Financial & Managerial Accounting, 5th Edition

600

Problem 10-3B (Concluded)

Part 4

Semiannual

Period-End

Unamortized

Premium

Carrying

Value

1/01/2013 ………….……..

$792,932

$4,192,932

6/30/2013 ………….……..

753,285

4,153,285

12/31/2013 ………….……..

713,638

4,113,638

6/30/2014 ………….……..

673,991

4,073,991

12/31/2014 ………….……..

634,344

4,034,344

Part 5

2013

June 30

Bond Interest Expense …………………………..

130,353

Premium on Bonds Payable ………………….……….

39,647

Cash ……………………………………………….………

170,000

To record six months’ interest and

premium amortization.

2013

Dec. 31

Bond Interest Expense …………………………..

130,353

Premium on Bonds Payable ………………….……….

39,647

Cash ……………………………………………….………

170,000

To record six months’ interest and

premium amortization.

Problem 10-4B (45 minutes)

Part 1

Ten payments of $14,400* …………………….

$ 144,000

Par value at maturity ……………………..……

320,000

Total repaid ………………………………………….

464,000

Less amount borrowed ………………….…….

(332,988)

Total bond interest expense …………..…….

$ 131,012

*$320,000 x 0.09 x ½ = $14,400

or:

Ten payments of $14,400 ……………….…….

$ 144,000

Less premium………………………………..…….

(12,988)

Total bond interest expense …………..…….

$ 131,012

Part 2

Straight-line amortization table ($12,988/10 = $1,299**)

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2013

$12,988

$332,988

6/30/2013

11,689

331,689

12/31/2013

10,390

330,390

6/30/2014

9,091

329,091

12/31/2014

7,792

327,792

6/30/2015

6,493

326,493

12/31/2015

5,194

325,194

6/30/2016

3,895

323,895

12/31/2016

2,596

322,596

6/30/2017

1,299*

321,299

12/31/2017

0

320,000

Financial & Managerial Accounting, 5th Edition

602

Problem 10-4B (Concluded)

Part 3

2013

June 30

Bond Interest Expense …………………………..

13,101

Premium on Bonds Payable ………………….……….

1,299

Cash ……………………………………………….………

14,400

To record six months’ interest and

premium amortization.

2013

Dec. 31

Bond Interest Expense …………………………..

13,101

Premium on Bonds Payable ………………….……….

1,299

Cash ……………………………………………….………

14,400

To record six months’ interest and

premium amortization.

Problem 10–5BB (45 minutes)

Part 1

Ten payments of $14,400 ……………….…….

$144,000

Par value at maturity ……………………..……

320,000

Total repaid ………………………………………….

464,000

Less amount borrowed ………………….…….

(332,988)

Total bond interest expense …………..…….

$131,012

or:

Ten payments of $14,400 ……………….…….

$144,000

Less premium………………………………..…….

(12,988)

Total bond interest expense …………..…….

