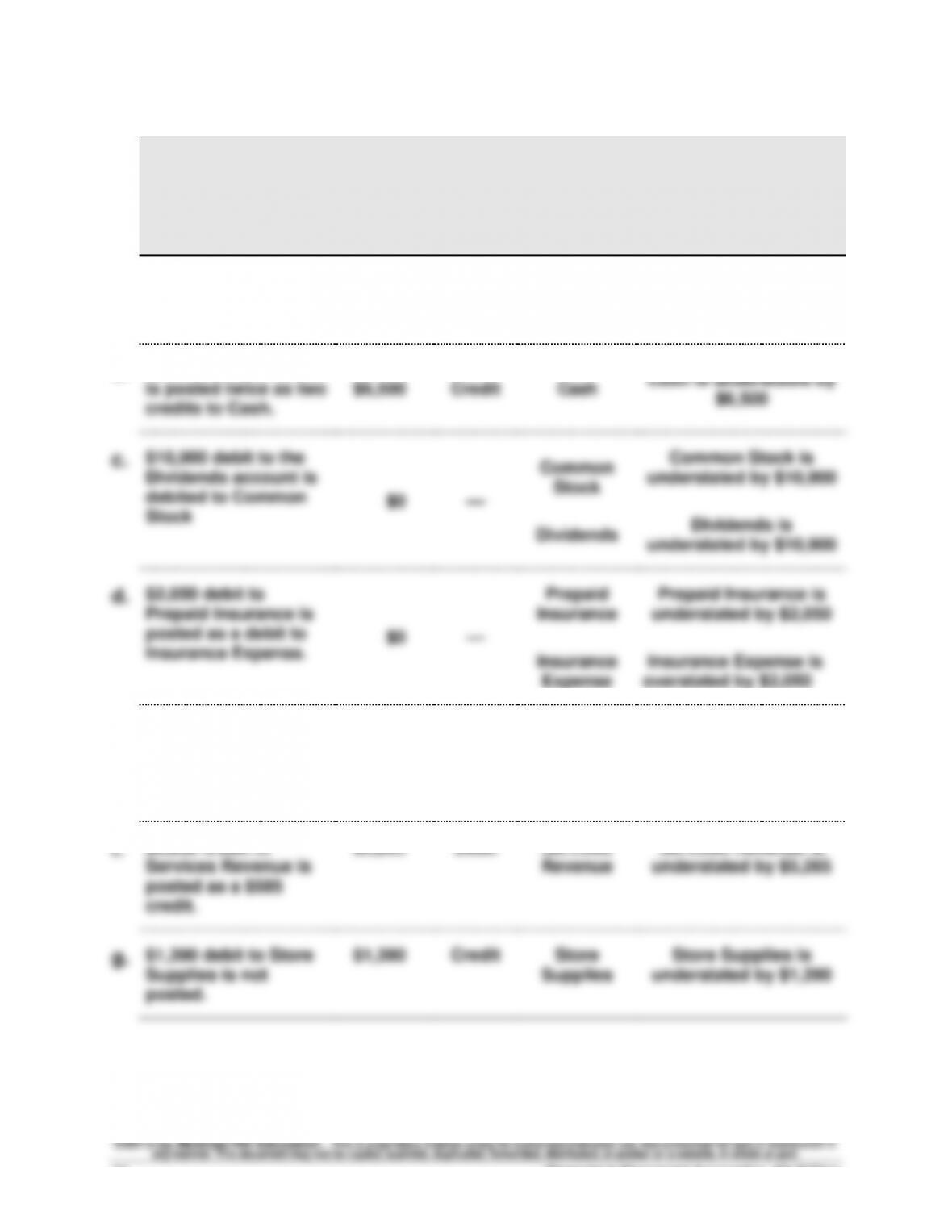

Exercise 2-20 (20 minutes)

Description

(1)

Difference

between

Debit and

Credit

Columns

(2)

Column

with the

Larger

Total

(3)

Identify

account(s)

incorrectly

stated

(4)

Amount that account(s)

is overstated or

understated

a.

