Chapter 12 – Reporting and Analyzing Cash Flows

website, in whole or part. 12-9

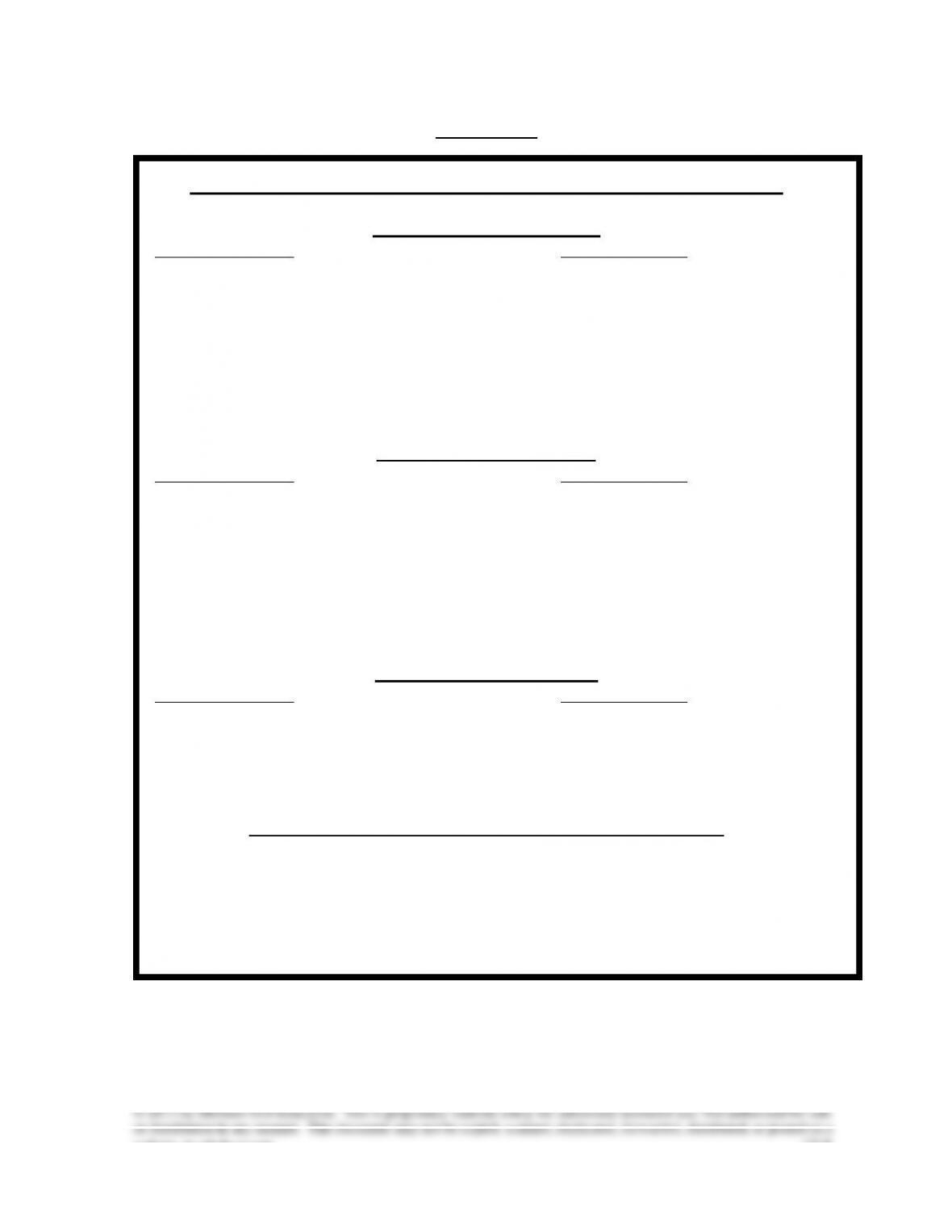

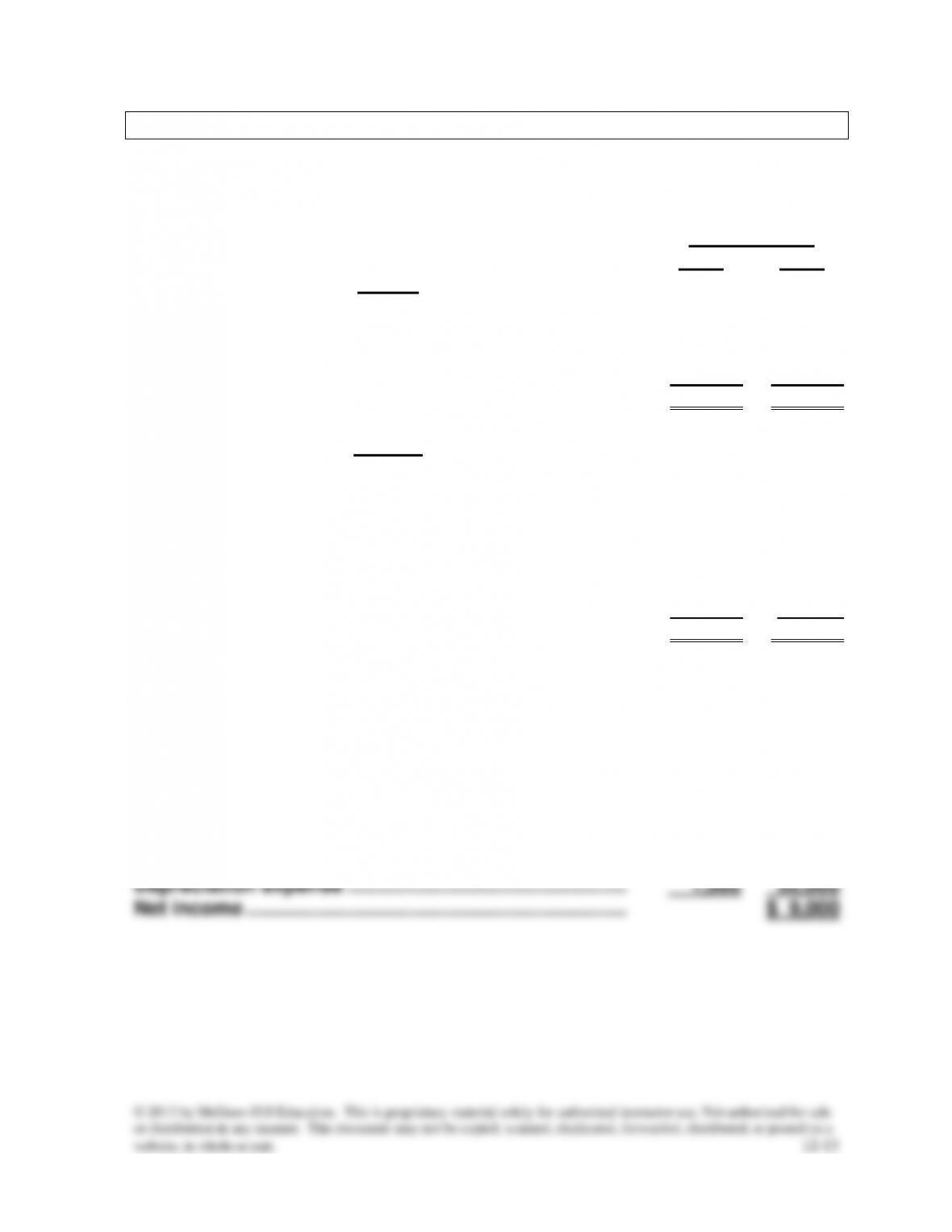

VISUAL #12-1

CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS

OPERATING ACTIVITIES

Cash inflows from Cash outflows to

• Sale of goods or services • Suppliers of goods and

• Interest services

• Dividends • Salaries and wages

• Sale of trading securities • Government for taxes

• Other operating receipts • Lenders for interest

• Purchase trading securities

• Others for expenses

INVESTING ACTIVITIES

Cash inflows from Cash outflows to

• Sale of property, plant, • Purchase property, plant,

and equipment and equipment

• Sale of debt or equity securities • Purchase debt or equity

of other entities securities of other entities

• Collection of principal on loans • Make loans to another entity

