Chapter 18

Cost Behavior and Cost-Volume-Profit

Analysis

QUESTIONS

1. A variable cost is one that varies proportionately with the volume of activity. For

2. Variable costs per unit stay the same (remain constant) when output volume

3. Fixed costs per unit decrease when output volume increases. This is because the

4. Cost-volume-profit analysis is especially useful in the planning phase for a

5. A step-wise cost remains constant over a limited range of output activity, outside of

6. Contribution margin ratio means that for each sales dollar a specified percent is

7. Definition: Contribution margin ratio = Contribution margin / Sales price per unit.

8. Definition: Unit contribution margin = Sales price per unit – Variable costs per unit.

9. A CVP analysis for a manufacturing company is simplified by assuming that the

Financial & Managerial Accounting, 5th Edition

1008

10. The first is that although individual costs classified as fixed or variable might not

11. By assuming a relevant range for operating activity, management can more

justifiably assume either fixed or variable relations between costs and volume, and

12. Three common methods for measuring cost behavior are: the scatter diagram, the

13. A scatter diagram is used to display the relation between past costs and sales

15. This line represents total cost, which equals the sum of the fixed and variable costs

16. Fixed costs are depicted as a horizontal line on a CVP chart because they remain the

17. Company A has a contribution margin of 50% [($20,000 – $10,000) / ($20,000)] and

Company B has a contribution margin of 80% [($20,000 – $4,000) / ($20,000)]. This

19. Arctic Cat’s primary variable costs in making snowmobiles are: costs of the

component parts (metals, engine parts, seat components, wiring, gauges, etc.), and

20. Polaris offers a variety of two-, three- and four- wheel vehicles. To adequately

21. A 65% increase in sales of a popular scooter model of Piaggio is likely viewed as a

substantial increase. When this occurs, the sales and cost structures are likely to

QUICK STUDIES

Quick Study 18-1 (10 minutes)

Quick Study 18-2 (10 minutes)

Quick Study 18-3 (10 minutes)

Quick Study 18-4 (15 minutes)