$3,600 debit to Rent

Expense is posted as

a $1,340 debit.

$2,260

Credit

Rent Expense

Rent Expense is

understated by $2,260

b.

$6,500 credit to Cash

is posted twice as two

credits to Cash.

$6,500

Credit

Cash

Cash is understated by

$6,500

c.

$10,900 debit to the

Dividends account is

debited to Common

Stock

$0

––

Common

Stock

Dividends

Common Stock is

understated by $10,900

Dividends is

understated by $10,900

d.

$2,050 debit to

Prepaid Insurance is

posted as a debit to

Insurance Expense.

$0

––

Prepaid

Insurance

Insurance

Expense

Prepaid Insurance is

understated by $2,050

Insurance Expense is

overstated by $2,050

e.

$38,000 debit to

Machinery is posted

as a debit to Accounts

Payable.

$0

––

Machinery

Accounts

Payable

Machinery is

understated by $38,000

Accounts Payable is

understated by $38,000

f.

$5,850 credit to

Services Revenue is

posted as a $585

credit.

$5,265

Debit

Services

Revenue

Services Revenue is

understated by $5,265

g.

$1,390 debit to Store

Supplies is not

posted.

$1,390

Credit

Store

Supplies

Store Supplies is

understated by $1,390

Exercise 2-21 (15 minutes)

a. The debit column is correctly stated because the erroneous debit (to

Accounts Payable) is deducted from an account with a (larger assumed)

credit balance.

Exercise 2-22 (15 minutes)

a.

Co.

Liabilities

/

Assets

=

Debt

Ratio

Net

Income

/

Average

Assets

=

ROA

1

$11,765

$ 90,500

0.13

$20,000

$100,000

0.200

2

46,720

64,000

0.73

3,800

40,000

0.095

3

26,650

32,500

0.82

650

50,000

0.013

4

55,860

147,000

0.38

21,000

200,000

0.105

5

31,280

92,000

0.34

7,520

40,000

0.188

6

52,250

104,500

0.50

12,000

80,000

0.150

b. Company 3 relies most heavily on creditor (non-owner) financing with 82%

of its assets financed by liabilities.

c. Company 1 relies least on creditor (non–owner) financing at only 13%.

Financial & Managerial Accounting, 5th Edition

76

Exercise 2-23 (10 minutes)

BMW

Balance Sheet (in Euro millions)

December 31, 2011

Assets Equity and liabilities

Noncurrent assets …….. € 9,826 Total equity …………………….. € 8,222

PROBLEM SET A

Problem 2-1A (90 minutes)

Part 1

a. Cash……………………………………………………. 101 100,000

Office Equipment …………………………………. 163 5,000

Drafting Equipment ……………………………… 164 60,000

Common Stock …………………………….. 307 165,000

Owner invested cash and equipment for stock.

b. Land ……………………………………………………. 172 49,000

f. Drafting Equipment ……………………………… 164 20,000

Cash …………………………………………….. 101 9,500

Notes Payable ………………………………. 250 10,500

Purchased equipment with cash and notes

payable.

g. Accounts Receivable …………………………... 106 14,000

Financial & Managerial Accounting, 5th Edition

78

Problem 2-1A (Part 1 Continued)

i. Accounts Receivable …………………………... 106 22,000

Engineering Fees Earned ……………… 402 22,000

Billed client for completed work.

j. Equipment Rental Expense ………………….. 602 1,333

m. Accounts Payable ……………………………….. 201 1,150

Cash ………………………………………….. 101 1,150

Paid amount due on account.

