Financial & Managerial Accounting, 5th Edition

1022

Exercise 18-17 (25 minutes)

1. Selling price per composite unit

8 windows @ $200 per unit ……………………………………………………...

$1,600

2 doors @ $500 per unit …………………………………………………………..

1,000

Selling price per composite unit ……………………………………………...

$2,600

2. Variable costs per composite unit

8 windows @ $125 per unit ……………………………………………………...

$1,000

2 doors @ $350 per unit …………………………………………………………..

700

Variable costs per composite unit …………………………..……………....

$1,700

3. Break-even point in composite units

4. Unit sales of windows and doors at break-even point

Windows: 8 x 1,000 units (from 3) ………..…….

8,000 units

Doors: 2 x 1,000 units (from 3) ………..…….

2,000 units

Exercise 18-18 (20 minutes)

Contribution Percentage of Weighted

(1) margin per unit x sales mix = unit CM

Windows ……………………….. $75.00 80% $60

(3) Unit sales of windows and doors at break-even point:

Windows: 80% x 10,000 units (from 2) …………………………..

8,000 units

Doors: 20% x 10,000 units (from 2) …………………………..

2,000 units

Exercise 18-19 (25 minutes)

1. Selling price per composite unit

5 Easy returns @ $50 each …………………………………………………….

$ 250

3 Moderate returns @ $125 each …………………………………………...

375

2 Business returns @ $275 each …………………………………………...

Selling price per composite unit …………………………………………….

550

$1,175

2. Variable costs per composite unit

5 Easy returns @ $30 each …………………………………………………….

$ 150

3 Moderate returns @ $75 each ……………………………………………..

225

2 Business returns @ $100 each ……………………………………………

Variable costs per composite unit …………………………..……………..

200

$ 575

Financial & Managerial Accounting, 5th Edition

1024

Exercise 18-19 (concluded)

3. Break-even point in composite units

Fixed costs .

4. Unit sales of Easy, Moderate, and Business returns at break-even point

Easy: 5 x 30 units (from 3) …………….…….

150 units

Moderate: 3 x 30 units (from 3) …………….…….

90 units

Business: 2 x 30 units (from 3) …………….…….

60 units

Exercise 18-20 (25 minutes)

Contribution Percentage of Weighted

(1) Margin per unit x sales mix = Unit CM

Easy …………………………..…. $ 20 50% $10

Moderate ………………………. 50 30 15

(3) Unit sales of Easy, Moderate, and Business returns at break-even point:

Easy: 50% x 300 units (from 2) ……………

150 units

Moderate: 30% x 300 units (from 2) ……………

90 units

Business: 20% x 300 units (from 2) ……………

60 units

Exercise 18-21 (30 minutes)

Instructor note: This exercise is solved in 3 steps

1. Prepare a contribution margin income statement for Co. A to compute its DOL;

2. Prepare a contribution margin income statement for Co. B to compute its DOL;

3. Analyze and interpret which company benefits more from a 20% sales increase.

Step 1.

Company A

Contribution Margin Income Statement

Sales (given)…………………………………………………………………..

$6,000,000

Variable costs [$6,000,000 x (100% – 60%)] ………………………

2,400,000

Contribution margin ($6,000,000 x 60%) ………………………….

3,600,000

Fixed costs (given) …………………………………………………………

2,600,000

Pretax income ……………………………………………………….……….

$1,000,000

Contribution margin in dollars / Pretax income

$3,600,000 / $1,000,000

Sales (given)…………………………………………………………………..

Variable costs [$4,500,000 x (100% – 25%)] ………………………

Contribution margin ($4,500,000 x 25%) ………………………….

Fixed costs (given) …………………………………………………………

Pretax income ……………………………………………………….……….

$1,125,000 / $750,000

PROBLEM SET A

Problem 18-1A (25 minutes)

Parts 1 and 2

Tom Thompson Company

Contribution Margin Income Statement

For Year Ended December 31, 2013

(1,000 units) Per unit % of sales

Sales ($500 x 1,000) ……………………….

$500,000

$500

100%

Variable costs

Plastic for casing …………………..…….

$17,000

$17

Assembly worker wages ………………..

82,000

82

Drum stands …………………………..

26,000

26

Sales commissions ……………….…….