to other entities

• Selling (discounting) of loans

FINANCING ACTIVITIES

Cash inflows from Cash outflows to

• Sale of capital stock (or owner • Shareholders as dividends (or

investment) owner’s withdrawal)

• Issuance of debt (bonds and notes) • Repay debts

• Issuing short-term liabilities • Purchase treasury stock

NONCASH INVESTING AND FINANCING ACTIVITIES

• Retirement of debt by issuing stock

• Conversion of preferred stock to common stock

• Purchase of a long-term asset by issuing a note payable

• Leasing of assets classified as a capital lease

Chapter 12 – Reporting and Analyzing Cash Flows

website, in whole or part. 12–10

VISUAL #12-2

STEPS TO DETERMINE INFORMATION

STATEMENT OF CASH FLOWS

1. Find Change in Cash—This is the target number.

2. Find Cash Flow From Operations

(Using direct or indirect method)

3. Find Cash Flow from A. Financing and

B. Investing

Procedure:

In real life: Using data from comparative balance sheets, trace

changes through ledgers and journals probably using a

worksheet to organize, analyze, and prove data disclosed.

In the classroom: Determine the changes in noncurrent accounts

and notes from comparative balance sheets. Use the relevant

data the text provides that comes from the ledgers and the

journals to systematically analyze the data using chart and/or

reconstructing journal entries.

4. Combine cash flows from all three activities (from 2 and 3) to

find net cash flow and prove change in cash. (Target number

determined in Step 1).

Note: Once the above information has been gathered, the statement

can be prepared following the required format. If the direct method

was used, GAAP requires a reconciliation of net income to cash

provided from operations.

