Chapter 13

Analyzing Financial Statements

QUESTIONS

1. Financial reporting includes the entire process of preparing and issuing financial

2. With comparative statements, financial statement items for two or more successive

accounting periods are placed side by side on a single statement, with the change in

3. Total assets (or equivalently, the total of liabilities plus equity) are assigned a value of

4. The nature of a company’s business, the composition of its current assets, and the

5. A 2-to-1 current ratio may not be adequate if the company’s current assets consist of

6. Adequate working capital enables a company to carry sufficient inventories, meet

7. When evaluated in light of a company’s credit terms, the number of days’ sales

8. A high accounts receivable turnover implies that accounts are collected quickly,

9. Users are interested in the capital structure of a company, as measured by debt and

equity ratios, for at least two reasons. First, as a company includes more debt in its

10. Inventory turnover reflects on the efficiency of inventory management. That is, a

high inventory turnover means that a given sales volume can be supported with a

11. Since management is responsible for a company’s performance, all ratios that are

12. Almost all companies have some liabilities. Since total assets equals total liabilities

plus equity, total assets are almost always higher than common stockholders‘

13. This gain is considered to be unusual but not infrequent. It would be included in the

14. Profit margin: Net Income / Sales ($ in thousands)

15. Equity ratio: Total Equity / Total Assets ($ in thousands)

16. Debt ratio: Total Liabilities / Total Assets (€ in thousands)

17. Return on total assets: Net Income / Average Total Assets (€ in thousands)

QUICK STUDY

Quick Study 13-1 (5 minutes)

Items not part of general-purpose financial statements:

Quick Study 13-2 (5 minutes)

Trend percents

Quick Study 13-3 (5 minutes)

Common-size percents

Quick Study 13-4 (15 minutes)

2013

2012

Dollar

Change

Percent

Change

Short-term investments ………….

$374,634

$234,000

$140,634

60.1%

Accounts receivable ……………….

97,364

101,000

(3,636)

–3.6%

Notes payable…………………..…….

0

88,000

88,000

(not calculable)

Quick Study 13-5 (10 minutes)

The four usual standards of comparisons are:

• Intracompany. The company under analysis provides standards for

comparisons based on prior performance and relations between its

financial items.

All of these standards of comparisons are useful when properly applied.

Yet, analysis measures taken from a selected competitor or group of

Quick Study 13-6 (10 minutes)

Ratio

2013

2012

Change

1. Profit Margin Ratio …………………………..

9%

8%

Favorable

2. Debt Ratio …………………………………..…..

47%

42%

Unfavorable

3. Gross Margin Ratio ……………………..…..

34%

46%

Unfavorable

4. Acid-test Ratio…………………………….…..

1.00

1.15

Unfavorable

5. Accounts Receivable Turnover ………..

5.5

6.7

Unfavorable

6. Basic Earnings Per Share ………………..

$1.25

$1.10

Favorable

7. Inventory Turnover ……………………..…..

3.6

3.4

Favorable

8. Dividend Yield …………………………….…..

2.0%

1.2%

Favorable

Quick-Study 13-7 (30 minutes)

Parker has a greater amount of working capital. This by itself does not

indicate whether the company is more capable of meeting its current

obligations. However, support is provided by the current ratio and acid–

test ratio, which show Parker is in a more liquid position than Morgan. This

evidence does not mean that Morgan’s liquidity is inadequate. Such a

low returns.

The accounts receivable turnover and inventory turnover indicate that

Morgan is more efficient in collecting its accounts receivable and in

generating sales from available inventory. However, these statistics also

Quick Study 13-8A (5 minutes)

This material error should be reported on the statement of retained

earnings (and/or the statement of stockholders’ equity) as a prior period

Financial & Managerial Accounting, 5th Edition

728

Quick Study 13-9 (10 minutes)

a. Although ratio analysis can eliminate currency differences, it cannot

eliminate differences in the application of GAAP under different

accounting systems. For example, if we compare the gross margin

paragraph’s first example, however, many of these differences in asset

revaluations will be captured over time (multiple periods) with both

accounting systems.

