Chapter 15 Job Order Costing and Analysis

Chapter 15

Job Order Costing and Analysis

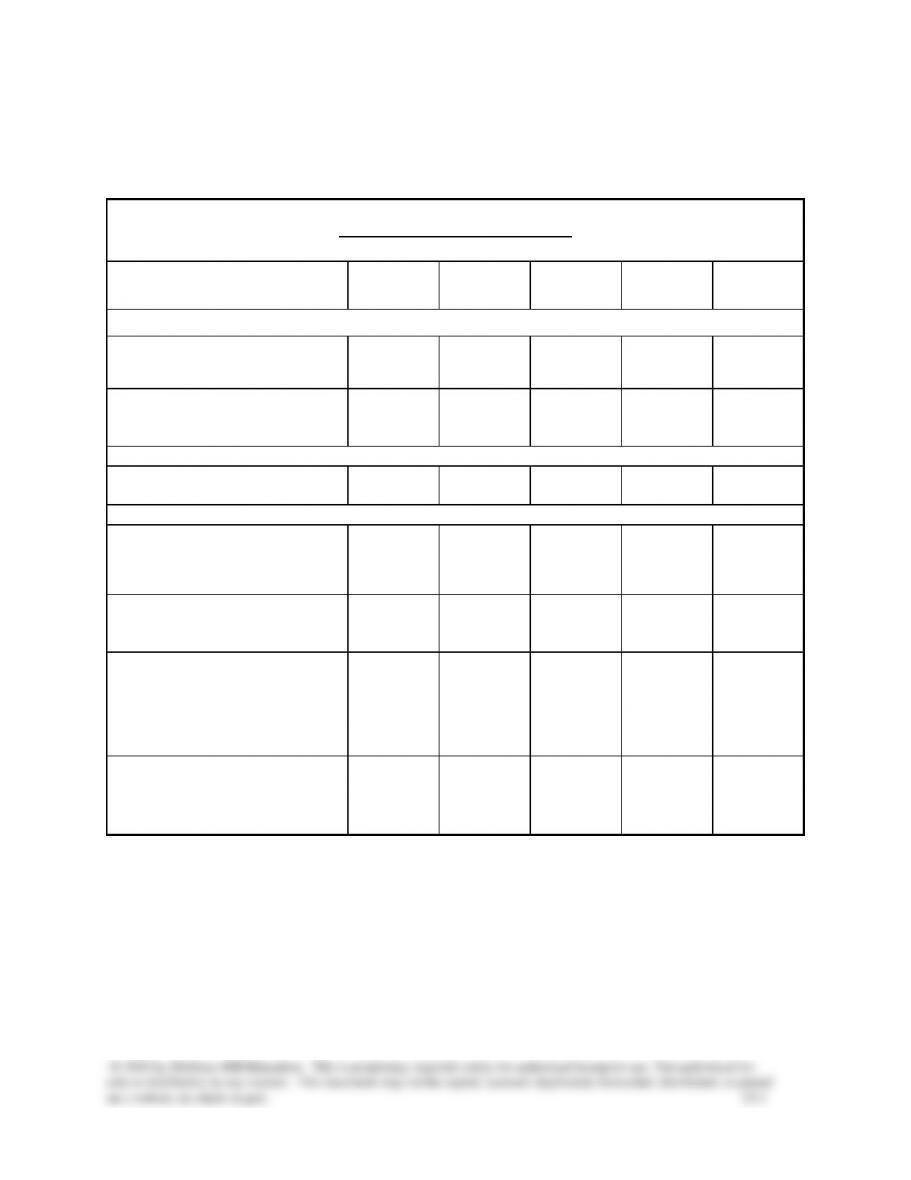

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Describe important features of

job order production.

10, 13

15-1, 15-12

15-1

RIA, CA, CIP,

TTN, TIA,

ED, GD

C2. Explain job cost sheets and how

they are used in job order cost

accounting.

3, 4

15-2, 15-3

15-2, 15-4

15-1

CIP, HTR, ED

Analytical objectives:

A1 Apply job order costing in

pricing services.

12, 14

15–11

15-18

Procedural objectives:

P1. Describe and record the flow of

materials costs in job order cost

accounting.