15,000

140,000

15

140

28%

Contribution margin ………………..…….

360,000

$360

72%

Fixed costs

Taxes on factory …………………….…….

5,000

Factory maintenance ……………………..

10,000

Factory machinery deprec. ……..……..

40,000

Sales equipment lease …………………..

10,000

Accounting staff salaries ………..……..

35,000

Admin. mgmt. salaries …………………..

125,000

225,000

Pretax income …………………………..

135,000

Income tax (25%) ……………………..……

33,750

Net income …………………………..….……..

$101,250

Part 3 Analysis Component

Contribution margin shows how much of total sales are available to cover fixed

costs and contribute to operating income. This is why the title for this statement

is “Contribution Margin Income Statement.” Contribution margin ratio shows

management the percent of each sales dollar that is available to cover fixed costs

and to contribute to operating income. That is, for each $1 of sales, $0.72 is

available both to cover fixed costs and to contribute to operating income.

Problem 18-2A (40 minutes)

Part 1

(a) Instructor note: Use the equation in Exhibit 18.11

Break-even in sales units = Fixed costs / Contribution margin per unit

(b) Instructor note: Use the equation in Exhibit 18.12

Break-even in sales dollars = Fixed costs / Contribution margin ratio

Financial & Managerial Accounting, 5th Edition

1028

Problem 18-2A (Continued)

