Problem 13-2B (120 minutes)

Part 1

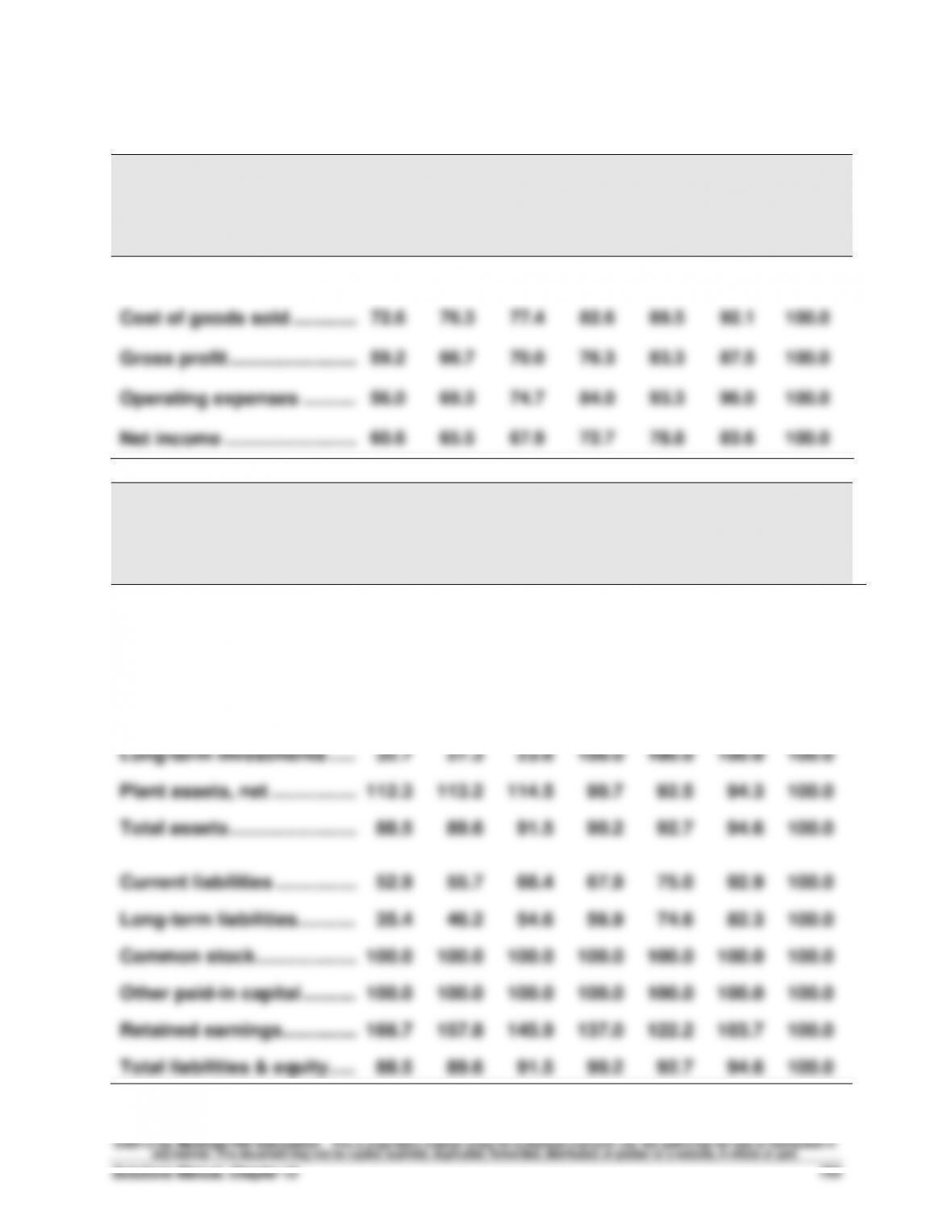

TRIPOLY COMPANY

Income Statement Trends

For Years Ended December 31, 2014-2008

2014

2013

2012

2011

2010

2009

2008

Sales ……………………………….

65.1%

70.9%

73.3%

79.1%

86.0%

89.5%

100.0%

Cost of goods sold …………..

72.6

76.3

77.4

82.6

89.5

92.1

100.0

Gross profit ……………………..

59.2

66.7

70.0

76.3

83.3

87.5

100.0

Operating expenses ………...

