Chapter 19 Variable Costing and Performance Reporting

Chapter 19

Variable Costing and

Performance Reporting

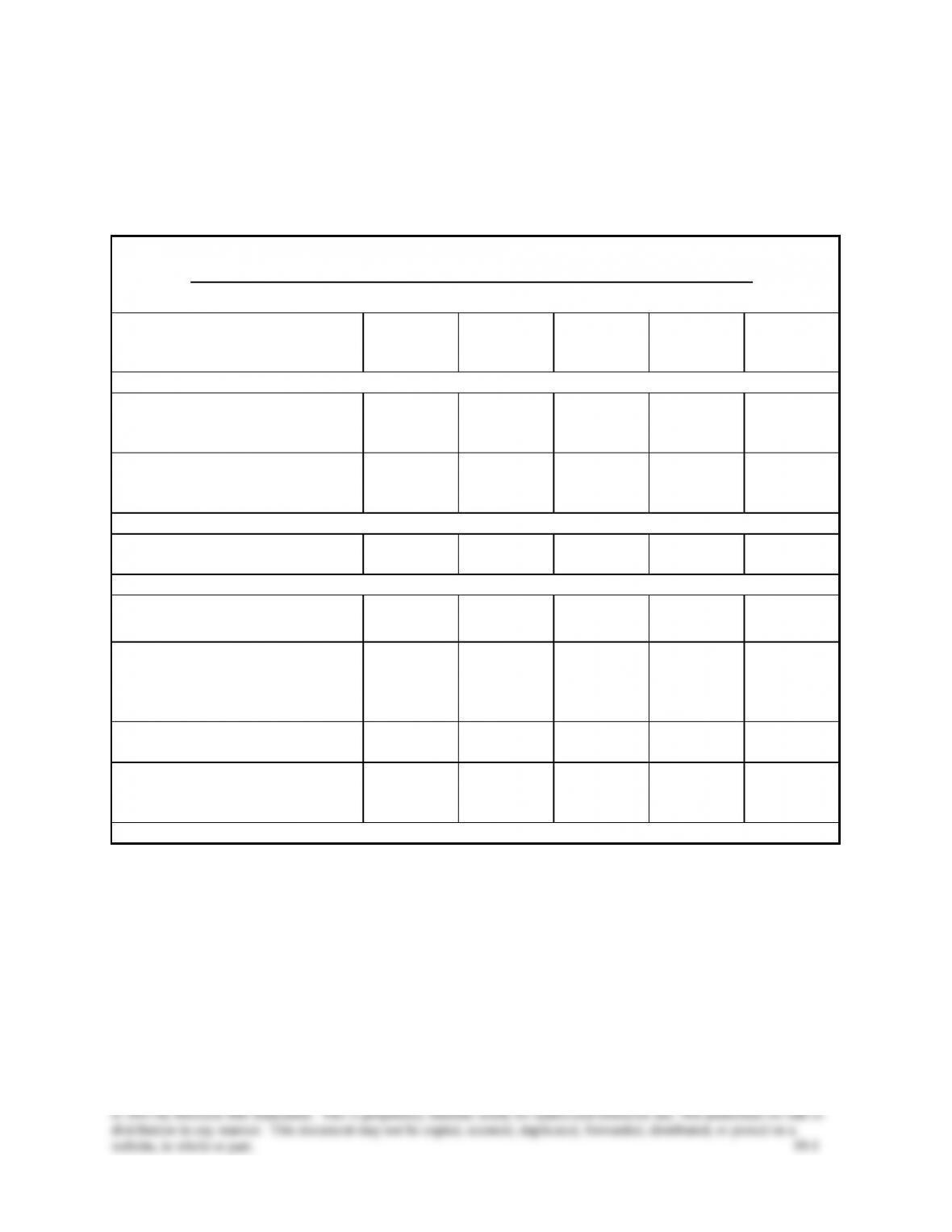

Student Learning Objectives and Related Assignment Materials*

Student Learning Objectives

Discussion

Questions

Quick

Studies

Exercises

Problems**

(A & B set)

Beyond the

Numbers

Conceptual objectives:

C1. Describe how absorption

costing can result in over

production.