$131,012

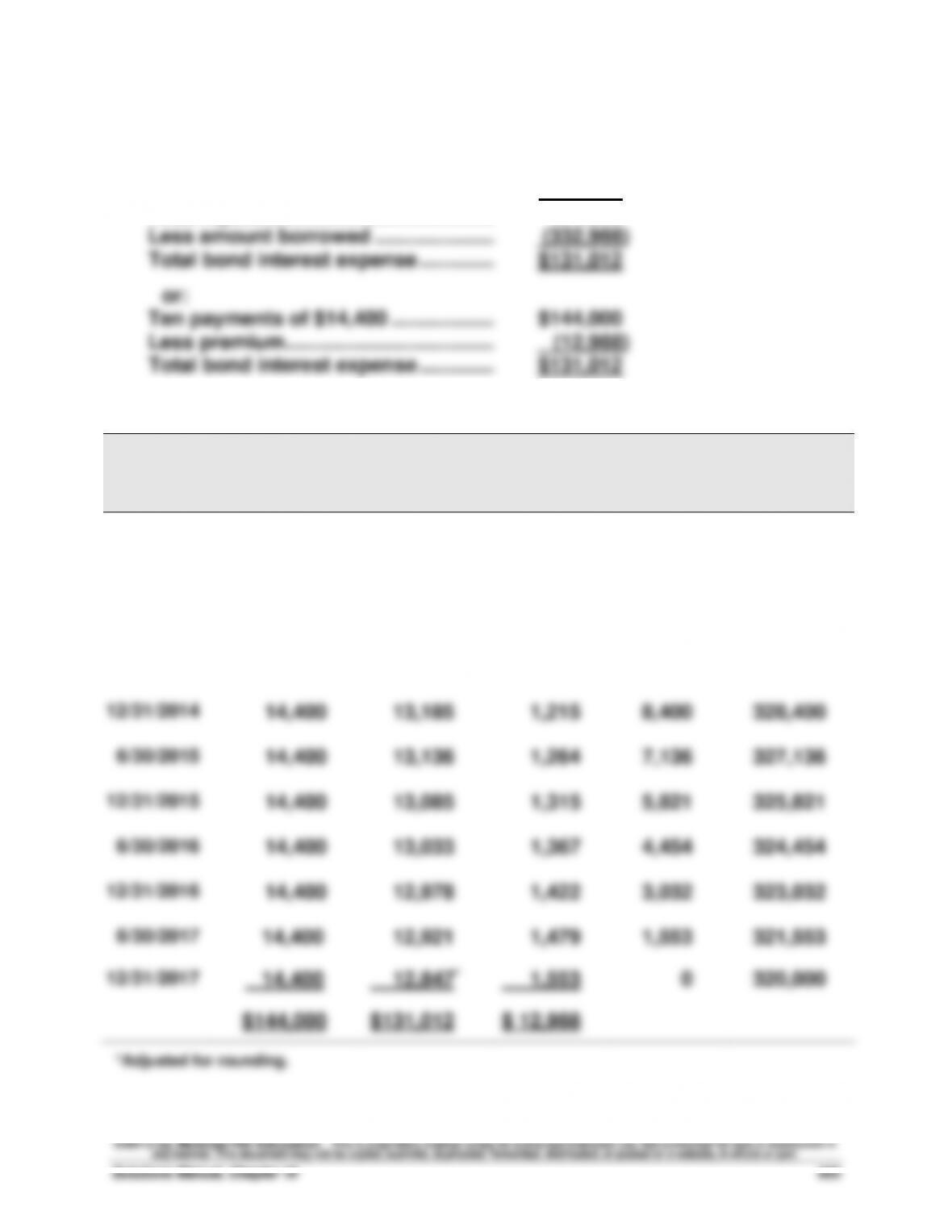

Part 2

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[4.5% x $320,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$320,000 + (D)]

1/01/2013

$12,988

$332,988

6/30/2013

$ 14,400

$ 13,320

$ 1,080

11,908

331,908

12/31/2013

14,400

13,276

1,124

10,784

330,784

6/30/2014

14,400

13,231

1,169

9,615

329,615

12/31/2014

14,400

13,185

1,215

8,400

328,400

6/30/2015

14,400

13,136

1,264

7,136

327,136

12/31/2015

14,400

13,085

1,315

5,821

325,821

6/30/2016

14,400

13,033

1,367

4,454

324,454

12/31/2016

14,400

12,978

1,422

3,032

323,032

6/30/2017

14,400

12,921

1,479

1,553

321,553

12/31/2017

14,400

12,847*

1,553

0

320,000

$144,000

$131,012

$ 12,988

*Adjusted for rounding.

Financial & Managerial Accounting, 5th Edition

604

Problem 10–5BB (Concluded)

Part 3

2013

June 30

Bond Interest Expense …………………………..

13,320

Premium on Bonds Payable ………………….……….

1,080

Cash ……………………………………………….………

14,400

To record six months’ interest and

premium amortization.

2013

Dec. 31

Bond Interest Expense …………………………..

13,276

Premium on Bonds Payable ………………….……….

1,124

Cash ……………………………………………….………

14,400

To record six months’ interest and

premium amortization.

Part 4

As of December 31, 2015

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ……………..

B.1

0.8548

$320,000

$273,536

Interest (annuity) ….

B.3

3.6299

14,400

52,271

Price of bonds ……..

$325,807

* Table values are based on a discount rate of 4% (half the annual original market

rate) and 4 periods (semiannual payments).

Comparison to Part 2 Table

Except for a small rounding difference, this present value ($325,807) equals

the carrying value of the bonds in column (E) of the amortization table

Problem 10–6B (60 minutes)

Part 1

2013

Jan. 1

Cash …………………………………………………….…

198,494

Discount on Bonds Payable ………………….……….