56.0

69.3

74.7

84.0

93.3

96.0

100.0

Net income ……………………...

60.6

65.5

67.9

72.7

78.8

83.6

100.0

TRIPOLY COMPANY

Balance Sheet Trends

December 31, 2014-2008

2014

2013

2012

2011

2010

2009

2008

Cash ………………………………

64.7%

67.6%

76.5%

79.4%

88.2%

91.2%

100.0%

Accounts recble., net ……….

81.3

85.0

87.5

90.0

93.8

96.3

100.0

Merchandise inventory ……..

79.8

82.7

85.6

86.5

89.4

91.3

100.0

Other current assets ………...

85.0

85.0

90.0

95.0

95.0

100.0

100.0

Long-term investments …….

32.7

27.3

23.6

100.0

100.0

100.0

100.0

Plant assets, net ……………...

112.3

113.2

114.5

90.7

92.5

94.3

100.0

Total assets ……………………..

88.5

89.6

91.5

90.2

92.7

94.6

100.0

Current liabilities ……………..

52.9

55.7

66.4

67.9

75.0

92.9

100.0

Long-term liabilities ………….

35.4

46.2

54.6

56.9

74.6

82.3

100.0

Common stock ………………...

100.0

100.0

100.0

100.0

100.0

100.0

100.0

Other paid-in capital ………...

100.0

100.0

100.0

100.0

100.0

100.0

100.0

Retained earnings…………….

166.7

157.8

145.9

137.0

122.2

103.7

100.0

Total liabilities & equity …….

88.5

89.6

91.5

90.2

92.7

94.6

100.0

Financial & Managerial Accounting, 5th Edition

754

Problem 13-2B (Concluded)

Part 2

Analysis and Interpretation

• The statements and the trend percent data show that sales declined

every year. However, cost of goods sold did not fall as rapidly as sales.

As a result, gross profit fell more rapidly than sales.

• Operating expenses fell less rapidly than gross profit, so the final result

Problem 13-3B (60 minutes)