b. A key advantage to using horizontal and vertical analyses when

examining companies reporting under different currencies is that the

computation of the percentages eliminates the currency effects. This

EXERCISES

Exercise 13-1 (10 minutes)

Exercise 13-4 (25 minutes)

Supporting calculations: When the sum of each year’s common-size cost of

goods sold and total expenses is subtracted from the common-size sales

percent, the net income percent is as follows:

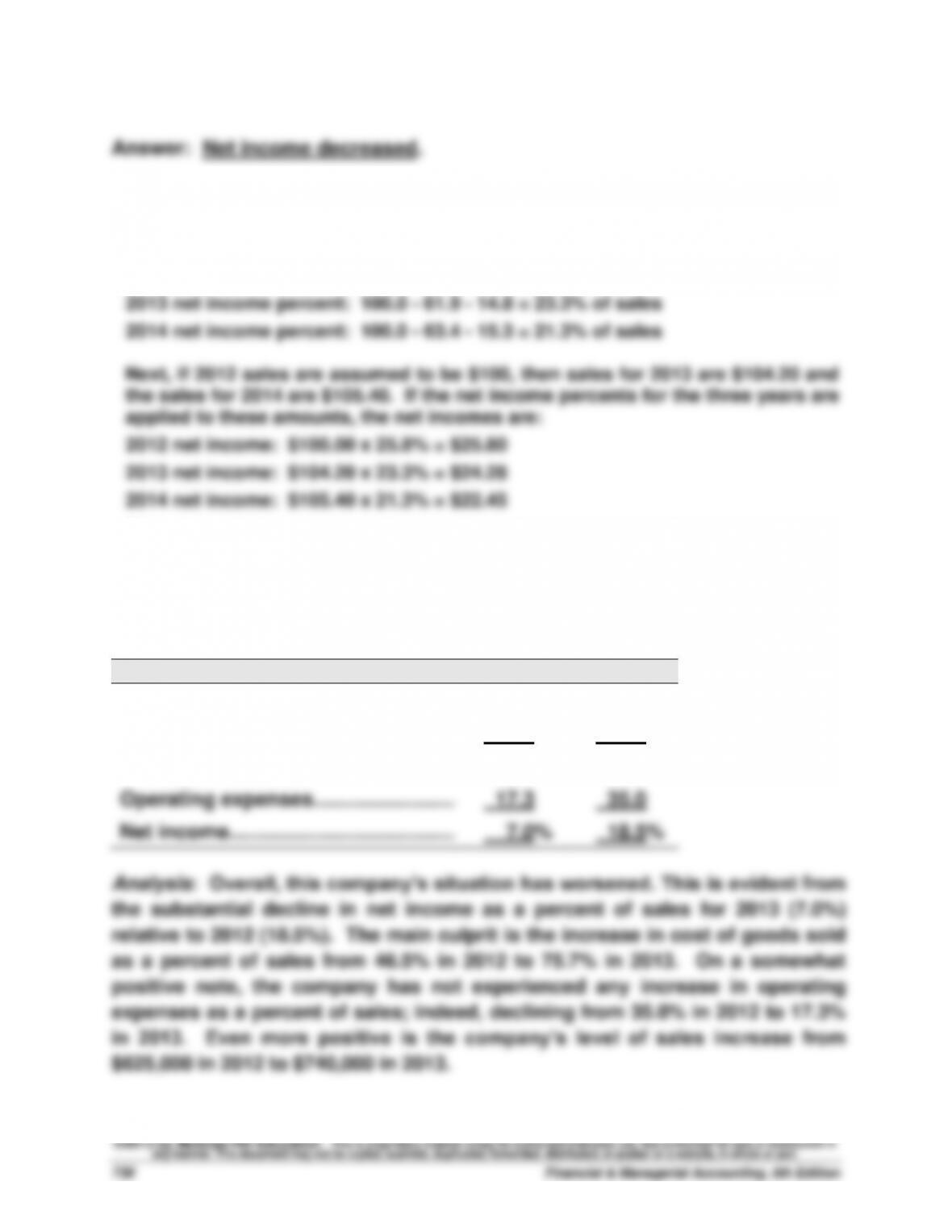

2012 net income percent: 100.0 – 59.1 – 15.1 = 25.8% of sales

This shows that net income decreased over the three-year period.