2, 3, 4, 5, 8

19-1

19-10

19-5

CIP

C2. Explain the role of variable

costing in pricing special

orders.

1, 4, 6, 7, 9,

10, 14

19-10

19-7

19-4

HTR

Analytical objectives:

A1. Compute and interpret

breakeven volume in units.

19-11

19-4

19-2

Procedural objectives:

P1. Compute unit cost under both

absorption and variable costing.

12

19-4, 19-5

19-1, 19-9

P2. Prepare and analyze an income

statement using absorption

costing and using variable

costing.

3

19-6, 19-7,

19-9

19-2, 19-3,

19-5, 19-6,

19-9, 19-12

19-1, 19-3,

19-5

RIA, CA,

EC, TTN,

TIA, GD

P3. Prepare a contribution margin

report.

9, 11

19-2, 19-3,

19-8

19-8, 11

P4. Convert income under variable

costing to the absorption cost

basis.

19-12, 19-13,

19-14

19-3, 19-5,

19-6

19-1, 19-3

ED

Notes appear on next page.

Chapter 19 Variable Costing and Performance Reporting

* Assignment materials that can be completed by students using:

Sage 50 and QuickBooks Pro 2013 templates – None.

Excel templates – None.

** The Serial Problem for Success Systems, which covers numerous learning objectives, can be

of the chapters. Even if previous segments are not assigned, students can begin the problem in any

chapter. It is most readily solved if students use the Working Papers that accompany the book.)

Synopsis of Chapter Revisions

• Guy Brown: NEW opener with new entrepreneurial assignment

• New Global View with reference to McDonald’s international operations

• Revised section on limitations of variable costing

• New discussion of absorption costing and IFRS

• Revised several exhibits for better learning

• Enhanced examples of absorption and variable costing and their differences

• Added new assignments for better learning

Chapter 19 Variable Costing and Performance Reporting

Chapter Outline

Notes

I. Introducing Variable Costing and Absorption Costing – under the

traditional costing approach, absorption costing, or full costing,

products absorb all costs incurred to product them which can result in

misleading product cost information for decision-making. Under

variable costing only costs that change in total with changes in

production level are included in product costs.

A. Under both methods direct materials, direct labor and variable

overhead are included in product costs.

B. Key difference is in treatment of fixed overhead.

C. Fixed overhead is included in product costs under absorption costs

and included in period expenses under variable costing.

D. Computing Unit Cost

1. For absorption costing, the product unit cost consists of direct

labor, direct materials, variable overhead, and fixed overhead.

2. For variable costing, the product units cost consists of direct

labor, direct materials and variable overhead. Fixed overhead

costs are treated as period costs and recorded as expense in the

period incurred.

3. The difference between the two costing methods is the

exclusion of fixed overhead from product cost for variable

costing.

II. Performance Reporting (Income) Implications

A. Units Produced Equal Units Sold

1. The income statement under variable costing is referred to as

2. Contribution Margin Report is a performance report that

excludes fixed expenses and net income and focuses on

revenue minus variable costs.

4. When quantity produced equals quantity sold, there is no

difference in total costs assigned, but there is a difference in

B. Units Produced Exceed Units Sold

1. Under variable costing, the entire fixed overhead is treated as

2. Under absorption costing, the fixed overhead cost is allocated

to each unit.

3. When production exceeds sales, the fixed overhead cost

allocated to these units is carried as part of the cost of ending

Chapter 19 Variable Costing and Performance Reporting

Chapter Outline

reported in cost of goods sold when the products are sold.

4. Income under absorption costing is higher than income

under variable costing when units produced exceed units

sold because of the greater fixed overhead cost allocated

to ending inventory.

Notes

C. Units Produced are Less Than Units Sold

1. Ending inventory under absorption costing is higher than

under variable costing.

2. Income under absorption costing is less than income under

variable costing.

