SERIAL PROBLEM — SP 13

Serial Problem — SP 13, Success Systems (45 minutes)

1. Gross margin with services revenue

Gross margin = Total revenue – Cost of goods sold

= $43,853 – $14,052 = $29,801

2. Current ratio = $105,209 / $875 = 120.2

4. Current assets are 81.0% of total assets ($105,209/$129,909)

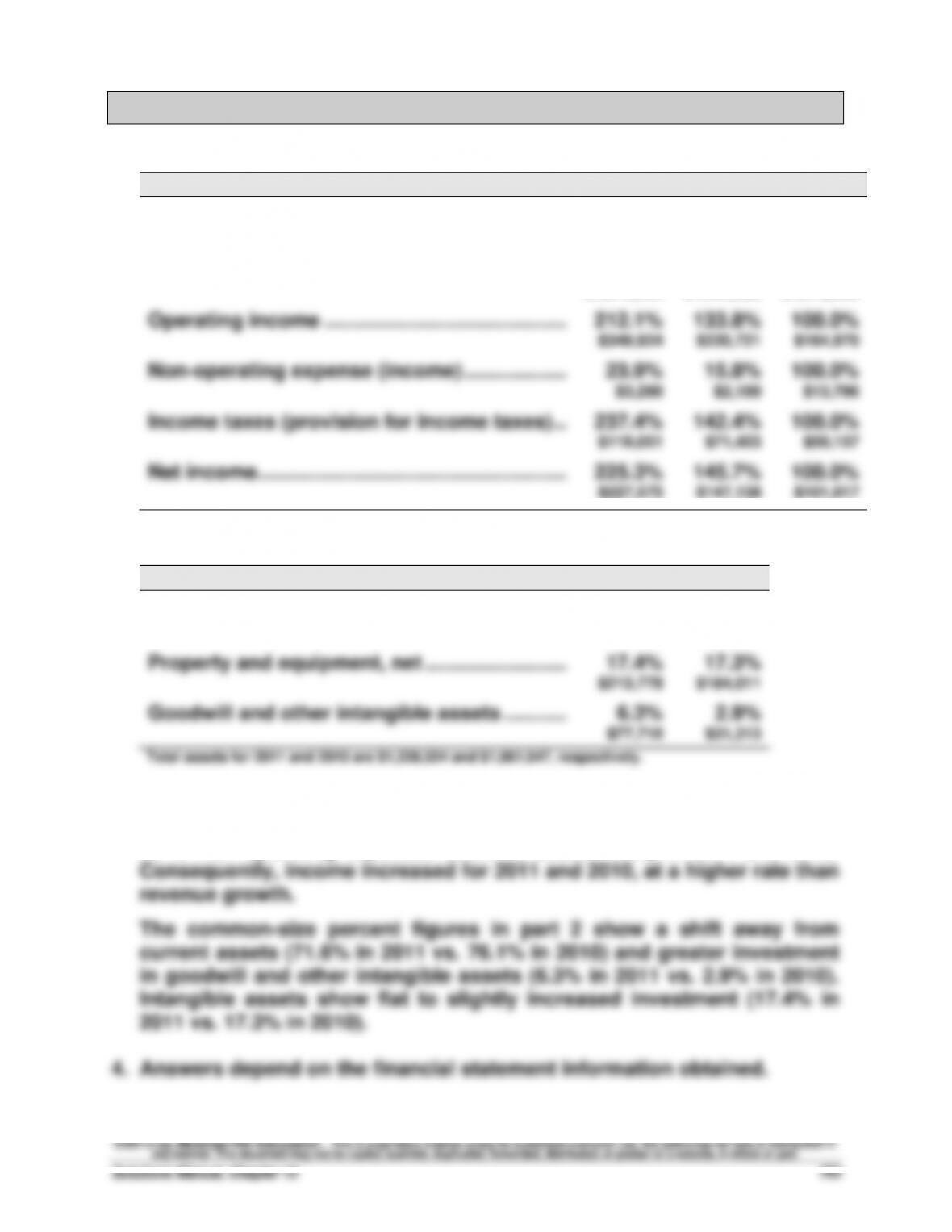

Reporting in Action — BTN 13-1

1. Trend percents for selected income statement accounts

($ in thousands)

2011

2010

2009

Revenues ………………………………………………….….

169.7%

127.2%

100.0%

$2,656,949

$1,991,139

$1,565,887

Cost of goods sold ……………………………………….

163.4%

124.6%

100.0%

$1,916,366

$1,460,926

$1,172,668

Operating income ……………………………………..….

212.1%

133.8%

100.0%

$349,924

$220,721

$164,970

Non-operating expense (income) ……………….….

23.9%

15.8%

100.0%

$3,298

$2,180

$13,796

Income taxes (provision for income taxes) …….

237.4%

142.4%

100.0%

$119,051

$71,403

$50,157

Net income ………………………………………………..….

225.3%

145.7%

100.0%

$227,575

$147,138

$101,017

2. Common-size percents for asset categories and accounts

($ in thousands)

2011

2010

Total current assets …………………………………..….

71.6%

76.1%

$878,676

$808,145

Property and equipment, net ……………………..….

17.4%

17.3%

$213,778

$184,011

Goodwill and other intangible assets …………….

6.3%

2.9%

$77,718

$31,313

Total assets for 2011 and 2010 are $1,228,024 and $1,061,647, respectively.

3. For 2011 and 2010, revenues grew at a higher rate than cost of goods

sold. Operating income grew at a higher rate than revenues for 2011 and

2010. Non-operating expenses declined substantially in 2011 and 2010.

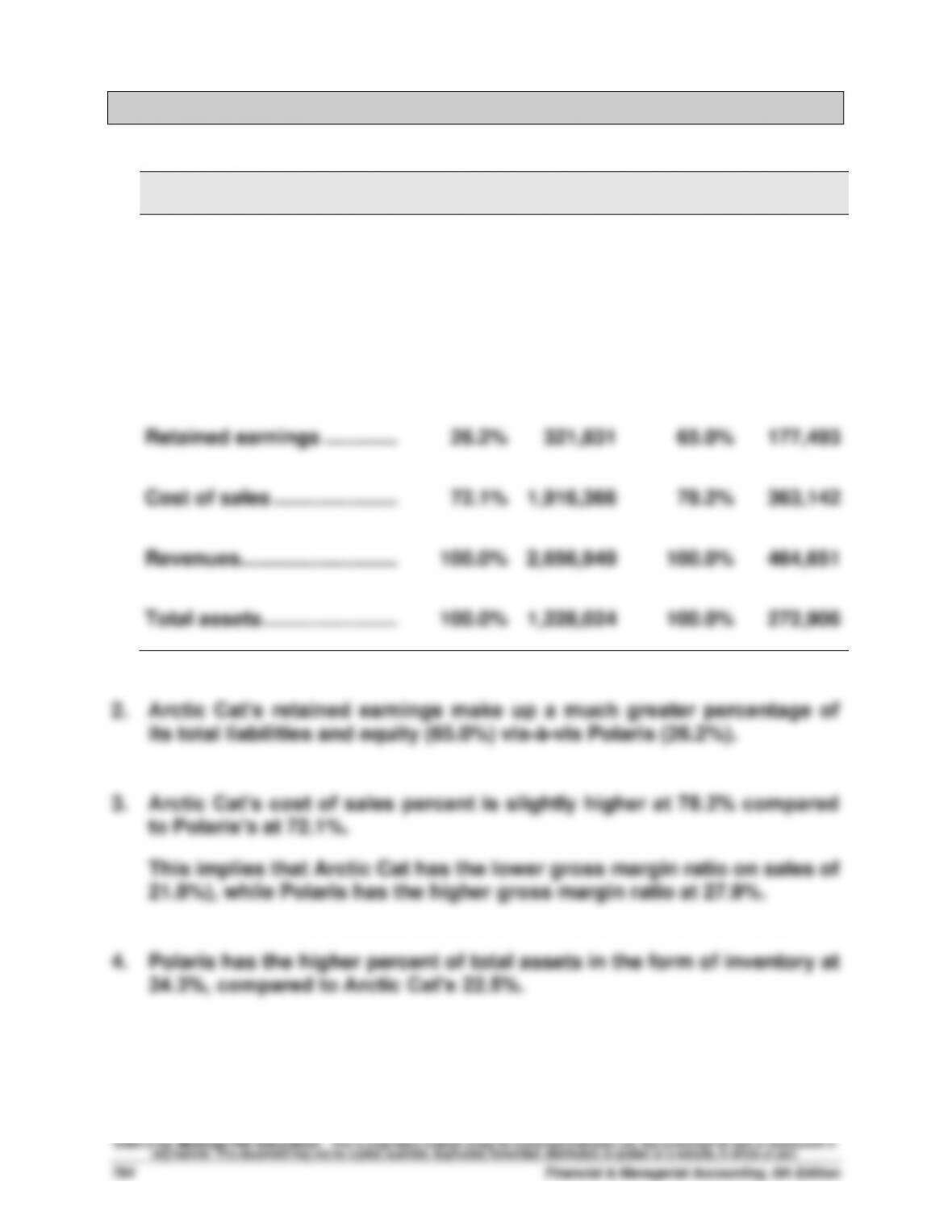

Comparative Analysis — BTN 13-2

1.