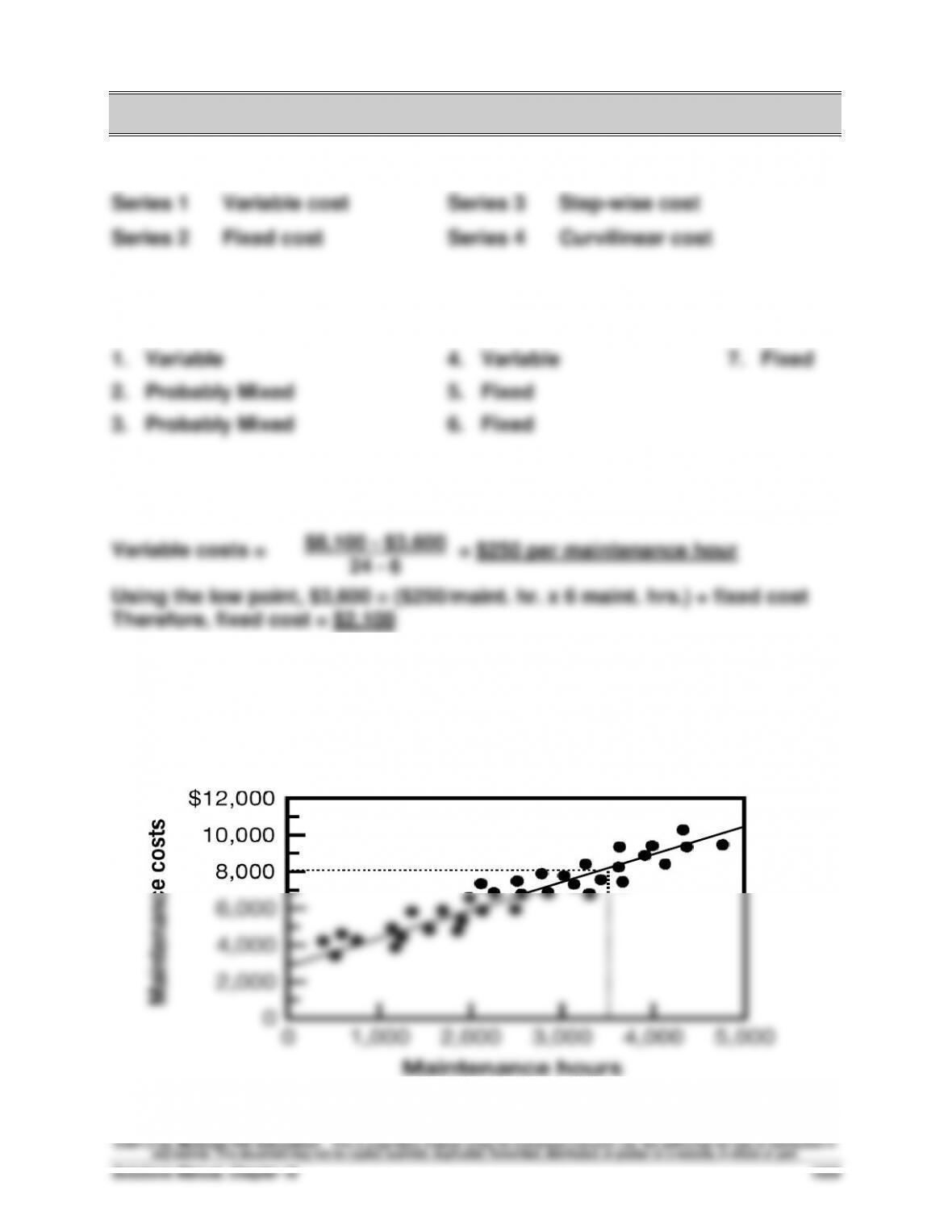

1. Estimated line of cost behavior

Quick Study 18–4 (Concluded)

2. Estimated cost components

Fixed costs = $3,000

Instructor note: Answers to part 2 can vary slightly depending on where students draw the cost

line.

*(rounded)

Quick Study 18-5 (10 minutes)

Contribution margin $5,000 – $3,000 = $2,000

Quick Study 18-6 (10 minutes)

1. Contribution margin per unit = $90 – $36 = $54

Quick Study 18-7 (10 minutes)

Quick Study 18-8 (10 minutes)

1. Contribution margin ratio = = 60%

3,500 – 0

$54

$90

Quick Study 18-9 (10 minutes)

Pretax income = $140,000 / (1 – 0.30) = $200,000

Quick Study 18-10 (5 minutes)

Quick Study 18-11 (15 minutes)

Explanation: Company B has a relatively low proportion of variable costs to

total costs. This means that the contribution margin (sales – variable costs)

for Company B is relatively high. Also, given that the fixed costs for

Quick Study 18-12 (10 minutes)

Number of smart phones sold at break–even: 840 x 3 = 2,520 phones

Financial & Managerial Accounting, 5th Edition

1012

Quick Study 18-13 (10 minutes)

