Student Name:

Class:

Part 1.

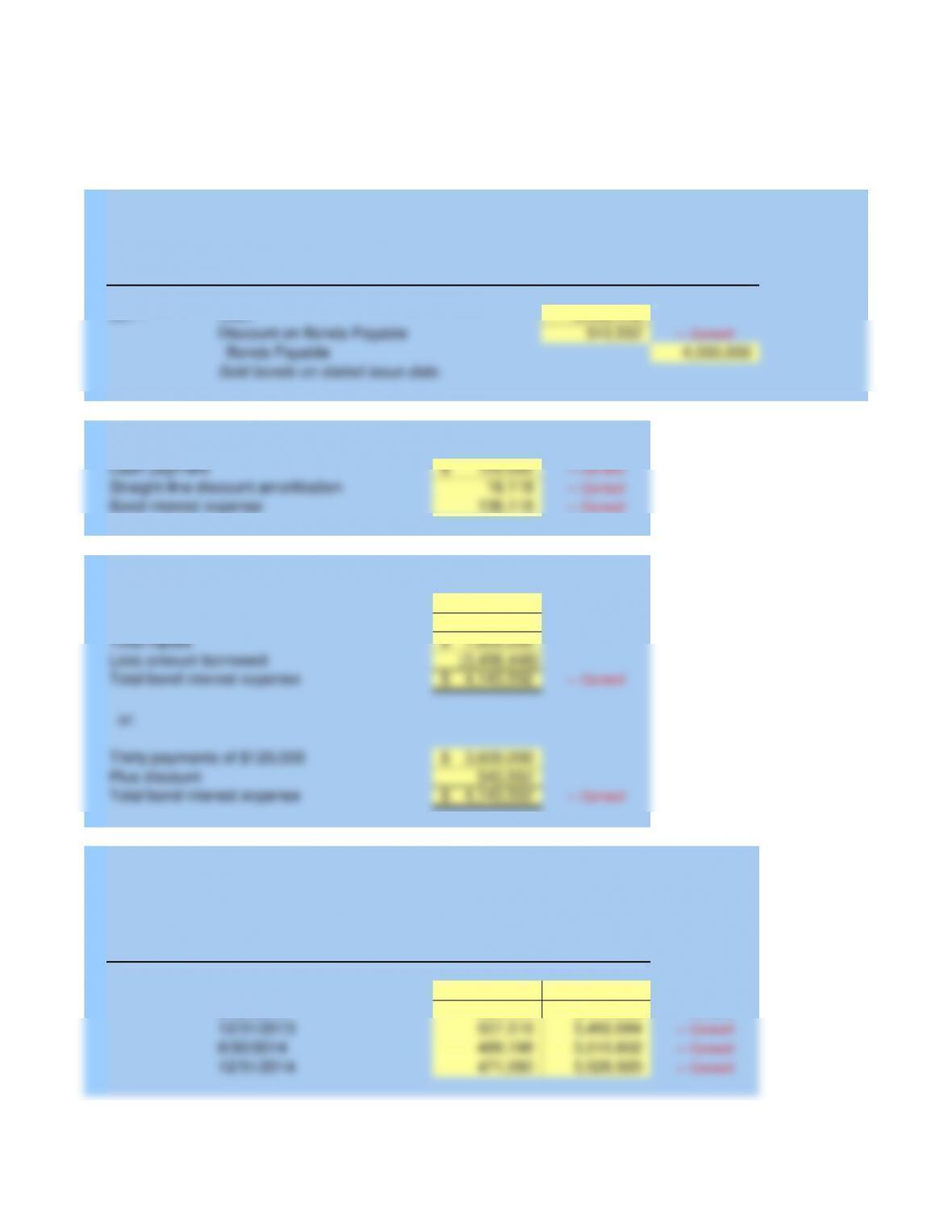

Date Account Titles Debit Credit

2013

Jan 1 3,456,448

543,552 «- Correct!