Key figures ($ thousands)

Polaris

Arctic Cat

Cash and equivalents ……..….

26.5%

$325,336

5.4%

$14,700

Accounts receivable, net …….

9.4%

115,302

8.7%

23,732

Inventories ……………………..….

24.3%

298,042

22.5%

61,478

Retained earnings …………..….

26.2%

321,831

65.0%

177,493

Cost of sales …………………..….

72.1%

1,916,366

78.2%

363,142

Revenues………………………..…

100.0%

2,656,949

100.0%

464,651

Total assets …………………….….

100.0%

1,228,024

100.0%

272,906

Ethics Challenge — BTN 13-3

1. The CEO appears to have selectively chosen from the 11 available

ratios to present only the ones that show trends that are favorable to

2. The consequences of this action by the CEO might be mixed. It is likely

that the analysts will ask other questions that may reveal some

negative trends such as the trends in return and profit margins. The

Communicating in Practice — BTN 13-4

There is no set solution to this activity. Each team’s memorandum will

vary based on the industry and companies chosen for analysis.

(Instructor: Consider having each team do a brief presentation discussing

the findings in their memorandum to engage in a classroom discussion of

the findings.)

Financial & Managerial Accounting, 5th Edition

766

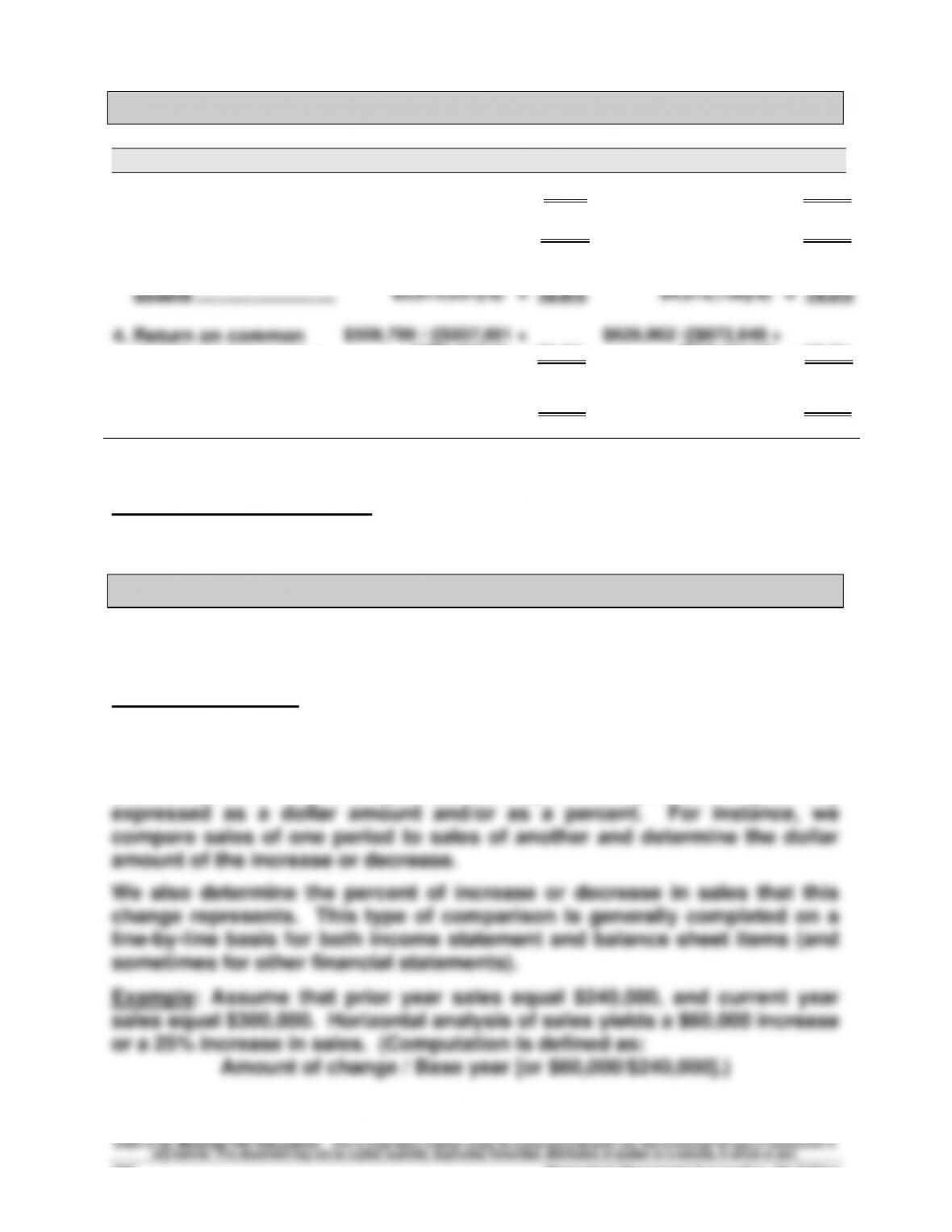

Taking It to the Net — BTN 13-5

($ thousands)

As of 12/31/2010

As of 12/31/2011

1. Profit margin ratio …….……….

$509,799/$5,671,009 = 9.0%

$628,962/$6,080,788 = 10.3%

2. Gross profit ratio ……..……….

$2,415,208/ $5,671,009 = 42.6%

$2,531,892/$6,080,788 = 41.6%

3. Return on total

assets …………………….…….

$509,799 / ([$4,272,732 +

$3,675,031]/2) = 12.8%

$628,962/ ([$4,412,199 +

$4,272,732]/2) = 14.5%

4. Return on common

stockholders’ equity* ..……….

$509,799 / ([$937,601 +

$760,339]/2) = 60.0%

$628,962/ ([$872,648 +

$937,601]/2) = 69.5%

5. Basic net income per

common share** ……………….

$ 2.29

$ 2.85

*An acceptable alternative solution would be to include minority interest in equity.

**Taken from consolidated statement of income.

Analysis and Interpretation: Hershey’s performance generally improved in

all areas evaluated for the profitability metrics reported in the table above.

Teamwork in Action — BTN 13–6

Part 1

Team reports should look something like the following:

Horizontal Analysis

Horizontal analysis is comparing a company’s financial statement amounts

across time. We compare data from comparative statements that are