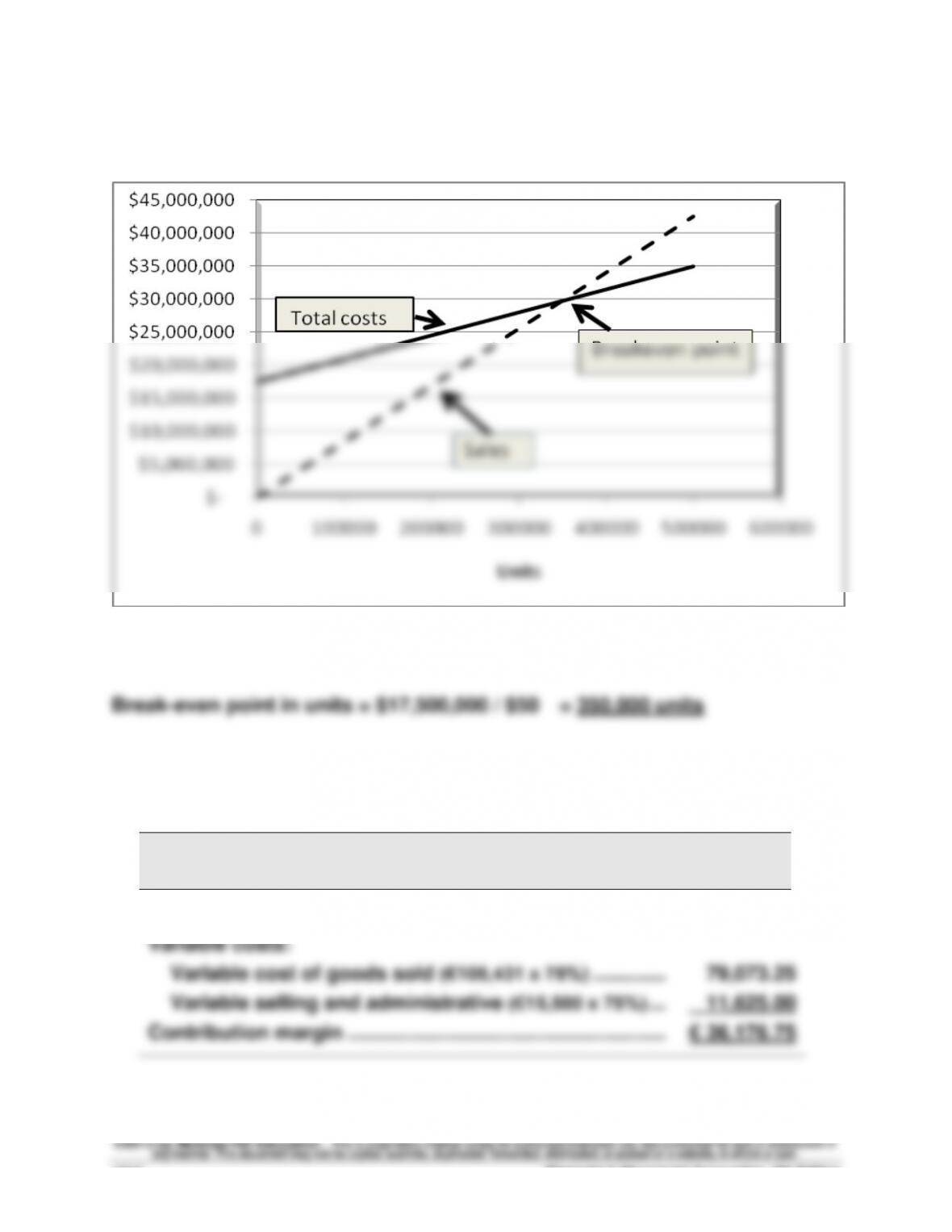

CVP Chart

Notes: Expected sales are 400,000 units ($34 million), thus selling price is $85 per unit.

Fixed costs are $17.5 million, and variable costs are $35 per unit.

Quick Study 18-14 (10 minutes)

VOLKSWAGEN

Contribution Margin Statement (in € millions)

Sales ……………………………………………………………………….…………..

€126,875.00

Variable costs:

Variable cost of goods sold (€105,431 x 75%) ………….……………..

79,073.25

Variable selling and administrative (€15,500 x 75%) ………………..

11,625.00

Contribution margin ……………………………………………………….

€ 36,176.75

EXERCISES

Exercise 18-1 (20 minutes)