4,000,000

Part 2.

18,118 «- Correct!

138,118 «- Correct!

Part 3.

Par value at maturity

Thirty payments of $120,000

7,600,000$

(3,456,448)

Cash payment

4,143,552$ «- Correct!

4,143,552$ «- Correct!

Plus discount

Total bond interest expense

Thirty payments of $120,000

Total repaid

Less amount borrowed

Total bond interest expense

or:

Bonds Payable

Straight-line discount amortization

Bond interest expense

McGraw-Hill/Irwin

Instructor

General Journal

HILLSIDE

Problem 10-02A

Sold bonds on stated issue date.

Discount on Bonds Payable

Cash

Student Name:

Class:

McGraw-Hill/Irwin

Instructor

Problem 10-02A

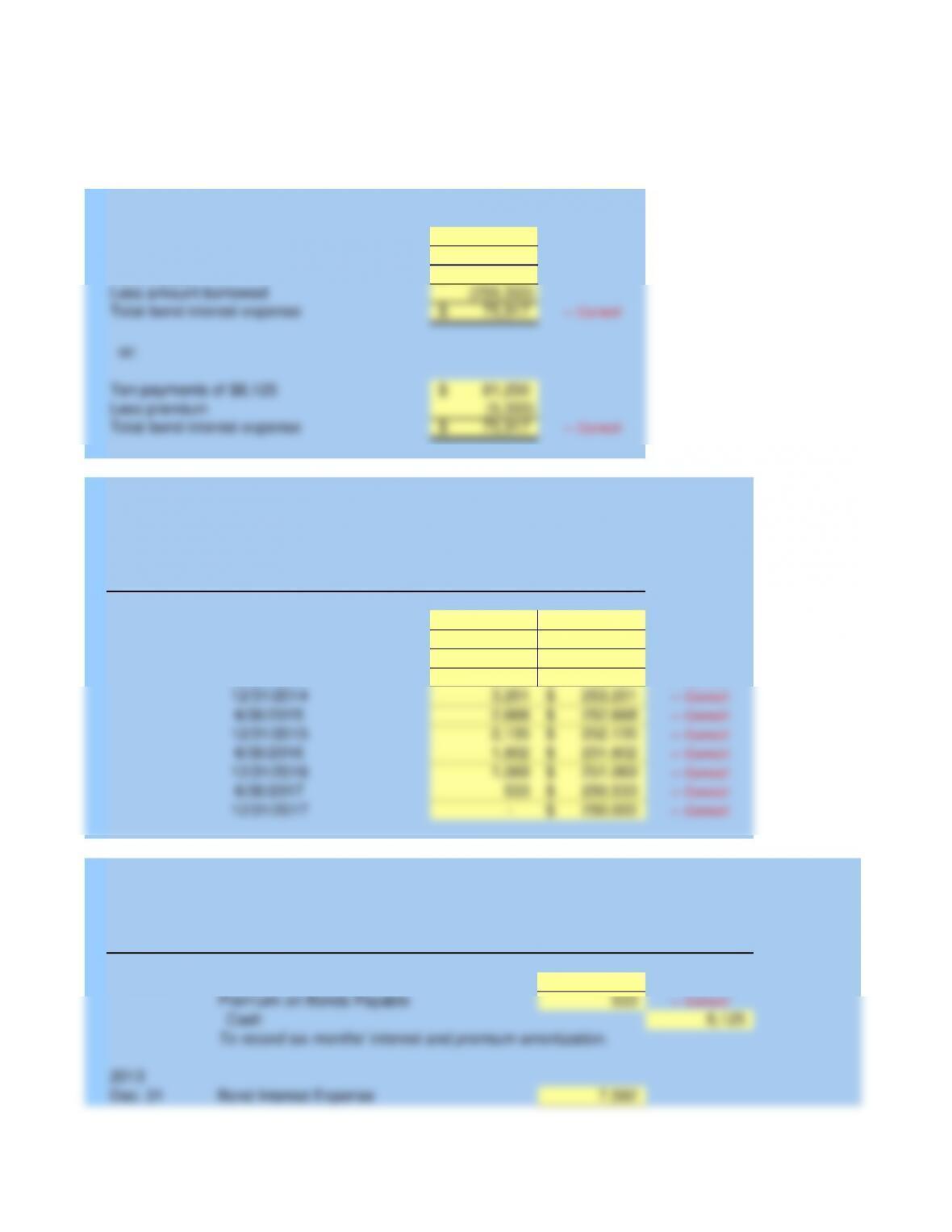

Part 5.

Date Account Titles Debit Credit

2013

Jun 30 138,118

18,118 «- Correct!

120,000 «- Correct!

2013

Dec 31 138,118

18,118 «- Correct!

120,000 «- Correct!

Discount on Bonds Payable

Cash

Bond Interest Expense

Discount on Bonds Payable

Cash

Bond Interest Expense

To record six months’ interest and discount amortization.

To record six months’ interest and discount amortization.

General Journal

HILLSIDE

4,000,000$

6%

15

3,456,448$

4,143,552$

3,528,920$

Given Data P10-02A:

HILLSIDE

(4) 12/31/2014 carrying value

(3)

Check figures:

Issuance price

Maturity in years

Annual interest

Bonds issued, face value

Student Name:

Class:

Part 1

81,250$

250,000

331,250$

(255,333)

75,917$ «- Correct!

81,250$

(5,333)

75,917$ «- Correct!

Part 2

Unamortized Carrying

Premium Value

5,333$ 255,333$ «- Correct!

4,800 254,800$ «- Correct!

4,267 254,267$ «- Correct!

3,734 253,734$ «- Correct!

3,201 253,201$ «- Correct!

2,668 252,668$ «- Correct!

2,135 252,135$ «- Correct!

1,602 251,602$ «- Correct!