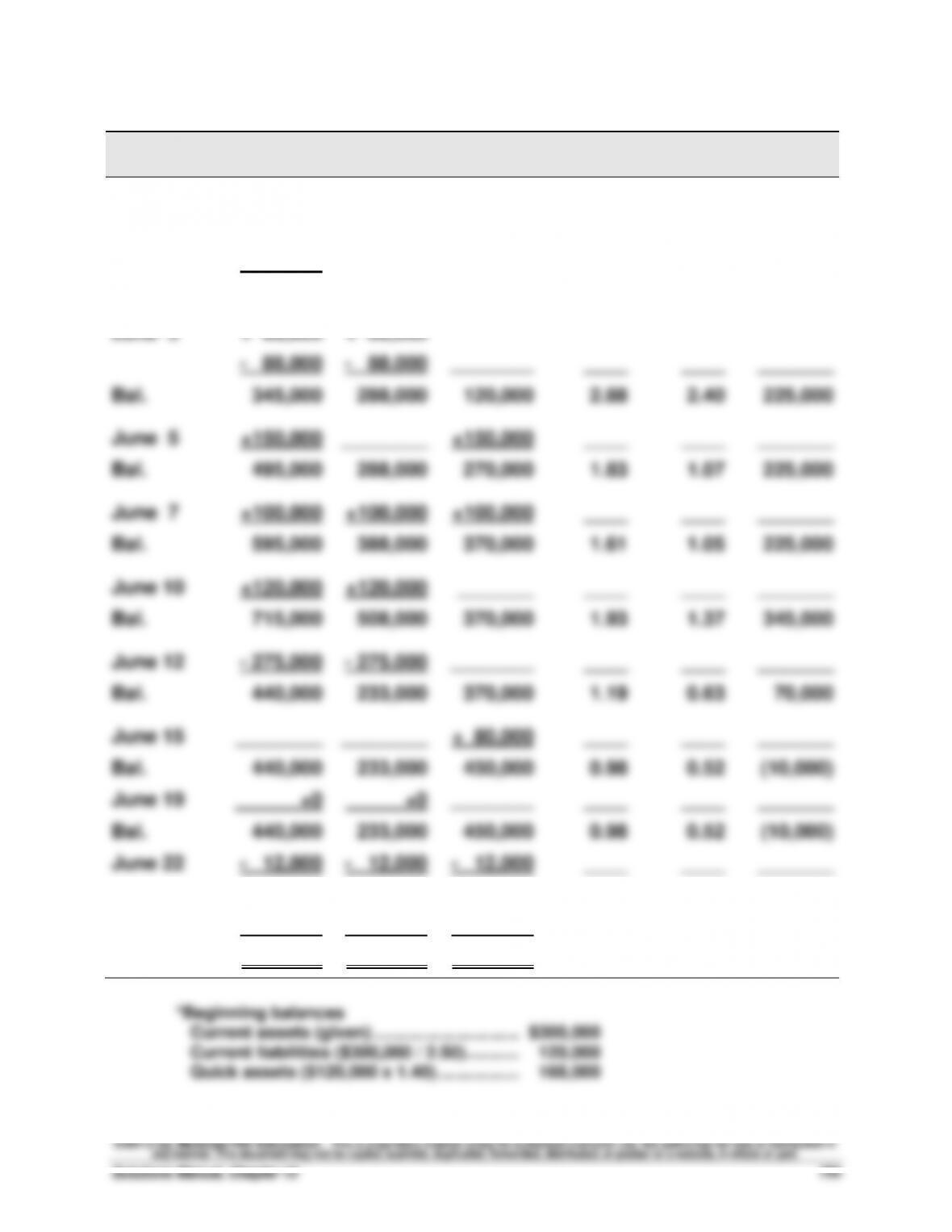

Trans-

action

Current

Assets

Quick

Assets

Current

Liabilities

Current

Ratio

Acid-Test

Ratio

Working

Capital

Beginning*

$300,000

$168,000

$120,000

2.50

1.40

$180,000

June 1

+120,000

+120,000

– 75,000

_______

________

____

____

_______

Bal.

345,000

288,000

120,000

2.88

2.40

225,000

June 3

+ 88,000

+ 88,000

– 88,000

– 88,000

________

____

____

_______

Bal.

345,000

288,000

120,000

2.88

2.40

225,000

June 5

+150,000

________

+150,000

____

____

_______

Bal.

495,000

288,000

270,000

1.83

1.07

225,000

June 7

+100,000

+100,000

+100,000

____

____

_______

Bal.

595,000

388,000

370,000

1.61

1.05

225,000

June 10

+120,000

+120,000

_______

____

____

_______

Bal.

715,000

508,000

370,000

1.93

1.37

345,000

June 12

– 275,000

– 275,000

________

____

____

_______

Bal.

440,000

233,000

370,000

1.19

0.63

70,000

June 15

________

________

+ 80,000

____

____

_______

Bal.

440,000

233,000

450,000

0.98

0.52

(10,000)

June 19

+0

+0

________

____

____

_______

Bal.

440,000

233,000

450,000

0.98

0.52

(10,000)

June 22

– 12,000

– 12,000

– 12,000

____

____

_______

Bal.

428,000

221,000

438,000

0.98

0.50

(10,000)

June 30

– 80,000

– 80,000

– 80,000

____

____

_______

Bal.

$348,000

$141,000

$358,000

0.97

0.39

(10,000)

Financial & Managerial Accounting, 5th Edition

756

Problem 13-4B (50 minutes)