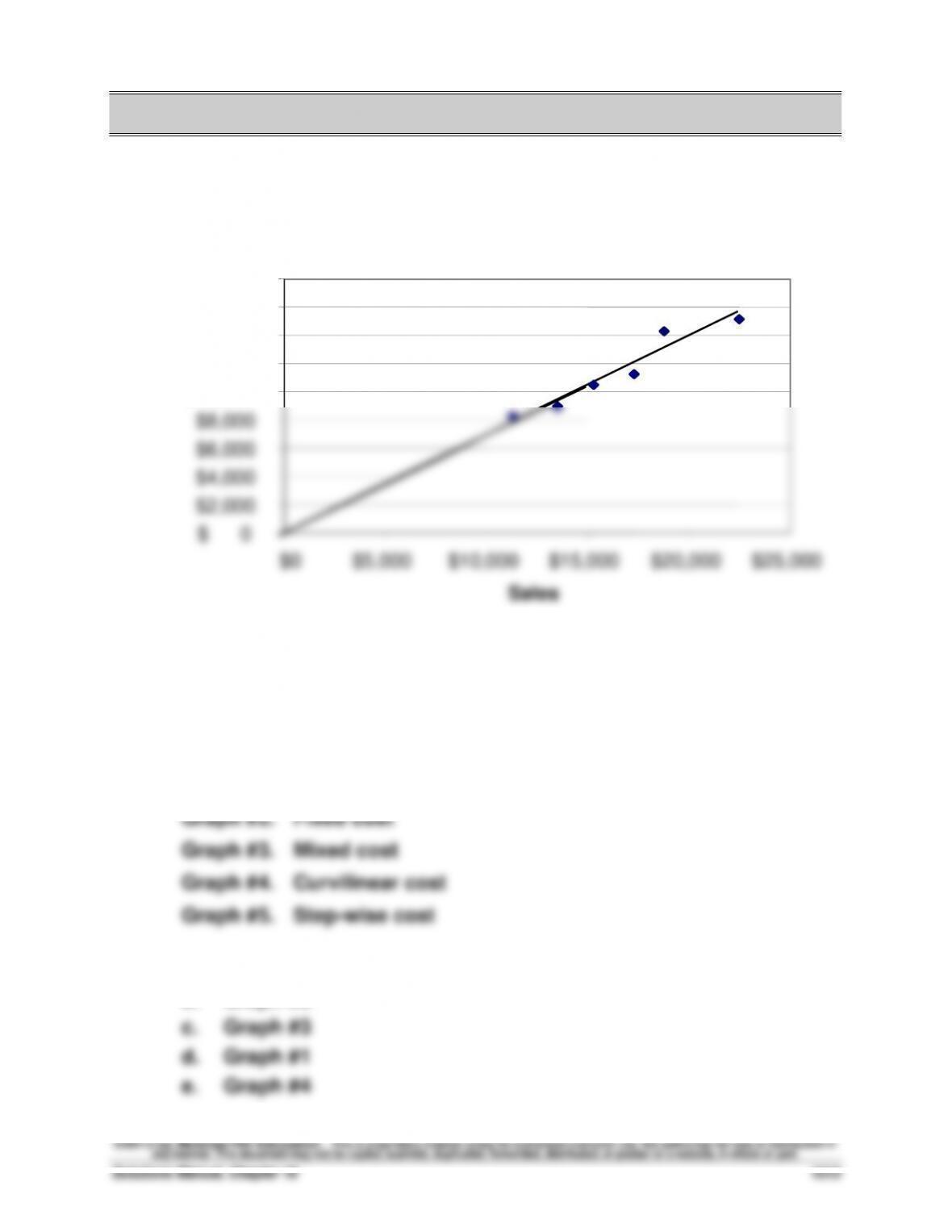

The scatter diagram and its estimated line of cost behavior appear below

The cost line appears to reflect a variable cost because it increases at a

reasonably constant rate with changes in sales and it appears to intersect

the cost axis at zero (the origin).

Exercise 18-2 (15 minutes)

1. Graph #1. Variable cost

2. a. Graph #5

b. Graph #2

$ 0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$0

$5,000

$10,000

$15,000

$20,000

$25,000

Sales

Cost of sales

Financial & Managerial Accounting, 5th Edition

1014

Exercise 18-3 (10 minutes)

Exercise 18-4 (15 minutes)

Exercise 18-5 (20 minutes)

1. Fixed costs + Target pretax income

Dollar sales = Contribution margin ratio

2.

Sales ……………………………………….……

$1,296,000

Fixed costs ……………………………………

(160,000)

Pretax income …………………………..

(164,000)

Variable costs …………………………..

$ 972,000

(Alternatively: $1,296,000 in sales x [1 – 0.25 CM ratio] = $972,000)

Exercise 18-6 (20 minutes)