Part 2

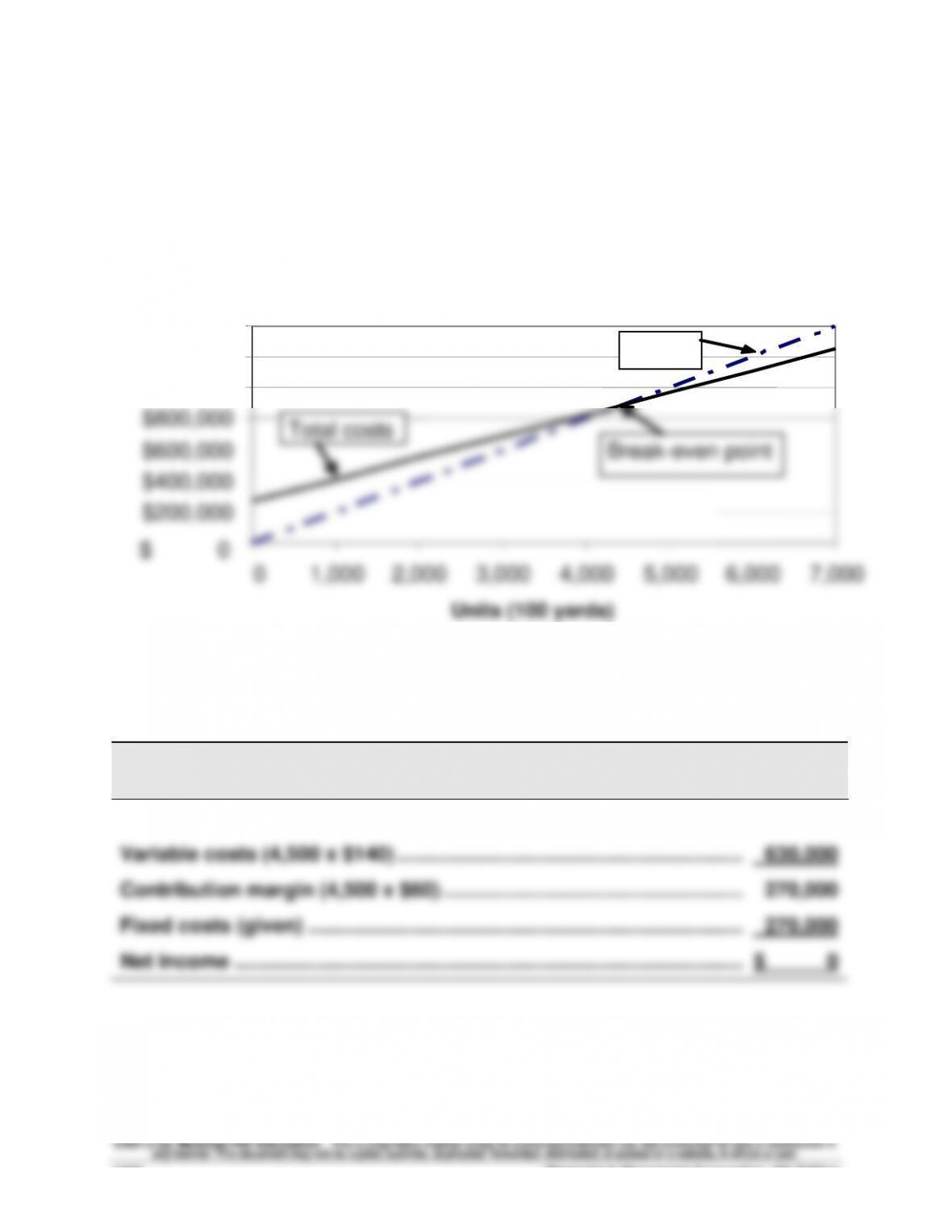

CVP Chart for Xcite Equipment Company

Part 3

XCITE EQUIPMENT CO.

Contribution Margin Income Statement (at Break-Even) — Product XT

Sales (4,500 x $200) ……………………………………………………….…………..

$900,000

Variable costs (4,500 x $140) ……………………………………………………...

630,000

Contribution margin (4,500 x $60) ……………………………………………….

270,000

Fixed costs (given) …………………………………………………………………….

270,000

Net income ………………………………………………………………………………...

$ 0

$ 0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Units (100 yards)

Total costs

Sales

Break-even point

Problem 18-3A (45 minutes)