Exercise 13-5 (25 minutes)

2013

2012

Sales …………………………………………….

100.0%

100.0%

Cost of goods sold ……………………….

75.7

46.5

Gross profit ………………………………….

24.3

53.5

Operating expenses……………………...

17.3

35.0

Net income …………………………………...

7.0%

18.5%

Exercise 13-6 (30 minutes)

COMPARATIVE ANALYSIS REPORT

Clay’s profit margins are higher than Roak’s. However, Roak has

significantly higher total asset turnover ratios. As a result, Roak generates

a substantially higher return on total assets.

The trends of both companies include evidence of growth in sales, total

asset turnover, and return on total assets. However, Clay’s rates of

improvement are better than Roak’s. These differences may result from the

fact that Clay is only three years old, while Roak is a somewhat more

Financial & Managerial Accounting, 5th Edition

732

Exercise 13-7 (20 minutes)

Simon Company

Common-Size Comparative Balance Sheets

December 31, 2012-2014

At December 31

2014

2013*

2012

Assets

Cash ………………………………………………………….

6.1%

8.0%

10.0%

Accounts receivable, net …………………………….

17.1

14.0

13.3

Merchandise inventory ……………………………….

21.5

18.5

14.3

Prepaid expenses ……………………………………….

2.0

2.1

1.3

Plant assets, net ………………………………………..

53.3

57.3

61.1

Total assets ……………………………………………….

100.0%

100.0%

100.0%

Liabilities and Equity

Accounts payable ………………………………………

24.8%

16.9%

13.6%

Long-term notes payable secured by

mortgages on plant assets ……………………..

18.8

22.9

22.1

Common stock, $10 par value …………………….

31.3

36.7

43.3

Retained earnings ……………………………………..

25.1

23.5

21.0

Total liabilities and equity …………………………..

100.0%

100.0%

100.0%

* Column does not equal 100.0 due to rounding.

Analysis: Several observations can be made.

(1) Cash as a percent of assets has declined—this is favorable provided sufficient

cash is available for operations.

(2) Accounts receivable have increased as a percent of assets—this may be

unfavorable in that assets are tied up in an unproductive manner and there would

Exercise 13-8 (25 minutes)

1. Current ratio

2. Acid-test ratio

Analysis and Interpretation: Simon’s short-term liquidity position has

deteriorated over this three-year period. Both the current and acid-test

ratios show declining trends. Although we do not have information about

$51,250

$51,250

Exercise 13-9 (25 minutes)

1. Days’ sales uncollected

$673,500

2. Accounts receivable turnover

3. Inventory turnover

4. Days’ sales in inventory

$411,225

$82,500

Analysis and Interpretation: The number of days’ sales uncollected has

increased and the accounts receivable turnover has declined. Also, the

$89,500

$673,500

$112,500

$345,500

Exercise 13-10 (25 minutes)

1. Debt and equity ratios

2014

2013

Total liabilities and debt ratio

$129,900 + $98,500 …………………..

$228,400

43.7%

$75,250 + $101,500 …………………..

$176,750

39.7%

Total equity and equity ratio

$163,500 + $131,100 …………….…..

294,600

56.3

$163,500 + $104,750 …………….…..

_______

_____

268,250

60.3

Total liabilities and equity ……………

$523,000

100.0%

$445,000

100.0%

2. Debt–to-equity ratio

3. Times interest earned

Analysis and Interpretation: Simon added debt to its capital structure

during 2014, with the result that the debt ratio increased from 39.7% to

Exercise 13-11 (30 minutes)

1. Profit margin

2014: $31,100 / $673,500 = 4.6%

2013: $29,375 / $532,000 = 5.5%

2. Total asset turnover

3. Return on total assets

Analysis and Interpretation: Simon’s operating efficiency appears to be

declining because the return on total assets decreased from 7.1% to 6.4%.

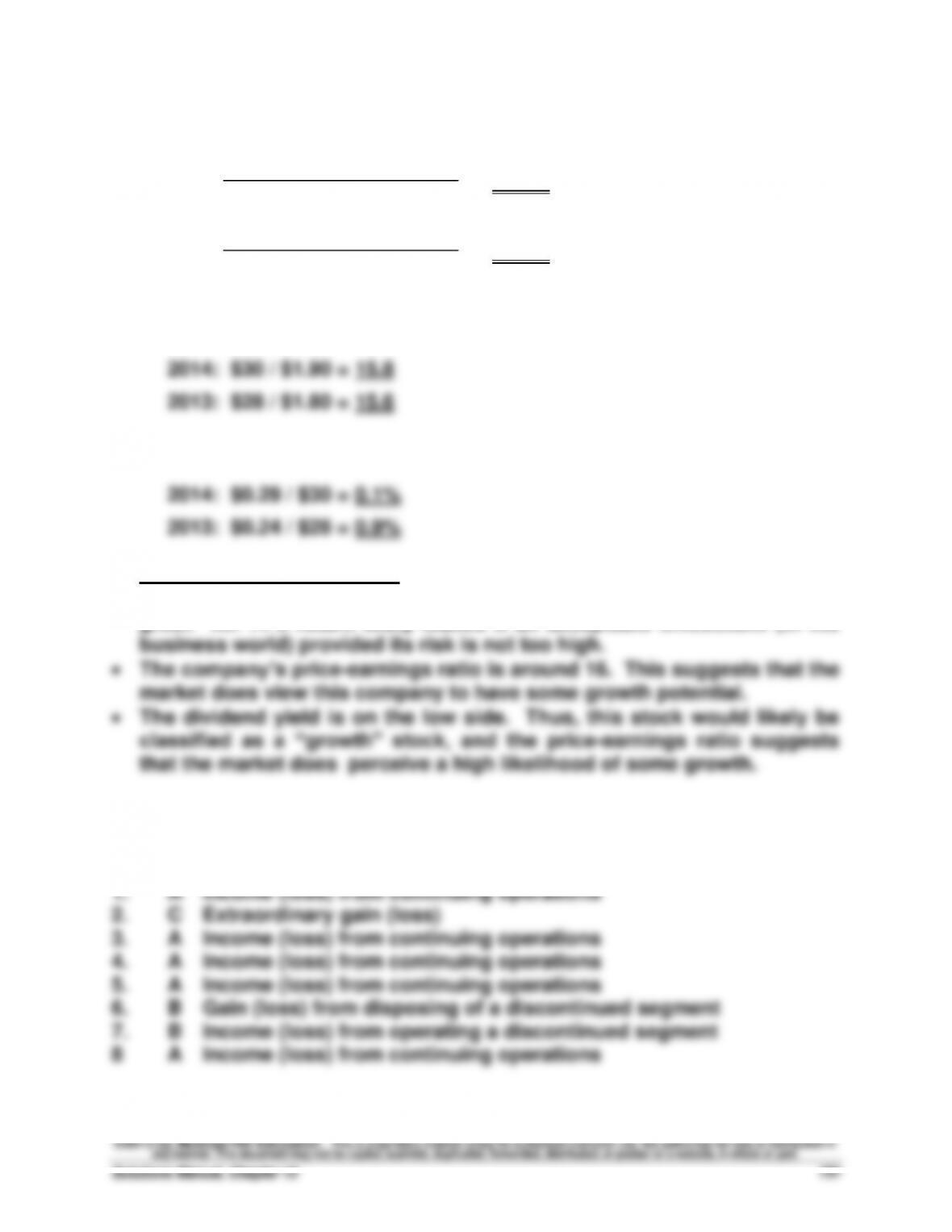

Exercise 13-12 (20 minutes)

1. Return on common stockholders’ equity

2014: = 11.1%

2013: = 11.5%

2. Price-earnings ratio, December 31

3. Dividend yield

Analysis and interpretation

• The company’s return on common stockholders’ equity is good, but not

great. An 11% return likely makes it an acceptable investment (in the

Exercise 13-13A (10 minutes)

$31,100

($294,600 + $268,250)/2

$29,375

($268,250 + $242,750)/2