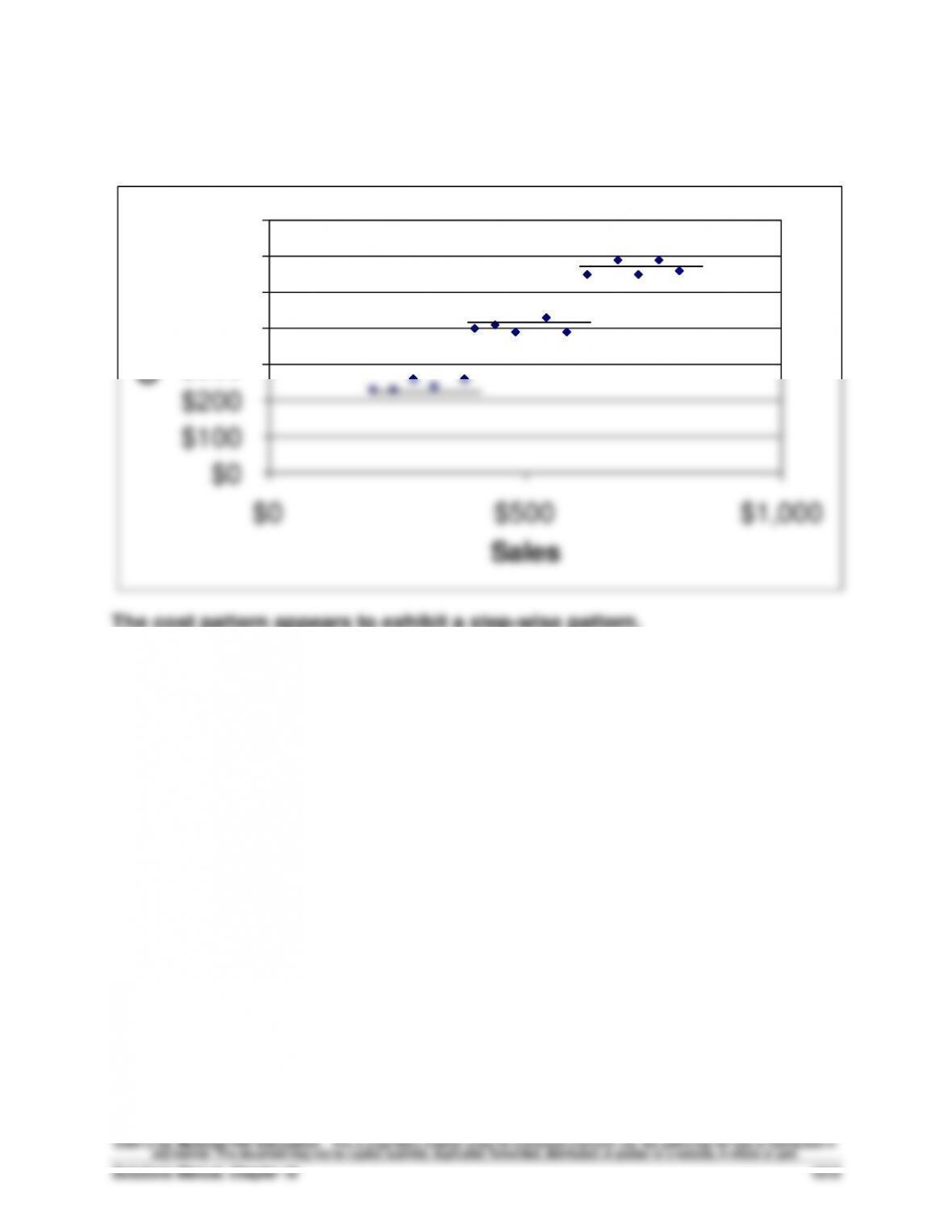

The scatter diagram and its estimated line of cost behavior appear below.

The cost pattern appears to exhibit a step-wise pattern.

$0

$100

$200

$300

$400

$500

$600

$700

$0 $500 $1,000

Costs

Sales

Financial & Managerial Accounting, 5th Edition

1016

Exercise 18-7 (20 minutes)