1,069 251,069$ «- Correct!

533 250,533$ «- Correct!

– 250,000$ «- Correct!

Part 3

Date Account Titles Debit Credit

2013

June 30 7,592

533 «- Correct!

8,125

2013

Dec. 31 7,592

6/30/2016

12/31/2016

6/30/2014

12/31/2014

Straight-line Amortization Table

Semiannual Interest Period-End

1/1/2013

6/30/2015

12/31/2015

6/30/2013

12/31/2013

Less amount borrowed

Total bond interest expense

or:

Ten payments of $8,125

Less premium

Total bond interest expense

ELLIS

To record six months’ interest and premium amortization.

ELLIS

General Journal

Bond Interest Expense

Premium on Bonds Payable

Cash

6/30/2017

12/31/2017

Problem 10-04A

McGraw-Hill/Irwin

Instructor

Bond Interest Expense

Ten payments of $8,125

Par value at maturity

Total repaid

533 «- Correct!

8,125

To record six months’ interest and premium amortization.

Premium on Bonds Payable

Cash

250,000$

6.5%

5

255,333$

6%

252,668$

Given Data P10-04A:

Check figures:

(2) 6/30/2015 carrying value

Annual market rate on issue date

ELLIS

Bonds issued, par value

Annual interest

Maturity in years

Issuance price

Student Name:

Class:

Part 1.

Date Account Titles Debit Credit

2013

Jan 1 Cash 292,181

Discount on Bonds Payable 32,819 «- Correct!

Bonds Payable 325,000

Part 2.

65,000$

325,000

390,000$

(292,181)

97,819$ «- Correct!

65,000$

97,819$ «- Correct!

Total bond interest expense

Plus discount

Part 3.

Semiannual Cash Bond

Interest Interest Interest Discount Unamortized Carrying

Period-End Paid Expense Amortization Discount Value

1/1/2013 32,819$ 292,181$ «- Correct!

Total repaid

Less amount borrowed

Problem 10-07A

McGraw-Hill/Irwin

General Journal

LEGACY

Sold bonds on stated issue date.