5, 6

15-4

15-3, 15-4,

15-7, 15-8,

15-13, 15-17,

15–19

15-1, 15-2,

15-3, 15-5

HTR

P2. Describe and record the flow of

labor costs in job order cost

accounting.

7

15-5

15-3, 15-4,

15-7, 15-9,

15-13, 15-17

15-1, 15-2,

15-3, 15-5

HTR

P3. Describe and record the flow of

overhead costs in job order cost

accounting.

1, 2, 8, 11

15-6, 15-7,

15–10

15-3, 15-4,

15-5, 15-6,

15-7, 15-10,

15-13, 15-14,

15-15, 15-16,

15–17

15-1, 15-2,

15-3, 15-4,

15-5

EC, HTR

P4. Determine adjustments for

overapplied and underapplied

factory overhead.

8, 9

15-8, 15-9

15-7, 15-11,

15-12, 15-13,

15–14, 15-15

15-1, 15-2,

15-4, 15-5

*See additional information on next page that pertains to these quick studies, exercises and problems.

Chapter 15 Job Order Costing and Analysis

Additional information on Related Assignment Material

Assignment materials that can be completed by students using:

Sage 50 and QuickBooks Pro 2013 templates – Problem 15-1A, 15-2A.

Excel templates – Problems 15-4A

** The Serial Problem for Success Systems, which covers numerous learning objectives, can be

the chapters. Even if previous segments were not assigned, students can begin the segment of the

serial problem that is included in this chapter. It is most readily solved if students use the Working

Papers that accompany the book.).

Synopsis of Chapter Revision

• Astor and Black: NEW opener with new entrepreneurial assignment

• Reorganized discussion of job order costing for service companies

• New discussion of accounting for nonmanufacturing costs and their role in pricing decisions

• Added new journal entries for indirect materials and indirect labor for improved learning

PowerPoint® Show Slides

Chapter Learning Objective

PowerPoint® Slides

C1

6-9

C2

10

P1

11-13, 20, 31-32

P2

14-16, 33-34

P3

17-19, 21-22, 35-38

P4

23-30

A1

39

Chapter 15 Job Order Costing and Analysis

Chapter Outline

Notes

I. Job Order Cost Accounting

A. Cost Accounting System

1. Records manufacturing activities using a perpetual inventory

system which continuously updates records for costs of

materials, goods in process, and finished goods inventories.

2. Provides timely information about inventories, changes and

manufacturing costs per unit of product.

3. Two basic types of cost accounting systems are job order cost

accounting and process cost accounting.

B. Job Order Production— products individually designed to meet

the needs of a specific customer (special orders).

1. The production activities for a customized product represents

a job.

C. Job Order Costing of Services – the same principles apply to both

manufacturing and service companies.

D. Events in Job Order Costing

1. Jobs can be initiated by a customer order or less often,

2. First step is to predict the cost to complete the job.

3. Second step is to negotiate a price and decide whether to

pursue the job. Some jobs are priced on cost-plus basis where

the customer pays for manufacturing costs plus a negotiated

production occurs as materials and labor are applied to the job.

determines the cost of each job.

1. Classifies costs as direct materials, direct labor, or overhead.

3. Cost Flows: During production, accumulated job costs are kept

in the goods in process inventory while goods are being

manufactured.

Collection of job cost sheets for all jobs in process make up a

Chapter Outline

Notes

Inventory account in the general ledger.

Chapter 15 Job Order Costing and Analysis

Chapter Outline

time tickets and related entry as these costs are incurred.

d. Indirect labor cards in Factory Overhead Ledger—

accumulates indirect labor costs from time tickets and related

entry.

Notes

3. Overhead Cost Flows and Documents

a. Materials requisitions forms for indirect materials.

b. Time tickets for indirect labor.

c. Other sources include vouchers authorizing payments for

items such as supplies or utilities and adjusting entries for

costs such as depreciation.

d. Factory Overhead Ledger—contains a separate account

for each overhead cost. It is controlled by the Factory

Overhead account in the General Ledger which

accumulates costs until they are allocated to specific jobs.

4. Overhead Allocation Bases –generally allocate overhead by

a. Job Cost Sheets—show factory overhead costs that have

been applied using the predetermined factory overhead

b. Recording Overhead Costs—debited to Goods in Process

Inventory and credited to Factory Overhead as allocated to

specific jobs.