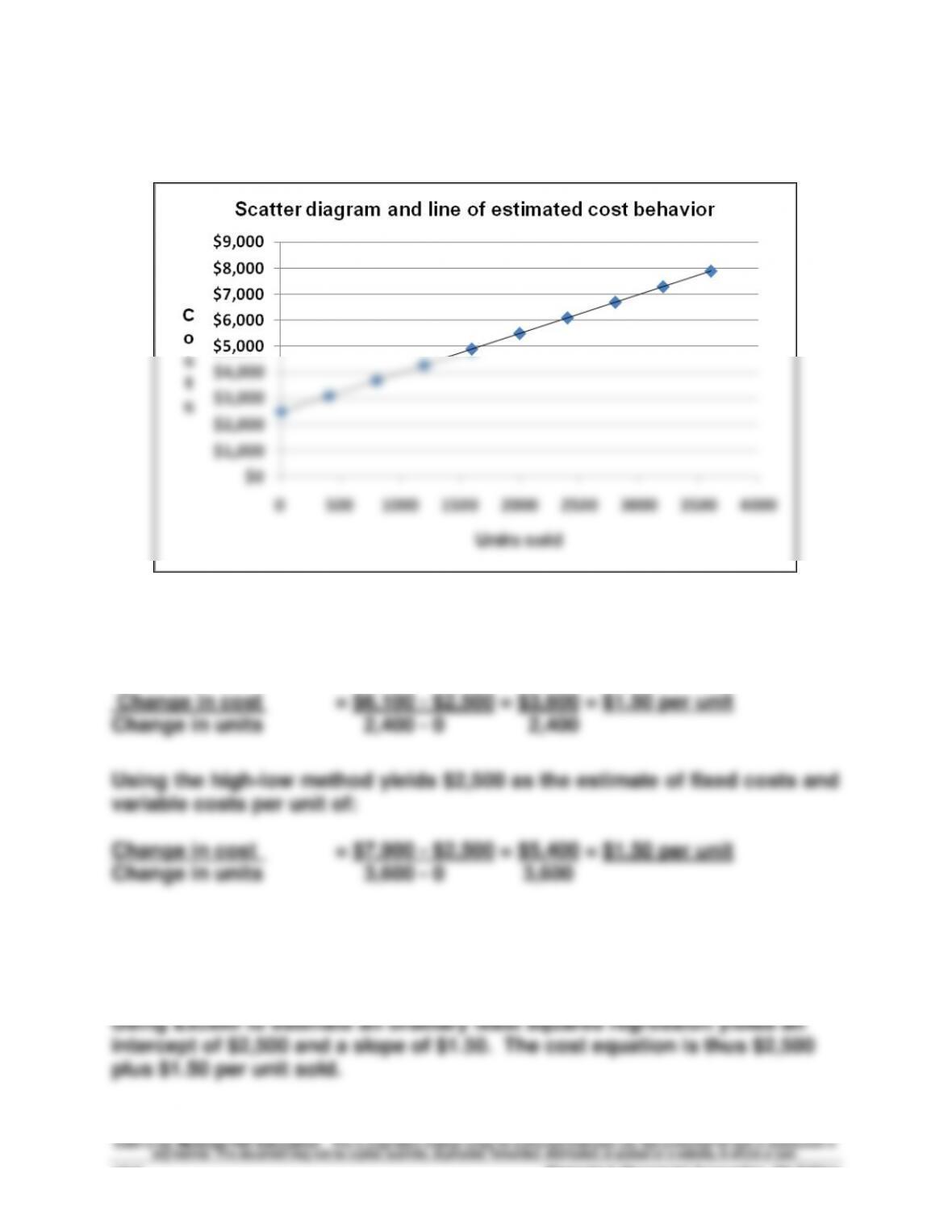

The scatter diagram and line of estimated cost behavior appear below.

Selecting 0 and 2,400 units sold as the activity levels yields $2,500 as the

estimate of fixed costs and the following estimate of variable costs per

unit:

Exercise 18-8A (20 minutes)

Exercise 18-9 (10 minutes)

(1) Contribution margin = Selling price – Variable costs

= $205 – $164 = $41 per unit

Exercise 18-10 (30 minutes)

