Chapter 10 – Long-Term Liabilities

Chapter Outline

2. Term or Serial

a. Term bonds and notes are scheduled for maturity on one

specified date.

b. Serial bonds and notes mature at more than one date (often in

series) and are usually repaid over a number of periods.

3. Registered or Bearer

a. Registered bonds are issued in the names and addresses of

their holders. Bond payments are sent directly to registered

holders.

b. Bearer bonds, also called unregistered bonds, are made

payable to whoever holds them (the bearer). Many bearer bonds

are also coupon bonds; which are interest coupons that are

attached to the bonds.

4. Convertible and/or Callable

a. Convertible bonds and notes can be exchanged for a fixed

number of shares of the issuing company’s common stock.

b. Callable bonds and notes have an option exercisable by the

issuer to retire them at a stated dollar amount before maturity.

B. Debt-to-Equity Ratio

1. Knowing the level of debt helps in assessing the risk of a

company’s financing structure.

2. A company financed mainly with debt is riskier than a company

financed mainly with equity because liabilities must be repaid.

3. Debt-to-equity ratio measures the risk of a company’s financing

structure.

4. Debt-to-equity ratio is computed by dividing total liabilities by

A. Present Value Concepts

1. Cash paid (or received) in the future has less value now than the

same amount of cash paid (or received) today.

4. Present Value tables can be used to determine the present value

of future cash payments of a single amount or an annuity.

B. Present Value Tables (Complete tables in Appendix B)

single payment.

Chapter 10 – Long-Term Liabilities

Chapter Outline

Notes

3. Present value of an annuity of $1 table is used to compute

present value of a series of equal payments (annuity).

C. Applying a Present Value Table (Complete tables in Appendix B)

1. Determine the column with the interest rate.

2. Determine the row with the periods hence.

3. The column and row will intersect at the factor number.

4. To convert the single payment to its present value, multiply this

amount by the factor.

D. Present Value of an Annuity (Complete tables in Appendix B)

1. Determine the column with the interest rate.

2. Determine the row with the number of periods.

3. The column and row will intersect at the factor number.

4. To convert the annuity to its present value, multiply the annuity

amount by the factor.

E. Compounding Periods Shorter than a Year

1. Interest rates are generally stated as annual rates.

2. They can be allocated to shorter periods of time.

VIII. Effective Interest Amortization (Appendix 10B)

A Effective Interest Amortization of a Discount Bond

1. The straight-line method yields changes in the bonds’ carrying

value while the amount for bond interest expense remains

constant.

2. The effective interest method allocates total bond interest

expense over the bonds’ life in a way that yields a constant rate

of interest.

3. The key difference between the two methods lies in computing

bond interest expense. Instead of assigning an equal amount of

bond interest expense in each period, the effective interest

method assigns a bond interest expense amount that increases

over the life of a discount bond.

4. Both methods allocate the same amount of bond interest expense

to the bonds’ life, but in different patterns.

5. Except for differences in amounts, journal entries recording the

expense and updating the Discount on Bonds Payable account

balance are the same under both methods.

B Effective Interest Amortization of a Premium Bond

constant rate of interest.

2. Except for differences in amounts between the two methods (that

is, the straight-line and effective interest methods), journal

Chapter 10 – Long-Term Liabilities

Chapter Outline

Notes

entries recording the expense and updating the Premium on

Bonds Payable account are the same under both methods.

IX. Issuing Bonds Between Interest Dates (Appendix 10C)

A. Procedure used to simplify recordkeeping:

1. Buyers pay the purchase price plus any interest accrued since the

prior interest payment date.

2. This accrued interest is repaid to these buyers on the next

interest date.

3. Entry to record issuance of bonds between interest dates: debit

Cash, credit Interest Payable (for any interest accrued since the

prior interest payment date), credit Bonds Payable.

4. Entry to record first semiannual interest payment for bonds

issued between interest dates: debit Interest Payable (for amount

accrued in entry above), debit Interest Expense (for interest

accrued since issuance date), credit Cash.

B. Accruing Bond Interest Expense

1. Necessary when bond’s interest period does not coincide with

issuer’s accounting period.

2. Adjusting entry is necessary to record bond interest expense

accrued since the most recent interest payment and requires

amortization of the premium or discount for this period.