3. Cost differences extend to both cost of goods sold and period

costs.

D. Summarizing Income Reporting

2. Income will be different whenever the quantity produced and

quantity sold are different.

3. Income under absorption costing is higher when more units

are produced relative to sales and is lower when fewer units

are produced than sold.

normally see differences in income for these two methods

extending over several years.

5. Converting Reports Under Variable Costing to Absorption

Costing – an income statement using the variable costing

method is restated under absorption costing by adding the

E. Converting Income Under Variable Costing to Absorption

cost in ending inventory and subtracting the fixed overhead cost in

beginning inventory.

III. Comparing Variable Costing and Absorption Costing

A. Planning Production

1. Production levels should be based on reliable sales forecasts.

Over-production and inventory build-up can occur because

many companies link manager bonuses to income computed

under absorption costing since this is how income is reported

to shareholders per GAAP.

2. Inventory build-up leads to increased costs in storage,

financing, and obsolescence. If excess inventory is never sold,

it will be disposed of at a loss.

Chapter 19 Variable Costing and Performance Reporting

Chapter Outline

Notes

3. Managers cannot increase income under variable costing by

merely increasing production without increasing sales.

4. Under absorption costing, fixed overhead per unit is lower

when more units are produced so fixed overhead cost is

allocated to more units. If these excess units are not sold, the

fixed overhead cost allocated to these units is not expensed

until a future period when these units are sold.

5. Reported income under variable costing is not affected by

production level changes because all fixed production costs

are expensed in the year incurred. Under this method,

companies increase income by selling more units since it is

not possible to increase income just by producing more units

and creating excess inventory.

B. Setting Prices

1. Cost information is a crucial factor in setting prices.

2. Over the long run, the selling price must be high enough to

cover all costs and still provide an acceptable return to

shareholders.

3. Absorption cost information is useful since it reflects the full

costs that sales must exceed for the company to be profitable.

4. Managers should accept special orders provided the special

change in the short run regardless of rejecting or accepting the

order. Using variable costing reveals the special orders

C. Controlling Costs

1. A cost is controllable if a manager has the power to determine

or at least markedly affect the amount incurred. An effective

cost control practice is to hold managers responsible only for

their controllable costs.

controlled at different levels of management.

4. Variable selling and administrative costs are usually controlled

5. Higher-level managers usually make fixed costs decisions.

6. Lower-level managers usually make most variable cost

decisions.

7. An income statement prepared in the contribution format

highlights the impact of each cost element for income which

makes it easier to identify problem areas and take cost control

Chapter 19 Variable Costing and Performance Reporting

Chapter Outline

measures by appropriate levels of management. This approach is

also useful in evaluating the performance of managers of different

segments within a company.

D. Limitations of Reports Using Variable Costing – Absorption

costing is the only acceptable basis for external reporting under

both U.S. GAAP and IFRS. For income tax purposes, absorption

costing is the only acceptable basis for filings with the IRS under

the Tax Reform Act of 1986.

Notes

IV. Variable Costing for Service Firms – variable costing also applies to

service companies. Service companies do not have inventory but a

focus on variable costs is still useful for managerial decisions.

V. Global View – U.S. multination companies must change their business

processes when moving their operations to international locations.

McDonald’s and Yum Brands offer delivery services in heavily

populated cities which discourage the building of drive-through

facilities which would increase fixed overhead costs. As fixed

overhead costs decrease, the difference in net income that would result

from applying variable costing versus absorption costing also

decreases.

VI. Decision Analysis – Break-Even Analysis

A. If the income statement is prepared under absorption costing, the

data needed for CVP analysis are not readily available.

Substantial effort is required to go back and reclassify the cost

data to obtain information necessary for conducting CVP analysis.

B. If the income statement is prepared using the contribution format,

the data needed for CVP analysis are readily available.