Chapter 12 – Reporting and Analyzing Cash Flows

website, in whole or part. 12–11

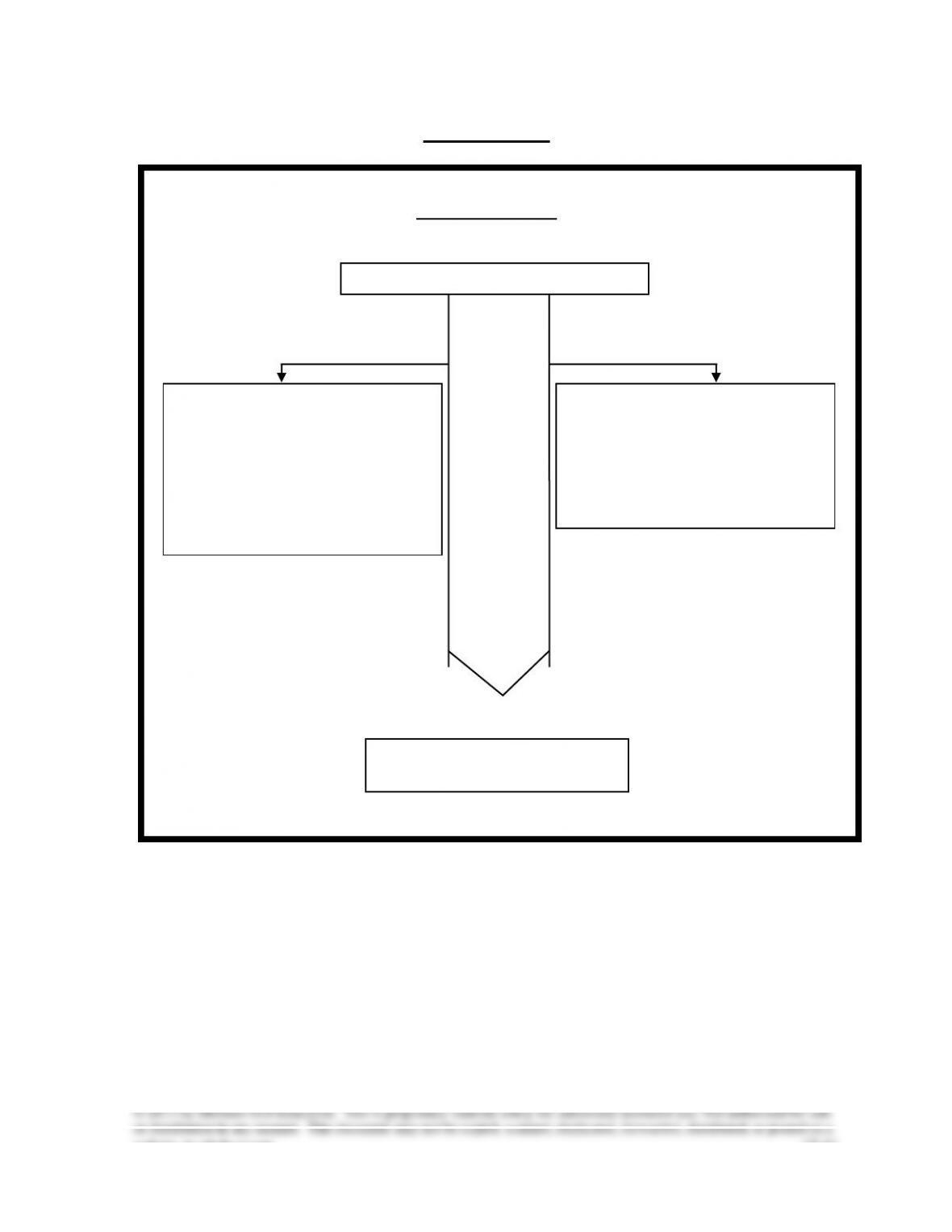

VISUAL #12-2

Determining Cash Flows from Operating Activities

Indirect Method

START WITH

NET INCOME OR (NET LOSS)

Add Subtract

1. Write-offs or noncash 1. Gains

expenses 2. Increases in current assets

2. Losses 3. Decreases in current

3. Decreases in current assets liabilities

4. Increases in current

liabilities.