6. Recording Allocated Overhead – entry to record allocation

b. Debit Goods In Process Inventory for direct materials and

debit Factory Overhead for indirect materials as goods are

c. Debit Factory Payroll as labor is incurred.

d. Debit Goods In Process for direct labor and debit Factory

Overhead for indirect labor as costs are analyzed. Credit

Chapter 15 Job Order Costing and Analysis

Chapter Outline

Factory Payroll. Direct labor costs are also accumulated

on Job Cost Sheets.

Notes

e. Debit Factory Overhead as other overhead costs are

incurred.

f Debit Goods In Process as overhead costs are applied

using overhead rate. Credit Factory Overhead.

g Debit Finished Goods Inventory as jobs are completed and

credit Goods in Process for the full cost of job taken from

completed Job Cost Sheets.

h Debit Cost of Goods Sold as goods are sold and credit

Finished Goods Inventory.

i. Any under or over applied factory overhead cost is

accounted for in an adjustment.

III. Adjusting Factory Overhead—Overhead applied rarely equals that

incurred because a predetermined overhead rate based on estimates is

used in applying factory overhead costs to jobs.

A. Underapplied overhead

1. Overhead incurred is less than amount applied.

2. Results in a debit balance in Factory Overhead.

3. Reflects manufacturing costs not charged to jobs.

4. If immaterial—Factory Overhead balance is credited to close

this account and debited to Cost of Goods Sold.

B. Overapplied overhead

1. Overhead applied exceeds the overhead incurred.

2. Results in a credit balance in Factory Overhead.

3. If immaterial—Factory Overhead balance is debited to close

this account and credited to Cost of Goods Sold resulting in a

reduction of Cost of Goods Sold.

C. Material overhead balances are allocated among Goods in

Process, Finished Goods, and Cost of Goods Sold.

IV. Decision Analysis—Pricing for Services

service setting.