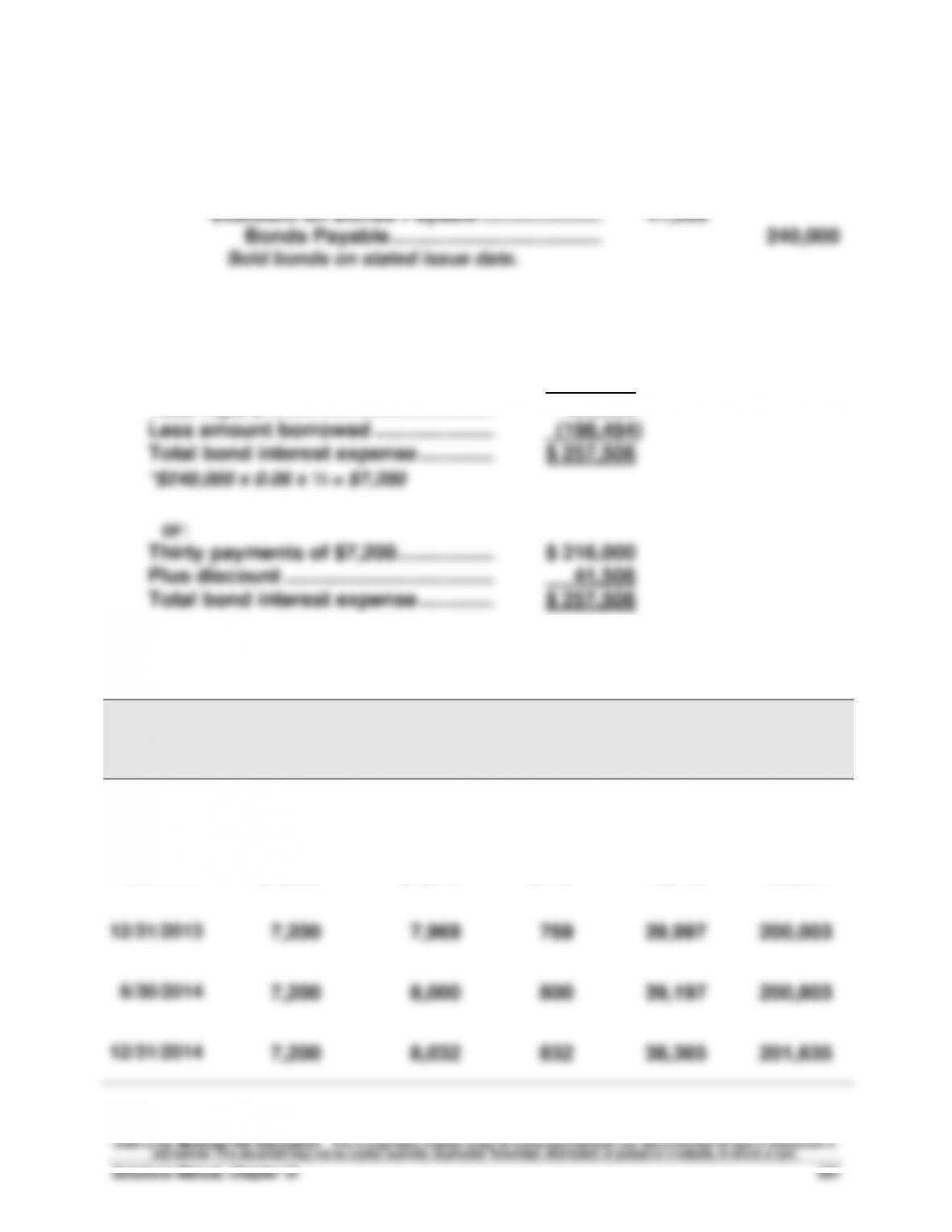

41,506

Bonds Payable ………………………………..……………….

240,000

Sold bonds on stated issue date.

Part 2

Thirty payments of $7,200* ……………..…….

$ 216,000

Par value at maturity ……………………..……

240,000

Total repaid ………………………………………….

456,000

Less amount borrowed ………………….…….

(198,494)

Total bond interest expense …………..…….

$ 257,506

$240,000 x 0.06 x ½ = $7,200

or:

Thirty payments of $7,200* …………….…….

$ 216,000

Plus discount ………………………………..…….

41,506

Total bond interest expense …………..…….

$ 257,506

* Semiannual interest payment, computed as $240,000 x 6% x ½ year.

Part 3 Straight-line amortization table ($41,506/30= $1,384)

Semiannual

Interest Period-End

Unamortized

Discount

Carrying

Value

1/01/2013

$41,506

$ 198,494

6/30/2013

40,122

199,878

12/31/2013

38,738

201,262

6/30/2014

37,354

202,646

12/31/2014

35,970

204,030

Financial & Managerial Accounting, 5th Edition

606

Problem 10-6B (Concluded)

Part 4

2013

June 30

Bond Interest Expense …………………………..