1. Current ratio

= 2.5 to 1

2. Acid-test ratio

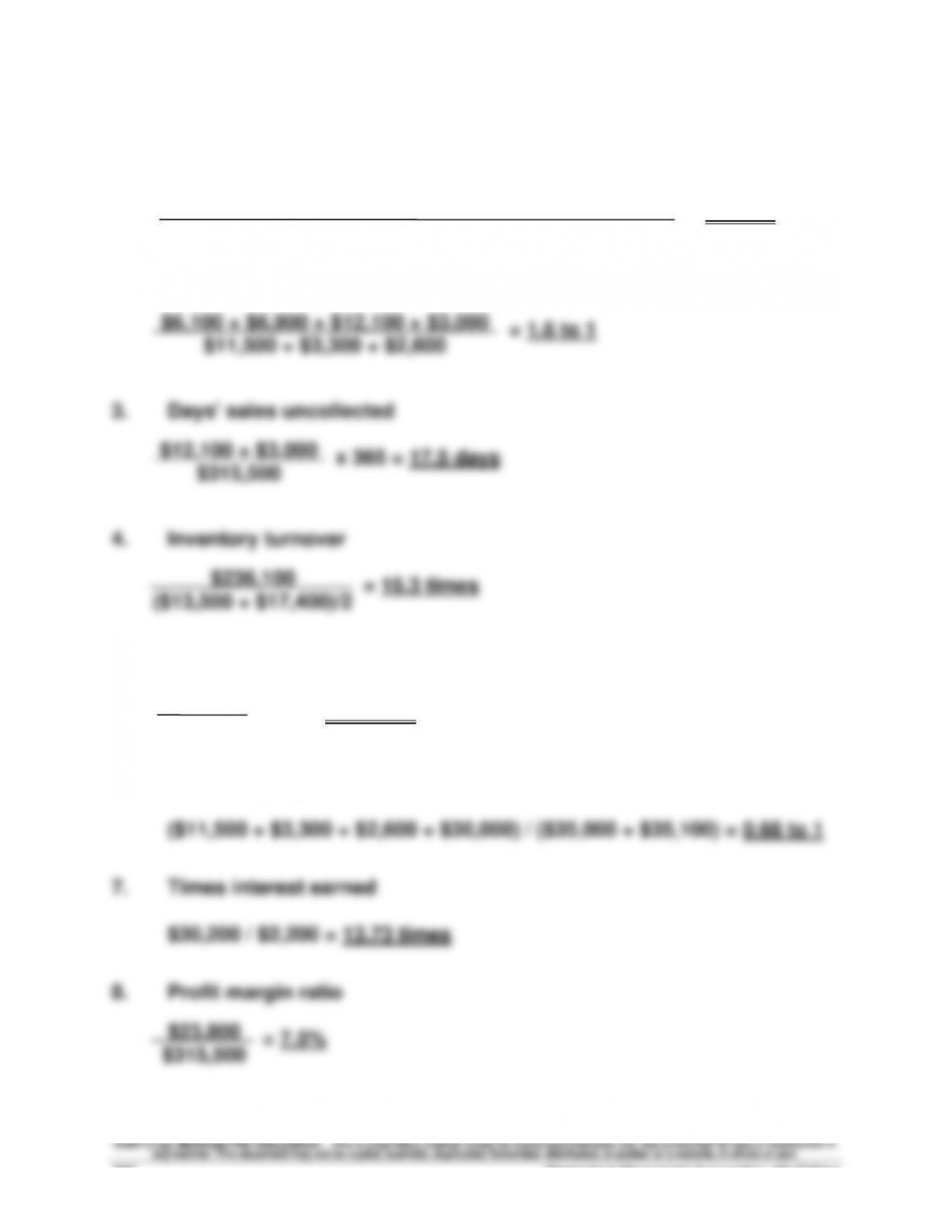

5. Days’ sales in inventory

x 365 = 20.9 days

6. Debt–to-equity ratio

$6,100 + $6,900 + $12,100 + $3,000 + $13,500 + $2,000

$11,500 + $3,300 + $2,600

$13,500

$236,100

Problem 13–4B (Concluded)