Parts 1 and 2

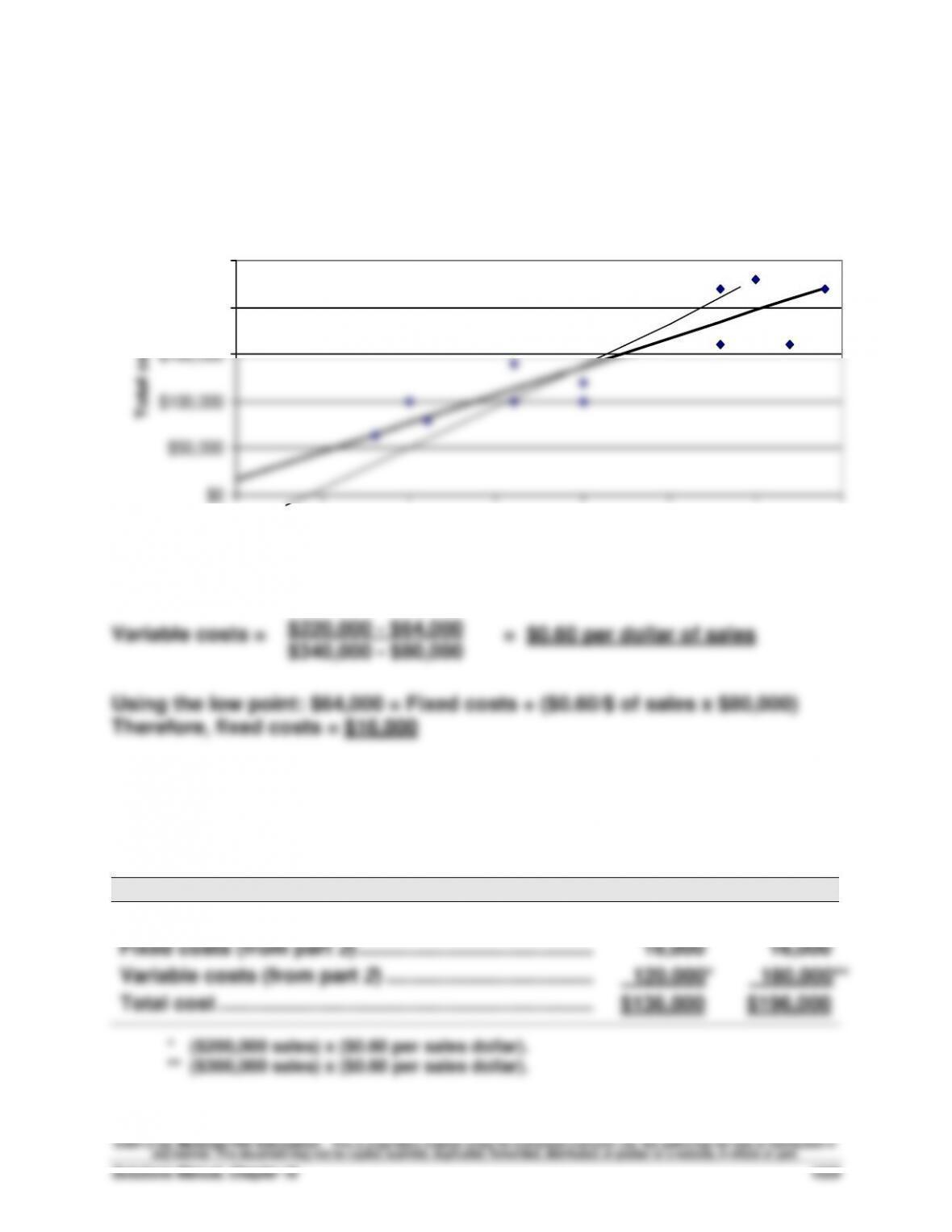

The scatter diagram and its estimated line of cost behavior appear below.

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$0 $50,000 $100,000 $150,000 $200,000 $250,000 $300,000 $350,000

Sales

Total cost

Part 2 – Calculation of variable and fixed costs

Part 3

The estimates in Part 2 can be used to predict the total costs that will be

incurred at sales levels of $200,000 and $300,000.

Predictions

Sales (given) ……………………………………………………….

$200,000

$300,000

Fixed costs (from part 2) …………………………………….….

16,000

16,000

Variable costs (from part 2) ………………………………..….

120,000*

180,000**

Total cost …………………………………………………………..….

$136,000

$196,000

* ($200,000 sales) x ($0.60 per sales dollar).

** ($300,000 sales) x ($0.60 per sales dollar).

$220,000 – $64,000

Alden Co.

Financial & Managerial Accounting, 5th Edition

1030

Problem 18-4A (75 minutes)

Part 1 Instructor note: Use the equation in Exhibit 18.12

2013 break-even in sales dollars = Fixed costs / Contribution margin ratio

Sales price per unit ($1,000,000 / 20,000) ………………………………….……………………

$50

Variable costs per unit ($800,000 / 20,000) ……………………………….…………………….

$40

Contribution margin ratio ($50- $40) / $50) ……………………………….…………………….

20%

Part 2 Instructor note: Use the equation in Exhibit 18.12 with predicted

numbers

2014 break-even in sales dollars = Fixed costs / Contribution margin ratio

2013 fixed costs plus 2014 increase ($250,000 + $200,000) ……….………………….

$450,000

**To compute predicted contribution margin ratio

Predicted sales price per unit (no change in sales price) ………….……………….

$50

Predicted variable costs per unit ($40 x 50%) …………………………..

$20

Predicted contribution margin ratio ($50- $20) / $50) …………………………..

60%

Part 3

ASTRO COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2014

Sales (20,000 x $50) ……………………………………………………….……..…

$1,000,000

Variable costs (20,000 x $20) ……………………………………………………

400,000

Contribution margin (20,000 x $30) ………………………………………..…

600,000

Fixed costs …………………………………………………………………………..…

450,000

Net income ………………………………………………………………………………

$ 150,000

Problem 18–4A (Continued)

Part 4 Instructor note: Use equations in Exhibits 18.22 and 18.23 with

predicted numbers

(Fixed costs + Target pretax income)

Required sales in dollars = Contribution margin ratio

= ($450,000* + $200,000**) / 60%***

= $650,000 / 60.0%

Alternately:

Problem 18-5A (65 minutes)

Part 1 Instructor note: Use the equation in Exhibit 18.12

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Product T:

= $125,000 / 20%*

Problem 18-5A (Continued)

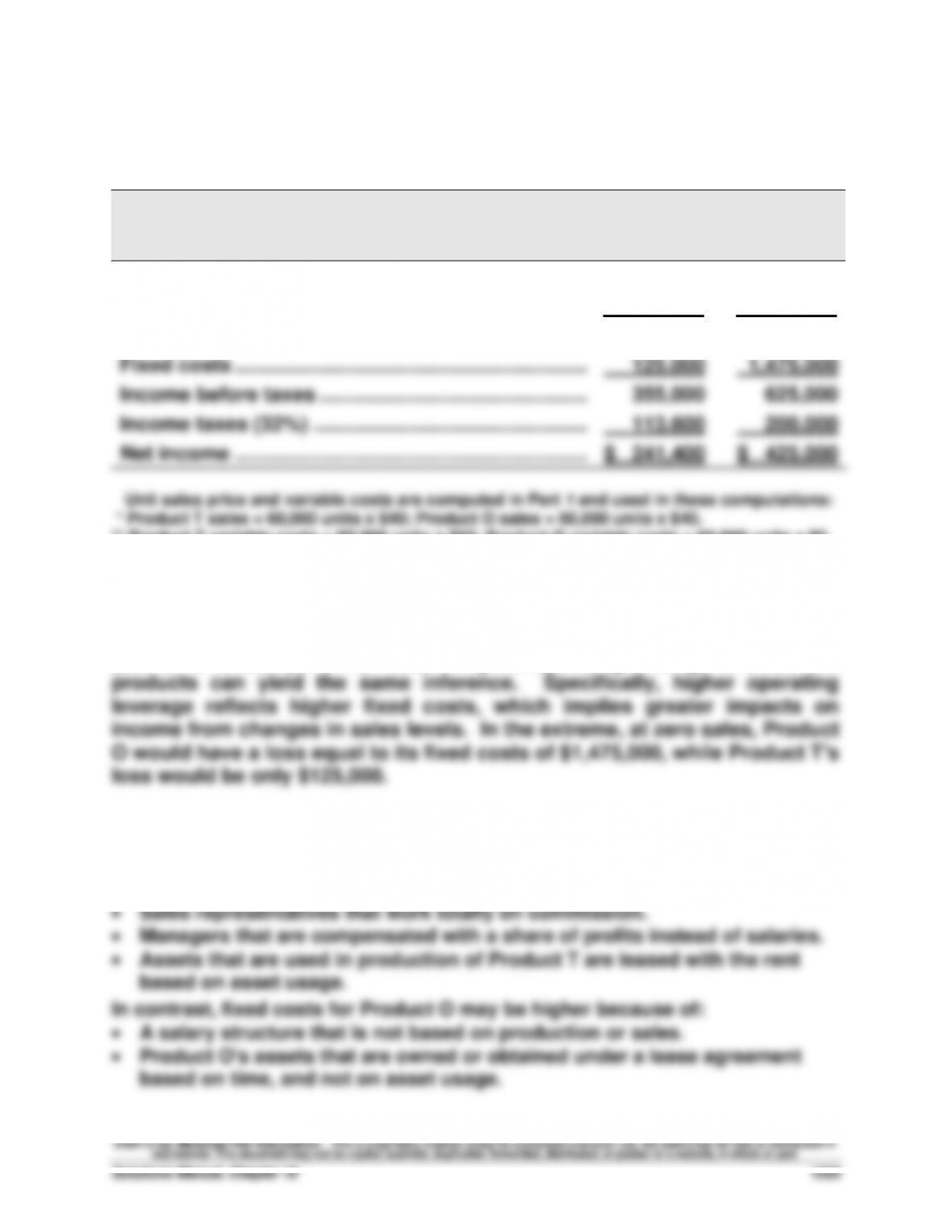

Part 3 Forecasted contribution margin income statements for each product

assuming sales increase to 60,000 units with no change in unit sales price

VANNA CO.

Forecasted Contribution Margin Income Statement

Product T

Product O

Sales* …………………………………………………………………

$2,400,000

$2,400,000

Variable costs** ………………………………………………..…

1,920,000

300,000

Contribution margin ……………………………………………

480,000

2,100,000

Fixed costs ……………………………………………………….

125,000

1,475,000

Income before taxes ……………………………………………

355,000

625,000

Income taxes (32%) ………………………………………….…

113,600

200,000

Net income ……………………………………………………….

$ 241,400

$ 425,000

Unit sales price and variable costs are computed in Part 1 and used in these computations:

* Product T sales = 60,000 units x $40; Product O sales = 60,000 units x $40.

** Product T variable costs = 60,000 units x $32; Product O variable costs = 60,000 units x $5.

Part 4

If sales were to greatly decrease, Product O would suffer the greater loss

because it would lose more contribution margin per unit than Product T

($35 for O versus $8 for T). Examining the operating leverage of these two

Part 5

Factors that could cause Product T to have lower fixed costs might include:

• Labor arrangement that pays workers for units produced.

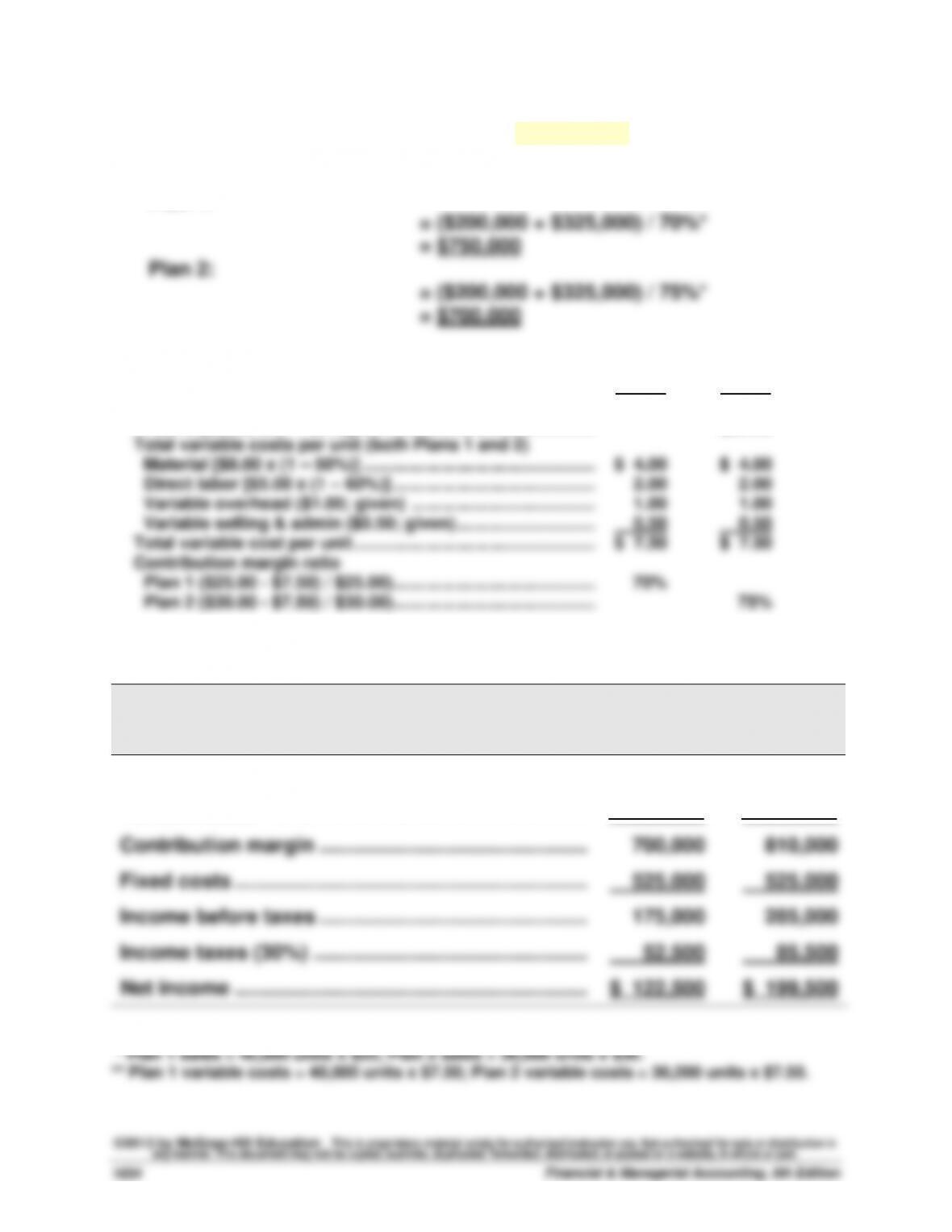

Problem 18-6A (45 minutes)

Part 1 Instructor note: Use the equation in Exhibit 18.12

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Plan 1:

*To compute contribution margin ratio

Sales price per unit

Plan 1 (no change)……………………………………………………....

Plan 2 [$25.00 x (1 + 20%)] ………………………………………….……………

Plan 1

$25.00

Plan 2

$30.00

Total variable costs per unit (both Plans 1 and 2)

Material [$8.00 x (1 – 50%)] ……………………………………………………….

Direct labor [$5.00 x (1 – 60%)] ……………………………………………………….

Variable overhead ($1.00; given) ………………………………..……………………..

Variable selling & admin ($0.50; given) ………………………..…

Total variable cost per unit …………………………………………..…………..

$ 4.00

2.00

1.00

0.50

$ 7.50

$ 4.00

2.00

1.00

0.50

$ 7.50

Contribution margin ratio

Plan 1 ($25.00 – $7.50) / $25.00)……………………………………………………….

Plan 2 ($30.00 – $7.50) / $30.00)……………………………………………………….

70%

75%

Part 2

BERTRAND CO.

Forecasted Contribution Margin Income Statement

Plan 1

Plan 2

Sales* …………………………………………………………………

$1,000,000

$1,080,000

Variable costs** ………………………………………………..…

300,000

270,000

Contribution margin ……………………………………………

700,000

810,000

Fixed costs ……………………………………………………….

525,000

525,000

Income before taxes ……………………………………………

175,000

285,000

Income taxes (30%) ………………………………………….…

52,500

85,500

Net income ……………………………………………………….

$ 122,500

$ 199,500

Unit sales price and variable costs are computed in Part 1 and used in these computations:

Problem 18-7A (50 minutes)

Part 1 BREAK–EVEN ANALYSIS ASSUMING USE OF SAME MATERIALS

Step 1: Compute break-even in composite units—Use equation in Exhibit 18.27

Break-even in composite units = Fixed costs/Contribution margin per composite unit

*To compute the contribution margin per composite unit

Unit Sales Price

Unit Variable Costs

5 units of Red

@ $20 per unit…………………………………………..

@ $12 per unit…………………………………………..

$100

$ 60

4 units of White

@ $35 per unit…………………………………………..

@ $22 per unit…………………………………………..

140

88

2 units of Blue

@ $65 per unit…………………………………………..

@ $50 per unit…………………………………………..

130

____

100

Selling price of a composite unit ………………….

Variable cost of a composite unit …………………

$370

$248

Thus:

Contribution margin per composite unit = $370 – $248 = $122

Contribution margin ratio (rounded) = $122 / $370 = 32.97%

Step 2: Compute break-even in individual product unit sales

Step 3: Compute break-even in individual product dollar sales

Dollar sales of Red at break-even: 10,250 units x $20 = $205,000

Financial & Managerial Accounting, 5th Edition

1036

Problem 18–7A (Continued)

Part 2 BREAK–EVEN ANALYSIS ASSUMING USE OF NEW MATERIALS

Step 1: Compute break-even in composite units—Use equation in Exhibit 18.27

Break-even in composite units = Fixed costs/Contribution margin per composite unit

*To compute the contribution margin per composite unit

Unit Sales Price

Unit Variable Costs

5 units of Red

@ $20 per unit ……………………………………………..

@ ($12 – $6) per unit …………………………………….

$100

$ 30

4 units of White

@ $35 per unit ……………………………………………..

@ ($22 – $12) per unit …………………………………..

140

40

2 units of Blue

@ $65 per unit ……………………………………………..

@ ($50 – $10) per unit …………………………………..

130

____

80

Selling price of a composite unit ……………………..

Variable cost of a composite unit …………………….

$370

$150

Thus:

Contribution margin per composite unit = $370 – $150 = $220

Contribution margin ratio (rounded) = $220/ $370 = 59.46%

Step 2: Compute break-even in individual product unit sales

Unit sales of Red at break-even: 1,364 x 5 = 6,820 units

Unit sales of White at break-even: 1,364 x 4 = 5,456 units

Unit sales of Blue at break-even: 1,364 x 2 = 2,728 units

Step 3: Compute break-even in individual product dollar sales

Dollar sales of Red at break-even: 6,820 units x $20 = $136,400

Dollar sales of White at break-even: 5,456 units x $35 = $190,960

Part 3

When a business invests in fixed assets, as in this case, there is an