3. Affects the subsequent interest payment date entry.

X. Leases and Pensions (Appendix 10D)

A. Lease Liabilities

A lease is a contractual agreement between a lessor (asset owner)

and a lessee (asset renter or tenant) that grants the lessee the right to

use the asset for a period of time in return for cash (rent) payments.

1. Operating leases are short-term (or cancelable) leases in which

the lessor retains the risks and rewards of ownership.

a. Lessee records lease payments as expenses.

b. Lessor records lease payments as revenues.

2. Capital leases are long-term (or noncancelable) leases in which

the lessor transfers substantially all risks and rewards of

ownership to the lessee. The lease must meet any one of the four

following criteria:

d. Have present value of leased payments of 90% or more of

leased asset’s market value.

Chapter 10 – Long-Term Liabilities

Chapter Outline

Notes

Failure to meet one of the criteria results in off-balance-

sheet financing (not recorded on the balance sheet).

Capital leases are recorded as assets and liabilities. The asset

is depreciated. At each lease payment date, the liability is

amortized to record interest expense incurred.

B. Pension Liabilities

A pension plan is a contractual agreement between an employer and

its employees for the employer to provided benefits (payments) to

employees after they have retired.

1. Employer records their payment into pension plan as a debit to

Pension Expense and a credit to Cash.

2. Based on contracted benefits, pension plans can be overfunded

(resulting in plan assets) or underfunded (resulting in plan

liabilities).

Chapter 10 – Long-Term Liabilities

website, in whole or part. 10–13

Chapter 10 – Alternate Demonstration Problem #1

(Appendix 10B)

ABC Company issued $200,000 face value bonds on January 1, 2012 with

semiannual interest payments to be made on June 30 and December 31

at a contract rate of 10%. The bonds were scheduled to mature five years

after they were issued. ABC Company uses the effective interest method

of amortization.

On January 1, 2015, three years after the bonds were issued, the

company repurchased 40% of the outstanding bonds for $79,000.

Required:

Part A

1. Assume that the bonds were issued when the market rate of interest

was 9%. Prepare a schedule showing the bond interest expense and

amounts of amortization for the life of the bonds.

2. Prepare the journal entry to record the bond issuance.

3. Prepare journal entries for the first two interest payments.

4. Prepare the journal entry to recognize the partial repurchase of the

bonds.

Part B

Redo Part A under the assumption that the market rate on the bonds

when issued was 16%.