8,584

Discount on Bonds Payable …………….…………….

1,384

Cash ……………………………………………….………

7,200

To record six months’ interest and

discount amortization.

2013

Dec. 31

Bond Interest Expense …………………………..

8,584

Discount on Bonds Payable …………….…………….

1,384

Cash ……………………………………………….………

7,200

To record six months’ interest and

discount amortization.

Problem 10–7BB (60 minutes)

Part 1

2013

Jan. 1

Cash …………………………………………………….…

198,494

Discount on Bonds Payable ………………….……….

41,506

Bonds Payable ………………………………..……………….

240,000

Sold bonds on stated issue date.

Part 2

Thirty payments of $7,200* ……………..…….

$ 216,000

Par value at maturity ……………………..……

240,000

Total repaid ………………………………………….

456,000

Less amount borrowed ………………….…….

(198,494)

Total bond interest expense …………..…….

$ 257,506

*$240,000 x 0.06 x ½ = $7,200

or:

Thirty payments of $7,200 …………………….

$ 216,000

Plus discount ………………………………..…….

41,506

Total bond interest expense …………..…….

$ 257,506

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[3% x $240,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Discount

Amortization

[(B) – (A)]

(D)

Unamortized

Discount

[Prior (D) – (C)]

(E)

Carrying

Value

[$240,000 – (D)]

1/01/2013

$41,506

$198,494

6/30/2013

$7,200

$7,940

$740

40,766

199,234

12/31/2013

7,200

7,969

769

39,997

200,003

6/30/2014

7,200

8,000

800

39,197

200,803

12/31/2014

7,200

8,032

832

38,365

201,635

Financial & Managerial Accounting, 5th Edition

608

Problem 10–7BB (Concluded)

Part 4

2013

June 30

Bond Interest Expense …………………………..

7,940

Discount on Bonds Payable …………….…………….

740

Cash ……………………………………………….………

7,200

To record six months’ interest and

discount amortization.

2013

Dec. 31

Bond Interest Expense …………………………..

7,969

Discount on Bonds Payable …………….…………….

769

Cash ……………………………………………….………

7,200

To record six months’ interest and

discount amortization.

Problem 10–8BB (70 minutes)