C. Contribution margin per unit = sales price per unit – variable cost

per unit.

website, in whole or part. 19-7

Chapter 19 Alternative Demonstration Problem

Major Company began operations on January 1, 2013. Cost and sales information

for its first two calendar years are summarized below:

Manufacturing costs:

Direct materials $50 per unit

Direct labor $25 per unit

Factory overhead costs for the year:

Variable overhead $10 per unit

Fixed overhead $1,000,000

Nonmanufacturing costs:

Variable selling and administrative $10 per unit

Fixed selling and administrative $5,000,000

Production and sales data:

Units produced, 2013 100,000 units

Units sold, 2013 80,000 units

Units in ending inventory, 2013 20,000 units

Units produced, 2014 60,000 units

Units sold, 2014 80,000 units

Units in ending inventory, 2014 0 units

Sales price per unit $500 per unit

Required:

1. Prepare an income statement for the company for 2013 under absorption

costing.

2. Prepare an income statement for the company for 2013 under variable

costing.

3. Prepare an income statement for the company for 2014 under absorption

costing.

4. Prepare an income statement for the company for 2014 under variable

costing.

5. Prepare a schedule to convert variable costing income to absorption

costing income for the years 2013 and 2014.

Chapter 19 Variable Costing and Performance Reporting

website, in whole or part. 19-8

Solution: Chapter 19 Alternative Demonstration Problem #1

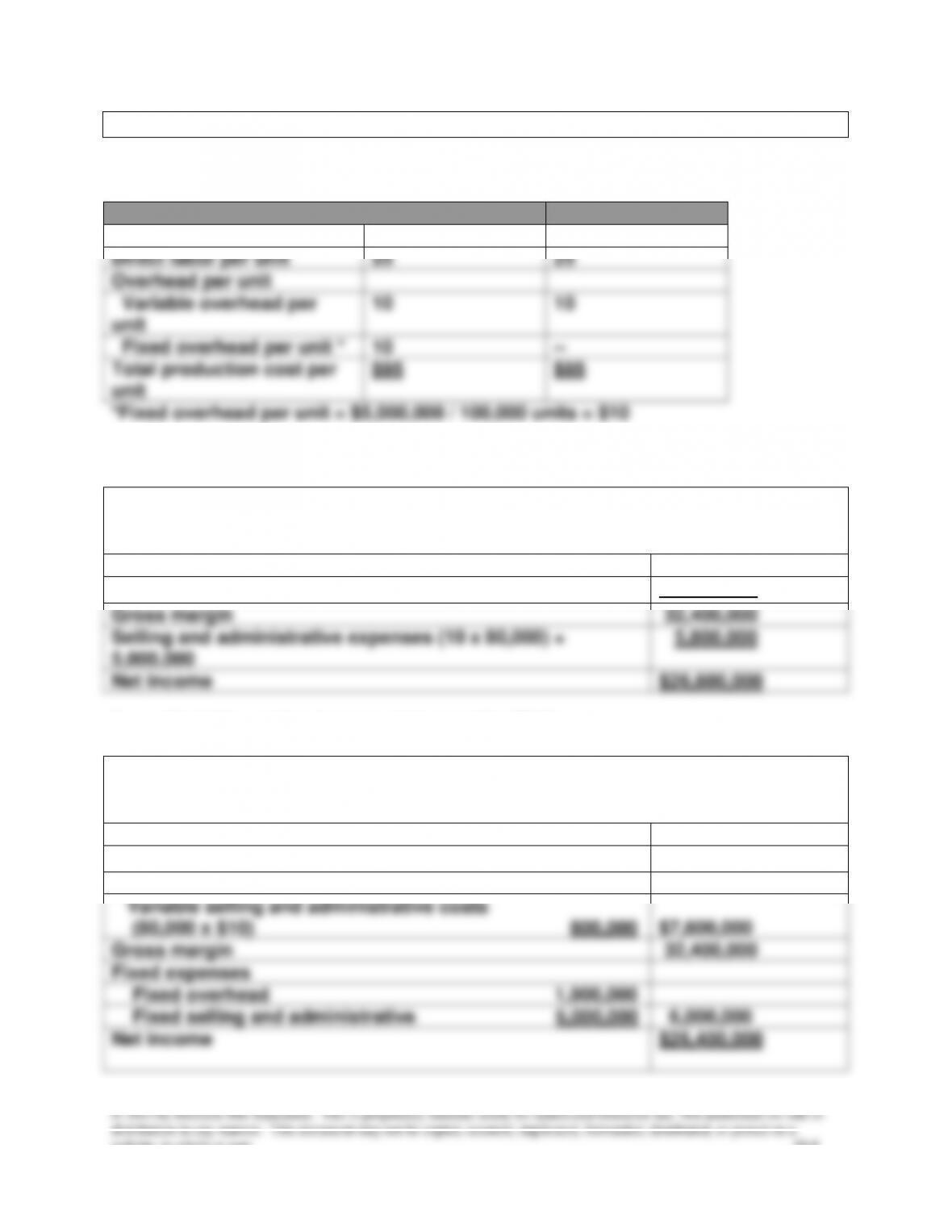

Compute unit costs for 2013 under the two costing methods as follows:

Absorption Costing

Variable Costing

Direct materials per unit

$50

$50

Direct labor per unit

25

25

Overhead per unit

Variable overhead per

unit

10

10

Fixed overhead per unit *

10

—

Total production cost per

unit

$95

$85

*Fixed overhead per unit = $5,000,000 / 100,000 units = $10

1. Absorption costing income statement for 2013:

Major Corporation

Income Statement

For Year Ended December 31, 2013

Sales (80,000 x $500)

$40,000,000

Cost of goods sold (80,000 x $95)

7,600,000

Gross margin

32,400,000

Selling and administrative expenses (10 x 80,000) +

5,000,000

5,800,000

Net income

$26,600,000

2. Variable costing income statement for 2013:

Major Corporation

Income Statement (Contribution Format)

For Year Ended December 31, 2013

Sales (80,000 x $500)

