Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 02 – Analyzing and Recording Transactions

Chapter Outline

Notes

e. Verify that each journal entry is properly posted.

f. Verify that the original journal entry has equal debits and

credits.

2. If an error in a journal entry is discovered before the entry is

posted, it can be corrected in a manual system by drawing a

line through the incorrect information and writing in the

correct information.

3. If an error in a journal entry is not discovered until after it is

posted, a correcting entry that removes the amount from the

wrong account and records it to the correct account should be

journalized and posted.

C. Using a Trial Balance to Prepare Financial Statements

The statements prepared in this chapter are called unadjusted

statements because further account adjustments need to be made

(as described in chapter 3).

1. A balance sheet reports on an organization’s financial position

at a point in time. The income statement, statement of retained

earnings, and statement of cash flows report on financial

performance over a period of time.

2. A one-year, or annual, reporting period is known as the

accounting, or fiscal, year. A business whose accounting year

noncalendar-year company.

3. Income Statement—reports the revenues earned less the

how retained earnings changes over the accounting period.

5. Balance Sheet—reports the financial position of a company at

a point in time, usually at the end of a month, quarter, or year.

equity on the bottom.

6. Presentation Issues:

a. Dollar signs are not used in journals and ledgers; they do

appear in financial statements and other reports such as

the trial balance. The usual practice is to put dollar signs

beside only the first and last numbers in a column.

b. Companies commonly round amounts in reports to the

Chapter 02 – Analyzing and Recording Transactions

Chapter Outline

IV. Global View

A. Analyzing and Recording Transactions – Both GAAP and IFRS

include broad and similar guidance for financial accounting but

these differences will fade as they work together toward a common

conceptual framework. All of the transactions in this chapter are

accounted for identically under these two systems.

B. Financial Statements – Both GAAP and IFRS prepare the same

four basic financial statements with some differences. Both require

balance sheets to separate current and noncurrent items. However,

GAAP balance sheets report current items first and IFRS balance

sheets present noncurrent items first (and equity before liabilities).

C. Accounting Controls and Assurance – Accounting systems

depend on control procedures that assure proper principles were

applied in processing accounting information. SOX legislation

strengthened U.S. control procedures. Global standards for control

are diverse which means that their application in different countries

can yield different outcomes depending on the quality of their

auditing standards and enforcement.

Notes

V. Decision Analysis—Debt Ratio

A. A company that finances a relatively large portion of its assets

with liabilities has a high degree of financial leverage. Higher

financial leverage involves greater risk because liabilities must be

repaid and often require regular interest payments (equity

financing does not). The risk that a company might not be able to

meet such required payments is higher if it has more liabilities (is

more highly leveraged).

B. One way to assess the risk associated with a company’s use of

liabilities is to compute the debt ratio.

1. It is calculated as total liabilities divided by total assets.

2. It tells us how much (what percentage) of the assets are

financed by creditors (non-owners) or liability financing; the

higher the debt ratio, the more risk a company faces from its

financial leverage.

Chapter 02 – Analyzing and Recording Transactions

VISUAL #2-1

THREE PARTS OF AN ACCOUNT

(1) ACCOUNT TITLE

Left Side

Right Side

called

called

(2) DEBIT

(3) CREDIT

RULES FOR USING ACCOUNTS

If total debits are greater than total credits, the account has a

debit balance equal to the difference of the two totals.

If total credits are greater than total debits, the account has a

credit balance equal to the difference of the two totals.