Part 1

2013

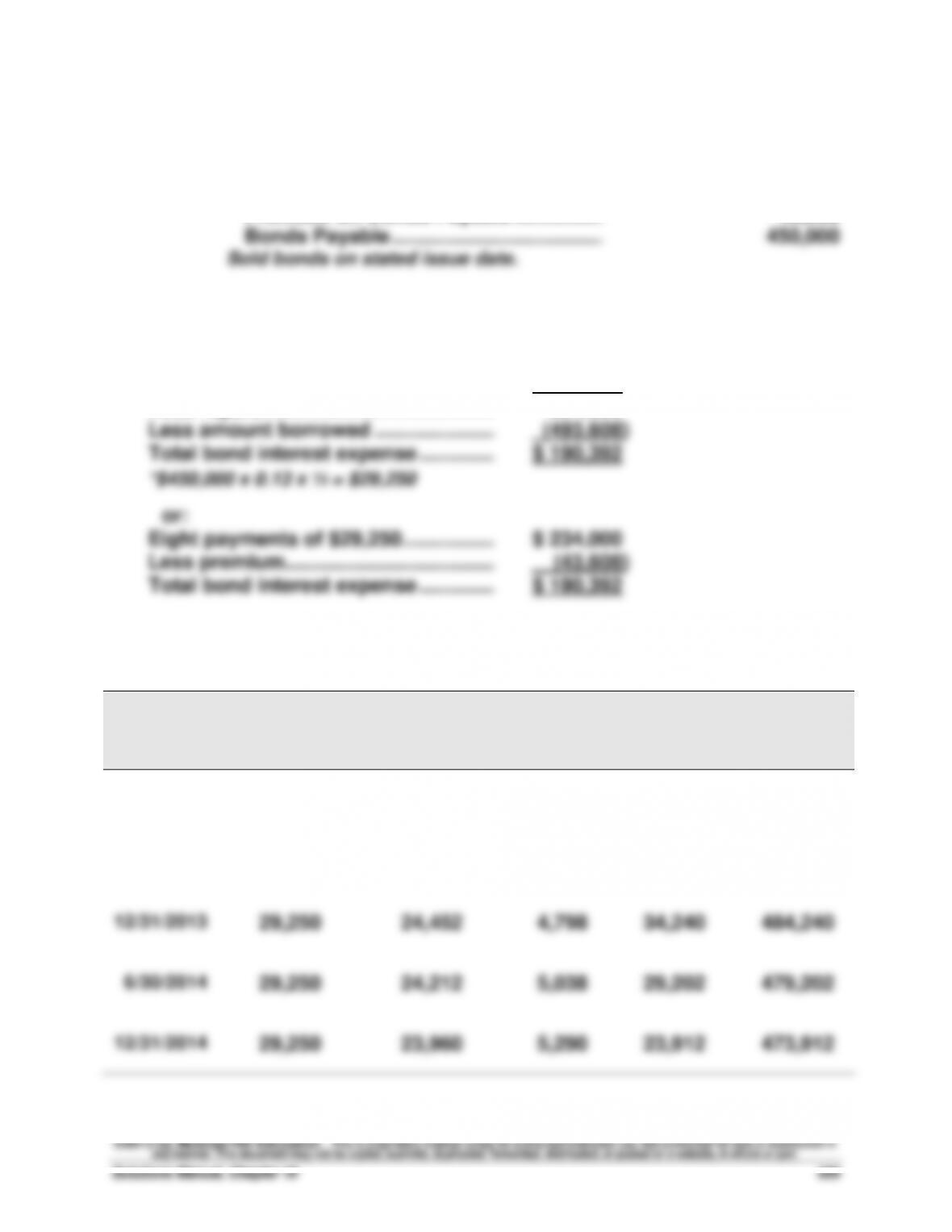

Jan. 1

Cash …………………………………………………….…

493,608

Premium on Bonds Payable …………….…………….

43,608

Bonds Payable ………………………………..……………….

450,000

Sold bonds on stated issue date.

Part 2

Eight payments of $29,250* ………………….

$ 234,000

Par value at maturity ……………………..……

450,000

Total repaid ………………………………………….

684,000

Less amount borrowed ………………….…….

(493,608)

Total bond interest expense …………..…….

$ 190,392

*$450,000 x 0.13 x ½ = $29,250

or:

Eight payments of $29,250 ……………..…….

$ 234,000

Less premium………………………………..…….

(43,608)

Total bond interest expense …………..…….

$ 190,392

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[6.5% x $450,000]

(B)

Bond Interest

Expense

[5% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$450,000 + (D)]

1/01/2013

$43,608

$493,608

6/30/2013

$29,250

$24,680

$4,570

39,038

489,038

12/31/2013

29,250

24,452

4,798

34,240

484,240

6/30/2014

29,250

24,212

5,038

29,202

479,202

12/31/2014

29,250

23,960

5,290

23,912

473,912

Problem 10–8BB (Concluded)

Part 4

2013

June 30

Bond Interest Expense …………………………..

24,680

Premium on Bonds Payable ………………….……….

4,570

Cash ……………………………………………….………

29,250

To record six months’ interest and

premium amortization.

2013

Dec. 31

Bond Interest Expense …………………………..

24,452

Premium on Bonds Payable ………………….……….

4,798

Cash ……………………………………………….………

29,250

To record six months’ interest and

premium amortization.

Part 5

2015

Jan. 1

Bonds Payable …………………………………….……………….

450,000

Premium on Bonds Payable ………………….……….

23,912

Loss on Retirement of Bonds ……………….………….

3,088

Cash*……………………………………………………….

477,000

To record the retirement of bonds.

*($450,000 x 106%)

Part 6

If the market rate on the issue date had been 14% instead of 10%, the bonds

would have sold at a discount because the contract rate of 13% would have been

lower than the market rate.

This change would affect the balance sheet because the bond liability would be

smaller (par value minus a discount instead of par value plus a premium). As the

Problem 10-9B (45 minutes)