Chapter 10 – Long-Term Liabilities

Solution: Chapter 10 – Alternate Demonstration Problem #1

Part A

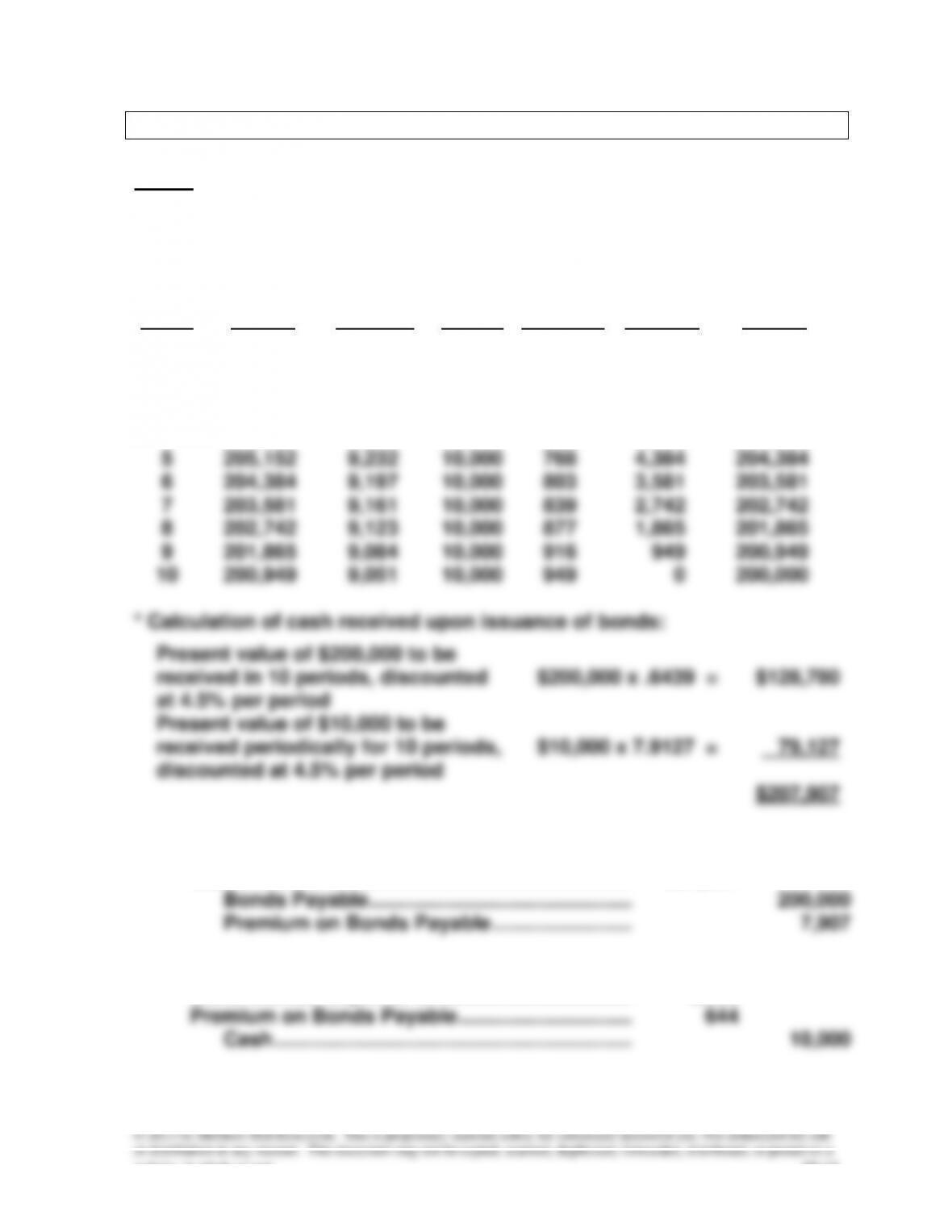

1.

Period

Beginning

of Period

Carrying

Amount

Interest

Expense

to be

Recorded

Interest

to be Paid

to Bond-

holders

Premium

to be

Amortized

Unamortized

Premium end

of Period

End-of–

Period

Carrying

Amount

0

$7,907

$207,907

*

1

$207,907

$9,356

$10,000

$644

7,263

207,263

2

207,263

9,327

10,000

673

6,590

206,590

3

206,590

9,297

10,000

703

5,887

205,887

4

205,887

9,265

10,000

735

5,152

205,152

5

205,152

9,232

10,000

768

4,384

204,384

6

204,384

9,197

10,000

803

3,581

203,581

7

203,581

9,161

10,000

839

2,742

202,742

8

202,742

9,123

10,000

877

1,865

201,865

9

201,865

9,084

10,000

916

949

200,949

10

200,949

9,051

10,000

949

0

200,000

Chapter 10 – Long-Term Liabilities

Solution: Chapter 10 – Alternate Demonstration Problem #1, continued

12/31/12

Bond Interest Expense …………………………………

9,327

Premium on Bonds Payable ………………………….

673

Cash ……………………………………………………….

10,000

4.

1/1/15

Bonds Payable ……………………………………………..

80,000

Premium on Bonds Payable ………………………….

1,432

Cash ……………………………………………………….

79,000

Gain on the Retirement of Bonds …………….