9. Total asset turnover

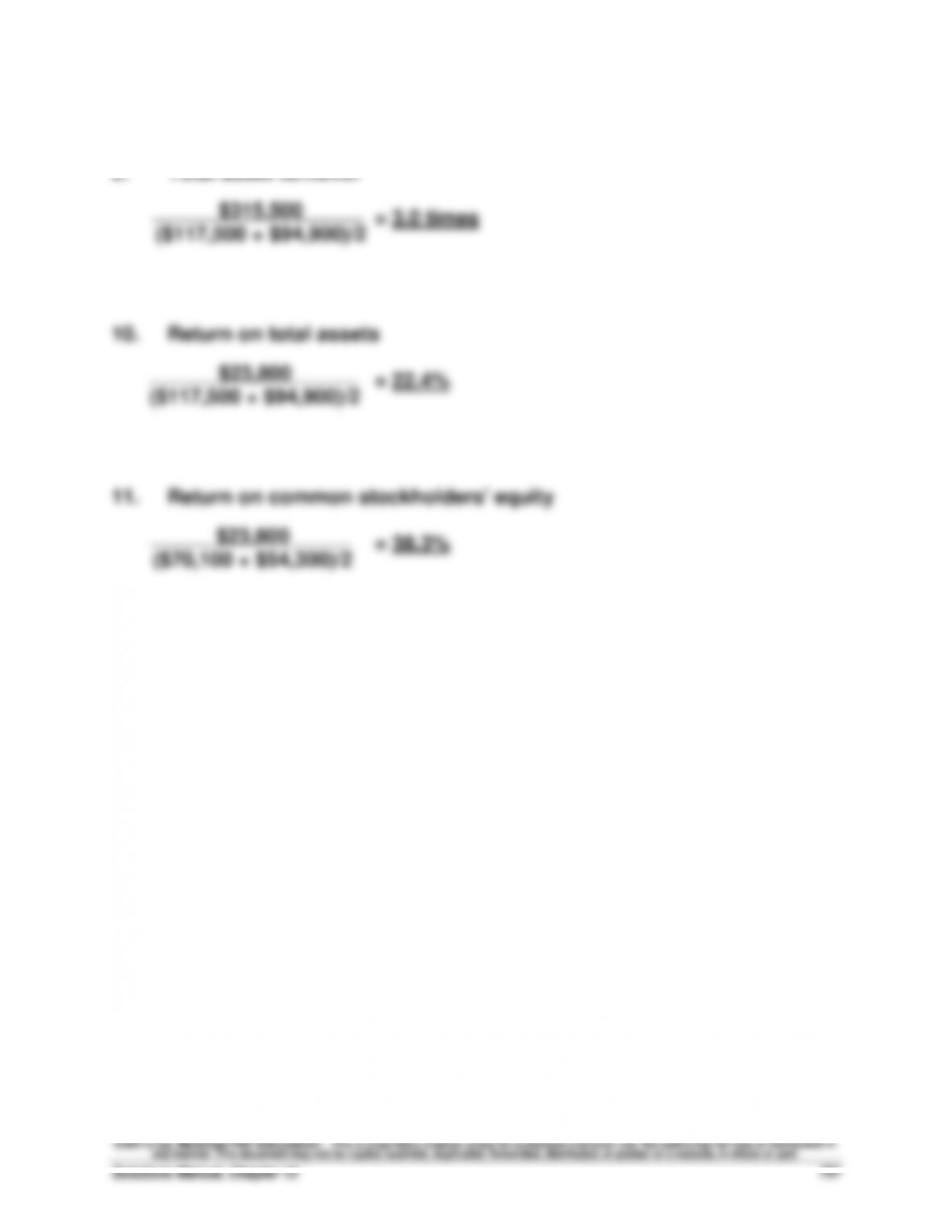