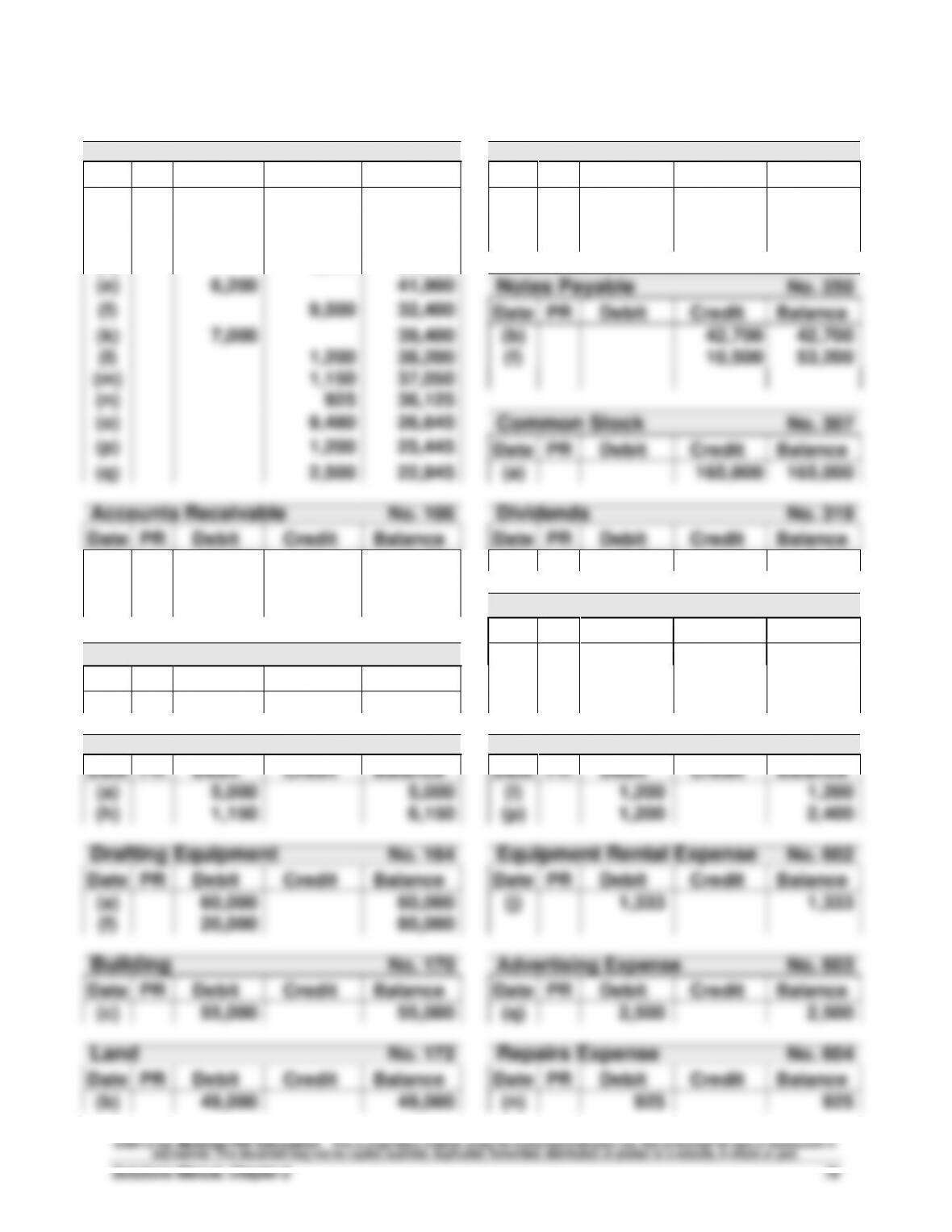

Problem 2-1A (Continued)

Part 2

Cash No. 101

Accounts Payable No. 201

Date

PR

Debit

Credit

Balance

Date

PR

Debit

Credit

Balance

(a)

100,000

100,000

(h)

1,150

1,150

(b)