B. Procedure to determine:

1. Direct labor costs

2. Overhead costs based on predetermined rate(s).

4. Cost of job by combining labor and overhead costs. Note:

Chapter 15 Job Order Costing and Analysis

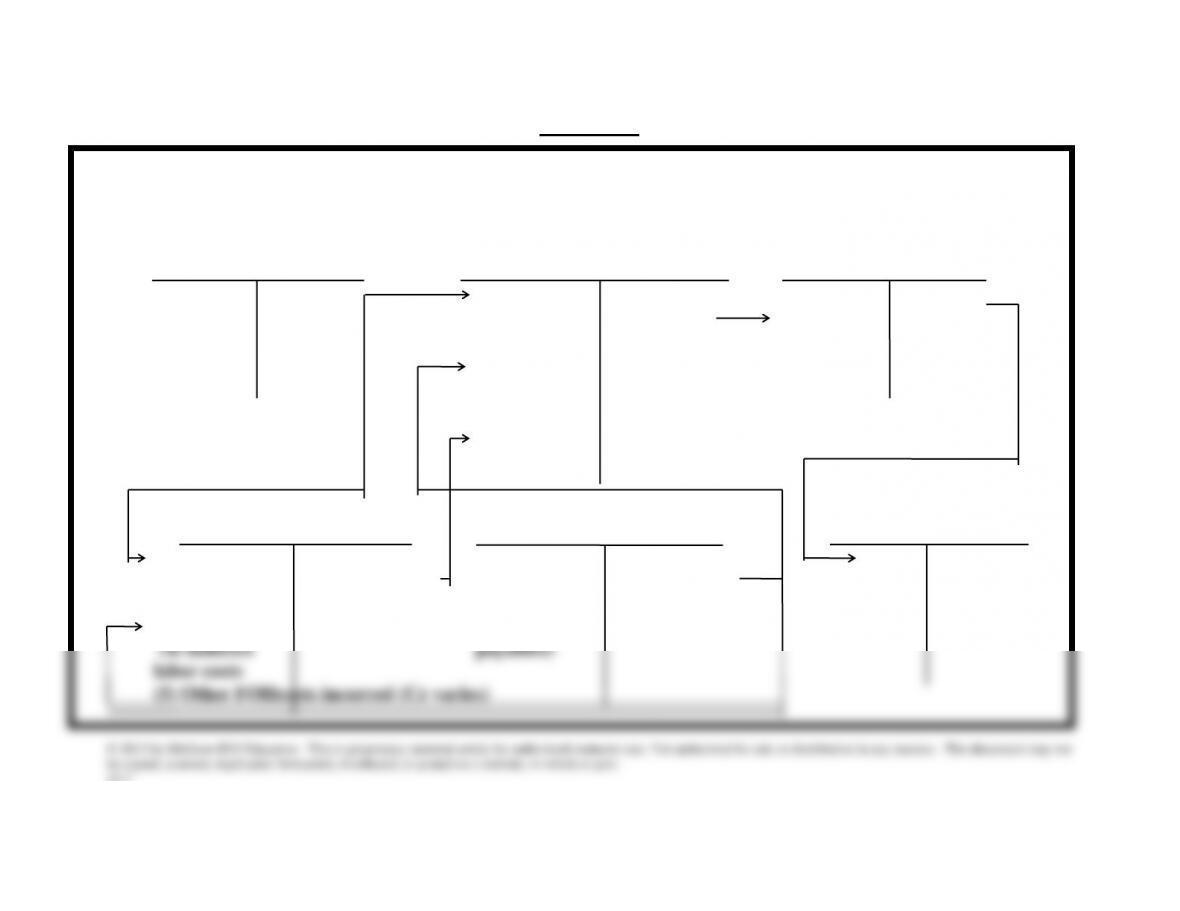

15-7

VISUAL #25

Tracing Product Costs

Through a Cost Accounting System

Work in Progress Finished Goods

Materials Inventory Inventory Inventory

(1) Buy Send (2) (2) Direct (7) Goods (7) Cost of (8) Goods

(Cr. A/P) materials material completed Finished Sold

to factory costs Goods

(4) Direct

labor

costs

(6) Overhead

costs

Factory Overhead Factory Payroll Cost of Goods Sold

(2) Indirect (6) Overhead (3) Labor (4) Labor (8)