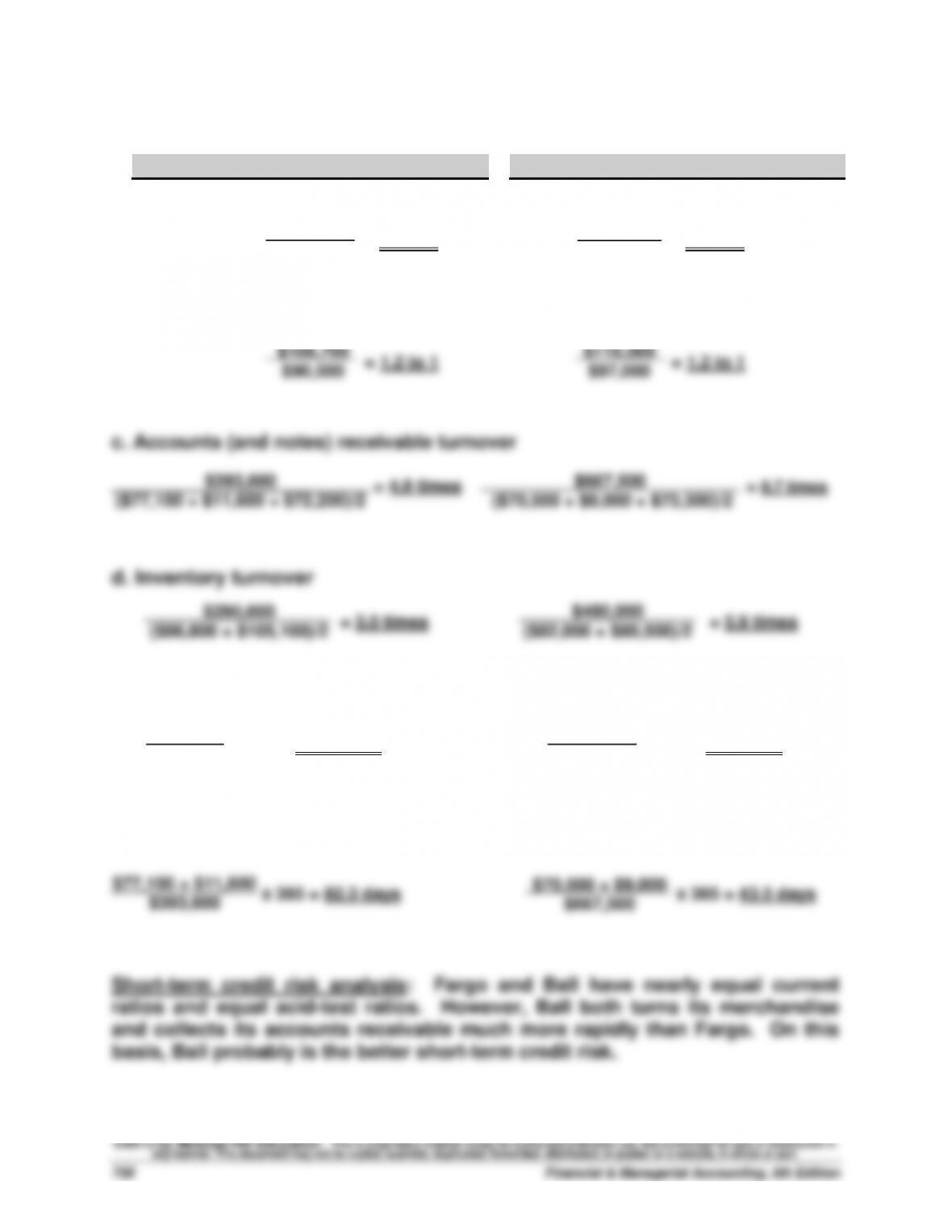

Problem 13-5B (60 minutes)