(a) Contribution margin per unit = $180 – $135 = $45 per unit

(b) Contribution margin ratio = $45 / $180 = 25%

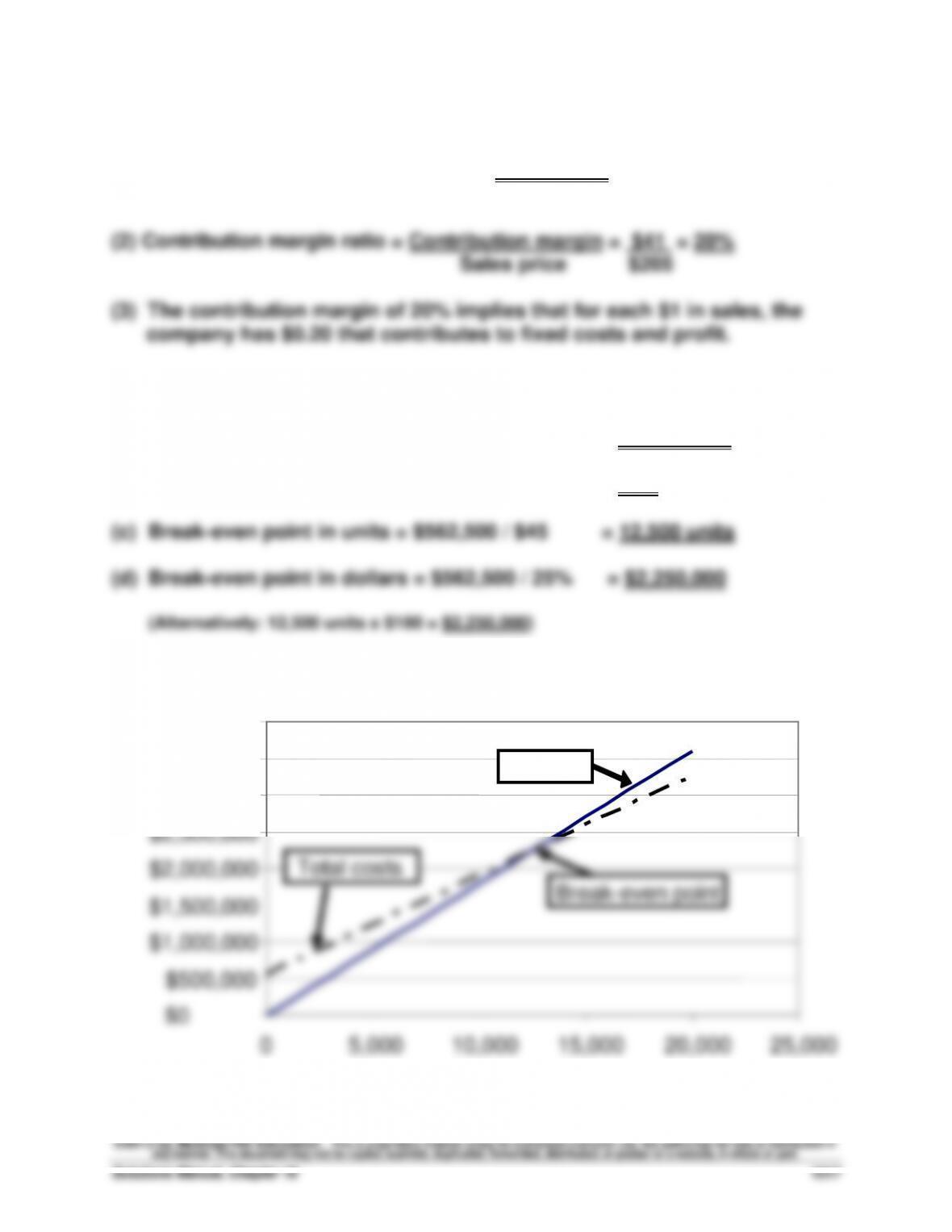

Exercise 18-11 (15 minutes)

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

0

5,000

10,000

15,000

20,000

25,000

Units

Sales

Total costs

Break-even point

Exercise 18-12 (20 minutes)

1.

BLANCHARD COMPANY

Contribution Margin Income Statement (at Break-Even)

Sales (12,500 x $180) ………………………………………………………..………

$2,250,000

Variable costs (12,500 x $135) …………………………………………..………

1,687,500

Contribution margin (12,500 x $45) ……………………………………………

562,500

Fixed costs ……………………………………………………………………..………

562,500

Net income ………………………………………………………………………………

$ 0

2. Sales (in dollars) to break even with increased fixed costs

Break–even = (Original fixed costs + Additional fixed costs)

Exercise 18-13 (25 minutes)

Preliminary computations

Pretax income = After-tax income / (1 – Tax rate)

= $810,000 / (1 – 0.20)

1. Unit sales at target income =

Fixed + Pretax

2. Dollar sales at target income = costs income

Contribution margin ratio

Fixed Pretax

costs income

Contribution margin/unit

+

Financial & Managerial Accounting, 5th Edition

1020

Exercise 18-14 (20 minutes)

BLANCHARD COMPANY

Forecasted Contribution Margin Income Statement

Sales (40,000 x $200) …………………………………………………………….….

$8,000,000

Variable costs (40,000 x $140) ……………………………………………….….

5,600,000

Contribution margin (40,000 x $60) ………………………………………..….

2,400,000

Fixed costs ………………………………………………………………………….….

562,500

Income before taxes …………………………………………………………….….

1,837,500

Income taxes (20% x $1,837,500) ……………………………………………….

367,500

Net income …………………………………………………………………………..….

$1,470,000

Exercise 18-15 (20 minutes)

1. Pretax income = Sales – Variable costs – Fixed costs

$155,000 = $___?___ – $390,000 – $430,000

2. Instructor note: Use the equation in Exhibit 18.23 with no tax effects

Unit sales = Fixed costs + Target pretax income

Contribution margin per unit

Exercise 18-16 (30 minutes)

(a) Total expected variable costs

= Variable costs per unit x units produced and sold