materials cost costs applied costs costs applied

or factory to production incurred

supplies (Cr

Chapter 15 Job Order Costing and Analysis

website, in whole or part. 15-8

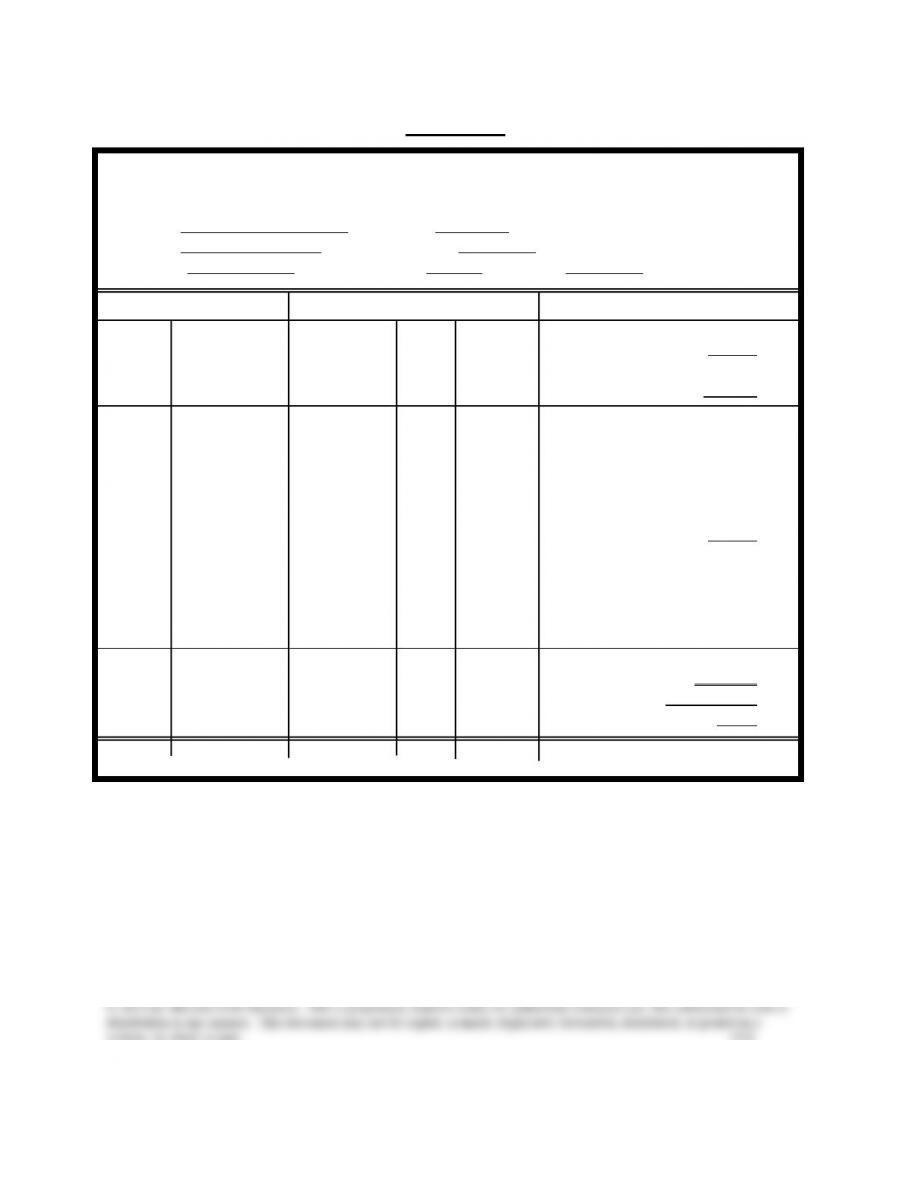

VISUAL #26

Job Cost Sheet

Customer Build We Must, Inc. Job No. 114

Product Bracket-H3 Date Promised 10/1/xx

Quantity 200 Dates: Started 9/1/xx Completed 9/20/xx

Direct Material Direct Labor Cost Summary

Mat’l. Payroll Direct Material $ 900.00

Req’n. Summary

No. Amount Dated Dept. Amount Direct Labor 600.00

667 $ 340.00 9/2 A $ 70.00

673 180.00 9/9 A 240.00 Factory Overhead

691 200.00 9/16 B 190.00 (applied at):

623 180.00 9/23 B 100.00

150% of direct

labor cost 900.00

Total Cost $2,400.00

Totals $ 900.00 $ 600.00 Units Finished 200

Unit Cost $12.00

Chapter 15 Job Order Costing and Analysis

website, in whole or part. 15-9

Chapter 15 — Alternate Demonstration Problem #1

The following information was taken from the accounting records of the

Superior Company:

Depreciation of equipment ………………………………………………

$ 70,000

Direct labor …………………………………………………………………….

120,000

Factory taxes ………………………………………………………………….

2,000

Goods in process inventory, Dec. 31, 2013 ………………………

250,000

Indirect labor …………………………………………………………………..

10,000

Power …………………………..…………………………………………………

16,000

Raw materials inventory, Dec. 31, 2013 …………………………...

60,000

Raw materials purchases, for year …………………………………..

230,000

Goods in process inventory, January 1, 2013 …………………..

302,000

Raw materials, January 1, 2013 ……………………………………….

110,000

Required:

Prepare a manufacturing statement for the Superior Company for the year

ended December 31, 2013.

Chapter 15 Job Order Costing and Analysis

website, in whole or part. 15–10

Solution: Chapter 15 — Alternate Demonstration Problem #1

SUPERIOR MANUFACTURING COMPANY

Manufacturing Statement

For Year Ended December 31, 2013

Direct materials:

Raw materials inventory, 1/1/13 ……………………..

$110,000

Raw materials purchases ………………………………

230,000

Raw materials available for use ……………………..

340,000

Raw materials inventory, 12/31/13 ………………….

60,000

Direct materials used …………………………………….

$280,000

Direct labor …………………………………………………..

120,000

Factory overhead costs: ………………………………..

Indirect labor …………………………………………………

10,000

Power …………………………..……………………………….

16,000

Factory taxes ………………………………………………..

2,000

Depreciation of equipment …………………………….

70,000

Total factory overhead costs …………………………

98,000

Total manufacturing costs …………………………….

498,000

Goods in process inventory, 1/1/13 ………………..

302,000

Total goods in process during the year ………….

800,000

Goods in process inventory, 12/31/13 …………….

250,000

Cost of goods manufactured …………………………

$550,000