Eight payments of $8,125

Par value at maturity

LEGACY

Eight payments of $8,125

Instructor

Total bond interest expense

or:

Part 4

Date Account Titles Debit Credit

2013

June 30 Bond Interest Expense 11,687

Discount on Bonds Payable 3,562

Cash 8,125 «- Correct!

2013

Dec. 31 Bond Interest Expense 11,830

Discount on Bonds Payable 3,705

Cash 8,125 «- Correct!

To record six months’ interest and discount amortization.

General Journal

LEGACY

To record six months’ interest and discount amortization.

325,000$

5%

4

292,181$

8%

97,819$

307,308$

Market interest rate

Given Data P10-07A:

Check figures:

(2)

LEGACY

(3) 12/31/2014 Carrying value

Bonds issued, face value

Annual interest

Maturity in years

Issuance price

Student Name:

Class:

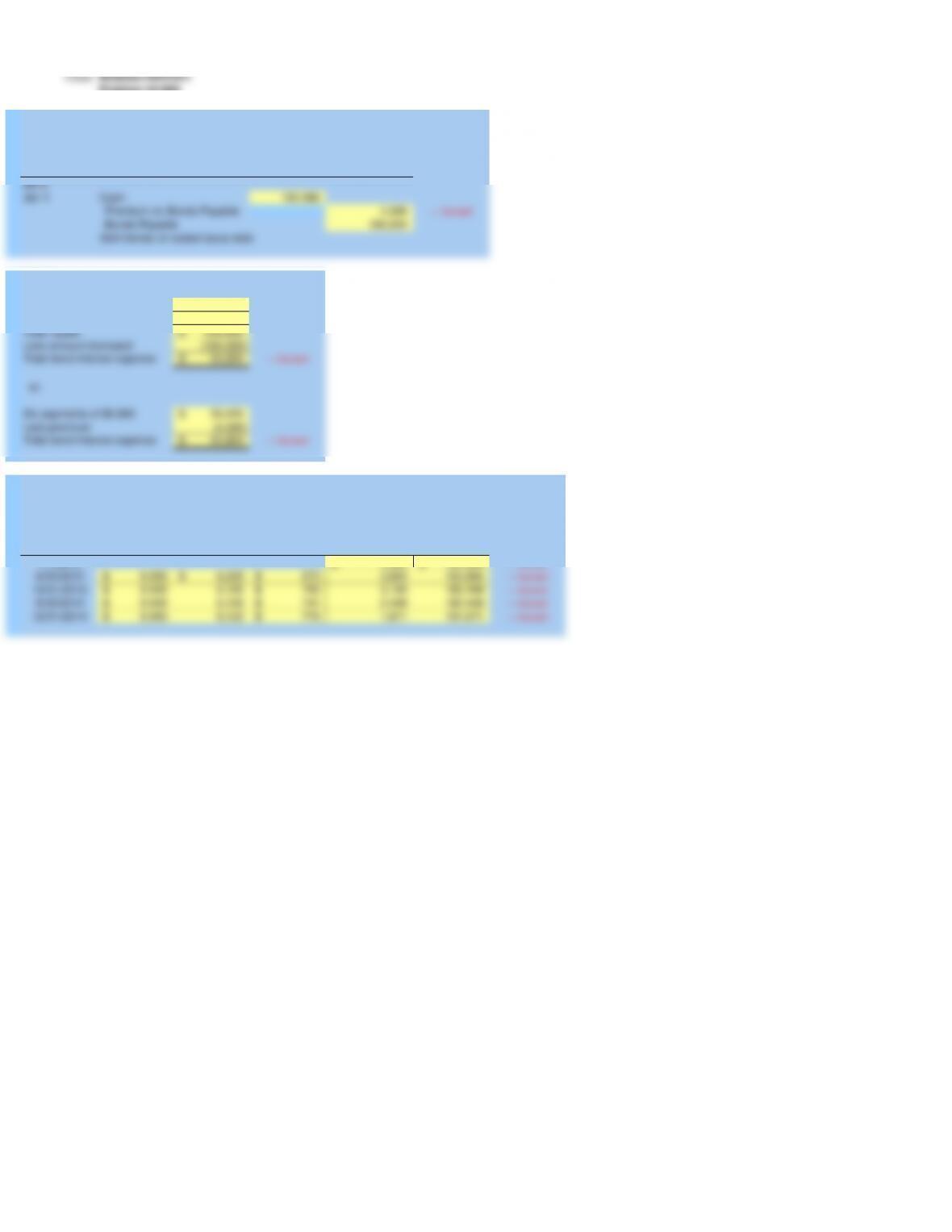

Part 1.

Date Account Titles Debit Credit

2013

Jan 1 184,566

4,566 «- Correct!

180,000

Part 2.

59,400$

180,000

239,400$

(184,566)

54,834$ «- Correct!

59,400$

(4,566)

54,834$ «- Correct!

Part 3.

Semiannual Cash Bond

Interest Interest Interest Premium Unamortized Carrying

Period-End Paid Expense Amortization Premium Value

1/1/2013 4,566$ 184,566$ «- Correct!

6/30/2013 9,900$ 9,228$ 672$ 3,894 183,894 «- Correct!

12/31/2013 9,900$ 9,195 705$ 3,189 183,189 «- Correct!

6/30/2014 9,900$ 9,159 741$ 2,448 182,448 «- Correct!

12/31/2014 9,900$ 9,122 778$ 1,671 181,671 «- Correct!

or:

Six payments of $9,900

Less premium

Total bond interest expense

LEGACY

Six payments of $9,900

Par value at maturity

Total repaid

Less amount borrowed

Total bond interest expense

McGraw-Hill/Irwin

Instructor

IKE

General Journal

Sold bonds on stated issue date.

Bonds Payable

Premium on Bonds Payable

Cash

Problem 10-08A

Part 4

Date Account Titles Debit Credit

2013

June 30 9,228

672

9,900 «- Correct!

2013

Dec. 31 9,195

705

9,900 «- Correct!

Part 5

Date Account Titles Debit Credit