Chapter 02 – Analyzing and Recording Transactions

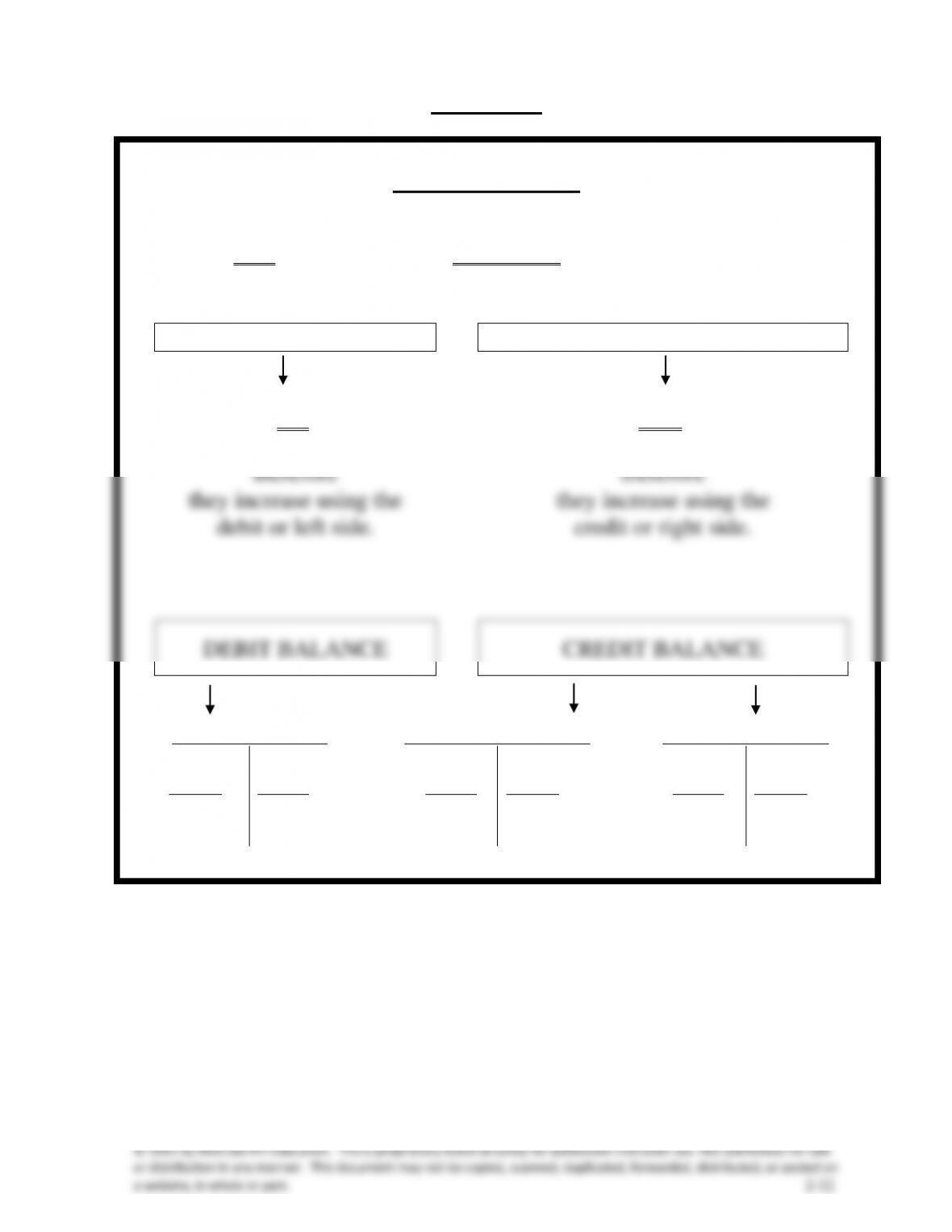

VISUAL #2-2

BALANCE SIDES

ALL ACCOUNTS ARE ASSIGNED BALANCE SIDES.

ASSETS

=

LIABILITIES + EQUITY

are on the left side of the

accounting equation,

therefore

they increase using the

debit or left side.

are on the right side of the

accounting equation,

therefore

they increase using the

credit or right side.

DEBIT BALANCE

CREDIT BALANCE

Asset Accounts

Liability Accounts

Equity Accounts

Debit

Credit

Debit

Credit

Debit

Credit

+ side

– side

– side

+ side

– side

+ side

Normal

Normal

Normal

Balance

Balance

Balance

Chapter 02 – Analyzing and Recording Transactions

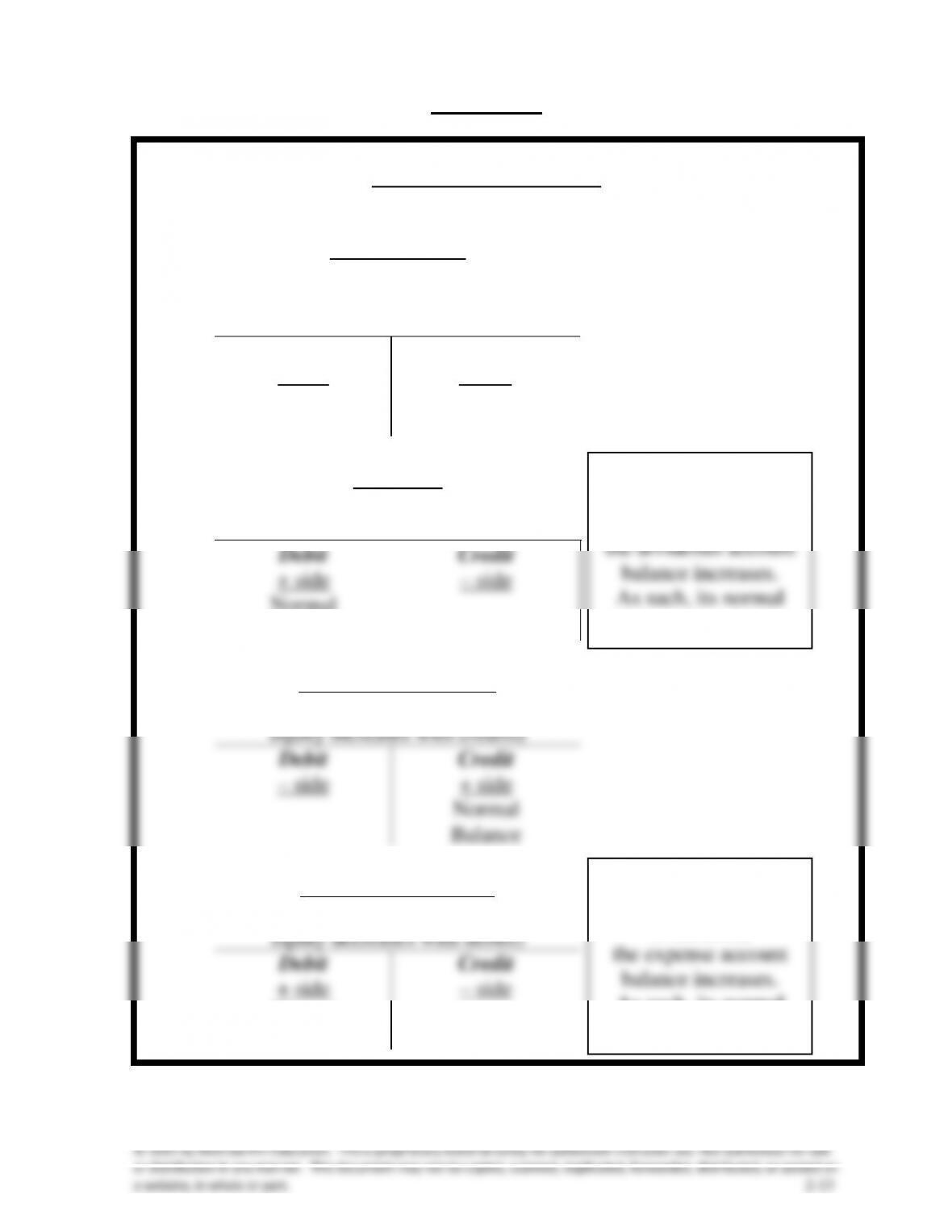

VISUAL #2-3

EQUITY ACCOUNTS

Common Stock

(increases equity, which is on the right

side of the accounting equation,

equity increases with credits)

Debit

Credit

– side

+ side

Normal

Balance

Dividends

(decreases equity,

equity decreases with debits)

Debit

Credit

+ side

– side

Normal

Balance

All Revenue Accounts

(increases equity,

equity increases with credits)

Debit

Credit

– side

+ side

Normal

Balance

All Expense Accounts

(decreases equity,

equity decreases with debits)

Debit

Credit

+ side

– side

Normal

Balance

Each time assets are

distributed to

stockholders,

the dividends account

balance increases.

As such, its normal

balance is a debit.

Each time

an expense

is incurred,

the expense account

balance increases.

As such, its normal

balance is a debit.

Chapter 02 – Analyzing and Recording Transactions

VISUAL #2-4

USING ACCOUNTS – SUMMARY

Assets = Liabilities + Equity

Asset Accounts

Liability Accounts

Equity Accounts

Debit +

Credit +

Credit +

Balance

Balance

Balance

Revenue Accounts

Expense Accounts

Credit +

Debit +

Balance

Balance

RULE REVIEW

Transaction analysis rules:

• Each transaction affects at least two accounts.

Chapter 02 – Analyzing and Recording Transactions

a website, in whole or part. 2-15

Chapter 2 – Alternate Demonstration Problem #1

Wigor Inc. completed the following transactions during the year ended

December 31, 2013, its first year of operations:

a. Bill Wiggins personally invests $30,000 in the new business in

exchange for common stock and deposits the cash in a bank

account opened under the name of Wigor Inc.

b. Equipment for use in the business was purchased for $9,000.

Two-thirds of the price was paid in cash; the rest was due in a

year.

c. Service fees earned were $60,000; $6,000 of this was on credit.

d. Operating expenses incurred were $35,000; $4,000 was on credit.

e. Wigor Co. collected half the money owed to it.

f. Wigor Co. paid off $2,000 it owed.

g. Wiggins bought a car for $12,000 for his personal use, half paid

for now from his personal savings and half to be paid in a year.

Required:

1. Prepare journal entries for each of the events.

2. Prepare a trial balance at the end of the year for Wigor Inc.

Chapter 02 – Analyzing and Recording Transactions

a website, in whole or part. 2-16

Solution: Chapter 2 – Alternate Demonstration Problem #1

1.

Dr.

Cr.

a.

Cash ........................................................

30,000

Common Stock ................................

30,000

b.

Equipment ..............................................

9,000

Cash ..................................................

6,000

Accounts Payable ...........................

3,000

c.

Cash ........................................................

54,000

Accounts Receivable ............................

6,000

Service Fee Earned .........................

60,000

d.

Operating Expenses ..............................

35,000

Cash ..................................................

31,000

Accounts Payable ...........................

4,000

e.

Cash ........................................................

3,000

Accounts Receivable ......................

3,000

f.

Accounts Payable .................................

2,000

Cash ..................................................

2,000

g.

No entry because this is a personal

transactions

2.

WIGOR INC.

Trial Balance

December 31, 2013

Dr.

Cr.

Cash ............................................................................

$48,000

Accounts receivable .................................................

3,000

Equipment ..................................................................

9,000

Accounts payable ......................................................

$ 5,000

Common Stock ..........................................................

30,000

Service fees earned ...................................................

60,000

Operating expenses ..................................................

35,000

______

Totals ..........................................................................

$95,000

$95,000