RESULT

CASH FLOWS FROM

OPERATING ACTIVITIES

Chapter 12 – Reporting and Analyzing Cash Flows

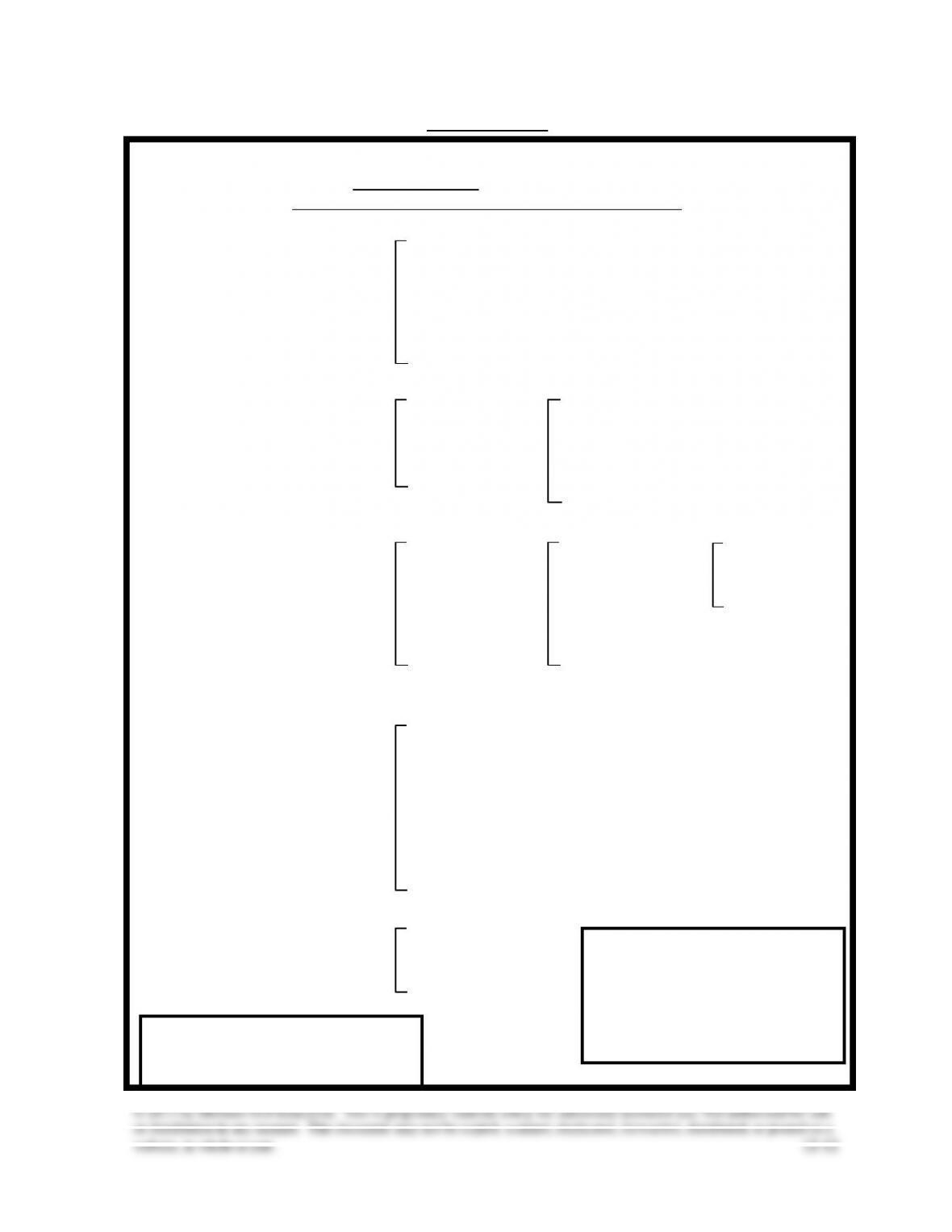

VISUAL #12-3

Determining Cash Flows from Operating Activities

Direct Method (Appendix 12B)

(Need income statement and balance sheet data)

1. Cash = Sales + Decrease in

Receipts Accounts

from Customers* Receivable

or

– Increase in

Accounts

Receivable

2. Cash = Cost of + Increase in + Decrease in

Payments Goods Sold Inventory Accounts

to Suppliers or Payable

– Decrease in – Increase in

Inventory Accounts

Payable

3. Cash = Operating + Increase in + Decrease in –

Depreciation

Payments Expenses Prepaid Accrued and Other

for Expenses Liabilities Noncash

Operating** or or Expenses

Expenses – Decrease in – Increase in

Prepaid Accrued

Expenses Liabilities

4. Cash = Income + Decrease in

Payments Taxes Income

for Expense Taxes

Income Payable

Taxes or

– Increase in

Income

Taxes

Payable

5. Cash = Interest + Decreases in

Payments Expense Interest Payable **Wage expense would be

for – Increase in taken out if CP for wages was

Interest Interest Payable to be reported separately.

The related prepaids and

*use similar computations for payables would be considered

CR from Interest in the computation.

CR from Dividends

Chapter 12 – Reporting and Analyzing Cash Flows

Chapter 12 – Alternate Demonstration Problem #1

The Carpet Company’s 2014 and 2013 balance sheets:

December 31

2014

2013

Debits

Cash ……………………………………………………………………

$10,500

$ 4,000

Accounts receivable …………………………………………….