2015

Jan. 1 180,000

1,671

176,400

5,271 «- Correct!

Cash

amounts reported on Ike’s financial statements.

10%. Without providing numbers, describe how this change affects the

Part 6: Assume that the market rate on January 1, 2013, is 12% instead of

General Journal

To record six months’ interest and premium amortization.

Premium on Bonds Payable

Gain on Retirement of Bonds

To record the retirement of bonds.

Bond Interest Expense

IKE

General Journal

Premium on Bonds Payable

Cash

Bonds Payable

Bond Interest Expense

Premium on Bonds Payable

Cash

IKE

To record six months’ interest and premium amortization.

If the market rate on the issue date had been 12% instead of 10%, the bonds

would have sold at a discount because the contract rate of 11% would have been

lower than the market rate. This change would affect the balance sheet because

the bond liability would be smaller (par value minus a discount instead of par

value plus a premium). As the years passed, the bond liability would increase

with amortization of the discount instead of decreasing with amortization of the

premium. The income statement would show larger amounts of bond interest

expense over the life of the bonds issued at a discount than it would show if the

bonds had been issued at a premium. The statement of cash flows would show

a smaller amount of cash received from borrowing. However, the cash flow

statements presented over the life of the bonds (after issuance) would report the

same total amount of cash paid for interest. This amount is fixed as it is the

product of the contract rate and the par value of the bonds and is unaffected by

the change in the market rate.

180,000$

11%

3

184,566$

10%

182,448$

5,270$

(5) Gain

IKE

(3) 6/30/2014 Carrying value

Bonds issued, face value

Annual interest

Maturity in years

Issuance price

Market interest rate

Given Data P10-08A:

Check figures: