Chapter 19

Variable Costing and Performance

Reporting

QUESTIONS

1. Variable costing includes direct materials, direct labor, and variable overhead as

2. Absorption costing includes direct materials, direct labor, variable overhead and

3. When units produced exceed units sold for a reporting period, income under

variable costing would be less than income determined under absorption costing.

4. a. Gross margin is computed as sales minus cost of goods sold. Cost of goods

b. Contribution margin is computed as sales minus variable expenses. Variable

5. For short-run pricing decisions (such as special orders) absorption costing may not

6. For variable costing to achieve correct short-run pricing decisions, the price should

Financial & Managerial Accounting, 5th Edition

1056

7. Generally, variable and fixed manufacturing costs are controllable at different levels

of management. Production managers may be able to control the direct materials

8. Absorption costing can lead to over-production for two reasons:

a. Fixed overhead cost per unit costs fall as production increases. Matching a

lower cost per unit against a constant selling price will cause gross margin and

9. Variable costing may violate the matching principle, in that all manufacturing costs

10. If units produced equals units sold, no conversion is necessary. If production

exceeds sales, absorption costing income can be determined by adding (increase in

unit in beginning inventory is the same as that for the period.

11. Reporting contribution margin by segment is useful in assessing the profitability of

12. The contribution margin format income statement has the cost-volume-profit data

13. There are several factors that Arctic Cat should consider before pricing this special

order. First, the selling price should exceed the variable costs of manufacturing

14. Piaggio’s selling prices must cover the cost of the items sold, as well as all selling

and administrative expenses. Obviously, a selling price must exceed the cost of

Financial & Managerial Accounting, 5th Edition

1058

QUICK STUDIES

Quick Study 19-1 (10 minutes)

1. The total production cost per unit if 12,500 units are produced is:

Per unit

Direct materials ……………………………………………………………………………….

$3.00

Direct labor …………………………………………………………………………….……..

2.00

Variable overhead …………………………………………………………………..……….

4.00

Fixed overhead ($50,000/12,500 units) ……………………………………..……….

4.00

Total production cost per unit ……………………………………………………….

$13.00

2. The manager might produce more than currently be sold if he believes

Quick Study 19-2 (10 minutes)

D’SOUZA COMPANY

Manufacturing Margin

Sales (10,000 units x $80 per unit) ………………………………………….

$800,000

Variable production costs (10,000 units x $40 per unit) …………..

400,000

Manufacturing margin ……………………………………………………………

$400,000

Quick Study 19-3 (10 minutes)

D’SOUZA COMPANY

Contribution Margin

Manufacturing margin (from QS 19-2) …………………………………….

$400,000

Variable selling and admin costs (10,000 units x $10 per unit) …

100,000

Contribution margin ………………………………………………………………

$300,000

Quick Study 19-4 (10 minutes)

Cost per unit using absorption costing

Per unit

Direct materials ……………………………………………………………………………….

$10.00

Direct labor …………………………………………………………………………….……..

20.00

Variable overhead …………………………………………………………………..……….

10.00

Fixed overhead ($160,000/20,000 units) …………………………………………….

8.00

Total production cost per unit ……………………………………………………….

$48.00

Quick Study 19-5 (10 minutes)

Cost per unit using variable costing

Per unit

Direct materials ……………………………………………………………………………….

$10.00

Direct labor …………………………………………………………………………….……..

20.00

Variable overhead …………………………………………………………………..……….

10.00

Total production cost per unit ……………………………………………………….

$40.00

Quick Study 19-6 (15 minutes)

ACES INC.

Variable Costing Income Statement

Sales (4,900 units x $90 per unit) ………………………..…

$441,000

Variable expenses

Var. manuf. expense (4,900 units x $25) …………….…….

$122,500

Var. selling and admin. expense (4,900 x $2) ……..…….

9,800

Total variable expenses ………………………………………….

132,300

Contribution margin …………………………………………..…….

308,700

Fixed expenses

Fixed manufacturing overhead …………………………..

78,000

Fixed selling and administrative expenses ………..…….

65,200

Total fixed expenses ………………………………………..…….

143,200

Net income ……………………………………………………………….

$165,500

Financial & Managerial Accounting, 5th Edition

1060

Quick Study 19-7 (10 minutes)

ACES INC.

Absorption Costing Income Statement

Sales (4,900 units x $90 per unit) ………………………………………….….

$441,000

Cost of goods sold (4,900 units x $38 per unit*) …………………….….

186,200

Gross margin ……………………………………………………………………….….

$254,800

Selling and administrative expenses

Variable (4,900 units x $2 per unit) ……………………………………..….

9,800

Fixed ……………………………………………………………………………………

65,200

Total selling and administrative expenses …………………………..

75,000

Net income …………………………………………………………………………..

$179,800

* Fixed overhead cost is $13 per unit, computed as ($78,000 fixed overhead cost/6,000

units). Total production cost at 6,000 units is $25 variable + $13 fixed = $38.

Quick Study 19-8 (10 minutes)

Assuming 20,000 units produced and 20,000 units sold

RAMORT COMPANY

Gross Margin

Sales (20,000 units x $60/unit) ……………………………………………………….

$1,200,000

Cost of goods sold (20,000 units x $27 per unit*) ……………………..……

540,000

Gross profit ……………………………………………………………………………………

$ 660,000

* Direct materials ……………………………..….

$10 per unit

Direct labor ………………………………….….

12 per unit

Variable overhead …………………………..

3 per unit

Fixed overhead ($40,000/20,000 units) ……….

2 per unit

Total cost of production ……………………….

$27 per unit

Quick Study 19-8 (continued)

Assuming 40,000 units produced and 20,000 units sold

RAMORT COMPANY

Gross Margin

Sales (20,000 units x $60/unit) ……………………………………………………….

$1,200,000

Cost of goods sold (20,000 units x $26 per unit*) ……………………..……

520,000

Gross profit ……………………………………………………………………………………

$ 680,000

* Direct materials ……………………………..………………………..

$10 per unit

Direct labor ………………………………….……………………

12 per unit

Variable overhead …………………………..

3 per unit

Fixed overhead ($40,000/40,000 units) …………………………..

1 per unit

Total cost of production …………………………..

$26 per unit

Quick Study 19-9 (5 minutes)

If Ramort uses variable costing, there will be no difference in gross margin

Quick Study 19-10 (10 minutes)

The suggested selling price for the special order ($68 per unit) exceeds the

variable costs per unit ($30 + $18 = $48 per unit). As long as fixed costs do

Quick Study 19-11 (5 minutes)

Total fixed costs = $700,000

Quick Study 19-12 (15 minutes)

Part 1

DIAZ COMPANY

Absorption Costing Income Statement

Sales (50,000 units x $60 per unit) ………………………………………..….

$3,000,000

Cost of goods sold (50,000 units x $32 per unit*) …………………..….

1,600,000

Gross margin ……………………………………………………………………….….

1,400,000

Selling and administrative expenses** ………………………………….….

410,000

Net income ………………………………………………………………………….

$ 990,000

* Variable manufacturing expenses …………………………..

$28 per unit

Fixed manufacturing expenses ($320,000/80,000 units) ….…………………

4 per unit

Total manufacturing cost per unit …………………………..

$32 per unit

** Variable selling and admin. expenses (50,000 x $5) …………………………

$250,000

Fixed selling and administrative expenses ………………..…………

160,000

Total selling and administrative expenses …………………………..

$410,000

Part 2

The difference in income equals $120,000, computed as $990,000 –

$870,000. Diaz’ ending inventory consists of 30,000 units (80,000 units

Quick Study 19-13 (5 minutes)

Variable costing income ……………………………………………………….

$772,200

Fixed overhead in ending inventory (5,200 x $3.00) ……………….….

15,600

Fixed overhead in beginning inventory (7,800 x $3.00) …………..….

(23,400)

Absorption costing income …………………………………………………..….

$764,400

Quick Study 19-14 (5 minutes)

Variable costing income ……………………………………………………….

$250,000

Fixed overhead in ending inventory (48,000 x $0.75) ……………..….

36,000

Fixed overhead in beginning inventory (50,000 x $0.75) …………….

(37,500)

Absorption costing income …………………………………………………..….

$248,500

EXERCISES

Exercise 19-1 (20 minutes)

Part 1

Cost per unit of finished goods using absorption costing:

Direct materials ……………………………………………………………………….

$15 per unit

Direct labor ………………………………………………………………………….….

16 per unit

Variable overhead ($80,000/20,000 units) ………………………………….

4 per unit

Fixed overhead ($160,000/20,000 units) …………………………………….

8 per unit

Total cost per unit ………………………………………………………………..….

$43 per unit

Part 2

Cost per unit of finished goods using variable costing:

Direct materials ……………………………………………………………………….

$15 per unit

Direct labor ………………………………………………………………………….….