Part 1

Fargo Company

Ball Company

a. Current ratio

= 2.3 to 1

= 2.1 to 1

b. Acid-test ratio

= 1.2 to 1

= 1.2 to 1

c. Accounts (and notes) receivable turnover

= 4.9 times = 8.7 times

d. Inventory turnover

= 3.0 times = 5.9 times

e. Days’ sales in inventory

x 365 = 109.0 days x 365 = 62.4 days

f. Days’ sales uncollected

$393,600

($77,100 + $11,600 + $72,200)/2

$290,600

($86,800 + $105,100)/2

$86,800

$290,600

$205,200

$90,500

$108,700

$90,500

$208,100

$97,000

$116,000

$97,000

$480,000

($82,000 + $80,500)/2

$82,000

$480,000

$667,500

($70,500 + $9,000 + $73,300)/2

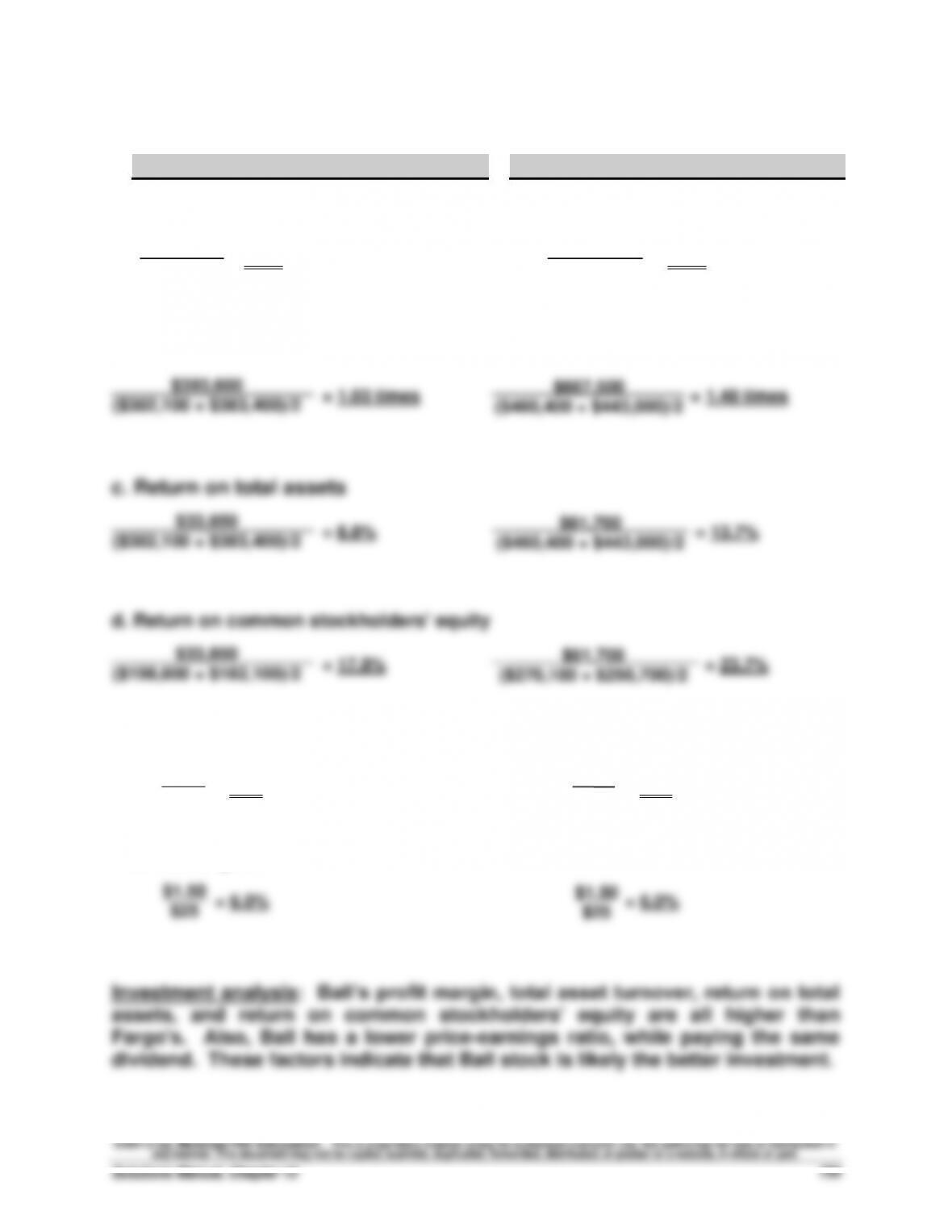

Problem 13-5B (Concluded)