6,300

93,700

(j)

1,333

2,483

(c)

55,000

38,700

(m)

1,150

1,333

(d)

3,000

35,700

(e)

6,200

41,900

Notes Payable No. 250

(f)

9,500

32,400

Date

PR

Debit

Credit

Balance

(k)

7,000

39,400

(b)

42,700

42,700

(l)

1,200

38,200

(f)

10,500

53,200

(m)

1,150

37,050

(n)

925

36,125

(o)

9,480

26,645

Common Stock No. 307

(p)

1,200

25,445

Date

PR

Debit

Credit

Balance

(q)

2,500

22,945

(a)

165,000

165,000

Accounts Receivable No. 106

Dividends No. 319

Date

PR

Debit

Credit

Balance

Date

PR

Debit

Credit

Balance

(g)

14,000

14,000

(o)

9,480

9,480

(i)

22,000

36,000

(k)

7,000

29,000

Engineering Fees Earned No. 402

Date

PR

Debit

Credit

Balance

Prepaid Insurance No. 108

(e)

6,200

6,200

Date

PR

Debit

Credit

Balance

(g)

14,000

20,200

(d)

3,000

3,000

(i)

22,000

42,200

Office Equipment No. 163

Wages Expense No. 601

Date

PR

Debit

Credit

Balance

Date

PR

Debit

Credit

Balance

(a)

5,000

5,000

(l)

1,200

1,200

(h)

1,150

6,150

(p)

1,200

2,400

Drafting Equipment No. 164

Equipment Rental Expense No. 602

Date

PR

Debit

Credit

Balance

Date

PR

Debit

Credit

Balance

(a)

60,000

60,000

(j)

1,333

1,333

(f)

20,000

80,000

Building No. 170

Advertising Expense No. 603

Date

PR

Debit

Credit

Balance

Date

PR

Debit

Credit

Balance

(c)

55,000

55,000

(q)

2,500

2,500

Land No. 172

Repairs Expense No. 604

Date

PR

Debit

Credit

Balance

Date

PR

Debit

Credit

Balance

(b)

49,000

49,000

(n)

925

925

Problem 2-1A (Concluded)

Part 3

ARACEL ENGINEERING

Trial Balance

June 30

Debit Credit

Cash ……………………………………………………. $ 22,945

Accounts receivable ……………………………. 29,000

Prepaid insurance ……………………………….. 3,000

Office equipment …………………………………. 6,150

Common stock ……………………………………. 165,000

Dividends ……………………………………………. 9,480

Engineering fees earned ………………………. 42,200

Problem 2-2A (90 minutes)

Part 1

Mar. 1 Cash……………………………………………………. 101 150,000

Office Equipment …………………………………. 163 22,000

Common Stock …………………………….. 307 172,000

Owner invested cash and equipment for stock.

2 Prepaid Rent ……………………………………….. 131 6,000

Cash …………………………………………….. 101 6,000

Prepaid six months’ rent.

3 Office Equipment …………………………………. 163 3,000

Office Supplies ……………………………………. 124 1,200

Paid premium for insurance.

22 Cash……………………………………………………. 101 3,500

Accounts Receivable ……………………. 106 3,500

Collected part of amount owed by client.

25 Accounts Receivable …………………………... 106 3,820

Problem 2-2A (Continued)

Part 2

Cash

Acct. No. 101

Date

Explanation

PR

Debit

Credit

Balance

Mar.

1

G1

150,000

150,000

2

G1

6,000

144,000

6

G1

4,000

148,000

12

G1

4,200

143,800

19

G1

5,000

138,800

22

G1

3,500

142,300

29

G1

5,100

137,200

31

G1

500

136,700

Accounts Receivable

Acct. No. 106

Date

Explanation

PR

Debit

Credit

Balance

Mar.

9

G1

7,500

7,500

22

G1

3,500

4,000

25

G1

3,820

7,820

Office Supplies

Acct. No. 124

Date

Explanation

PR

Debit

Credit

Balance

Mar.

3

G1

1,200

1,200

30

G1

600

1,800

Prepaid Insurance

Acct. No. 128

Date

Explanation

PR

Debit

Credit

Balance

Mar.

19

G1

5,000

5,000

Prepaid Rent

Acct. No. 131

Date

Explanation

PR

Debit

Credit

Balance

Mar.

2

G1

6,000

6,000

Office Equipment

Acct. No. 163

Date

Explanation

PR

Debit

Credit

Balance

Mar.

1

G1

22,000

22,000

3

G1

3,000

25,000

Problem 2-2A (Continued)

Part 2 (Continued)

Accounts Payable

Acct. No. 201

Date

Explanation

PR

Debit

Credit

Balance

Mar.

3

G1

4,200

4,200

12

G1

4,200

0

30

G1

600

600

Common Stock

Acct. No. 307

Date

Explanation

PR

Debit

Credit

Balance

Mar.

1

G1

172,000

172,000

Dividends

Acct. No. 319

Date

Explanation

PR

Debit

Credit

Balance

Mar.

29

G1

5,100

5,100

Services Revenue

Acct. No. 403

Date

Explanation

PR

Debit

Credit

Balance

Mar.

6

G1

4,000

4,000

9

G1

7,500

11,500

25

G1

3,820

15,320

Utilities Expense

Acct. No. 690

Date

Explanation

PR

Debit

Credit

Balance

Mar.

31

G1

500

500

Financial & Managerial Accounting, 5th Edition

84

Problem 2-2A (Concluded)

Part 3

VENTURE CONSULTANTS

Trial Balance

March 31

Debit Credit

Cash ……………………………………………………………. $136,700

Accounts receivable …………………………………….. 7,820

Office supplies ……………………………………………… 1,800

Prepaid insurance ………………………………………… 5,000

Problem 2-3A (90 minutes)

Part 1

April 1 Cash……………………………………………………. 101 80,000

Office Equipment …………………………………. 163 26,000

Common Stock …………………………….. 307 106,000

Owner invested cash and equipment for stock.

2 Prepaid Rent ……………………………………….. 131 9,000

Cash …………………………………………….. 101 9,000

Prepaid twelve months’ rent.

3 Office Equipment …………………………………. 163 8,000

Office Supplies ……………………………………. 124 3,600

22 Cash……………………………………………………. 101 4,400

Accounts Receivable ……………………. 106 4,400

Collected part of amount owed by client.

25 Accounts Receivable …………………………... 106 2,890

Services Revenue …………………………. 403 2,890

Billed client for completed work.

Problem 2-3A (Continued)

Part 2

Cash

Acct. No. 101

Date

Explanation

PR

Debit

Credit

Balance

April

1

G1

80,000

80,000

2

G1

9,000

71,000

6

G1

4,000

75,000

13

G1

11,600

63,400

19

G1

2,400

61,000

22

G1

4,400

65,400

28

G1

5,500

59,900

30

G1

435

59,465

Accounts Receivable

Acct. No. 106

Date

Explanation

PR

Debit

Credit

Balance

April

9

G1

6,000

6,000

22

G1

4,400

1,600

25

G1

2,890

4,490

Office Supplies

Acct. No. 124

Date

Explanation

PR

Debit

Credit

Balance

April

3

G1

3,600

3,600

29

G1

600

4,200

Prepaid Insurance

Acct. No. 128

Date

Explanation

PR

Debit

Credit

Balance

April

19

G1

2,400

2,400

Prepaid Rent

Acct. No. 131

Date

Explanation

PR

Debit

Credit

Balance

April

2

G1

9,000

9,000

Office Equipment

Acct. No. 163

Date

Explanation

PR

Debit

Credit

Balance

April

1

G1

26,000

26,000

3

G1

8,000

34,000