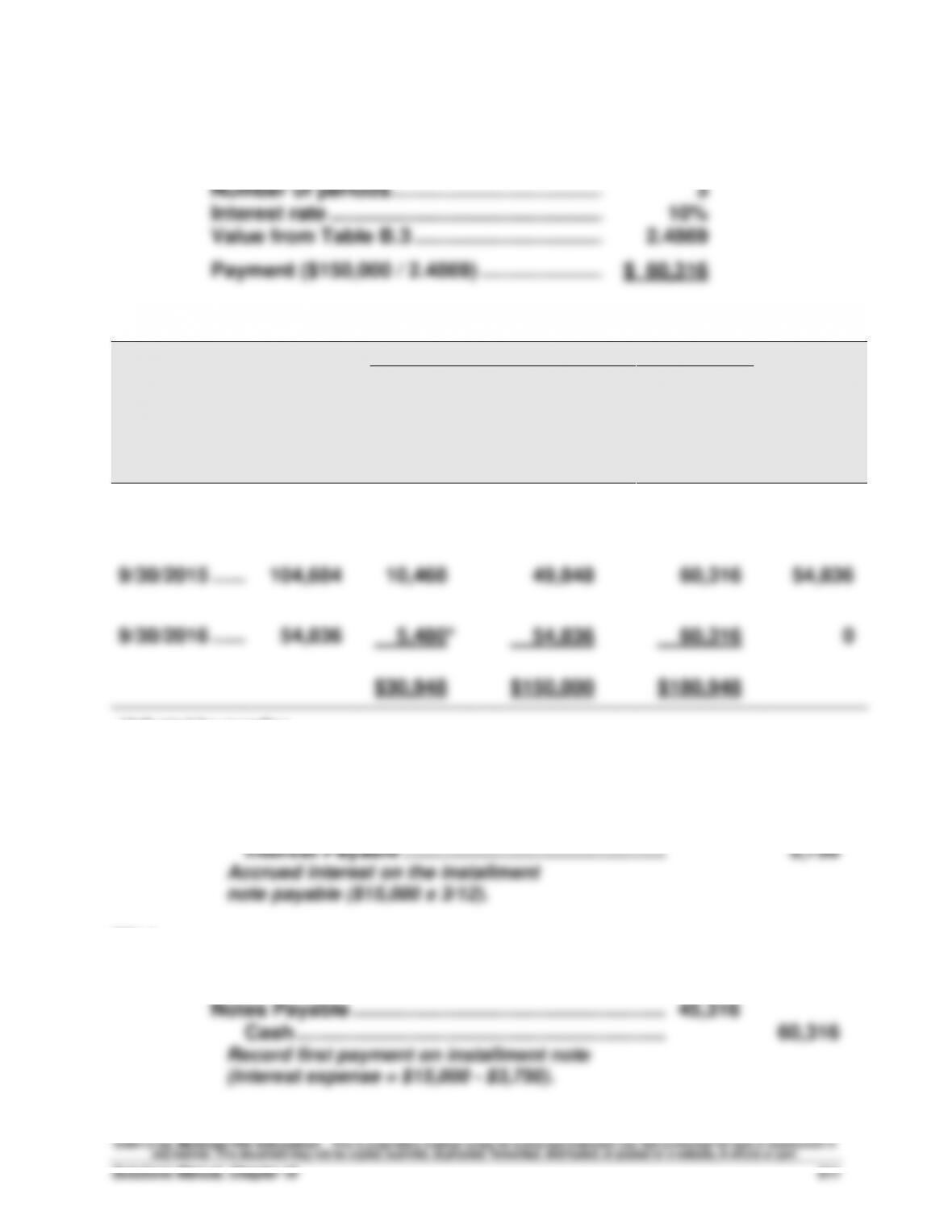

Part 1 Amount of Payment

Note balance ………………………………………..……………..

$150,000

Number of periods ………………………………..……………….

3

Interest rate ………………………………………….……………

10%

Value from Table B.3 …………………………….……………….

2.4869

Payment ($150,000 / 2.4869) ………………….……….

$ 60,316

Part 2

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[10% x (A)]

+

(C)

Debit

Notes

Payable

[(D) – (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

9/30/2014 ………….

$150,000

$15,000

$ 45,316

$ 60,316

$104,684

9/30/2015 ………….

104,684

10,468

49,848

60,316

54,836

9/30/2016 ………….

54,836

5,480*

54,836

60,316

0

$30,948

$150,000

$180,948

*Adjusted for rounding.

Part 3

2013

Dec. 31

Interest Expense …………………………..………………..……..

3,750

Interest Payable ………………………………………..……..

3,750

Accrued interest on the installment

note payable ($15,000 x 3/12).

2014

Sept. 30

Interest Expense …………………………..………………..……..

11,250

Interest Payable ……………………………………………..……..

3,750

Notes Payable ………………………………………………..……..

45,316

Cash ………………………………………………………………..

60,316

Record first payment on installment note

(interest expense = $15,000 – $3,750).