horizontally aligned; that is, we compare the same items from one period to

another period. The change disclosed by the comparison is generally

Teamwork in Action (Concluded)

If a horizontal comparison is made over a number of periods, the

comparisons are made to corresponding amounts in a selected period

called the base period. Each subsequent period’s amount is compared to

the base period. The change is expressed as a percent of the base period.

This is commonly referred to as trend analysis.

Vertical Analysis

Vertical analysis is comparing a company’s financial statement amounts to

[or $100,000/$500,000].)

Part 2

Explanations of the four categories or areas of ratio analysis follow:

a. Liquidity analysis measures the availability of resources to meet short-

Note: Students will select various ratios to illustrate these categories. Use

Exhibit 13.16 to verify the category, measurement, and use of each ratio.

Part 3

Each team member presents results to the entire team.

Entrepreneurial Decision — BTN 13-7

1. No. Although the current ratio improved over the three-year period, the

acid-test ratio declined and accounts receivable and merchandise

2. No. The decreasing turnover of accounts receivable indicates the

company is collecting its receivables more slowly.

3. No. Sales are increasing and accounts receivable are turning more

4. Yes. To illustrate, if sales are assumed to equal $100 in 2010, the sales

trend shows that they would equal $125 in 2011 and $137 in 2012. Then,

5. No. The percent of return on equity declines from 12.25% in 2010 to

9.75% in 2012.

6. The dollar amount of selling expenses increased in 2011 and decreased

sharply in 2012. Again assuming sales figures of $100 in 2010, $125 in

2011, and $137 in 2012, and multiplying each by its selling expense to

net sales ratio gives $15.30 of selling expenses in 2010, $17.13 in 2011,

and $13.43 in 2012.

Hitting the Road — BTN 13-8

Global Decision — BTN 13-9

Key figures (Euro in thousands)

KTM

Cash and equivalents ………………………………..…

3.1%

$ 14,962

Accounts receivable, net …………………………..

11.0%

53,594

Inventories ………………………………………………..…

23.5%

113,979

Retained earnings ……………………………………..…

43.0%

208,987

Cost of sales ……………………………………………..…

70.6%

371,752

Revenues ………………………………………………….…

100.0%

526,801

Total assets …………………………………………………

100.0%

485,775

Comparisons and comments:

• KTM’s cash and equivalents is less than that of Polaris and Arctic Cat as

a percent of assets.