$40,000,000

Variable expenses

Variable production costs (80,000 x $85) $6,800,000

Variable selling and administrative costs

(80,000 x $10) 800,000

$7,600,000

Gross margin

32,400,000

Fixed expenses

Fixed overhead 1,000,000

Fixed selling and administrative 5,000,000

6,000,000

Net income

$26,400,000

Chapter 19 Variable Costing and Performance Reporting

website, in whole or part. 19-9

Solution: Chapter 19 Alternative Demonstration Problem #1, Continued

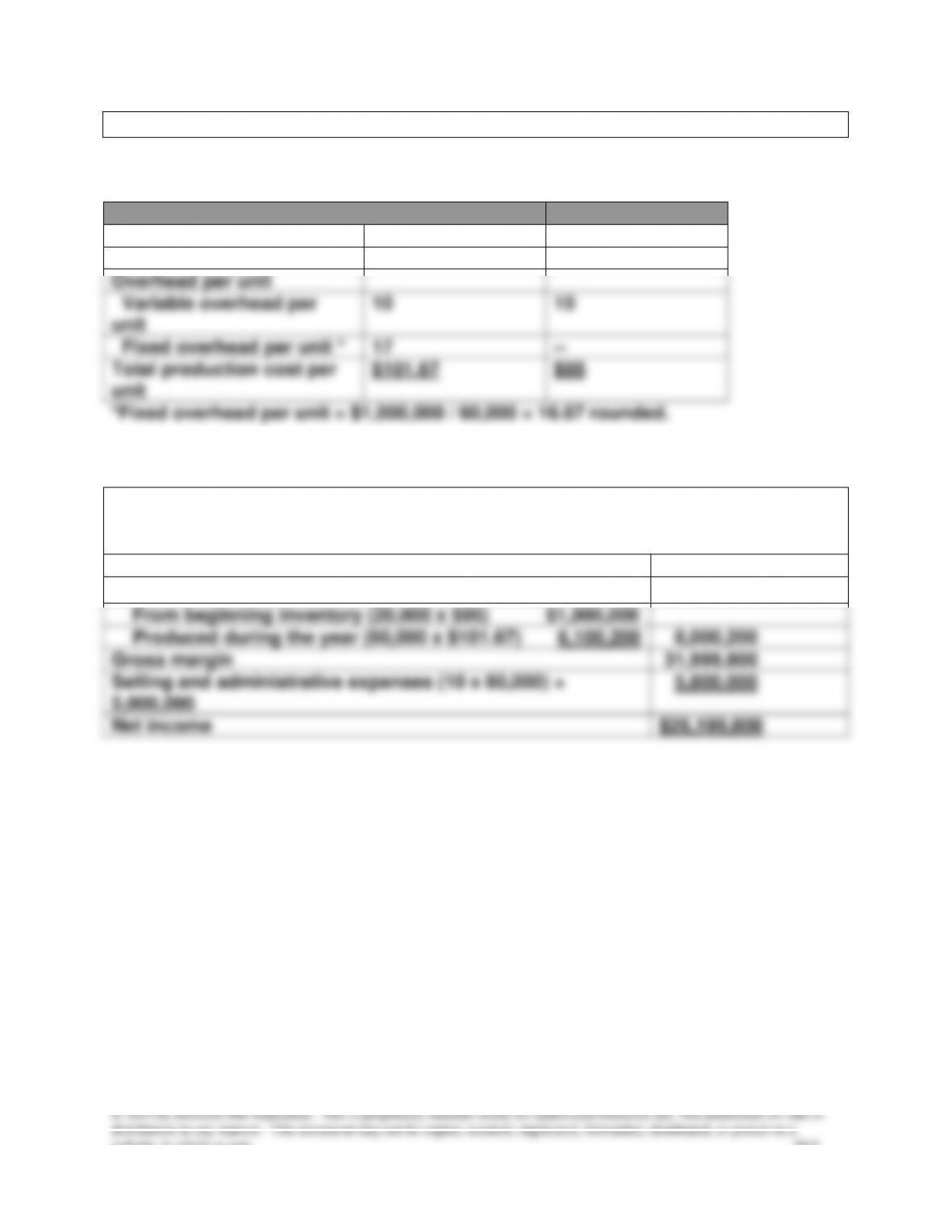

Compute unit costs for 2014 under the two costing methods as follows:

Absorption Costing

Variable Costing

Direct materials per unit

$50

$50

Direct labor per unit

25

25

Overhead per unit

Variable overhead per

unit

10

10

Fixed overhead per unit *

17

—

Total production cost per

unit

$101.67

$85

*Fixed overhead per unit = $1,000,000 / 60,000 = 16.67 rounded.

3. Absorption costing income statement for 2014:

Major Corporation

Income Statement

For Year Ended December 31, 2014

Sales (80,000 x $500)

$40,000,000

Cost of goods sold

From beginning inventory (20,000 x $95) $1,900,000

Produced during the year (60,000 x $101.67) 6,100,200

8,000,200

Gross margin

31,999,800

Selling and administrative expenses (10 x 80,000) +

5,000,000

5,800,000

Net income

$26,199,800

Chapter 19 Variable Costing and Performance Reporting

website, in whole or part. 19–10

Solution: Chapter 19 Alternative Demonstration Problem #1 Continued

4. Variable costing income statement for 2014:

Major Corporation

Income Statement (Contribution Format)

For Year Ended December 31, 2014

Sales (80,000 x $500)

$40,000,000

Variable expenses

Variable production costs (80,000 x $85) $6,800,000

Variable selling and administrative costs

(80,000 x $10) 800,000

$7,600,000

Gross margin

32,400,000

Fixed expenses

Fixed overhead 1,000,000

Fixed selling and administrative 5,000,000

6,000,000

Net income

$26,400,000

5. Conversion of variable costing income to absorption costing income:

2012

2013

Variable costing income

$26,400,000

$26,400,000

Add: Fixed overhead cost deferred in

ending inventory (20,000 x $10)

200,000

0

Less: Fixed overhead cost recognized

from beginning inventory (20,000 x $10)

0

(200,000)

Absorption costing income

$26,600,000

$26,200,000