Part 2

Fargo Company

Ball Company

a. Profit margin ratio

= 8.6% = 9.2%

b. Total asset turnover

e. Price-earnings ratio

= 19.7 = 11.4

f. Dividend yield

$33,850

$393,600

$25

$1.27

$61,700

$667,500

$25

$2.19

Financial & Managerial Accounting, 5th Edition

760

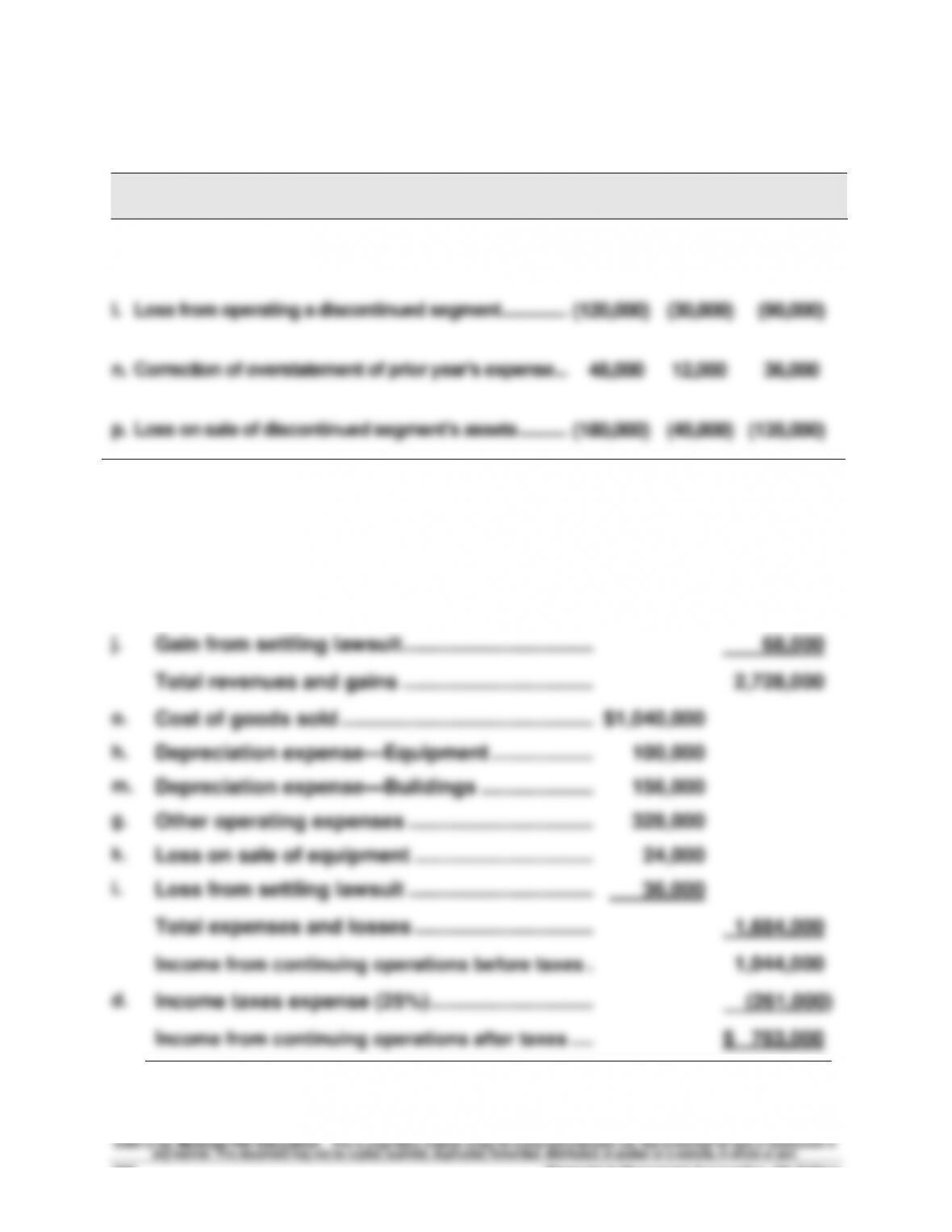

Problem 13–6BA (60 minutes)

Part 1 Effect of income taxes (debits or losses in parentheses)

Pretax

25% Tax

Effect

After-Tax

e. Loss on hurricane damage ……………………………………..……….

(64,000)

(16,000)

(48,000)

l. Loss from operating a discontinued segment …………………….

(120,000)

(30,000)

(90,000)

n. Correction of overstatement of prior year’s expense ………….

48,000

12,000

36,000

p. Loss on sale of discontinued segment’s assets ………..……….

(180,000)

(45,000)

(135,000)

Part 2 Income from continuing operations (and its components)

c.

Net sales ……………………………………………………….

$2,640,000

b.

Interest revenue …………………………………………………….

20,000

j.

Gain from settling lawsuit ……………………………..……….

68,000

Total revenues and gains ……………………………..……….

2,728,000

o.

Cost of goods sold ……………………………………….……….

$1,040,000

h.

Depreciation expense—Equipment ……………….……….

100,000

m.

Depreciation expense—Buildings ………………………….

156,000

g.

Other operating expenses …………………………….……….

328,000

k.

Loss on sale of equipment …………………………………….

24,000

i.

Loss from settling lawsuit …………………………….……….

36,000

Total expenses and losses …………………………………….

1,684,000

Income from continuing operations before taxes ..……….

1,044,000

d.

Income taxes expense (25%) …………………………..

(261,000)

Income from continuing operations after taxes …..……….

$ 783,000

Problem 13–6BA (Concluded)

Part 3 Income from discontinued segment

l.

Loss from operating a discontinued segment (after-tax) ………………

$ (90,000)

p.

Loss on sale of discontinued segment’s assets (after-tax) …..………

(135,000)

Loss from discontinued segment …………………………………………

$(225,000)

Part 4 Income before extraordinary items

Income from cont. operations after taxes (from Part 2) …….……….

$ 783,000

Loss from discontinued segment (from Part 3) ………………..……….

(225,000)

Income before extraordinary items ……………………………..……….

$ 558,000

Part 5 Net income

Income before extraordinary items ……………………………….……..

$ 558,000

Extraordinary item:

e.

Loss on hurricane damage (after-tax) …………………………………..

(48,000)

Net income …………………………..……………………………………………..

$ 510,000