16 per unit

Variable overhead ($80,000/20,000 units) ………………………………….

4 per unit

Total cost per unit ………………………………………………………………..….

$35 per unit

Part 3

Cost of ending finished goods inventory using absorption costing:

Part 4

Cost of ending finished goods inventory using variable costing:

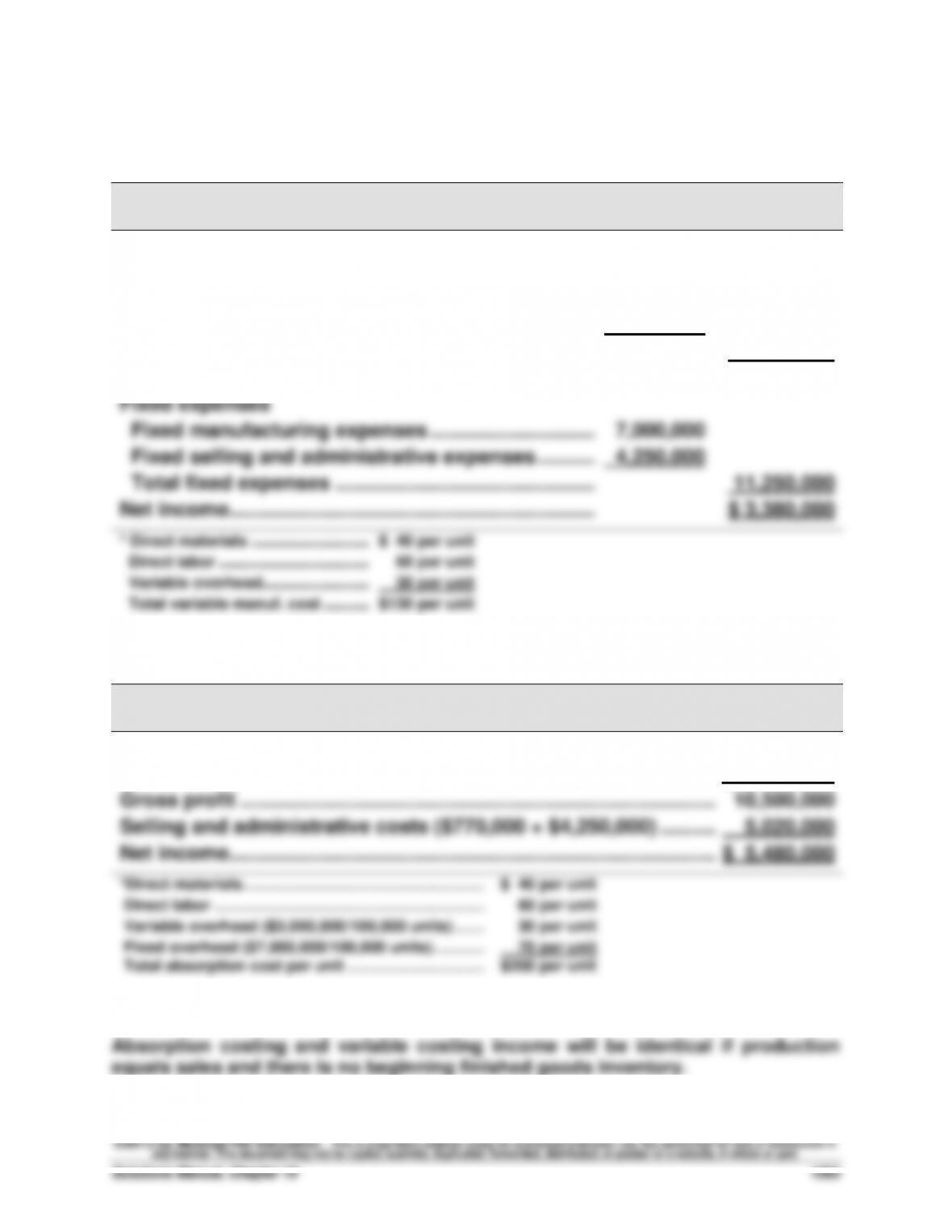

Exercise 19-2 (25 minutes)

Part 1

SIMS COMPANY

Variable Costing Income Statement

Sales (70,000 units x $350/unit) …………………………..

$24,500,000

Variable expenses

Var. manuf. expense (70,000 units x 130/unit*) …..…….

$9,100,000

Var. selling and administrative expense ………………….

770,000

Total variable expenses ………………………………………….

9,870,000

Contribution margin …………………………………………..…….

14,630,000

Fixed expenses

Fixed manufacturing expenses …………………………..

7,000,000

Fixed selling and administrative expenses ………..…….

4,250,000

Total fixed expenses ………………………………………..…….

11,250,000

Net income ……………………………………………………………….

$ 3,380,000

* Direct materials ………………….……….

$ 40 per unit

Direct labor ……………………….….

60 per unit

Variable overhead ………………..…………

30 per unit

Total variable manuf. cost …………………..

$130 per unit

Part 2

SIMS COMPANY

Absorption Costing Income Statement

Sales (70,000 units x $350 per unit) ……………………………………….…

$24,500,000

Cost of goods sold (70,000 units x $200 per unit*)………………….…

14,000,000

Gross profit ………………………………………………………………………….…

10,500,000

Selling and administrative costs ($770,000 + $4,250,000) ……….…

5,020,000

Net income ………………………………………………………………………………

$ 5,480,000

*Direct materials ………………………………………………..

$ 40 per unit

Direct labor ………………………………………………………

60 per unit

Variable overhead ($3,000,000/100,000 units) …….

30 per unit

Fixed overhead ($7,000,000/100,000 units) …………

70 per unit

Total absorption cost per unit …………………………..

$200 per unit

Part 3

Exercise 19-3 (15 minutes)

Part 1

KENZI KAYAKING

Variable Costing Income Statement

Sales (800 x $1,050) ……………………………………………….

$840,000

Variable expenses

Variable production costs (800 x $400) ………………..

$320,000

Variable selling and administrative expenses ……...

75,000

Total variable expenses ……………………………………...

395,000

Contribution margin ……………………………………………...

445,000

Fixed expenses

Fixed manufacturing costs ………………………………….

105,000

Fixed selling and administrative expenses …………..

155,000

Total fixed expenses …………………………………………..

260,000

Net income …………………………………………………………….

$185,000

Part 2

The absorption costing income is $25,000 higher than the variable costing

Exercise 19-4 (10 minutes)

Total fixed costs = $160,000 + $200,000 = $360,000

Exercise 19-5 (15 minutes)

Part 1

HAYEK FURNACES

Absorption Costing Income Statement

Sales (225 units x $1,600 per unit) …………………………………………..………..

$360,000

Cost of goods sold (225 units x $775 per unit*) ………………………..…

174,375

Gross profit ……………………………………………………………………………………

185,625

Selling and administrative expense ($14,625 + $75,000) …………..………..

89,625

Net income ……………………………………………………………………………..…….

$ 96,000

* Production cost per unit:

Variable production costs ………………………………..….

$625

Fixed overhead ($56,250 / 375 units) …………………….

150

Total production costs ……………………………………..….

$775

Part 2

The absorption costing income is $22,500 ($96,000 – $73,500) higher than

Exercise 19-6 (25 minutes)

Part 1

OAK MART COMPANY

Variable Costing Income Statement

Sales (118,000 units x $320 per unit) ………………..…….

$37,760,000

Variable expenses

Variable production costs* …………………………….…….

$15,355,000

Variable selling and administrative expenses ……….

1,416,000

Total variable expenses ……………………………………….

16,771,000

Contribution margin ………………………………………..…….

20,989,000

Fixed expenses

Fixed manufacturing costs …………………………….…….

7,400,000

Fixed selling and administrative expenses ……..…….

4,600,000

Total fixed expenses ……………………………………..…….

12,000,000

Net income ……………………………………………………….

$ 8,989,000

*Beginning variable finished goods ……………….……….

$ 405,000

Variable cost of goods manufactured

Direct materials ($40 x 115,000) …………………….…….

4,600,000

Direct labor ($62 x 115,000) …………………………..

7,130,000

Variable overhead ………………………………………..……….

3,220,000

Total variable costs available ……………………….….

15,355,000

Less ending finished goods…………………………..

0

Variable production costs of goods sold ……………….

$15,355,000

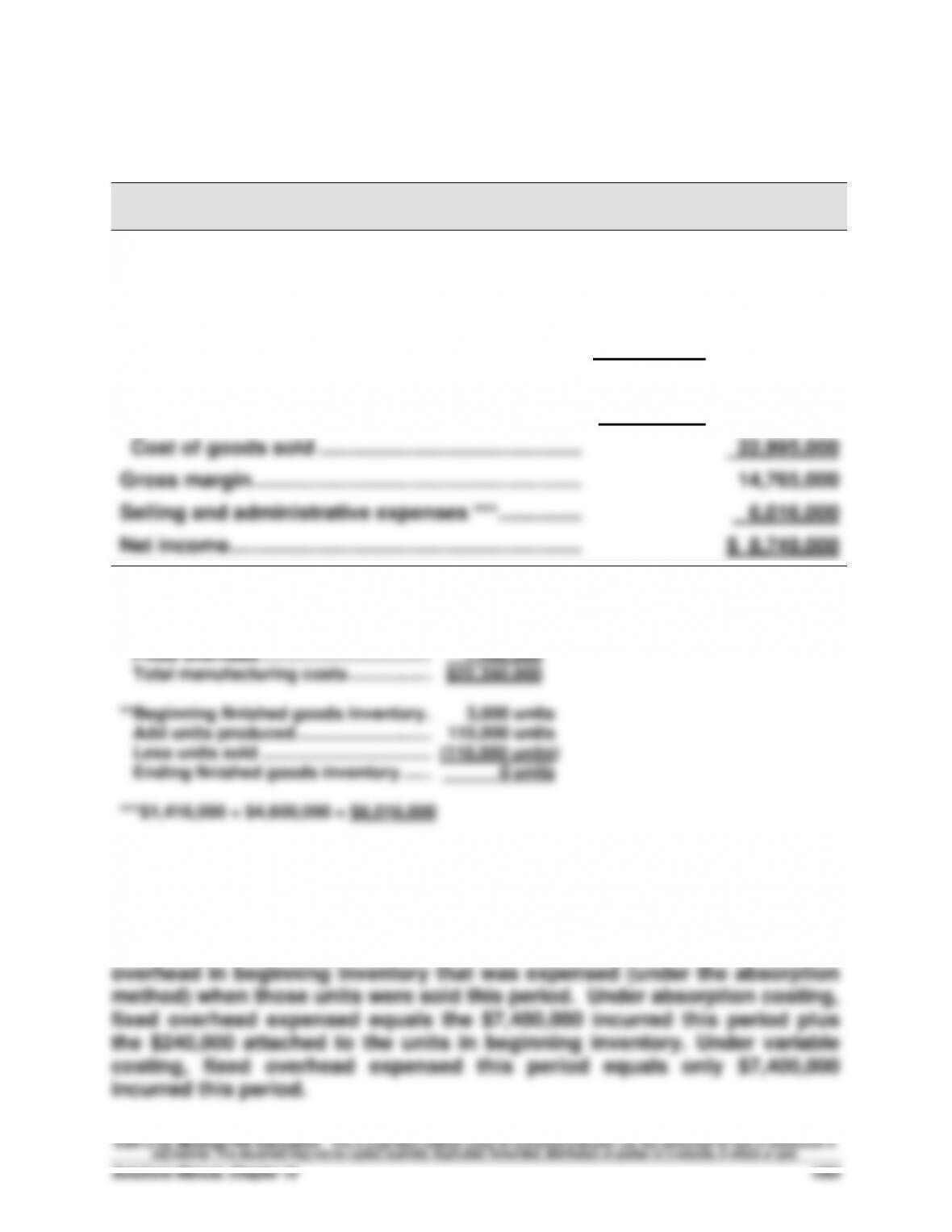

Exercise 19-6 (concluded)

Part 2

OAK MART COMPANY

Absorption Costing Income Statement

Sales (118,000 units x $320 per unit) ………………..…….

$37,760,000

Cost of goods sold

Beginning finished goods …………………………………….

$ 645,000

Cost of goods manufactured * ……………………….….

22,350,000

Goods available for sale ………………………………..…….

22,995,000

Less ending finished goods ** ……………………….….

0

Cost of goods sold ………………………………………..…….

22,995,000

Gross margin …………………………………………………..…..

14,765,000

Selling and administrative expenses *** ………………….

6,016,000

Net income ……………………………………………………….

$ 8,749,000

* Direct materials ($40 x 115,000) ………

$ 4,600,000

Direct labor ($62 x 115,000)…………….

7,130,000

Variable overhead ………………………….

3,220,000

Fixed overhead ……………………………..

7,400,000

Total manufacturing costs ……………..

$22,350,000

**Beginning finished goods inventory .

3,000 units

Add units produced ……………………….

115,000 units

Less units sold ……………………………..

(118,000 units)

Ending finished goods inventory ……

0 units

***$1,416,000 + $4,600,000 = $6,016,000

Part 3

Variable costing income is $240,000 ($8,989,000 – $8,749,000) higher than

the absorption costing income. This is equal to the $240,000 of fixed