2,432

Part B

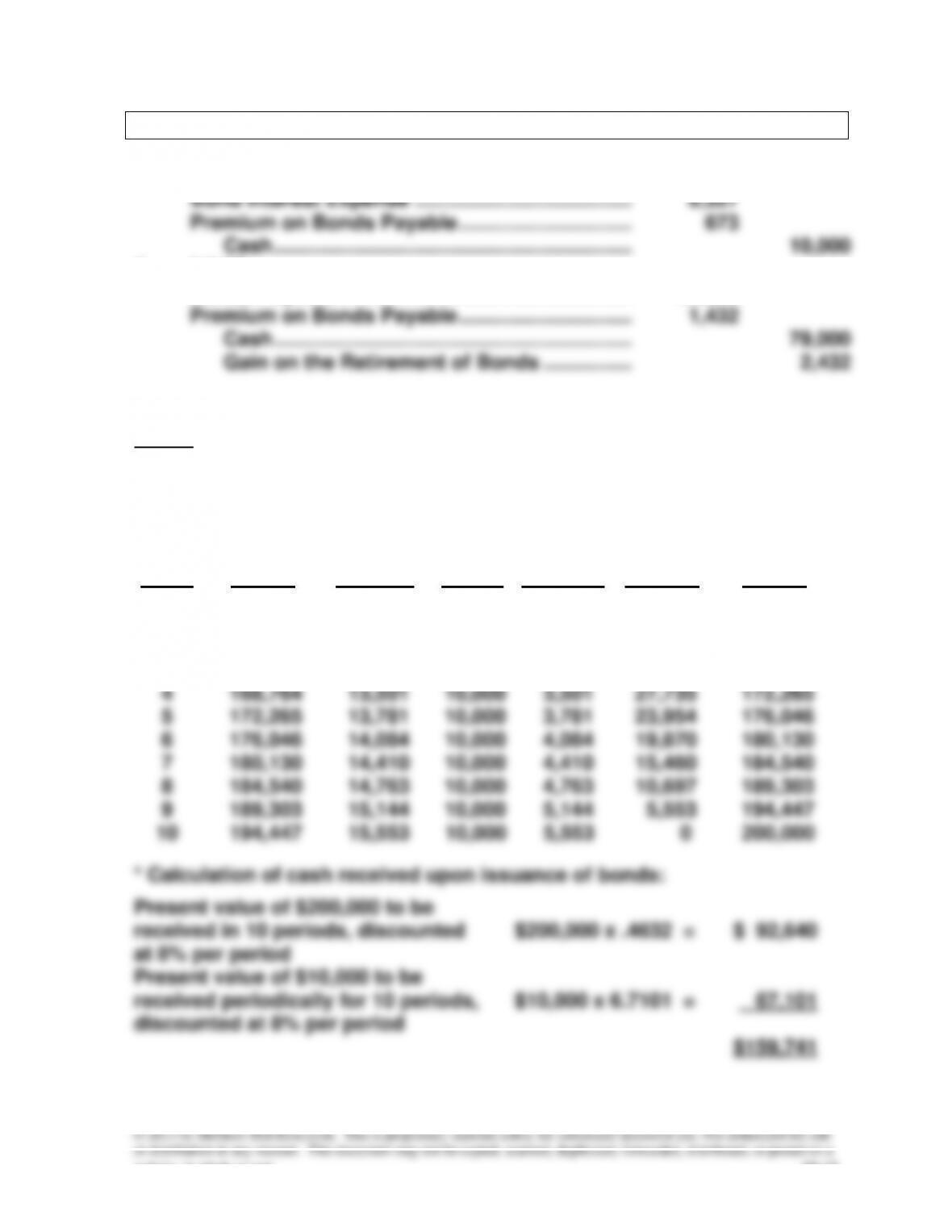

1.

Period

Beginning

of-Period

Carrying

Amount

Interest

Expense

to be

Recorded

Interest to

be Paid

to Bond-

holders

Discount

to be

Amortized

Unamortized

Discount end

of Period

End-of–

Period

Carrying

Amount

0

$40,259

$159,741

*

1

$159,741

$12,779

$10,000

$2,779

37,480

162,520

2

162,520

13,002

10,000

3,002

34,478

165,522

3

165,522

13,242

10,000

3,242

31,236

168,764

4

168,764

13,501

10,000

3,501

27,735

172,265

5

172,265

13,781

10,000

3,781

23,954

176,046

6

176,046

14,084

10,000

4,084

19,870

180,130

7

180,130

14,410

10,000

4,410

15,460

184,540

8

184,540

14,763

10,000

4,763

10,697

189,303

9

189,303

15,144

10,000

5,144

5,553

194,447

10

194,447

15,553

10,000

5,553

0

200,000

Chapter 10 – Long-Term Liabilities

website, in whole or part. 10–16

Solution: Chapter 10 – Alternate Demonstration Problem #1, continued

2.

1/1/12

Cash …………………………………………………………….

159,741

Discount on Bonds Payable ………………………….

40,259

Bonds Payable ………………………………………..

200,000

3.

6/30/12

Bond Interest Expense …………………………………

12,779

Discount on Bonds Payable …………………….

2,779

Cash ……………………………………………………….

10,000

4.

12/31/12

Bond Interest Expense …………………………………

13,002

Discount on Bonds Payable …………………….

3,002

Cash ……………………………………………………….

10,000

1/1/15

Bonds Payable ……………………………………………..

80,000

Loss on the Retirement of Bonds ………………….

6,948

Discount on Bonds Payable …………………….

7,948

Cash ……………………………………………………….

79,000