8,000

9,000

Merchandise inventory …………………………………………

21,000

18,000

Equipment ……………………………………………………………

18,000

15,000

Totals ………………………………………………………….

$57,500

$46,000

Credits

Accumulated depreciation, equipment ………………….

$ 4,000

$ 3,000

Accounts payable …………………………………………………

7,000

5,000

Taxes payable ………………………………………………………

1,000

2,000

Dividends payable ………………………………………………..

1,500

0

Common stock, $10 par value ……………………………….

27,000

25,000

Contributed capital in excess of par, common stock

6,000

5,000

Retained earnings ………………………………………………..

11,000

6,000

Totals ………………………………………………………….

$57,500

$46,000

The Carpet Company’s income statement:

For the Year Ended December 31, 2014

Sales ……………………………………………………………………

$61,000

Cost of goods sold ……………………………………………….

$40,000

Wages and other operating expenses……………………

6,300

Income taxes expense ………………………………………….

4,200

Depreciation expense …………………………..………………

1,500

52,000

Net income …………………………………………………………..

$ 9,000

Chapter 12 – Reporting and Analyzing Cash Flows

website, in whole or part. 12–14

Chapter 12 – Alternate Demonstration Problem #1, continued

Additional information includes the following:

a. Equipment costing $3,500 was purchased during the year.

b. Fully depreciated equipment that cost $500 was discarded and its

cost and accumulated depreciation were removed from the

accounts.

c. Two hundred shares of stock were sold and issued at $15 per

share.

d. The company declared $4,000 of cash dividends and paid $2,500.

Required:

Prepare the statement of cash flows for the year ended December 31,

2014, using the:

1. Indirect method.

2. Direct method (Appendix 12B).

Chapter 12 – Reporting and Analyzing Cash Flows

website, in whole or part. 12–15

1. Indirect Method:

CARPET COMPANY

Statement of Cash Flows

For Year Ended December 31, 2014

Cash flows from operating activities:

Net income …………………………………………………………….

$ 9,000

Adjustments to reconcile net income to net cash

provided by operating activities:

Decrease in accounts receivable ……………………….

1,000

Increase in merchandise inventory ……………………

(3,000

)

Increase in accounts payable …………………………...

2,000

Decrease in taxes payable …………………………………

(1,000

)

Depreciation expense ……………………………………….

1,500

Net cash provided by operating activities ………….

$ 9,500

Cash flows from investing activities:

Cash paid for purchase of plant asset ……………….

(3,500

)

Net cash used by investing activities ………………..

(3,500

)

Cash flows from financing activities:

Cash received from issuing stock ……………………..

3,000

Cash paid for dividends …………………………………….

(2,500

)

Net cash provided by financing activities ………….

500

Net increase in cash ……………………………………………….

6,500

Cash balance at beginning of 2014 …………………………

4,000

Cash balance at end of 2014 …………………………………..

$10,500

Chapter 12 – Reporting and Analyzing Cash Flows

Solution: Chapter 12 – Alternate Demonstration Problem #1, continued

2. Direct Method:

CARPET COMPANY

Statement of Cash Flows

For Year Ended December 31, 2014

Cash flows from operating activities:

Cash received from customers ………………………….

$ 62,000

Cash paid for merchandise ……………………………….

(41,000

)

Cash paid for wages and other operating

expenses ………………………………………………………

(6,300

)

Cash paid for taxes …………………………………………..

(5,200

)

Net cash provided by operating activities ………….

$ 9,500

Cash flows from investing activities:

Cash paid for purchase of plant assets ……………..

(3,500

)

Net cash used by investing activities ………………..

(3,500

)

Cash flows from financing activities:

Cash received from issuing stock ……………………..

3,000

Cash paid for dividends …………………………………….

(2,500

)

Net cash provided by financing activities ………….

500

Net increase in cash ……………………………………………….

$ 6,500

Cash balance at beginning of 2014 …………………………

4,000

Cash balance at end of 2014 …………………………………..

$10,500